25. Amend paragraphs 718-20-05-1 and 718-20-15-2, with a link to transition paragraph 718-10-65-11, as follows:

Compensation—Stock Compensation—Awards classified as Equity

Overview and Background

718-20-05-1 Share-based payment awards

to employees

may be classified as either equity or liabilities. This Subtopic deals with instruments classified as equity. It is interrelated with Subtopic 718-10, which contains guidance applicable to instruments classified as either equity or liabilities issued in

share-based payment transactions. It may also be necessary in some cases to refer to the guidance contained in Subtopic 718-30.

Scope and Scope Exceptions

> Overall Guidance

718-20-15-1 This Subtopic follows the same Scope and Scope Exceptions as outlined in the Overall Subtopic, see Section 718-10-15, with specific transaction qualifications noted below.

> Transactions

718-20-15-2 The guidance in this Subtopic applies to share-based payment awards

to employees

that are classified as equity (see paragraphs 718-10-25-6 through

25-19

25-19A for a description of what is classified as equity).

26. Amend paragraphs 718-20-35-1 through 35-2, 718-20-35-3 through 35-3A, 718-20-35-5, and 718-20-35-7 through 35-8, with a link to transition paragraph 718-10-65-11, as follows:

Subsequent Measurement

> Fair Value Not Reasonably Estimable

718-20-35-1 An equity instrument for which it is not possible to reasonably estimate fair value at the grant date shall be remeasured at each reporting date through the date of exercise or other settlement. The final measure of compensation cost shall be the intrinsic value of the instrument at the date it is settled. Compensation cost for each period until settlement shall be based on the change (or a portion of the change, depending on the percentage of the requisite service that has been rendered for an employee award or the percentage that would have been recognized had the grantor paid cash for the goods or services instead of paying with a nonemployee award at the reporting date) in the intrinsic value of the instrument in each reporting period. The entity shall continue to use the intrinsic value method for those instruments even if it subsequently concludes that it is possible to reasonably estimate their fair value.

> Contingent Features

718-20-35-2 A contingent feature of an

award that might cause

an employee

a grantee to return to the entity either equity instruments earned or realized gains from the sale of equity instruments earned for consideration that is less than fair value on the date of transfer (including no consideration), such as a clawback feature (see paragraph 718-10-55-8), shall be accounted for if and when the contingent event occurs. Example 10 (see paragraph 718-20-55-84) provides an illustration of an

employee award with a clawback feature.

> Modification of an Award

718-20-35-3 Except as described in paragraph 718-20-35-2A, a modification of the terms or conditions of an equity award shall be treated as an exchange of the original award for a new award. In substance, the entity repurchases the original instrument by issuing a new instrument of equal or greater value, incurring additional compensation cost for any incremental value. The effects of a modification shall be measured as follows:

a. Incremental compensation cost shall be measured as the excess, if any, of the fair value of the modified award determined in accordance with the provisions of this Topic over the fair value of the original award immediately before its terms are modified, measured based on the share price and other pertinent factors at that date. As indicated in paragraph 718-10-30-20, references to fair value throughout this Topic shall be read also to encompass calculated value. The effect of the modification on the number of instruments expected to vest also shall be reflected in determining incremental compensation cost. The estimate at the modification date of the portion of the award expected to vest shall be subsequently adjusted, if necessary, in accordance with paragraph 718-10-35-1D or 718-10-35-3 and other guidance in Examples 14 through 15 (see paragraphs 718-20-55-107 through 55-121).

b. Total recognized compensation cost for an equity award shall at least equal the fair value of the award at the grant date unless at the date of the modification the performance or service conditions of the original award are not expected to be satisfied. Thus, the total compensation cost measured at the date of a modification shall be the sum of the following:

1. The portion of the grant-date fair value of the original award for which

the promised good is expected to be delivered (or has already been delivered) or the

requisite

service is expected to be rendered (or has already been rendered) at that date

2. The incremental cost resulting from the modification. Compensation cost shall be subsequently adjusted, if necessary, in accordance with paragraph 718-10-35-1D or 718-10-35-3 and other guidance in Examples 14 through 15 (see paragraphs 718-20-55-107 through 55-121).

c. A change in compensation cost for an equity award measured at intrinsic value in accordance with paragraph 718-20-35-1 shall be measured by comparing the intrinsic value of the modified award, if any, with the intrinsic value of the original award, if any, immediately before the modification.

718-20-35-3A An entity that has an accounting policy to account for forfeitures when they occur in accordance with paragraph 718-10-35-1D or 718-10-35-3 shall assess at the date of the modification whether the performance or service conditions of the original award are expected to be satisfied when measuring the effects of the modification in accordance with paragraph 718-20-35-3. However, the entity shall apply its accounting policy to account for forfeitures when they occur when subsequently accounting for the modified award.

> > Short-Term Inducements

718-20-35-5 Except as described in paragraph 718-20-35-2A, a

short-term inducement shall be accounted for as a modification of the terms of only the awards of

employees

grantees who accept the inducement, and other inducements shall be accounted for as modifications of the terms of all awards subject to them.

> > Repurchase or Cancellation

718-20-35-7 The amount of cash or other assets transferred (or liabilities incurred) to repurchase an equity award shall be charged to equity, to the extent that the amount paid does not exceed the fair value of the equity instruments repurchased at the repurchase date. Any excess of the repurchase price over the fair value of the instruments repurchased shall be recognized as additional compensation cost. An entity that repurchases an award for which the

promised goods have not been delivered or the requisite

service has not been rendered has, in effect, modified the

employee's requisite service period

or nonemployee's vesting period to the period for which

goods have already been delivered or service already has been rendered, and thus the amount of compensation cost measured at the grant date but not yet recognized shall be recognized at the repurchase date.

> > Cancellation and Replacement

718-20-35-8 Except as described in paragraph 718-20-35-2A, cancellation of an award accompanied by the concurrent grant of (or offer to grant) a

replacement award or other valuable consideration shall be accounted for as a modification of the terms of the cancelled award. (The phrase

offer to grant is intended to cover situations in which the

service inception date precedes the grant date.) Therefore, incremental compensation cost shall be measured as the excess of the fair value of the replacement award or other valuable consideration over the fair value of the cancelled award at the cancellation date in accordance with paragraph 718-20-35-3. Thus, the total compensation cost measured at the date of a cancellation and replacement shall be the portion of the grant-date fair value of the original award for which the

promised good is expected to be delivered (or has already been delivered) or the requisite

service is expected to be rendered (or has already been rendered) at that date plus the incremental cost resulting from the cancellation and replacement.

27. Add paragraphs 718-20-55-3A, 718-20-55-4A through 55-4C, 718-20-55-35A through 55-35B, 718-20-55-41A through 55-41B, 718-20-55-47A through 55-47B, 718-20-55-51A through 55-51B, 718-20-55-61A through 55-61B, 718-20-55-68A through 55-68B, 718-20-55-84A through 55-84B, 718-20-55-93A through 55-93D, 718-20-55-109A through 55-109B, 718-20-55-120A through 55-120B, and 718-20-55-122A through 55-122C and amend paragraphs 718-20-55-4, 718-20-55-71 and its related heading, the heading preceding paragraph 718-20-55-87, and 718-20-55-108, with a link to transition paragraph 718-10-65-11, as follows:

Implementation Guidance and Illustrations

> Illustrations

718-20-55-3 The following Examples are included in this Subtopic because they assume equity classification. However, these Examples would also apply to awards classified as liabilities except that the amounts in the Examples would likely change due to the requirement under Subtopic 718-30 to remeasure share-based liability awards at fair value each reporting period until settlement.

718-20-55-3A The following Examples describe awards to employees. However, where specifically identified, guidance for certain aspects of the Examples (for example, changes in total compensation cost to be recognized, forfeiture treatment, taxes, and modifications) also is applicable to nonemployee awards. Therefore, the guidance in those identified instances may serve as implementation guidance for nonemployee awards. Specific valuation amounts used in the Examples could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions. An entity should consider the facts and circumstances of its nonemployee awards and use judgment in applying the guidance.

> > Example 1: Accounting for Share Options with Service Conditions

718-20-55-4 The following Cases illustrate the guidance in paragraphs 718-10-35-1D through 35-1E for nonemployee awards, paragraphs 718-10-35-2 through 35-7 for employee awards, and paragraphs 718-740-25-2 through 25-3 for both nonemployee and employee awards, except for the vesting provisions:

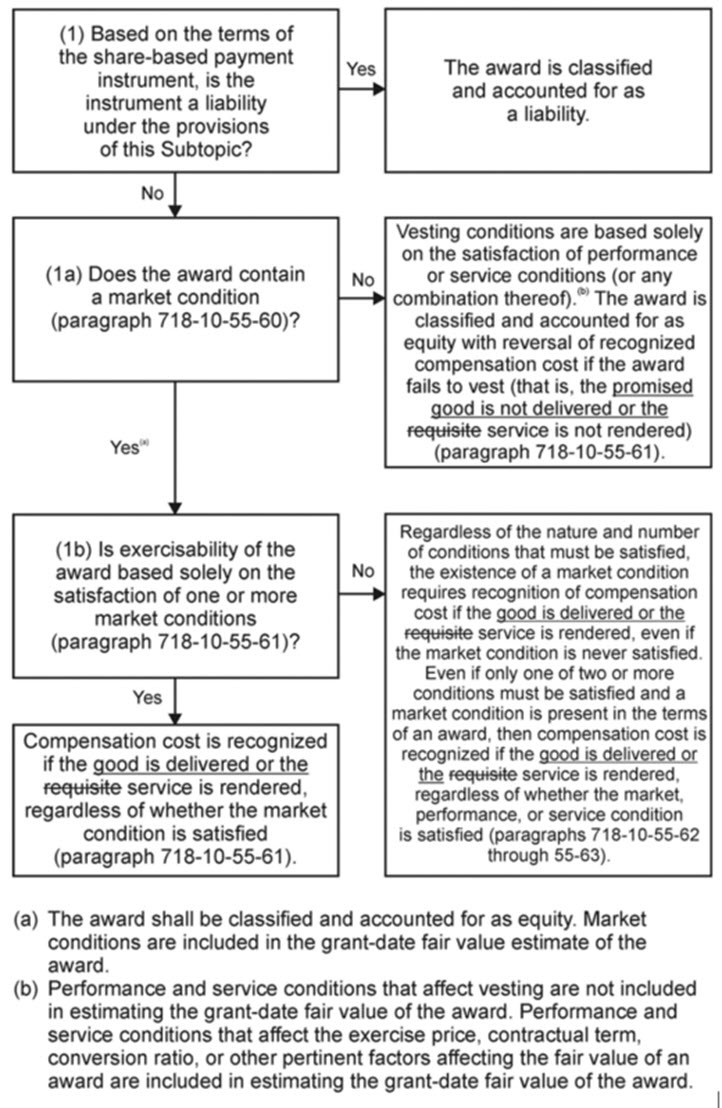

a. Share options with cliff vesting and forfeitures estimated in initial accruals of compensation cost (Case A)

b. Share options with graded vesting and forfeitures estimated in initial accruals of compensation cost (Case B)

c. Share options with cliff vesting and forfeitures recognized when they occur (Case C).

718-20-55-4A Cases A through C (see paragraphs 718-20-55-10 through 55-34G) describe employee awards. However, the principles on accounting for employee awards, except for the compensation cost attribution, are the same for nonemployee awards. Consequently, all of the following in Case A are equally applicable to nonemployee awards with the same features as the awards in Cases A through C (that is, awards with a specified time period for vesting):

a. The assumptions in paragraphs 718-20-55-6 through 55-9

b. Total compensation cost considerations (including estimates of forfeitures) in paragraphs 718-20-55-10 through 55-12

c. Changes in the estimation of forfeitures in paragraphs 718-20-55-14 through 55-15

d. Exercise or expiration considerations in paragraphs 718-20-55-18 through 55-21 and 718-20-55-23.

Therefore, the guidance in those paragraphs may serve as implementation guidance for nonemployee awards. Similarly, an entity also may elect to account for nonemployee award forfeitures as they occur as illustrated in Case C (see paragraph 718-20-55-34A).

718-20-55-4B Nonemployee awards may be similar to employee awards (that is, cliff vesting or graded vesting). However, the compensation cost attribution for awards to nonemployees may be the same as or different from employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in the Cases could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-4C Because of the differences in compensation cost attribution, the accounting policy election illustrated in Case B (see paragraph 718-20-55-25) does not apply to nonemployee awards.

718-20-55-5 Cases A, B, and C share all of the assumptions in paragraphs 718-20-55-6 through 55-34G, with the following exceptions:

a. In Case C, Entity T has an accounting policy to account for forfeitures when they occur in accordance with paragraph 718-10-35-3.

b. In Cases A and B, Entity T has an accounting policy to estimate the number of forfeitures expected to occur, also in accordance with paragraph 718-10-35-3.

c. In Case B, the share options have graded vesting.

d. In Cases A and C, the share options have cliff vesting.

718-20-55-6 Entity T, a public entity, grants at-the-money employee share options with a contractual term of 10 years. All share options vest at the end of three years (cliff vesting), which is an explicit service (and requisite service) period of three years. The share options do not qualify as incentive stock options for U.S. tax purposes. The enacted tax rate is 35 percent. In each Case, Entity T concludes that it will have sufficient future taxable income to realize the deferred tax benefits from its share-based payment transactions.

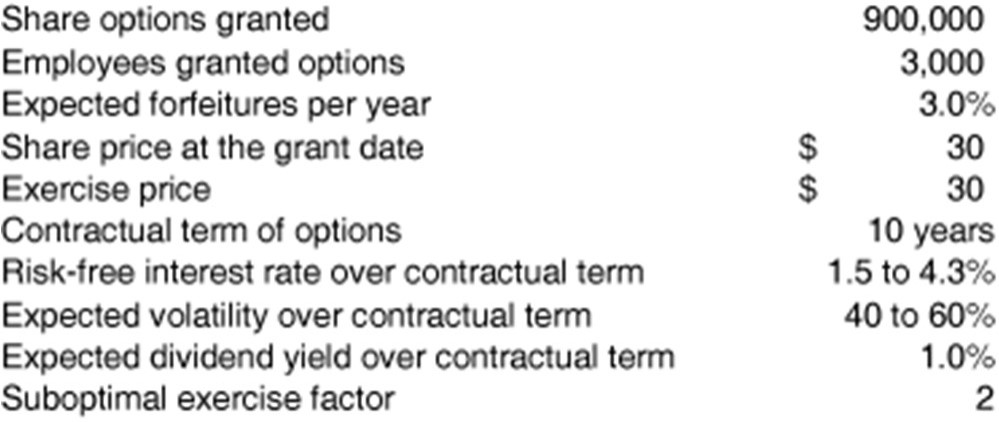

718-20-55-7 The following table shows assumptions and information about the share options granted on January 1, 20X5 applicable to all Cases, except for expected forfeitures per year, which does not apply in Case C.

718-20-55-8 A suboptimal exercise factor of two means that exercise is generally expected to occur when the share price reaches two times the share option's exercise price. Option-pricing theory generally holds that the optimal (or profit-maximizing) time to exercise an option is at the end of the option's term; therefore, if an option is exercised before the end of its term, that exercise is referred to as suboptimal. Suboptimal exercise also is referred to as early exercise. Suboptimal or early exercise affects the expected term of an option. Early exercise can be incorporated into option-pricing models through various means. In this Case, Entity T has sufficient information to reasonably estimate early exercise and has incorporated it as a function of Entity T's future stock price changes (or the option's intrinsic value). In this Case, the factor of 2 indicates that early exercise would be expected to occur, on average, if the stock price reaches $60 per share ($30 × 2). Rather than use its weighted average suboptimal exercise factor, Entity T also may use multiple factors based on a distribution of early exercise data in relation to its stock price.

718-20-55-9 This Case assumes that each employee receives an equal grant of 300 options. Using as inputs the last 7 items from the table in paragraph 718-20-55-7, Entity T's lattice-based valuation model produces a fair value of $14.69 per option. A lattice model uses a suboptimal exercise factor to calculate the expected term (that is, the expected term is an output) rather than the expected term being a separate input. If an entity uses a Black-Scholes-Merton option-pricing formula, the expected term would be used as an input instead of a suboptimal exercise factor.

> > > Case A: Share Options with Cliff Vesting and Forfeitures Estimated in Initial Accruals of Compensation Cost

718-20-55-10 Total compensation cost recognized over the requisite service period (which is the vesting period in this Case) shall be the grant-date fair value of all share options that actually vest (that is, all options for which the requisite service is rendered). This Case assumes that Entity T's accounting policy is to estimate the number of forfeitures expected to occur in accordance with paragraph 718-10-35-3. As a result, Entity T is required to estimate at the grant date the number of share options for which the requisite service is expected to be rendered (which, in this Case, is the number of share options for which vesting is deemed probable). If that estimate changes, it shall be accounted for as a change in estimate and its cumulative effect (from applying the change retrospectively) recognized in the period of change. Entity T estimates at the grant date the number of share options expected to vest and subsequently adjusts compensation cost for changes in the estimated rate of forfeitures and differences between expectations and actual experience. This Case also assumes that none of the compensation cost is capitalized as part of the cost of an asset.

718-20-55-11 The estimate of the number of forfeitures considers historical employee turnover rates and expectations about the future. Entity T has experienced historical turnover rates of approximately 3 percent per year for employees at the grantees' level, and it expects that rate to continue over the requisite service period of the awards. Therefore, at the grant date Entity T estimates the total compensation cost to be recognized over the requisite service period based on an expected forfeiture rate of 3 percent per year. Actual forfeitures are 5 percent in 20X5, but no adjustments to cumulative compensation cost are recognized in 20X5 because Entity T still expects actual forfeitures to average 3 percent per year over the 3-year vesting period. As of December 31, 20X6, management decides that the forfeiture rate will likely increase through 20X7 and changes its estimated forfeiture rate for the entire award to 6 percent per year. Adjustments to cumulative compensation cost to reflect the higher forfeiture rate are made at the end of 20X6. At the end of 20X7 when the award becomes vested, actual forfeitures have averaged 6 percent per year, and no further adjustment is necessary.

718-20-55-12 The first set of calculations illustrates the accounting for the award of share options on January 1, 20X5, assuming that the share options granted vest at the end of three years. (Case B illustrates the accounting for an award assuming graded vesting in which a specified portion of the share options granted vest at the end of each year.) The number of share options expected to vest is estimated at the grant date to be 821,406 (900,000 ×.97 3). Thus, the compensation cost to be recognized over the requisite service period at January 1, 20X5, is $12,066,454 (821,406 × $14.69), and the compensation cost to be recognized during each year of the 3-year vesting period is $4,022,151 ($12,066,454 ÷ 3). The journal entries to recognize compensation cost and related deferred tax benefit at the enacted tax rate of 35 percent are as follows for 20X5.

To recognize compensation cost.

To recognize the deferred tax asset for the temporary difference related to compensation cost ($4,022,151 ×.35 = $1,407,753).

718-20-55-13 The net after-tax effect on income of recognizing compensation cost for 20X5 is $2,614,398 ($4,022,151 – $1,407,753).

718-20-55-14 Absent a change in estimated forfeitures, the same journal entries would be made to recognize compensation cost and related tax effects for 20X6 and 20X7, resulting in a net after-tax cost for each year of $2,614,398. However, at the end of 20X6, management changes its estimated employee forfeiture rate from 3 percent to 6 percent per year. The revised number of share options expected to vest is 747,526 (900,000 ×.94 3). Accordingly, the revised cumulative compensation cost to be recognized by the end of 20X7 is $10,981,157 (747,526 × $14.69). The cumulative adjustment to reflect the effect of adjusting the forfeiture rate is the difference between two-thirds of the revised cost of the award and the cost already recognized for 20X5 and 20X6. The related journal entries and the computations follow.

At December 31, 20X6, to adjust for new forfeiture rate.

718-20-55-15 The related journal entries are as follows.

To adjust previously recognized compensation cost and equity to reflect a higher estimated forfeiture rate.

To adjust the deferred tax accounts to reflect the tax effect of increasing the estimated forfeiture rate ($723,531 ×.35 = $253,236).

718-20-55-16 Journal entries for 20X7 are as follows.

To recognize compensation cost ($10,981,157 ÷ 3 = $3,660,386).

To recognize the deferred tax asset for additional compensation cost ($3,660,386 ×.35 = $1,281,135).

718-20-55-17 As of December 31, 20X7, the entity would examine its actual forfeitures and make any necessary adjustments to reflect cumulative compensation cost for the number of shares that actually vested.

718-20-55-18 All 747,526 vested share options are exercised on the last day of 20Y2. Entity T has already recognized its income tax expense for the year without regard to the effects of the exercise of the employee share options. In other words, current tax expense and current taxes payable were recognized based on income and deductions before consideration of additional deductions from exercise of the employee share options. Upon exercise, the amount credited to common stock (or other appropriate equity accounts) is the sum of the cash proceeds received and the amounts previously credited to additional paid-in capital in the periods the services were received (20X5 through 20X7). In this Case, Entity T has no-par common stock and at exercise, the share price is assumed to be $60.

718-20-55-19 At exercise the journal entries are as follows.

To recognize the issuance of common stock upon exercise of share options and to reclassify previously recorded paid-in capital.

718-20-55-20 In this Case, the difference between the market price of the shares and the exercise price on the date of exercise is deductible for tax purposes pursuant to U.S. tax law in effect in 2004 (the share options do not qualify as incentive stock options). Paragraph 718-740-35-2 requires that the tax effect be recognized as income tax expense or benefit in the income statement for the difference between the deduction for an award for tax purposes and the cumulative compensation cost of that award recognized for financial reporting purposes. With the share price of $60 at exercise, the deductible amount is $22,425,780 [747,526 × ($60 – $30)], and the tax benefit is $7,849,023 ($22,425,780 ×.35).

718-20-55-21 At exercise the journal entries are as follows.

To write off the deferred tax asset related to deductible share options at exercise ($10,981,157 ×.35 = $3,843,405).

To adjust current tax expense and current taxes payable to recognize the current tax benefit from deductible compensation cost upon exercise of share options.

718-20-55-22 Paragraph superseded by Accounting Standards Update No. 2016-09.

718-20-55-23 If instead the share options expired unexercised, previously recognized compensation cost would not be reversed. There would be no deduction on the tax return and, therefore, the entire deferred tax asset of $3,843,405 would be charged to income tax expense.

718-20-55-23A If employees terminated with out-of-the-money vested share options, the deferred tax asset related to those share options would be written off when those options expire.

718-20-55-24 Paragraph superseded by Accounting Standards Update No. 2016-09.

> > > Case B: Share Options with Graded Vesting

718-20-55-25 Paragraph 718-10-35-8 provides for the following two methods to recognize compensation cost for awards with graded vesting:

a. On a straight-line basis over the requisite service period for each separately vesting portion of the award as if the award was, in-substance, multiple awards (graded vesting attribution method)

b. On a straight-line basis over the requisite service period for the entire award (that is, over the requisite service period of the last separately vesting portion of the award), subject to the limitation noted in paragraph 718-10-35-8.

718-20-55-26 The choice of attribution method for awards with graded vesting schedules is a policy decision that is not dependent on an entity's choice of valuation technique. In addition, the choice of attribution method applies to awards with only service conditions.

718-20-55-27 The accounting is illustrated below for both methods and uses the same assumptions as those noted in Case A except for the vesting provisions.

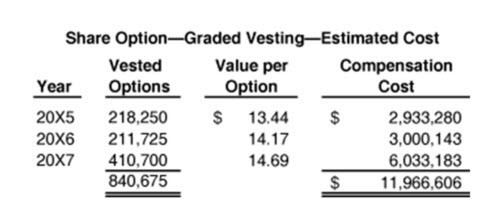

718-20-55-28 Entity T awards 900,000 share options on January 1, 20X5, that vest according to a graded schedule of 25 percent for the first year of service, 25 percent for the second year, and the remaining 50 percent for the third year. Each employee is granted 300 share options. The following table shows the calculation as of January 1, 20X5, of the number of employees and the related number of share options expected to vest. Using the expected 3 percent annual forfeiture rate, 90 employees are expected to terminate during 20X5 without having vested in any portion of the award, leaving 2,910 employees to vest in 25 percent of the award (75 options). During 20X6, 87 employees are expected to terminate, leaving 2,823 to vest in the second 25 percent of the award. During 20X7, 85 employees are expected to terminate, leaving 2,738 employees to vest in the last 50 percent of the award. That results in a total of 840,675 share options expected to vest from the award of 900,000 share options with graded vesting.

718-20-55-29 The value of the share options that vest over the three-year period is estimated by separating the total award into three groups (or tranches) according to the year in which they vest (because the expected life for each tranche differs). The following table shows the estimated compensation cost for the share options expected to vest. The estimates of expected volatility, expected dividends, and risk-free interest rates are incorporated into the lattice, and the graded vesting conditions affect only the earliest date at which suboptimal exercise can occur (see paragraph 718-20-55-8 for information on suboptimal exercise). Thus, the fair value of each of the 3 groups of options is based on the same lattice inputs for expected volatility, expected dividend yield, and risk-free interest rates used to determine the value of $14.69 for the cliff-vesting share options (see paragraphs 718-20-55-7 through 55-9). The different vesting terms affect the ability of the suboptimal exercise to occur sooner (and affect other factors as well, such as volatility), and therefore there is a different expected term for each tranche.

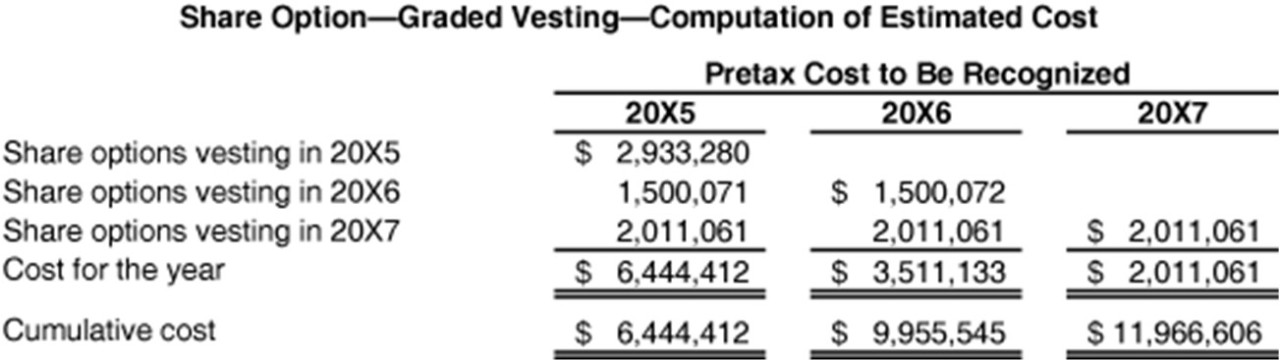

718-20-55-30 Compensation cost is recognized over the periods of requisite service during which each tranche of share options is earned. Thus, the $2,933,280 cost attributable to the 218,250 share options that vest in 20X5 is recognized in 20X5. The $3,000,143 cost attributable to the 211,725 share options that vest at the end of 20X6 is recognized over the 2-year vesting period (20X5 and 20X6). The $6,033,183 cost attributable to the 410,700 share options that vest at the end of 20X7 is recognized over the 3-year vesting period (20X5, 20X6, and 20X7).

718-20-55-31 The following table shows how the $11,966,606 expected amount of compensation cost determined at the grant date is attributed to the years 20X5, 20X6, and 20X7.

718-20-55-32 Entity T could use the same computation of estimated cost, as in the preceding table, but could elect to recognize compensation cost on a straight-line basis for all graded vesting awards. In that case, total compensation cost to be attributed on a straight-line basis over each year in the 3-year vesting period is approximately $3,988,868 ($11,966,606 ÷ 3). Entity T also could use a single weighted-average expected life to value the entire award and arrive at a different amount of total compensation cost. Total compensation cost could then be attributed on a straight-line basis over the three-year vesting period. However, this Topic requires that compensation cost recognized at any date must be at least equal to the amount attributable to options that are vested at that date. For example, if 50 percent of this same option award vested in the first year of the 3-year vesting period, 436,500 options [2,910 × 150 (300 × 50%)] would be vested at the end of 20X5. Compensation cost amounting to $5,866,560 (436,500 × $13.44) attributable to the vested awards would be recognized in the first year.

718-20-55-33 Compensation cost is adjusted for awards with graded vesting to reflect differences between estimated and actual forfeitures as illustrated for the cliff-vesting options, regardless of which method is used to estimate value and attribute cost.

718-20-55-34 Accounting for the tax effects of awards with graded vesting follows the same pattern illustrated in paragraphs 718-20-55-20 through 55-23. However, unless Entity T identifies and tracks the specific tranche from which share options are exercised, it would not know the recognized compensation cost that corresponds to exercised share options for purposes of calculating the tax effects resulting from that exercise. If an entity does not know the specific tranche from which share options are exercised, it should assume that options are exercised on a first-vested, first-exercised basis (which works in the same manner as the firstin, first-out [FIFO] basis for inventory costing).

> > > Case C: Share Options with Cliff Vesting and Forfeitures Recognized When They Occur

718-20-55-34A This Case uses the same assumptions as Case A except that Entity T's accounting policy is to account for forfeitures when they occur in accordance with paragraph 718-10-35-3. Consequently, compensation cost previously recognized for an employee share option is reversed in the period in which forfeiture of the award occurs. Previously recognized compensation cost is not reversed if an employee share option for which the requisite service has been rendered expires unexercised. This Case also assumes that none of the compensation cost is capitalized as part of the cost of an asset.

718-20-55-34B In 20X5, 20X6, and 20X7, share option forfeitures are 45,000, 47,344, and 60,130, respectively.

718-20-55-34C The compensation cost to be recognized over the requisite service period at January 1, 20X5, is $13,221,000 (900,000 × $14.69), and the compensation cost to be recognized (excluding the effect of forfeitures) during each year of the 3-year vesting period is $4,407,000 ($13,221,000 ÷ 3). The journal entries for 20X5 to recognize compensation cost and related deferred tax benefit at the enacted tax rate of 35 percent are as follows.

To recognize compensation cost excluding the effect of forfeitures for 20X5.

To recognize the deferred tax asset for the temporary difference related to compensation cost ($4,407,000 × .35).

718-20-55-34D During 20X5, 45,000 share options are forfeited; accordingly, Entity T remeasures compensation cost to reflect the effect of forfeitures when they occur and recognizes compensation costs for 855,000 (900,000 – 45,000) share options (net of forfeitures) at an amount of $12,559,950 (855,000 × $14.69) over the 3-year vesting period, or $4,186,650 each year ($12,559,950 ÷ 3). Therefore, Entity T reverses recognized compensation cost of $220,350 (45,000 share options × $14.69 ÷ 3) to account for forfeitures that occurred during 20X5. The journal entries to recognize the effect of forfeitures during 20X5 and the related reduction in the deferred tax benefit are as follows.

To recognize the effect of forfeitures on compensation cost when they occur for 20X5.

To reverse the deferred tax asset related to the forfeited awards ($220,350 × .35).

718-20-55-34E As of January 1, 20X6, Entity T determines the compensation cost and related tax effects to recognize during 20X6. The journal entries for 20X6 to recognize compensation cost and related deferred tax benefit at the enacted tax rate of 35 percent are as follows (excluding the effect of forfeitures in 20X6).

To recognize compensation cost excluding the effect of awards that forfeited during 20X6.

To recognize the deferred tax asset for the temporary difference related to compensation cost ($4,186,650 × .35).

718-20-55-34F In 20X6, 47,344 share options are forfeited (that is, 92,344 share options in total have been forfeited by December 31, 20X6); accordingly, Entity T would recognize compensation cost for 807,656 share options over the 3-year vesting period. On the basis of actual forfeitures in 20X5 and 20X6, Entity T should recognize a cumulative compensation cost of $11,864,467 (807,656 × $14.69) for the 3-year vesting period, or $3,954,822 a year ($11,864,467 ÷ 3 years). Therefore, Entity T reverses recognized compensation cost of $231,828 ($4,186,650 – $3,954,822) for 20X5 and 20X6, or $463,656 in total, to account for forfeitures that occurred during 20X6. The journal entries to recognize the effect of forfeitures during 20X6 and the related reduction in the deferred tax benefit are as follows.

To recognize the effect of the forfeitures on compensation cost when they occur for 20X6.

To reverse the deferred tax asset related to the forfeited awards ($463,656 × .35).

718-20-55-34G Entity T follows the same approach in 20X7 as it applied in 20X6 to recognize compensation cost and related tax effects.

> > Example 2: Share Option Award under Which the Number of Options to Be Earned Varies

718-20-55-35 This Example illustrates the guidance in paragraph 718-10-30-15.

718-20-55-35A This Example (see paragraphs 718-20-55-36 through 55-40)describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards.Consequently, all of the following are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, the number of options earned varies on the basis of the achievement of particular performance conditions):

a. Certain valuation assumptions in paragraph 718-20-55-36

b. Total compensation cost considerations provided in paragraphs 718-20-55-37 through 55-39 (that is, an entity must consider if it is probable that specific performance conditions will be achieved for an award with a specified time period for vesting and performance conditions)

c. Forfeiture adjustments in paragraph 718-20-55-40.

Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-35B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-36 This Example shows the computation of compensation cost if Entity T grants an award of share options with multiple performance conditions. Under the award, employees vest in differing numbers of options depending on the amount by which the market share of one of Entity T's products increases over a three-year period (the share options cannot vest before the end of the three-year period). The three-year explicit service period represents the requisite service period. On January 1, 20X5, Entity T grants to each of 1,000 employees an award of up to 300 10-year-term share options on its common stock. If market share increases by at least 5 percentage points by December 31, 20X7, each employee vests in at least 100 share options at that date. If market share increases by at least 10 percentage points, another 100 share options vest, for a total of 200. If market share increases by more than 20 percentage points, each employee vests in all 300 share options. Entity T's share price on January 1, 20X5, is $30 and other assumptions are the same as in Example 1 (see paragraph 718-20-55-4). The grant-date fair value per share option is $14.69. While the vesting conditions in this Example and in Example 1 (see paragraph 718-20-55-4) are different, the equity instruments being valued have the same estimate of grant-date fair value. That is a consequence of the modified grant-date method, which accounts for the effects of vesting requirements or other restrictions that apply during the vesting period by recognizing compensation cost only for the instruments that actually vest. (This discussion does not refer to awards with market conditions that affect exercisability or the ability to retain the award as described in paragraphs 718-10-55-60 through 55-63.)

718-20-55-37 The compensation cost of the award depends on the estimated number of options that will vest. Entity T must determine whether it is probable that any performance condition will be achieved, that is, whether the growth in market share over the 3-year period will be at least 5 percent. Accruals of compensation cost are initially based on the probable outcome of the performance conditions—in this case, different levels of market share growth over the three-year vesting period—and adjusted for subsequent changes in the estimated or actual outcome. If Entity T determines that no performance condition is probable of achievement (that is, market share growth is expected to be less than 5 percentage points), then no compensation cost is recognized; however, Entity T is required to reassess at each reporting date whether achievement of any performance condition is probable and would begin recognizing compensation cost if and when achievement of the performance condition becomes probable.

718-20-55-38 Paragraph 718-10-25-20 requires accruals of cost to be based on the probable outcome of performance conditions. Accordingly, this Topic prohibits Entity T from basing accruals of compensation cost on an amount that is not a possible outcome (and thus cannot be the probable outcome). For instance, if Entity T estimates that there is a 90 percent, 30 percent, and 10 percent likelihood that market share growth will be at least 5 percentage points, at least 10 percentage points, and greater than 20 percentage points, respectively, it would not try to determine a weighted average of the possible outcomes because that number of shares is not a possible outcome under the arrangement.

718-20-55-39 The following table shows the compensation cost that would be recognized in 20X5, 20X6, and 20X7 if Entity T estimates at the grant date that it is probable that market share will increase at least 5 but less than 10 percentage points (that is, each employee would receive 100 share options). That estimate remains unchanged until the end of 20X7, when Entity T's market share has increased over the 3-year period by more than 10 percentage points. Thus, each employee vests in 200 share options.

718-20-55-40 As in Example 1, Case A (see paragraph 718-20-55-10), Entity T experiences actual forfeiture rates of 5 percent in 20X5, and in 20X6 changes its estimate of forfeitures for the entire award from 3 percent to 6 percent per year. In 20X6, cumulative compensation cost is adjusted to reflect the higher forfeiture rate. By the end of 20X7, a 6 percent forfeiture rate has been experienced, and no further adjustments for forfeitures are necessary. Through 20X5, Entity T estimates that 913 employees (1,000 ×.97 3) will remain in service until the vesting date. At the end of 20X6, the number of employees estimated to remain in service is adjusted for the higher forfeiture rate, and the number of employees estimated to remain in service is 831 (1,000 ×.94 3). The compensation cost of the award is initially estimated based on the number of options expected to vest, which in turn is based on the expected level of performance and the fair value of each option. That amount would be adjusted as needed for changes in the estimated and actual forfeiture rates and for differences between estimated and actual market share growth. The amount of compensation cost recognized (or attributed) when achievement of a performance condition is probable depends on the relative satisfaction of the performance condition based on performance to date. Entity T determines that recognizing compensation cost ratably over the three-year vesting period is appropriate with one-third of the value of the award recognized each year.

> > Example 3: Share Option Award under Which the Exercise Price Varies

718-20-55-41 This Example illustrates the guidance in paragraph 718-10-30-15.

718-20-55-41A This Example (see paragraphs 718-20-55-42 through 55-46) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, both of the following are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, an immediately vested and exercisable award with an exercise price that varies on the basis of the achievement of particular performance conditions):

a. Certain valuation assumptions in paragraphs 718-20-55-42 through 55-43

b. The total compensation cost considerations provided in paragraphs 718-20-55-44 through 55-46 (that is, an entity must consider if it is probable that specific performance conditions will be achieved).

Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-41B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-42 This Example shows the computation of compensation cost if Entity T grants a share option award with a performance condition under which the exercise price, rather than the number of shares, varies depending on the level of performance achieved. On January 1, 20X5, Entity T grants to its chief executive officer 10-year share options on 10,000 shares of its common stock, which are immediately vested and exercisable (an explicit service period of zero). The share price at the grant date is $30, and the initial exercise price also is $30. However, that price decreases to $15 if the market share for Entity T's products increases by at least 10 percentage points by December 31, 20X6, and provided that the chief executive officer continues to be employed by Entity T and has not previously exercised the options (an explicit service period of 2 years, which also is the requisite service period).

718-20-55-43 Entity T estimates at the grant date the expected level of market share growth, the exercise price of the options, and the expected term of the options. Other assumptions, including the risk-free interest rate and the service period over which the cost is attributed, are consistent with those estimates. Entity T estimates at the grant date that its market share growth will be at least 10 percentage points over the 2-year performance period, which means that the expected exercise price of the share options is $15, resulting in a fair value of $19.99 per option. Option value is determined using the same assumptions noted in paragraph 718-20-55-7 except the exercise price is $15 and the award is not exercisable at $15 per option for 2 years.

718-20-55-44 Total compensation cost to be recognized if the performance condition is satisfied would be $199,900 (10,000 × $19.99). Paragraph 718-10-30-15 requires that the fair value of both awards with service conditions and awards with performance conditions be estimated as of the date of grant. Paragraph 718-10-35-3 also requires recognition of cost for the number of instruments for which the requisite service is provided. For this performance award, Entity T also selects the expected assumptions at the grant date if the performance goal is not met. If market share growth is not at least 10 percentage points over the 2-year period, Entity T estimates a fair value of $13.08 per option. Option value is determined using the same assumptions noted in paragraph 718-20-55-7 except the award is immediately vested.

718-20-55-45 Total compensation cost to be recognized if the performance goal is not met would be $130,800 (10,000 × $13.08). Because Entity T estimates that the performance condition would be satisfied, it would recognize compensation cost of $130,800 on the date of grant related to the fair value of the fully vested award and recognize compensation cost of $69,100 ($199,900 – $130,800) over the 2year requisite service period related to the condition. Because of the nature of the performance condition, the award has multiple requisite service periods that affect the manner in which compensation cost is attributed. Paragraphs 718-10-55-67 through 55-79 provide guidance on estimating the requisite service period.

718-20-55-46 During the two-year requisite service period, adjustments to reflect any change in estimate about satisfaction of the performance condition should be made, and, thus, aggregate cost recognized by the end of that period reflects whether the performance goal was met.

> > Example 4: Share Option Award with Other Performance Conditions

718-20-55-47 This Example illustrates the guidance in paragraph 718-10-30-15.

718-20-55-47A This Example (see paragraphs 718-20-55-48 through 55-50) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, the concepts about valuation, expected term, and total compensation cost that should be recognized (that is, the consideration of whether it is probable that performance conditions will be achieved) in paragraphs 718-20-55-48 through 55-50 are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, awards with performance conditions that affect inputs to an award's fair value). Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-47B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-48 While performance conditions usually affect vesting conditions, they may affect exercise price, contractual term, quantity, or other factors that affect an award's fair value before, at the time of, or after vesting. This Topic requires that all performance conditions be accounted for similarly. A potential grant-date fair value is estimated for each of the possible outcomes that are reasonably determinable at the grant date and associated with the performance condition(s) of the award (as demonstrated in Example 3 [see paragraph 718-20-55-41)]. Compensation cost ultimately recognized is equal to the grant-date fair value of the award that coincides with the actual outcome of the performance condition(s).

718-20-55-49 To illustrate the notion described in the preceding paragraph and attribution of compensation cost if performance conditions have different service periods, assume Entity C grants 10,000 at-the-money share options on its common stock to an employee. The options have a 10-year contractual term. The share options vest upon successful completion of phase-two clinical trials to satisfy regulatory testing requirements related to a developmental drug therapy. Phase-two clinical trials are scheduled to be completed (and regulatory approval of that phase obtained) in approximately 18 months; hence, the implicit service period is approximately 18 months. Further, the share options will become fully transferable upon regulatory approval of the drug therapy (which is scheduled to occur in approximately four years). The implicit service period for that performance condition is approximately 30 months (beginning once phase-two clinical trials are successfully completed). Based on the nature of the performance conditions, the award has multiple requisite service periods (one pertaining to each performance condition) that affect the pattern in which compensation cost is attributed. Paragraphs 718-10-55-67 through 55-79 and 718-10-55-86 through 55-88 provide guidance on estimating the requisite service period of an award. The determination of whether compensation cost should be recognized depends on Entity C's assessment of whether the performance conditions are probable of achievement. Entity C expects that all performance conditions will be achieved. That assessment is based on the relevant facts and circumstances, including Entity C's historical success rate of bringing developmental drug therapies to market.

718-20-55-50 At the grant date, Entity C estimates that the potential fair value of each share option under the 2 possible outcomes is $10 (Outcome 1, in which the share options vest and do not become transferable) and $16 (Outcome 2, in which the share options vest and do become transferable). The difference in estimated fair values of each outcome is due to the change in estimate of the expected term of the share option. Outcome 1 uses an expected term in estimating fair value that is less than the expected term used for Outcome 2, which is equal to the award's 10-year contractual term. If a share option is transferable, its expected term is equal to its contractual term (see paragraph 718-10-55-29). If Outcome 1 is considered probable of occurring, Entity C would recognize $100,000 (10,000 × $10) of compensation cost ratably over the 18-month requisite service period related to the successful completion of phase-two clinical trials. If Outcome 2 is considered probable of occurring, then Entity C would recognize an additional $60,000 [10,000 × ($16 – $10)] of compensation cost ratably over the 30-month requisite service period (which begins after phase-two clinical trials are successfully completed) related to regulatory approval of the drug therapy. Because Entity C believes that Outcome 2 is probable, it recognizes compensation cost in the pattern described. However, if circumstances change and it is determined at the end of Year 3 that the regulatory approval of the developmental drug therapy is likely to be obtained in six years rather than four, the requisite service period for Outcome 2 is revised, and the remaining unrecognized compensation cost would be recognized prospectively through Year 6. On the other hand, if it becomes probable that Outcome 2 will not occur, compensation cost recognized for Outcome 2, if any, would be reversed.

> > Example 5: Share Option with a Market Condition—Indexed Exercise Price

718-20-55-51 This Example illustrates the guidance in paragraph 718-10-30-15.

718-20-55-51A This Example (see paragraphs 718-20-55-52 through 55-60) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards.Consequently, the concepts about valuation in paragraphs 718-20-55-52 through 55-60 are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, awards with market conditions that affect exercise prices). Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-51B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

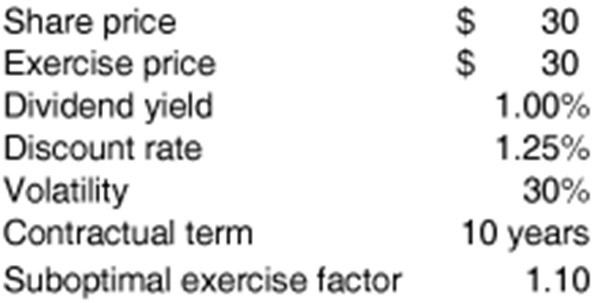

718-20-55-52 Entity T grants share options whose exercise price varies with an index of the share prices of a group of entities in the same industry, that is, a market condition. Assume that on January 1, 20X5, Entity T grants 100 share options on its common stock with an initial exercise price of $30 to each of 1,000 employees. The share options have a maximum term of 10 years. The exercise price of the share options increases or decreases on December 31 of each year by the same percentage that the index has increased or decreased during the year. For example, if the peer group index increases by 10 percent in 20X5, the exercise price of the share options during 20X6 increases to $33 ($30 × 1.10). On January 1, 20X5, the peer group index is assumed to be 400. The dividend yield on the index is assumed to be 1.25 percent.

718-20-55-53 Each indexed share option may be analyzed as a share option to exchange 0.0750 (30 ÷ 400) shares of the peer group index for a share of Entity T stock—that is, to exchange one noncash asset for another noncash asset. A share option to purchase stock for cash also can be thought of as a share option to exchange one asset (cash in the amount of the exercise price) for another (the share of stock). The intrinsic value of a cash share option equals the difference between the price of the stock upon exercise and the amount—the price—of the cash exchanged for the stock. The intrinsic value of a share option to exchange 0.0750 shares of the peer group index for a share of Entity T stock also equals the difference between the prices of the two assets exchanged.

718-20-55-54 To illustrate the equivalence of an indexed share option and the share option above, assume that an employee exercises the indexed share option when Entity T's share price has increased 100 percent to $60 and the peer group index has increased 75 percent, from 400 to 700. The exercise price of the indexed share option thus is $52.50 ($30 × 1.75).

718-20-55-55 That is the same as the intrinsic value of a share option to exchange 0.0750 shares of the index for 1 share of Entity T stock.

718-20-55-56 Option-pricing models can be extended to value a share option to exchange one asset for another. The principal extension is that the volatility of a share option to exchange two noncash assets is based on the relationship between the volatilities of the prices of the assets to be exchanged—their cross-volatility. In a share option with an exercise price payable in cash, the amount of cash to be paid has zero volatility, so only the volatility of the stock needs to be considered in estimating that option's fair value. In contrast, the fair value of a share option to exchange two noncash assets depends on possible movements in the prices of both assets—in this Example, fair value depends on the cross-volatility of a share of the peer group index and a share of Entity T stock. Historical cross-volatility can be computed directly based on measures of Entity T's share price in shares of the peer group index. For example, Entity T's share price was 0.0750 shares at the grant date and 0.0857 (60 ÷ 700) shares at the exercise date. Those share amounts then are used to compute cross-volatility. Cross-volatility also can be computed indirectly based on the respective volatilities of Entity T stock and the peer group index and the correlation between them. The expected cross-volatility between Entity T stock and the peer group index is assumed to be 30 percent.

718-20-55-57 In a share option with an exercise price payable in cash, the assumed risk-free interest rate (discount rate) represents the return on the cash that will not be paid until exercise. In this Example, an equivalent share of the index, rather than cash, is what will not be paid until exercise. Therefore, the dividend yield on the peer group index of 1.25 percent is used in place of the risk-free interest rate as an input to the option-pricing model.

718-20-55-58 The initial exercise price for the indexed share option is the value of an equivalent share of the peer group index, which is $30 (0.0750 × $400). The fair value of each share option granted is $7.55 based on the following inputs.

718-20-55-59 In this Example, the suboptimal exercise factor is 1.1. In Example 1 (see paragraph 718-20-55-4), the suboptimal exercise factor is 2.0. See paragraph 718-20-55-8 for an explanation of the meaning of a suboptimal exercise factor of 2.0.

718-20-55-60 The indexed share options have a three-year explicit service period. The market condition affects the grant-date fair value of the award and its exercisability; however, vesting is based solely on the explicit service period of three years. The at-the-money nature of the award makes the derived service period irrelevant in determining the requisite service period in this Example; therefore, the requisite service period of the award is three years based on the explicit service period. The accrual of compensation cost would be based on the number of options for which the requisite service is rendered or is expected to be rendered depending on an entity's accounting policy in accordance with paragraph 718-10-35-3 (which is not addressed in this Example). That cost would be recognized over the requisite service period as shown in Example 1 (see paragraph 718-20-55-4).

> > Example 6: Share Unit with Performance and Market Conditions

718-20-55-61 This Example illustrates the guidance in paragraphs 718-10-25-20 through 25-21, 718-10-30-27, and 718-10-35-4.

718-20-55-61A This Example (see paragraphs 718-20-55-62 through 55-67) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, both of the following are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, awards with a specified time period for vesting and the recognition of compensation cost based on the achievement of particular performance conditions):

a. The performance conditions in paragraph 718-20-55-62

b. Concepts about valuation, compensation cost reversal, and total compensation cost that should be recognized (that is, the consideration of whether it is probable that performance conditions will be achieved) in paragraphs 718-20-55-63 and 718-20-55-65 through 55-67.

Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-61B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-62 Entity T grants 100,000 share units to each of 10 vice presidents (1 million share units in total) on January 1, 20X5. Each share unit has a contractual term of three years and a vesting condition based on performance. The performance condition is different for each vice president and is based on specified goals to be achieved over three years (an explicit three-year service period). If the specified goals are not achieved at the end of three years, the share units will not vest. Each share unit is convertible into shares of Entity T at contractual maturity as follows:

a. If Entity T's share price has appreciated by a percentage that exceeds the percentage appreciation of the S&P 500 index by at least 10 percent (that is, the relative percentage increase is at least 10 percent), each share unit converts into 3 shares of Entity T stock.

b. If the relative percentage increase is less than 10 percent but greater than zero percent, each share unit converts into 2 shares of Entity T stock.

c. If the relative percentage increase is less than or equal to zero percent, each share unit converts into 1 share of Entity T stock.

d. If Entity T's share price has depreciated, each share unit converts into zero shares of Entity T stock.

718-20-55-63 Appreciation or depreciation for Entity T's share price and the S&P 500 index is measured from the grant date.

718-20-55-64 This market condition affects the ability to retain the award because the conversion ratio could be zero; however, vesting is based solely on the explicit service period of three years, which is equal to the contractual maturity of the award. That set of circumstances makes the derived service period irrelevant in determining the requisite service period; therefore, the requisite service period of the award is three years based on the explicit service period.

718-20-55-65 The share units' conversion feature is based on a variable target stock price (that is, the target stock price varies based on the S&P 500 index); hence, it is a market condition. That market condition affects the fair value of the share units that vest. Each vice president's share units vest only if the individual's performance condition is achieved; consequently, this award is accounted for as an award with a performance condition (see paragraphs 718-10-55-60 through 55-63). This Example assumes that all share units become fully vested; however, if the share units do not vest because the performance conditions are not achieved, Entity T would reverse any previously recognized compensation cost associated with the nonvested share units.

718-20-55-66 The grant-date fair value of each share unit is assumed for purposes of this Example to be $36. Certain option-pricing models, including Monte Carlo simulation techniques, have been adapted to value path-dependent options and other complex instruments. In this case, the entity concludes that a Monte Carlo simulation technique provides a reasonable estimate of fair value. Each simulation represents a potential outcome, which determines whether a share unit would convert into three, two, one, or zero shares of stock. For simplicity, this Example assumes that no forfeitures will occur during the vesting period. The grant-date fair value of the award is $36 million (1 million × $36); management of Entity T expects that all share units will vest because the performance conditions are probable of achievement. Entity T recognizes compensation cost of $12 million ($36 million ÷ 3) in each year of the 3-year service period; the following journal entries are recognized by Entity T in 20X5, 20X6, and 20X7.

To recognize compensation cost.

To recognize the deferred tax asset for the temporary difference related to compensation cost ($12,000,000 ×.35 = $4,200,000).

718-20-55-67 Upon contractual maturity of the share units, four outcomes are possible; however, because all possible outcomes of the market condition were incorporated into the share units' grant-date fair value, no other entry related to compensation cost is necessary to account for the actual outcome of the market condition. However, if the share units' conversion ratio was based on achieving a performance condition rather than on satisfying a market condition, compensation cost would be adjusted according to the actual outcome of the performance condition (see Example 4 [paragraph 718-20-55-47]).

> > Example 7: Share Option with Exercise Price That Increases by a Fixed Amount or Fixed Percentage

718-20-55-68 This Example illustrates the guidance in paragraph 718-10-30-15.

718-20-55-68A This Example (see paragraphs 718-20-55-69 through 55-70) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, the concepts about valuation in paragraphs 718-20-55-69 through 55-70 are equally applicable to nonemployee awards with the same features as the awards in this Example (that is, awards with exercise prices that increase by a fixed amount or fixed percentage). Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-68B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-69 Some entities grant share options with exercise prices that increase by a fixed amount or a constant percentage periodically. For example, the exercise price of the share options in Example 1 (see paragraph 718-20-55-4) might increase by a fixed amount of $2.50 per year. Lattice models and other valuation techniques can be adapted to accommodate exercise prices that change over time by a fixed amount. Such an arrangement has a market condition and may have a derived service period.

718-20-55-70 Share options with exercise prices that increase by a constant percentage also can be valued using an option-pricing model that accommodates changes in exercise prices. Alternatively, those share options can be valued by deducting from the discount rate the annual percentage increase in the exercise price. That method works because a decrease in the risk-free interest rate and an increase in the exercise price have a similar effect—both reduce the share option value. For example, the exercise price of the share options in Example 1 (see paragraph 718-20-55-4) might increase at the rate of 1 percent annually. For that example, Entity T's share options would be valued based on a risk-free interest rate less 1 percent. Holding all other assumptions constant from that Example, the value of each share option granted by Entity T would be $14.34.

> > Example 8: Employee Share Award Granted by a Nonpublic Entity

718-20-55-71 The Example illustrates the guidance in paragraphs 718-10-30-17 through 30-19 and 718-740-25-2 through 25-4 for employee awards. The accounting demonstrated in this Example also would be applicable to a public entity that grants share awards to its employees. The same measurement method and basis is used for both nonvested share awards and restricted share awards (which are a subset of nonvested share awards).

718-20-55-72 On January 1, 20X6, Entity W, a nonpublic entity, grants 100 shares of stock to each of its 100 employees. The shares cliff vest at the end of three years. Entity W estimates that the grant-date fair value of 1 share of stock is $7. The grant-date fair value of the share award is $70,000 (100 × 100 × $7). The fair value of shares, which is equal to their intrinsic value, is not subsequently remeasured. For simplicity, the example assumes that no forfeitures occur during the vesting period. Because the requisite service period is 3 years, Entity W recognizes $23,333 ($70,000 ÷ 3) of compensation cost for each annual period as follows.

To recognize compensation cost.

To recognize the deferred tax asset for the temporary difference related to compensation cost ($23,333 ×.35 = $8,167).

718-20-55-73 After three years, all shares are vested. For simplicity, this Example assumes that no employees made an Internal Revenue Service (IRS) Code §83(b) election and Entity W has already recognized its income tax expense for the year in which the shares become vested without regard to the effects of the share award. (IRS Code §83(b) permits an employee to elect either the grant date or the vesting date for measuring the fair market value of an award of shares.)

718-20-55-74 The fair value per share on the vesting date, assumed to be $20, is deductible for tax purposes. Paragraph 718-740-35-2 requires that the tax effect be recognized as income tax expense or benefit in the income statement for the difference between the deduction for an award for tax purposes and the cumulative compensation cost of that award recognized for financial reporting purposes. With the share price at $20 on the vesting date, the deductible amount is $200,000 (10,000 × $20), and the tax benefit is $70,000 ($200,000 ×.35).

718-20-55-75 At vesting the journal entries would be as follows.

To write off deferred tax asset related to deductible share award at vesting ($70,000 ×.35 = $24,500).

To adjust current tax expense and current taxes payable to recognize the current tax benefit from deductible compensation cost upon vesting of share award.

> > Example 9: Share Award Granted by a Nonpublic Entity That Uses the Calculated Value Method

[Note: Paragraph 718-20-55-76 is amended and paragraphs 718-20-55-76A through 55-76B are added in Issue 4. They are shown here for context.]

718-20-55-76 This Example illustrates the guidance in

paragraph 718-10-30-20

paragraphs 718-10-30-19A through 30-20.

718-20-55-76A This Example (see paragraphs 718-20-55-77 through 55-83) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, an entity should substitute the historical volatility of an appropriate industry sector index for expected volatility in accordance with paragraph 718-10-30-20 when measuring the grant-date fair value of nonemployee awards with similar facts and circumstances (that is, an entity has determined that it is not practicable for it to estimate the expected volatility of its share price), as illustrated in paragraphs 718-20-55-77 through 55-80. Therefore, the guidance in those paragraphs may serve as implementation guidance for similar nonemployee awards.

718-20-55-76B Compensation cost attribution for awards to nonemployees may be the same as or different from that which is illustrated in paragraph 718-20-55-81 for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.

718-20-55-77 On January 1, 20X6, Entity W, a small nonpublic entity that develops, manufactures, and distributes medical equipment, grants 100 share options to each of its 100 employees. The share price at the grant date is $7. The options are granted at-the-money, cliff vest at the end of 3 years, and have a 10-year contractual term. Entity W estimates the expected term of the share options granted as 5 years and the risk-free rate as 3.75 percent. For simplicity, this Example assumes that no forfeitures occur during the vesting period and that no dividends are expected to be paid in the future, and this Example does not reflect the accounting for income tax consequences of the awards.

718-20-55-78 Entity W does not maintain an internal market for its shares, which are rarely traded privately. It has not issued any new equity or convertible debt instruments for several years and has been unable to identify any similar entities that are public. Entity W has determined that it is not practicable for it to estimate the expected volatility of its share price and, therefore, it is not possible for it to reasonably estimate the grant-date fair value of the share options. Accordingly, Entity W is required to apply the provisions of paragraph 718-10-30-20 in accounting for the share options under the calculated value method.

718-20-55-79 Entity W operates exclusively in the medical equipment industry. It visits the Dow Jones Indexes website and, using the Industry Classification Benchmark, reviews the various industry sector components of the Dow Jones U.S. Total Market Index. It identifies the medical equipment subsector, within the health care equipment and services sector, as the most appropriate industry sector in relation to its operations. It reviews the current components of the medical equipment index and notes that, based on the most recent assessment of its share price and its issued share capital, in terms of size it would rank among entities in the index with a small market capitalization (or small-cap entities). Entity W selects the small-cap version of the medical equipment index as an appropriate industry sector index because it considers that index to be representative of its size and the industry sector in which it operates. Entity W obtains the historical daily closing total return values of the selected index for the five years immediately before January 1, 20X6, from the Dow Jones Indexes website. It calculates the annualized historical volatility of those values to be 24 percent, based on 252 trading days per year.

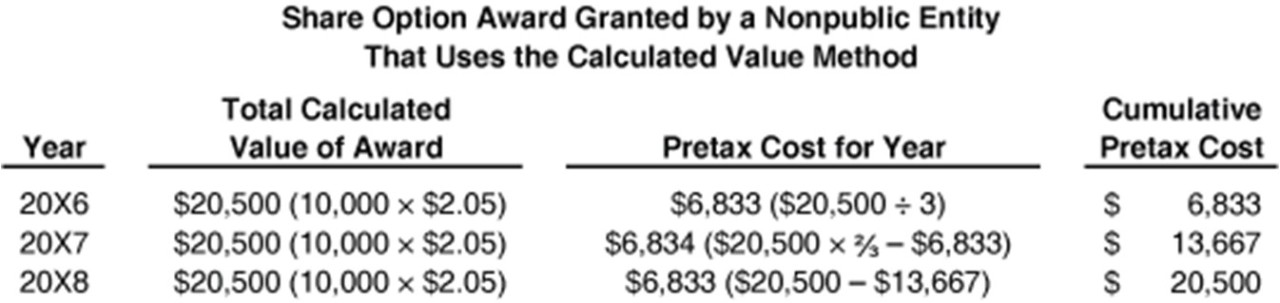

718-20-55-80 Entity W uses the inputs that it has determined above in a Black-Scholes-Merton option-pricing formula, which produces a value of $2.05 per share option. This results in total compensation cost of $20,500 (10,000 × $2.05) to be accounted for over the requisite service period of 3 years.

718-20-55-81 For each of the 3 years ending December 31, 20X6, 20X7, and 20X8, Entity W will recognize compensation cost of $6,833 ($20,500 ÷ 3). The journal entry for each year is as follows.

To recognize compensation cost.

718-20-55-82 The share option award granted by a nonpublic entity that used the calculated value method is as follows.

718-20-55-83 Assuming that all 10,000 share options are exercised on the same day in 20Y2, the accounting for the option exercise will follow the same pattern as in Example 1, Case A (see paragraph 718-20-55-10) and will result in the following journal entry.

At exercise the journal entry is as follows.

To recognize the issuance of shares upon exercise of options and to reclassify previously recognized paid-in capital.

> > Example 10: Share Award with a Clawback Feature

718-20-55-84 This Example illustrates the guidance in paragraph 718-20-35-2.

718-20-55-84A This Example (see paragraphs 718-20-55-85 through 55-86) describes employee awards. However, the principles on how to account for the various aspects of employee awards, except for the compensation cost attribution and certain inputs to valuation, are the same for nonemployee awards. Consequently, the accounting for a contingent feature (such as a clawback) of an award that might cause a grantee to return to the entity either equity instruments earned or realized gains from the sale of the equity instruments earned is equally applicable to nonemployee awards with the same feature as the awards in this Example (that is, the clawback feature). Therefore, the guidance in this Example also serves as implementation guidance for similar nonemployee awards.

718-20-55-84B Compensation cost attribution for awards to nonemployees may be the same or different for employee awards. That is because an entity is required to recognize compensation cost for nonemployee awards in the same manner as if the entity had paid cash in accordance with paragraph 718-10-25-2C. Additionally, valuation amounts used in this Example could be different because an entity may elect to use the contractual term as the expected term of share options and similar instruments when valuing nonemployee share-based payment transactions.