2. Amend paragraphs 323-740-05-2 through 05-3, 323-740-15-3, 323-740-25-1 through 25-2, 323-740-25-4 through 25-5, 323-740-30-1, 323-740-35-1 through 35-3, and 323-740-45-1 through 45-2 and add paragraphs 323-740-25-1A through 25-1C and 323-740-35-4 through 35-6, with a link to transition paragraph 323-740-65-1, as follows:

Investments—Equity Method and Joint Ventures—Income Taxes

Overview and Background

Qualified Affordable Housing Project Investments

323-740-05-2 The Qualified Affordable Housing Project Investments Subsections provide income tax accounting guidance on a specific type of investment in real estate. This guidance applies to investments in limited

partnerships

liability entities that

operate

manage or invest in qualified affordable housing projects

and are flow-through entities for tax purposes.

323-740-05-3 The following discussion refers to and describes a provision within the Revenue Reconciliation Act of 1993; however, it shall not be considered a definitive interpretation of any provision of the Act for any purpose. The Revenue Reconciliation Act of 1993, enacted in August 1993, retroactively extended and made permanent the affordable housing credit. Investors in entities

operating

that manage or invest in qualified affordable housing projects receive tax benefits in the form of tax deductions from operating losses and tax credits. The tax credits are allowable on the tax return each year over a 10-year period as a result of renting a sufficient number of units to qualifying tenants and are subject to restrictions on gross rentals paid by those tenants. These credits are subject to recapture over a 15-year period starting with the first year tax credits are earned. Corporate investors generally purchase an interest in a limited

partnership

liability entity that

operates

manages or invests in the qualified affordable housing projects.

Scope and Scope Exceptions

Qualified Affordable Housing Project Investments

> Transactions

323-740-15-3 The guidance in the Qualified Affordable Housing Project Investments Subsections applies to

reporting entities that are investors investments

in

limited partnerships that operate

qualified affordable housing projects

through limited liability entities that are flow-through entities for tax purposes.

Recognition

Qualified Affordable Housing Project Investments

323-740-25-1 An

A reporting entity that invests in a qualified affordable housing

project

projects through

a

limited

partnership investment

liability entities (that is, the investor) may elect to account for

the investment

those investments using the

effective yield

proportional amortization method (described in paragraphs 323-740-35-2 and 323-740-45-2) provided all of the following conditions are met:

a.

The availability (but not necessarily the realization) of the tax credits allocable to the investor is guaranteed by a creditworthy entity through a letter of credit, a tax indemnity agreement, or another similar arrangement.

It is probable that the tax credits allocable to the investor will be available. aa. The investor does not have the ability to exercise significant influence over the operating and financial policies of the limited liability entity.

aaa. Substantially all of the projected benefits are from tax credits and other tax benefits (for example, tax benefits generated from the operating losses of the investment).

b. The investor's projected yield based solely on the cash flows from the

guaranteed

tax credits

and other tax benefits is positive.

c. The investor is a limited

liability investor partner

in the

affordable housing project

limited liability entity for both legal and tax

purposes

purposes, and the investor's liability is limited to its capital investment.

323-740-25-1A In determining whether an investor has the ability to exercise significant influence over the operating and financial policies of the limited liability entity, a reporting entity shall consider the indicators of significant influence in paragraphs 323-10-15-6 through 15-7.

323-740-25-1B Other transactions between the investor and the limited liability entity (for example, bank loans) shall not be considered when determining whether the conditions in paragraph 323-740-25-1 are met, provided that all three of the following conditions are met:

- The reporting entity is in the business of entering into those other transactions (for example, a financial institution that regularly extends loans to other projects).

- The terms of those other transactions are consistent with the terms of arm's-length transactions.

- The reporting entity does not acquire the ability to exercise significant influence over the operating and financial policies of the limited liability entity as a result of those other transactions.

323-740-25-1C At the time of the initial investment, a reporting entity shall evaluate whether the conditions in paragraphs 323-740-25-1 through 25-1B have been met to elect to apply the proportional amortization method on the basis of facts and circumstances that exist at that time. A reporting entity shall subsequently reevaluate the conditions upon the occurrence of either of the following:

- A change in the nature of the investment (for example, if the investment is no longer in a flow-through entity for tax purposes)

- A change in the relationship with the limited liability entity that could result in the reporting entity no longer meeting the conditions in paragraphs 323-740-25-1 through 25-1B.

323-740-25-2 For

a limited partnership

an investment in a qualified affordable housing project

through a limited liability entity not accounted for using the

effective yield

proportional amortization method, the investment shall be accounted for in accordance with Subtopic 970-323. In accounting for such an investment under that Subtopic, the requirements

in paragraphs 323-740-25-3 through 25-5 and paragraphs 323-740-50-1 through 50-2 of this Subsection

that are not related to the

effective yield

proportional amortization method

, shall be applied.

323-740-25-3 A liability shall be recognized for delayed equity contributions that are unconditional and legally binding. A liability also shall be recognized for equity contributions that are contingent upon a future event when that contingent event becomes probable. Topic 450 and paragraph 840-30-55-15 provide additional guidance on the accounting for delayed equity contributions.

323-740-25-4 The decision to apply the

effective yield

proportional amortization method of accounting is an accounting policy decision

to be applied consistently to all investments in qualified affordable housing projects that meet the conditions in paragraph 323-740-25-1 rather than a decision to be applied to individual investments that qualify for use of the

effective yield

proportional amortization method.

323-740-25-5 At the time of initial investment, immediate Immediate

recognition

at the time the investment is purchased

of the entire benefit of the tax credits to be received during the term of

a limited partnership

an investment in a qualified affordable housing project is not appropriate (that is, affordable housing credits shall not be recognized in the financial statements before their inclusion in the investor's tax return).

Initial Measurement

Qualified Affordable Housing Project Investments

323-740-30-1 Paragraph 323-740-25-5 prohibits immediate recognition of tax credits, at the time of

initial investment, for the entire benefit of tax credits to be received during the term of

a limited partnership

an investment in a qualified affordable housing project. See paragraph 323-740-35-2 for the required subsequent measurement calculation methodology when an entity uses the

effective yield

proportional amortization method of accounting for

a limited partnership

an investment in a qualified affordable housing project

through a limited liability entity.

Subsequent Measurement

Qualified Affordable Housing Project Investments

323-740-35-1 This guidance addresses the methodology for measuring

the periodic net benefit of an affordable housing tax credit when a limited partnership

an investment in a qualified affordable housing project

through a limited liability entity that is accounted for using the

effective yield

proportional amortization method.

323-740-35-2 Under the

effective yield

proportional amortization method, the investor

recognizes tax credits as they are allocated and

amortizes the initial cost of the investment

to provide a constant effective yield over the period that

in proportion to the tax credits

and other tax benefits are

allocated to the investor.

The amortization amount shall be calculated as follows:

- The initial investment balance less any expected residual value of the investment, multiplied by

- The percentage of actual tax credits and other tax benefits allocated to the investor in the current period divided by the total estimated tax credits and other tax benefits expected to be received by the investor over the life of the investment.

The effective yield is the internal rate of return on the investment, based on the cost of the investment and the guaranteed tax credits allocated to the investor. Any expected residual value of the investment shall be excluded from the effective yield calculation. Cash received from operations of the limited partnership or sale of the property, if any, shall be included in earnings when realized or realizable.

323-740-35-3 Example 1 (see paragraph 323-740-55-2) illustrates the application of accounting guidance to a limited

liability partnership

investment in a qualified affordable housing project using the cost, equity, and

effective yield

proportional amortization methods.

323-740-35-4 As a practical expedient, an investor is permitted to amortize the initial cost of the investment in proportion to only the tax credits allocated to the investor if the investor reasonably expects that doing so would produce a measurement that is substantially similar to the measurement that would result from applying the requirement in paragraph 323-740-35-2.

323-740-35-5 Any expected residual value of the investment shall be excluded from the proportional amortization calculation. Cash received from operations of the limited liability entity shall be included in earnings when realized or realizable. Gains or losses on the sale of the investment, if any, shall be included in earnings at the time of sale.

323-740-35-6 An investment in a qualified affordable housing project through a limited liability entity shall be tested for impairment when events or changes in circumstances indicate that it is more likely than not that the carrying amount of the investment will not be realized. An impairment loss shall be measured as the amount by which the carrying amount of an investment exceeds its fair value. A previously recognized impairment loss shall not be reversed.

Other Presentation Matters

Qualified Affordable Housing Project Investments

323-740-45-1 This guidance addresses the income statement presentation of the affordable housing tax credit when

a limited partnership

an investment in a qualified affordable housing project

through a limited liability entity is accounted for using the

effective yield

proportional amortization method.

323-740-45-2 Under the

effective yield

proportional amortization method,

the tax credit allocated, net of

the amortization of the investment in the limited

partnership

,

liability entity is recognized in the income statement as a component of

income taxes

income tax expense (or benefit).attributable to continuing operations. Any

The other

current tax expense (or benefit) tax benefits received

shall be accounted for pursuant to the general requirements of Topic 740.

3. Add paragraphs 323-740-50-1 through 50-2 and their Subsection title, with a link to transition paragraph 323-740-65-1, as follows:

Disclosure

Qualified Affordable Housing Project Investments

323-740-50-1 A reporting entity that invests in a qualified affordable housing project shall disclose information that enables users of its financial statements to understand the following:

a. The nature of its investments in qualified affordable housing projects

b. The effect of the measurement of its investments in qualified affordable housing projects and the related tax credits on its financial position and results of operations.

323-740-50-2 To meet the objectives in the preceding paragraph, a reporting entity may consider disclosing the following:

a. The amount of affordable housing tax credits and other tax benefits recognized during the year

b. The balance of the investment recognized in the statement of financial position

c. For qualified affordable housing project investments accounted for using the proportional amortization method, the amount recognized as a component of income tax expense (benefit)

d. For qualified affordable housing project investments accounted for using the equity method, the amount of investment income or loss included in pretax income

e. Any commitments or contingent commitments (for example, guarantees or commitments to provide additional capital contributions), including the amount of equity contributions that are contingent commitments related to qualified affordable housing project investments and the year or years in which contingent commitments are expected to be paid

f. The amount and nature of impairment losses during the year resulting from the forfeiture or ineligibility of tax credits or other circumstances. For example, those impairment losses may be based on actual property-level foreclosures, loss of qualification due to occupancy levels, compliance issues with tax code provisions, or other issues.

4. Amend paragraphs 323-740-55-2 through 55-5 and paragraphs 323-740-55-7 through 55-8 and supersede paragraphs 323-740-55-6 and 323-740-55-10, with a link to transition paragraph 323-740-65-1, as follows:

Implementation Guidance and Illustrations

Qualified Affordable Housing Project Investments

323-740-55-1 This Section is an integral part of the requirements of this Subtopic.

> Illustrations

> > Example 1: Application of Accounting Guidance to a Limited Liability Partnership

Investment in a Qualified Affordable Housing Project

323-740-55-2 This Example

demonstrates

illustrates the application of the cost, equity, and

effective yield

proportional amortization methods of accounting for a limited

partnership

liability investment in a qualified affordable housing project.

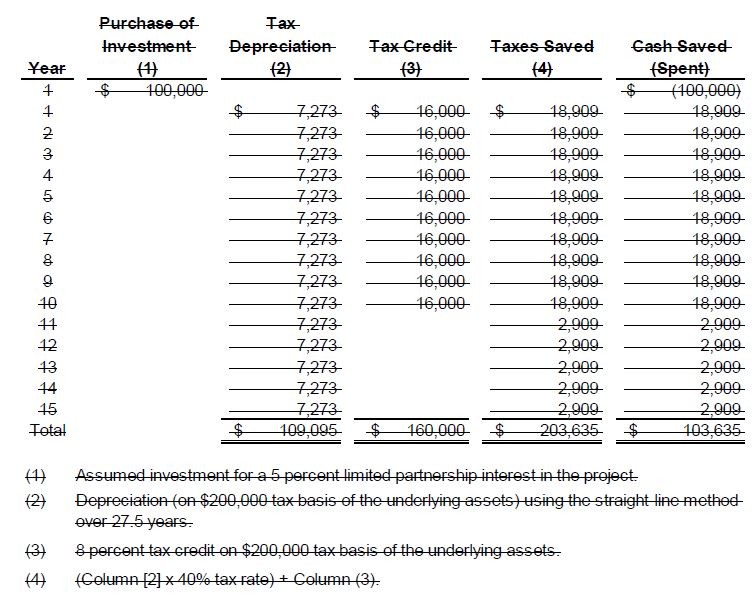

323-740-55-3 The following are the terms for this Example.

323-740-55-4 This Example has the following assumptions:

- All cash flows (except initial investment) occur at the end of each year.

- Depreciation expense is computed, for book and tax purposes, using the straight-line method with a 27.5 year life (the same method is used for simplicity).

- The {remove glossary link}investor{remove glossary link} made a $100,000 investment for a 5 percent limited partnership interest in the project at the beginning of the first year of eligibility for the tax credit.

- The partnership finances the project cost of $4,000,000 with 50 percent equity and 50 percent debt.

- The annual tax credit allocation (equal to

8

4 percent of the project's original cost) will be received for a period of 10 years.

- The investor's tax rate is 40 percent.

- The project will operate with break-even pretax cash flows including debt service during the first 15 years of operations.

- The project's taxable

and book

loss will be equal to depreciation expense. The cumulative book loss (and thus the cumulative depreciation expense) recognized by the investor under the equity method of accounting

is limited to the $100,000 investment.

- Subparagraph superseded by Accounting Standards Update 2014-01.

Deferred taxes are provided for the difference between the book and tax bases of the investment. Deferred taxes are provided for losses in excess of the at-risk investment.

The investor will maintain the investment for 15 years (so there will be no recapture of tax credits).

It is assumed that all requirements are met to retain allocable tax credits so there will be no recapture of tax credits.- The investor expects that the estimated residual value of the investment will be zero.

Under the effective yield method, a letter of credit or similar guarantee exists

All of the conditions described in paragraph 323-740-25-1 are met to qualify the investment for the use of the effective yield

proportional amortization method.

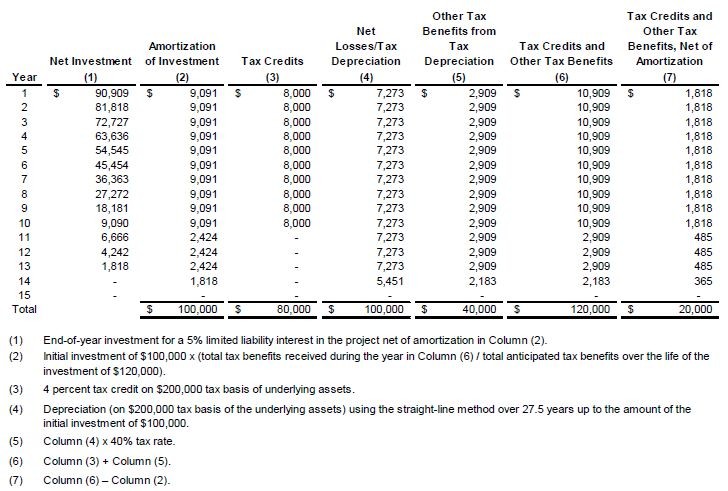

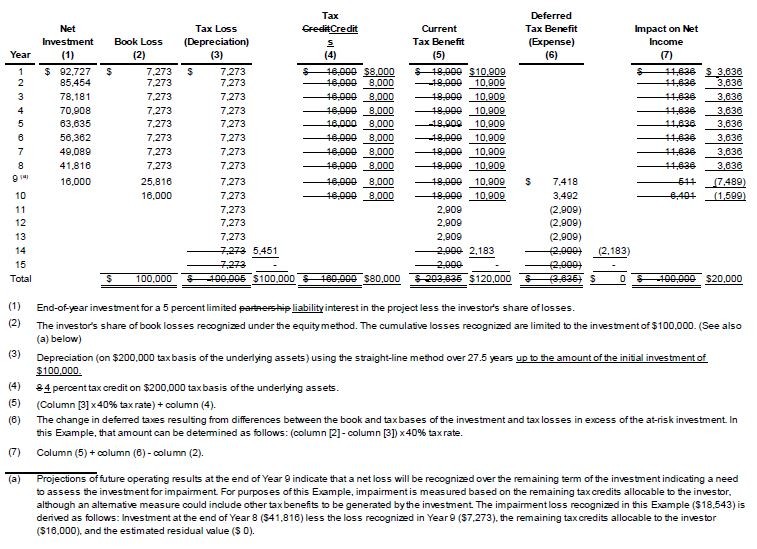

323-740-55-5 The investor's cash flow analysis follows

An analysis of the proportional amortization method follows.

[For ease of readability, the table is not underlined as new text.]

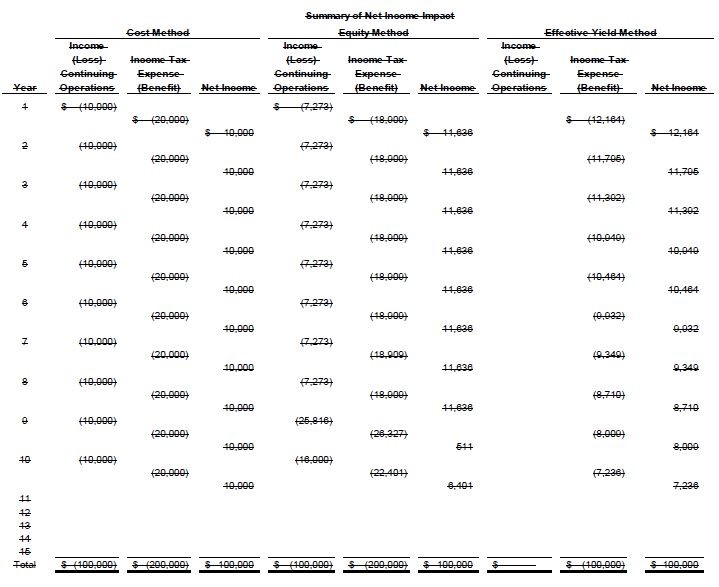

323-740-55-6 Paragraph superseded by Accounting Standards Update 2014-01.A summary of the net income effect of the cost, equity, and effective yield methods follows. This summary is based on the detailed analyses of the cost method with amortization, the equity method, and the effective yield method, which appear after the following summary.

323-740-55-7 A detailed analysis of the cost method with amortization follows.

323-740-55-8 A detailed analysis of the equity method follows.

323-740-55-9 This Example is but one method for recognition and measurement of impairment of an investment accounted for by the equity method. Inclusion of this method in this Example does not indicate that it is a preferred method.

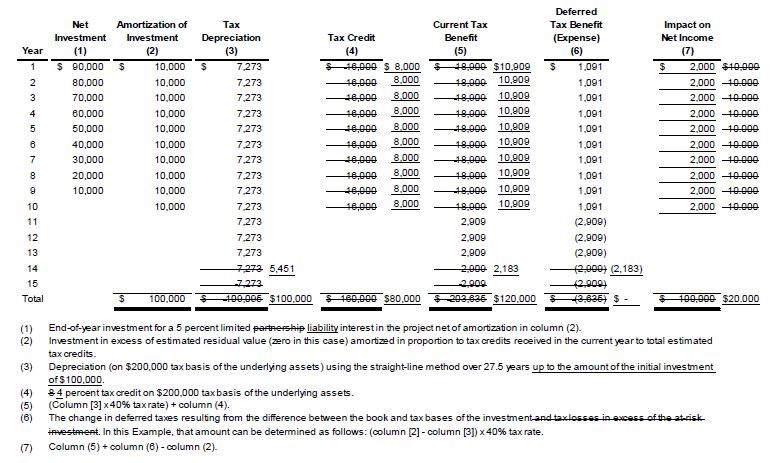

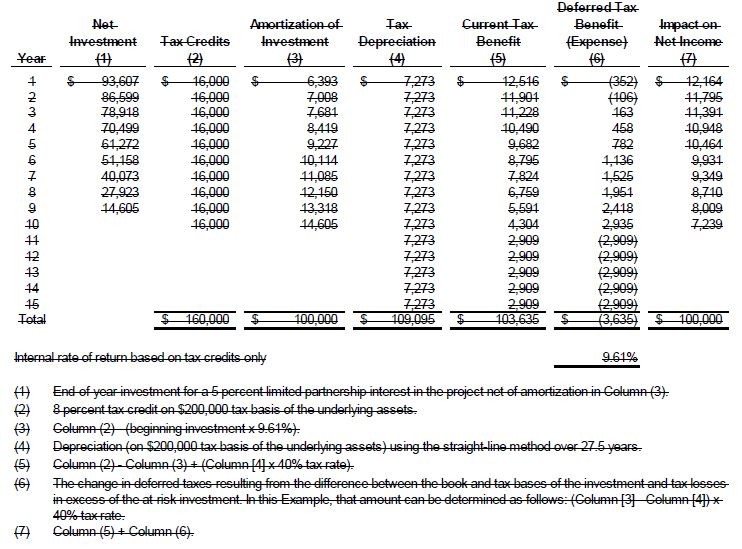

323-740-55-10 Paragraph superseded by Accounting Standards Update 2014-01.A detailed analysis of the effective yield method follows.

5. Add paragraph 323-740-65-1 and its related heading as follows:

> Transition Related to Accounting Standards Update No. 2014-01, Investments—Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects

323-740-65-1 The following represents the transition and effective date information related to Accounting Standards Update No. 2014-01, Investments— Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects:

- The pending content that links to this paragraph shall be effective for public business entities for annual periods and interim reporting periods within those annual periods, beginning after December 15, 2014. For all entities other than public business entities, the amendments shall be effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015.

- A reporting entity shall apply the pending content that links to this paragraph retrospectively to all periods presented. A reporting entity that uses the effective yield method to account for its investments in qualified affordable housing projects before the date of adoption of the pending content that links to this paragraph may continue to apply the effective yield method for those preexisting investments.

- Early application of the pending content that links to this paragraph is permitted.

- An entity shall provide the disclosures in paragraphs 250-10-50-1 through 50-2 in the period the entity adopts the pending content that links to this paragraph.

6. Amend paragraph 323-740-00-1 as follows:

323-740-00-1 The following table identifies the changes made to this Subtopic. No updates have been made to this subtopic.

Paragraph Number |

Action |

Accounting Standards Update |

Date |

Current Tax Expense (or Benefit) |

Added |

2014-01 |

01/15/2014 |

Income Taxes |

Superseded |

2014-01 |

01/15/2014 |

Income Tax Expense (or Benefit) |

Added |

2014-01 |

01/15/2014 |

Investor |

Superseded |

2014-01 |

01/15/2014 |

Public Business Entity |

Added |

2014-01 |

01/15/2014 |

323-740-05-2 |

Amended |

2014-01 |

01/15/2014 |

323-740-05-3 |

Amended |

2014-01 |

01/15/2014 |

323-740-15-3 |

Amended |

2014-01 |

01/15/2014 |

323-740-25-1 |

Amended |

2014-01 |

01/15/2014 |

323-740-25-1A through 25-1C |

Added |

2014-01 |

01/15/2014 |

323-740-25-2 |

Amended |

2014-01 |

01/15/2014 |

323-740-25-4 |

Amended |

2014-01 |

01/15/2014 |

323-740-25-5 |

Amended |

2014-01 |

01/15/2014 |

323-740-30-1 |

Amended |

2014-01 |

01/15/2014 |

323-740-35-1 through 35-3 |

Amended |

2014-01 |

01/15/2014 |

323-740-35-4 through 35-6 |

Added |

2014-01 |

01/15/2014 |

323-740-45-1 |

Amended |

2014-01 |

01/15/2014 |

323-740-45-2 |

Amended |

2014-01 |

01/15/2014 |

323-740-50-1 |

Added |

2014-01 |

01/15/2014 |

323-740-50-2 |

Added |

2014-01 |

01/15/2014 |

323-740-55-2 through 55-5 |

Amended |

2014-01 |

01/15/2014 |

323-740-55-6 |

Superseded |

2014-01 |

01/15/2014 |

323-740-55-7 |

Amended |

2014-01 |

01/15/2014 |

323-740-55-8 |

Amended |

2014-01 |

01/15/2014 |

323-740-55-10 |

Superseded |

2014-01 |

01/15/2014 |

323-740-65-1 |

Added |

2014-01 |

01/15/2014 |

View table

The amendments in this Update were adopted by the unanimous vote of the seven members of the Financial Accounting Standards Board:

Russell G. Golden, Chairman

James L. Kroeker, Vice Chairman

Daryl E. Buck

Thomas J. Linsmeier

R. Harold Schroeder

Marc A. Siegel

Lawrence W. Smith