BC14. The Task Force reached a consensus that all plans (that is, both plans with a divided interest and plans with an undivided interest) should disclose the dollar amount of the plan’s interest in each general type of investment held by the master trust, which supplements the existing requirement to disclose the master trust’s balances in each general type of investment. The Task Force did not intend for the examples of general types of investments included within this Update to be considered a prescriptive, all-inclusive list of categories that a plan may utilize.

BC15. The Task Force understands that because more of today’s plans have divided interests due to participant-directed investments, the current requirement to disclose the plan’s total percentage interest in the master trust may not appropriately reflect the dollar amount of the plan’s interest in each general type of investment that is held by the master trust. As such, most stakeholders indicated, and the Task Force ultimately agreed, that the current disclosure could be misleading for plans with a divided interest.

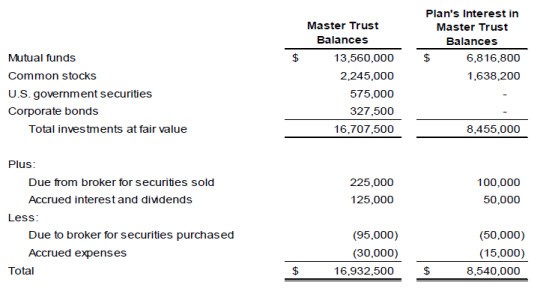

BC16. While the amendments in the proposed Update would have required the disclosure of the dollar amount of the plan’s interest in each general type of investment held by the master trust for only plans with a divided interest in the master trust, this Update requires that same disclosure for all plans. This is because some stakeholders noted an inconsistency in the proposed amendments whereby plans with an undivided interest would not be required to disclose the dollar amount of the plan’s interest in each general type of investment held by the master trust but would be required to disclose the dollar amount of the plan’s interest in the master trust’s other assets and liabilities as discussed in paragraph BC17 below. The Task Force ultimately decided to require that all plans disclose the dollar amount of the plan’s interest in each general type of investment held by the master trust because the disclosure would improve transparency for users by providing greater insight about the types of investments held by the plan and the associated dollar amount of the plan’s interest held in those investments. The Task Force understands that the cost of providing this disclosure would not be burdensome because much of the work of identifying the dollar amount of the plan’s interest in each general type of investment held by the master trust is currently done for purposes of having the plan’s interest in the master trust audited. While some stakeholders questioned whether the disclosure would be necessary for plans with an undivided interest, the Task Force noted that there is no conceptual basis for plans with an undivided interest to disclose the dollar amount of their interest in the master trust’s other assets and liabilities but not disclose the dollar amount of their interest in the general type of investments held by the master trust. In addition, the Task Force notes that not distinguishing between plans with a divided interest and plans with an undivided interest is consistent with the regulatory reporting requirements.

BC17. The Task Force also reached a consensus to require that all plans (that is, plans with a divided interest and plans with an undivided interest) disclose the master trust’s other assets and liabilities, as well as the dollar amount of the plan’s interest in each of those other assets and liabilities. The Task Force understands that the current disclosure requirements do not provide insight into all of the balances in the master trust’s statement of net assets, which make up the plan’s interest in the master trust. That is, the current disclosures focus only on the investments. As such, the Task Force decided that the master trust’s other assets and liabilities and the dollar amount of the plan’s interest in each of those other assets and liabilities also should be disclosed for all plans. The Task Force understands that the information is useful at the master trust level, provides information about the legal structure that is the master trust, and facilitates the regulator’s ability to reconcile the disclosure with the master trust’s Form 5500 regulatory filing under the Employee Retirement Income Security Act of 1974 (ERISA). The Task Force also concluded that the dollar amount of the plan’s interest in each of the master trust’s other assets and liabilities is useful because it helps a user better understand the amounts included in the plan’s interest in the master trust that is presented in the plan’s statement of net assets available for benefits. Lastly, this Update does not provide prescriptive guidance on how the other assets and liabilities should be disaggregated; instead, the amendments in this Update provide examples of other assets and liabilities that may be included, which allows plans to use judgment and provide the disclosure based on their specific facts and circumstances.

BC18. The Task Force decided not to require that plans disclose the master trust’s statement of net assets available for benefits and the statement of changes in net assets available for benefits. The Task Force concluded that much of the same information will be provided through other amendments in this Update, which will be less costly and will provide more targeted information to users. As such, the Task Force did not believe the benefits would justify the costs.

BC19. The Task Force also decided not to specify in situations in which financial statements were being prepared for the master trust, rather than for a specific plan, whether master trust financial statements should follow investment company or employee benefit plan guidance—or some combination of the two. The Task Force noted that while it agreed that the simplifications provided for employee benefit plans during the Board’s simplification initiative in 2015 (including presentation of fully-benefit-responsive investment contracts at contract value, and providing investment disclosures by general type of investment as opposed to nature, characteristics, and risks) should be considered for master trusts, it did not believe that issue was within the scope of this project.

BC20. Although GAAP does not currently require disclosures for the underlying investments held by a master trust (for example, disclosures in Topics 815 and 820), the Task Force understands that the majority of plans provide these disclosures on the basis of nonauthoritative guidance. This nonauthoritative guidance includes (a) AICPA Technical Practice Aid TIS Section 6931.11, Fair Value Measurement Disclosures for Master Trusts, and (b) the AICPA Audit and Accounting Guide, Employee Benefit Plans. While some Task Force members said that explicit GAAP requirements should be provided, other Task Force members said that there was no need for standard setting in this area. Ultimately, the Task Force decided not to address this issue, noting that it does not appear to be a significant current practice issue for which standard setting is warranted and there is no intent to change current practice.

BC21. Some stakeholders recommended that a plan be required to disclose whether its interest in a master trust is divided or undivided. However, the Task Force understands that this information is typically included as part of the disclosure requirement to provide a description of the basis used to allocate net assets and total investment income, which is in paragraphs 960-325-50-8, 962-325-50-8, and 965-325-50-6 of this Update. As such, the Task Force noted that when complying with the guidance in those paragraphs, the structure of the plan (that is, divided or undivided) is an important consideration to disclose.

BC22. Lastly, the Task Force reached a consensus that a health and welfare benefit plan is not required to provide investment disclosures (for example, the disclosures required by Topics 815 and 820) for 401(h) account assets because those disclosures are provided within the defined benefit pension plan financial statements. The Task Force understands that the defined benefit pension plan legally owns the 401(h) account assets. Therefore, the health and welfare benefit plan’s interest is that of a receivable from the defined benefit pension plan, not an investment. Furthermore, the Task Force notes that including the investment disclosures in the defined benefit pension plan financial statements more closely aligns with regulatory reporting requirements. As such, the Task Force sees no need to require the same investment disclosures within multiple financial statements; however, the Task Force also reached a consensus to require disclosure of the defined benefit pension plan name within the health and welfare benefit plan’s financial statements so that all users can access the disclosure information relating to the 401(h) account assets, if desired.