3. Add Subtopic 842-10, with a link to transition paragraph 842-10-65-1, as follows.

[For ease of readability, the new Subtopic is not underlined.]

Leases—Overall

Overview and Background

General

842-10-05-1 The Leases Topic includes the following Subtopics:

- Overall

- Lessee

- Lessor

- Sale and Leaseback Transactions

- Leveraged Lease Arrangements.

842-10-05-2 The Subtopics listed in paragraph 842-10-05-1 establish the requirements of financial accounting and reporting for lessees and lessors.

Objectives

General

842-10-10-1 This Topic specifies the accounting for leases. An entity should consider the terms and conditions of the contract and all relevant facts and circumstances when applying this Topic. An entity should apply this Topic consistently to leases with similar characteristics and in similar circumstances.

842-10-10-2 The objective of this Topic is to establish the principles that lessees and lessors shall apply to report useful information to users of financial statements about the amount, timing, and uncertainty of cash flows arising from a lease.

Scope and Scope Exceptions

General

842-10-15-1 An entity shall apply this Topic to all leases, including subleases. Because a lease is defined as a contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration, this Topic does not apply to any of the following:

- Leases of intangible assets (see Topic 350, Intangibles—Goodwill and Other).

- Leases to explore for or use minerals, oil, natural gas, and similar nonregenerative resources (see Topics 930, Extractive Activities— Mining, and 932, Extractive Activities—Oil and Gas). This includes the intangible right to explore for those natural resources and rights to use the land in which those natural resources are contained (that is, unless those rights of use include more than the right to explore for natural resources), but not equipment used to explore for the natural resources.

- Leases of biological assets, including timber (see Topic 905, Agriculture).

- Leases of inventory (see Topic 330, Inventory).

- Leases of assets under construction (see Topic 360, Property, Plant, and Equipment).

> Identifying a Lease

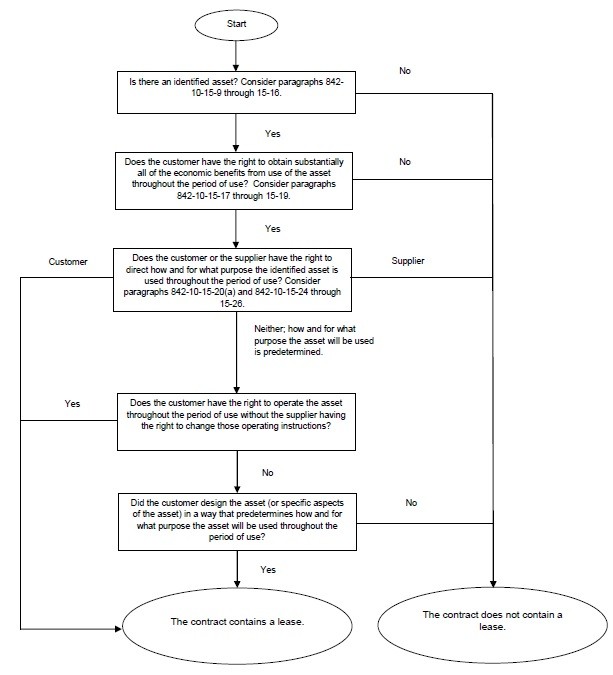

842-10-15-2 At inception of a contract, an entity shall determine whether that contract is or contains a lease.

842-10-15-3 A contract is or contains a lease if the contract conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration. A period of time may be described in terms of the amount of use of an identified asset (for example, the number of production units that an item of equipment will be used to produce).

842-10-15-4 To determine whether a contract conveys the right to control the use of an identified asset (see paragraphs 842-10-15-17 through 15-26) for a period of time, an entity shall assess whether, throughout the period of use, the customer has both of the following:

- The right to obtain substantially all of the economic benefits from use of the identified asset (see paragraphs 842-10-15-17 through 15-19)

- The right to direct the use of the identified asset (see paragraphs 842-10-15-20 through 15-26).

If the customer in the contract is a joint operation or a joint arrangement, an entity shall consider whether the joint operation or joint arrangement has the right to control the use of an identified asset throughout the period of use.

842-10-15-5 If the customer has the right to control the use of an identified asset for only a portion of the term of the contract, the contract contains a lease for that portion of the term.

842-10-15-6 An entity shall reassess whether a contract is or contains a lease only if the terms and conditions of the contract are changed.

842-10-15-7 In making the determination about whether a contract is or contains a lease, an entity shall consider all relevant facts and circumstances.

842-10-15-8 Paragraph 842-10-55-1 includes a flowchart that depicts the decision process for evaluating whether a contract is or contains a lease.

> > Identified Asset

842-10-15-9 An asset typically is identified by being explicitly specified in a contract. However, an asset also can be identified by being implicitly specified at the time that the asset is made available for use by the customer.

> > > Substantive Substitution Rights

842-10-15-10 Even if an asset is specified, a customer does not have the right to use an identified asset if the supplier has the substantive right to substitute the asset throughout the period of use. A supplier's right to substitute an asset is substantive only if both of the following conditions exist:

- The supplier has the practical ability to substitute alternative assets throughout the period of use (for example, the customer cannot prevent the supplier from substituting an asset, and alternative assets are readily available to the supplier or could be sourced by the supplier within a reasonable period of time).

- The supplier would benefit economically from the exercise of its right to substitute the asset (that is, the economic benefits associated with substituting the asset are expected to exceed the costs associated with substituting the asset).

842-10-15-11 An entity's evaluation of whether a supplier's substitution right is substantive is based on facts and circumstances at inception of the contract and shall exclude consideration of future events that, at inception, are not considered likely to occur. Examples of future events that, at inception of the contract, would not be considered likely to occur and, thus, should be excluded from the evaluation include, but are not limited to, the following:

- An agreement by a future customer to pay an above-market rate for use of the asset

- The introduction of new technology that is not substantially developed at inception of the contract

- A substantial difference between the customer's use of the asset, or the performance of the asset and the use or performance considered likely at inception of the contract

- A substantial difference between the market price of the asset during the period of use and the market price considered likely at inception of the contract.

842-10-15-12 If the asset is located at the customer's premises or elsewhere, the costs associated with substitution are generally higher than when located at the supplier's premises and, therefore, are more likely to exceed the benefits associated with substituting the asset.

842-10-15-13 If the supplier has a right or an obligation to substitute the asset only on or after either a particular date or the occurrence of a specified event, the supplier does not have the practical ability to substitute alternative assets throughout the period of use.

842-10-15-14 The supplier's right or obligation to substitute an asset for repairs or maintenance, if the asset is not operating properly, or if a technical upgrade becomes available, does not preclude the customer from having the right to use an identified asset.

842-10-15-15 If the customer cannot readily determine whether the supplier has a substantive substitution right, the customer shall presume that any substitution right is not substantive.

> > > Portions of Assets

842-10-15-16 A capacity portion of an asset is an identified asset if it is physically distinct (for example, a floor of a building or a segment of a pipeline that connects a single customer to the larger pipeline). A capacity or other portion of an asset that is not physically distinct (for example, a capacity portion of a fiber optic cable) is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset.

> > Right to Control the Use of the Identified Asset

> > > Right to Obtain the Economic Benefits from the Use of the Identified Asset

842-10-15-17 To control the use of an identified asset, a customer is required to have the right to obtain substantially all of the economic benefits from use of the asset throughout the period of use (for example, by having exclusive use of the asset throughout that period). A customer can obtain economic benefits from use of an asset directly or indirectly in many ways, such as by using, holding, or subleasing the asset. The economic benefits from use of an asset include its primary output and by-products (including potential cash flows derived from these items) and other economic benefits from using the asset that could be realized from a commercial transaction with a third party.

842-10-15-18 When assessing the right to obtain substantially all of the economic benefits from use of an asset, an entity shall consider the economic benefits that result from use of the asset within the defined scope of a customer's right to use the asset in the contract (see paragraph 842-10-15-23). For example:

- If a contract limits the use of a motor vehicle to only one particular territory during the period of use, an entity shall consider only the economic benefits from use of the motor vehicle within that territory and not beyond.

- If a contract specifies that a customer can drive a motor vehicle only up to a particular number of miles during the period of use, an entity shall consider only the economic benefits from use of the motor vehicle for the permitted mileage and not beyond.

842-10-15-19 If a contract requires a customer to pay the supplier or another party a portion of the cash flows derived from use of an asset as consideration, those cash flows paid as consideration shall be considered to be part of the economic benefits that the customer obtains from use of the asset. For example, if a customer is required to pay the supplier a percentage of sales from use of retail space as consideration for that use, that requirement does not prevent the customer from having the right to obtain substantially all of the economic benefits from use of the retail space. That is because the cash flows arising from those sales are considered to be economic benefits that the customer obtains from use of the retail space, a portion of which it then pays to the supplier as consideration for the right to use that space.

> > > Right to Direct the Use of the Identified Asset

842-10-15-20 A customer has the right to direct the use of an identified asset throughout the period of use in either of the following situations:

a. The customer has the right to direct how and for what purpose the asset is used throughout the period of use (as described in paragraphs 842-10-15-24 through 15-26).

b. The relevant decisions about how and for what purpose the asset is used are predetermined (see paragraph 842-10-15-21) and at least one of the following conditions exists:

1. The customer has the right to operate the asset (or to direct others to operate the asset in a manner that it determines) throughout the period of use without the supplier having the right to change those operating instructions.

2. The customer designed the asset (or specific aspects of the asset) in a way that predetermines how and for what purpose the asset will be used throughout the period of use.

842-10-15-21 The relevant decisions about how and for what purpose an asset is used can be predetermined in a number of ways. For example, the relevant decisions can be predetermined by the design of the asset or by contractual restrictions on the use of the asset.

842-10-15-22 In assessing whether a customer has the right to direct the use of an asset, an entity shall consider only rights to make decisions about the use of the asset during the period of use unless the customer designed the asset (or specific aspects of the asset) in accordance with paragraph 842-10-15-20(b)(2).

Consequently, unless that condition exists, an entity shall not consider decisions that are predetermined before the period of use. For example, if a customer is able only to specify the output of an asset before the period of use, the customer does not have the right to direct the use of that asset. The ability to specify the output in a contract before the period of use, without any other decision-making rights relating to the use of the asset, gives a customer the same rights as any customer that purchases goods or services.

> > > > Protective Rights

842-10-15-23 A contract may include terms and conditions designed to protect the supplier's interest in the asset or other assets, to protect its personnel, or to ensure the supplier's compliance with laws or regulations. These are examples of protective rights. For example, a contract may specify the maximum amount of use of an asset or limit where or when the customer can use the asset, may require a customer to follow particular operating practices, or may require a customer to inform the supplier of changes in how an asset will be used. Protective rights typically define the scope of the customer's right of use but do not, in isolation, prevent the customer from having the right to direct the use of an asset.

> > > > How and for What Purpose an Asset Is Used

842-10-15-24 A customer has the right to direct how and for what purpose an asset is used throughout the period of use if, within the scope of its right of use defined in the contract, it can change how and for what purpose the asset is used throughout that period. In making this assessment, an entity considers the decision-making rights that are most relevant to changing how and for what purpose an asset is used throughout the period of use. Decision-making rights are relevant when they affect the economic benefits to be derived from use. The decision-making rights that are most relevant are likely to be different for different contracts, depending on the nature of the asset and the terms and conditions of the contract.

842-10-15-25 Examples of decision-making rights that, depending on the circumstances, grant the right to direct how and for what purpose an asset is used, within the defined scope of the customer's right of use, include the following:

- The right to change the type of output that is produced by the asset (for example, deciding whether to use a shipping container to transport goods or for storage, or deciding on the mix of products sold from a retail unit)

- The right to change when the output is produced (for example, deciding when an item of machinery or a power plant will be used)

- The right to change where the output is produced (for example, deciding on the destination of a truck or a ship or deciding where a piece of equipment is used or deployed)

- The right to change whether the output is produced and the quantity of that output (for example, deciding whether to produce energy from a power plant and how much energy to produce from that power plant).

842-10-15-26 Examples of decision-making rights that do not grant the right to direct how and for what purpose an asset is used include rights that are limited to operating or maintaining the asset. Although rights such as those to operate or maintain an asset often are essential to the efficient use of an asset, they are not rights to direct how and for what purpose the asset is used and often are dependent on the decisions about how and for what purpose the asset is used. Such rights (that is, to operate or maintain the asset) can be held by the customer or the supplier. The supplier often holds those rights to protect its investment in the asset. However, rights to operate an asset may grant the customer the right to direct the use of the asset if the relevant decisions about how and for what purpose the asset is used are predetermined (see paragraph 842-10-15-20(b)(1)).

842-10-15-27 See Examples 1 through 10 (paragraphs 842-10-55-41 through 55-130) for illustrations of the requirements for identifying a lease.

> Separating Components of a Contract

842-10-15-28 After determining that a contract contains a lease in accordance with paragraphs 842-10-15-2 through 15-27, an entity shall identify the separate lease components within the contract. An entity shall consider the right to use an underlying asset to be a separate lease component (that is, separate from any other lease components of the contract) if both of the following criteria are met:

- The lessee can benefit from the right of use either on its own or together with other resources that are readily available to the lessee. Readily available resources are goods or services that are sold or leased separately (by the lessor or other suppliers) or resources that the lessee already has obtained (from the lessor or from other transactions or events).

- The right of use is neither highly dependent on nor highly interrelated with the other right(s) to use underlying assets in the contract. A lessee's right to use an underlying asset is highly dependent on or highly interrelated with another right to use an underlying asset if each right of use significantly affects the other.

842-10-15-29 The guidance in paragraph 842-10-15-28 notwithstanding, to classify and account for a lease of land and other assets, an entity shall account for the right to use land as a separate lease component unless the accounting effect of doing so would be insignificant (for example, separating the land element would have no effect on lease classification of any lease component or the amount recognized for the land lease component would be insignificant).

842-10-15-30 The consideration in the contract shall be allocated to each separate lease component and nonlease component of the contract (see paragraphs 842-10-15-33 through 15-37 for lessee allocation guidance and paragraphs 842-10-15-38 through 15-42 for lessor allocation guidance). Components of a contract include only those items or activities that transfer a good or service to the lessee. Consequently, the following are not components of a contract and do not receive an allocation of the consideration in the contract:

- Administrative tasks to set up a contract or initiate the lease that do not transfer a good or service to the lessee

- Reimbursement or payment of the lessor's costs. For example, a lessor may incur various costs in its role as a lessor or as owner of the underlying asset. A requirement for the lessee to pay those costs, whether directly to a third party or as a reimbursement to the lessor, does not transfer a good or service to the lessee separate from the right to use the underlying asset.

842-10-15-31 An entity shall account for each separate lease component separately from the nonlease components of the contract (that is, unless a lessee makes the accounting policy election described in paragraph 842-10-15-37). Nonlease components are not within the scope of this Topic and shall be accounted for in accordance with other Topics.

842-10-15-32 See Examples 11 through 14 (paragraphs 842-10-55-131 through 55-158) for illustrations of the requirements for allocating consideration to components of a contract.

> > Lessee

842-10-15-33 A lessee shall allocate (that is, unless the lessee makes the accounting policy election described in paragraph 842-10-15-37) the consideration in the contract to the separate lease components determined in accordance with paragraphs 842-10-15-28 through 15-31 and the nonlease components as follows:

- The lessee shall determine the relative standalone price of the separate lease components and the nonlease components on the basis of their observable standalone prices. If observable standalone prices are not readily available, the lessee shall estimate the standalone prices, maximizing the use of observable information. A residual estimation approach may be appropriate if the standalone price for a component is highly variable or uncertain.

- The lessee shall allocate the consideration in the contract on a relative standalone price basis to the separate lease components and the nonlease components of the contract.

Initial direct costs should be allocated to the separate lease components on the same basis as the lease payments.

842-10-15-34 A price is observable if it is the price that either the lessor or similar suppliers sell similar lease or nonlease components on a standalone basis.

842-10-15-35 The consideration in the contract for a lessee includes all of the payments described in paragraph 842-10-30-5, as well as all of the following payments that will be made during the lease term:

- Any fixed payments (for example, monthly service charges) or in substance fixed payments, less any incentives paid or payable to the lessee, other than those included in paragraph 842-10-30-5

- Any other variable payments that depend on an index or a rate, initially measured using the index or rate at the commencement date.

842-10-15-36 A lessee shall remeasure and reallocate the consideration in the contract upon either of the following:

- A remeasurement of the lease liability (for example, a remeasurement resulting from a change in the lease term or a change in the assessment of whether a lessee is or is not reasonably certain to exercise an option to purchase the underlying asset) (see paragraph 842-20-35-4)

- The effective date of a contract modification that is not accounted for as a separate contract (see paragraph 842-10-25-8).

842-10-15-37 As a practical expedient, a lessee may, as an accounting policy election by class of underlying asset, choose not to separate nonlease components from lease components and instead to account for each separate lease component and the nonlease components associated with that lease component as a single lease component.

> > Lessor

842-10-15-38 A lessor shall allocate the consideration in the contract to the separate lease components and the nonlease components using the requirements in paragraphs 606-10-32-28 through 32-41. A lessor also shall allocate any capitalized costs (for example, initial direct costs or contract costs capitalized in accordance with Subtopic 340-40 on other assets and deferred costs—contracts with customers) to the separate lease components or nonlease components to which those costs relate.

842-10-15-39 The consideration in the contract for a lessor includes all of the amounts described in paragraph 842-10-15-35 and any other variable payment amounts that would be included in the transaction price in accordance with the guidance on variable consideration in Topic 606 on revenue from contracts with customers that specifically relates to either of the following:

- The lessor's efforts to transfer one or more goods or services that are not leases

- An outcome from transferring one or more goods or services that are not leases.

Any variable payment amounts accounted for as consideration in the contract shall be allocated entirely to the nonlease component(s) to which the variable payment specifically relates if doing so would be consistent with the transaction price allocation objective in paragraph 606-10-32-28.

842-10-15-40 If the terms of a variable payment amount other than those in paragraph 842-10-15-35 relate to a lease component, even partially, the lessor shall recognize those payments as income in profit or loss in the period when the changes in facts and circumstances on which the variable payment is based occur (for example, when the lessee's sales on which the amount of the variable payment depends occur).

842-10-15-41 A lessor shall remeasure and reallocate the remaining consideration in the contract when there is a contract modification that is not accounted for as a separate contract in accordance with paragraph 842-10-25-8.

842-10-15-42 If the consideration in the contract changes, a lessor shall allocate those changes in accordance with the requirements in paragraphs 606-10-32-42 through 32-45.

> Other Considerations

842-10-15-43 Paragraph 815-10-15-79 explains that leases that are within the scope of this Topic are not derivative instruments subject to Subtopic 815-10 on derivatives and hedging although a derivative instrument embedded in a lease may be subject to the requirements of Section 815-15-25. Paragraph 815-10-15-80 explains that residual value guarantees that are subject to the guidance in this Topic are not subject to the guidance in Subtopic 815-10. Paragraph 815-10-15-81 requires that a third-party residual value guarantor consider the guidance in Subtopic 815-10 for all residual value guarantees that it provides to determine whether they are derivative instruments and whether they qualify for any of the scope exceptions in that Subtopic.

Glossary

Acquiree

The business or businesses that the acquirer obtains control of in a business combination. This term also includes a nonprofit activity or business that a not-for-profit acquirer obtains control of in an acquisition by a not-for-profit entity.

Acquirer

The entity that obtains control of the acquiree. However, in a business combination in which a variable interest entity (VIE) is acquired, the primary beneficiary of that entity always is the acquirer.

Acquisition by a Not-for-Profit Entity

A transaction or other event in which a not-for-profit acquirer obtains control of one or more nonprofit activities or businesses and initially recognizes their assets and liabilities in the acquirers financial statements. When applicable guidance in Topic 805 is applied by a not-for-profit entity, the term business combination has the same meaning as this term has for a for-profit entity. Likewise, a reference to business combinations in guidance that links to Topic 805 has the same meaning as a reference to acquisitions by not-for-profit entities.

Advance Refunding

A transaction involving the issuance of new debt to replace existing debt with the proceeds from the new debt placed in trust or otherwise restricted to retire the existing debt at a determinable future date or dates.

Business

An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants. Additional guidance on what a business consists of is presented in paragraphs 805-10-55-4 through 55-9

Business Combination

A transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as true mergers or mergers of equals also are business combinations. See also Acquisition by a Not-for-Profit Entity.

Commencement Date of the Lease (Commencement Date)

The date on which a lessor makes an underlying asset available for use by a lessee. See paragraphs 842-10-55-19 through 55-21 for implementation guidance on the commencement date.

Consideration in the Contract

See paragraph 842-10-15-35 for what constitutes the consideration in the contract for lessees and paragraph 842-10-15-39 for what constitutes consideration in the contract for lessors.

Contract

An agreement between two or more parties that creates enforceable rights and obligations.

Direct Financing Lease

From the perspective of a lessor, a lease that meets none of the criteria in paragraph 842-10-25-2 but meets the criteria in paragraph 842-10-25-3(b).

Discount Rate for the Lease

For a lessee, the discount rate for the lease is the rate implicit in the lease unless that rate cannot be readily determined. In that case, the lessee is required to use its incremental borrowing rate.

For a lessor, the discount rate for the lease is the rate implicit in the lease.

Economic Life

Either the period over which an asset is expected to be economically usable by one or more users or the number of production or similar units expected to be obtained from an asset by one or more users.

Effective Date of the Modification

The date that a lease modification is approved by both the lessee and the lessor.

Fair Value (second definition)

The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Finance Lease

From the perspective of a lessee, a lease that meets one or more of the criteria in paragraph 842-10-25-2.

Fiscal Funding Clause

A provision by which the lease is cancellable if the legislature or other funding authority does not appropriate the funds necessary for the governmental unit to fulfill its obligations under the lease agreement.

Incremental Borrowing Rate

The rate of interest that a lessee would have to pay to borrow on a collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment.

Initial Direct Costs

Incremental costs of a lease that would not have been incurred if the lease had not been obtained.

Inventory

The aggregate of those items of tangible personal property that have any of the following characteristics:

- Held for sale in the ordinary course of business

- In process of production for such sale

- To be currently consumed in the production of goods or services to be available for sale.

The term inventory embraces goods awaiting sale (the merchandise of a trading concern and the finished goods of a manufacturer), goods in the course of production (work in process), and goods to be consumed directly or indirectly in production (raw materials and supplies). This definition of inventories excludes long-term assets subject to depreciation accounting, or goods which, when put into use, will be so classified. The fact that a depreciable asset is retired from regular use and held for sale does not indicate that the item should be classified as part of the inventory. Raw materials and supplies purchased for production may be used or consumed for the construction of long-term assets or other purposes not related to production, but the fact that inventory items representing a small portion of the total may not be absorbed ultimately in the production process does not require separate classification. By trade practice, operating materials and supplies of certain types of entities such as oil producers are usually treated as inventory.

Lease

A contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.

Lease Liability

A lessee's obligation to make the lease payments arising from a lease, measured on a discounted basis.

Lease Modification

A change to the terms and conditions of a contract that results in a change in the scope of or the consideration for a lease (for example, a change to the terms and conditions of the contract that adds or terminates the right to use one or more underlying assets or extends or shortens the contractual lease term).

Lease Payments

See paragraph 842-10-30-5 for what constitutes lease payments from the perspective of a lessee and a lessor.

Lease Receivable

A lessor's right to receive lease payments arising from a sales-type lease or a direct financing lease plus any amount that a lessor expects to derive from the underlying asset following the end of the lease term to the extent that it is guaranteed by the lessee or any other third party unrelated to the lessor, measured on a discounted basis.

Lease Term

The noncancellable period for which a lessee has the right to use an underlying asset, together with all of the following:

- Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option

- Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option

- Periods covered by an option to extend (or not to terminate) the lease in which exercise of the option is controlled by the lessor.

Legal Entity

Any legal structure used to conduct activities or to hold assets. Some examples of such structures are corporations, partnerships, limited liability companies, grantor trusts, and other trusts.

Lessee

An entity that enters into a contract to obtain the right to use an underlying asset for a period of time in exchange for consideration.

Lessor

An entity that enters into a contract to provide the right to use an underlying asset for a period of time in exchange for consideration.

Leveraged Lease

From the perspective of a lessor, a lease that was classified as a leveraged lease in accordance with the leases guidance in effect before the effective date and for which the commencement date is before the effective date.

Market Participants

Buyers and sellers in the principal (or most advantageous) market for the asset or liability that have all of the following characteristics:

- They are independent of each other, that is, they are not related parties, although the price in a related-party transaction may be used as an input to a fair value measurement if the reporting entity has evidence that the transaction was entered into at market terms

- They are knowledgeable, having a reasonable understanding about the asset or liability and the transaction using all available information, including information that might be obtained through due diligence efforts that are usual and customary

- They are able to enter into a transaction for the asset or liability

- They are willing to enter into a transaction for the asset or liability, that is, they are motivated but not forced or otherwise compelled to do so.

Net Investment in the Lease

For a sales-type lease, the sum of the lease receivable and the unguaranteed residual asset.

For a direct financing lease, the sum of the lease receivable and the unguaranteed residual asset, net of any deferred selling profit.

Not-for-Profit Entity

An entity that possesses the following characteristics, in varying degrees, that distinguish it from a business entity:

- Contributions of significant amounts of resources from resource providers who do not expect commensurate or proportionate pecuniary return

- Operating purposes other than to provide goods or services at a profit

- Absence of ownership interests like those of business entities.

Entities that clearly fall outside this definition include the following:

- All investor-owned entities

- Entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants, such as mutual insurance entities, credit unions, farm and rural electric cooperatives, and employee benefit plans.

Operating Lease

From the perspective of a lessee, any lease other than a finance lease.

From the perspective of a lessor, any lease other than a sales-type lease or a direct financing lease.

Orderly Transaction

A transaction that assumes exposure to the market for a period before the measurement date to allow for marketing activities that are usual and customary for transactions involving such assets or liabilities; it is not a forced transaction (for example, a forced liquidation or distress sale).

Penalty

Any requirement that is imposed or can be imposed on the lessee by the lease agreement or by factors outside the lease agreement to do any of the following:

a. Disburse cash

b. Incur or assume a liability

c. Perform services

d. Surrender or transfer an asset or rights to an asset or otherwise forego an economic benefit, or suffer an economic detriment. Factors to consider in determining whether an economic detriment may be incurred include, but are not limited to, all of the following:

1. The uniqueness of purpose or location of the underlying asset

2. The availability of a comparable replacement asset

3. The relative importance or significance of the underlying asset to the continuation of the lessee's line of business or service to its customers

4. The existence of leasehold improvements or other assets whose value would be impaired by the lessee vacating or discontinuing use of the underlying asset

5. Adverse tax consequences

6.The ability or willingness of the lessee to bear the cost associated with relocation or replacement of the underlying asset at market rental rates or to tolerate other parties using the underlying asset.

Period of Use

The total period of time that an asset is used to fulfill a contract with a customer (including the sum of any nonconsecutive periods of time).

Probable (second definition)

The future event or events are likely to occur.

Public Business Entity

A public business entity is a business entity meeting any one of the criteria below. Neither a not-for-profit entity nor an employee benefit plan is a business entity.

- It is required by the U.S. Securities and Exchange Commission (SEC) to file or furnish financial statements, or does file or furnish financial statements (including voluntary filers), with the SEC (including other entities whose financial statements or financial information are required to be or are included in a filing).

- It is required by the Securities Exchange Act of 1934 (the Act), as amended, or rules or regulations promulgated under the Act, to file or furnish financial statements with a regulatory agency other than the SEC.

- It is required to file or furnish financial statements with a foreign or domestic regulatory agency in preparation for the sale of or for purposes of issuing securities that are not subject to contractual restrictions on transfer.

- It has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market.

- It has one or more securities that are not subject to contractual restrictions on transfer, and it is required by law, contract, or regulation to prepare U.S. GAAP financial statements (including footnotes) and make them publicly available on a periodic basis (for example, interim or annual periods). An entity must meet both of these conditions to meet this criterion.

An entity may meet the definition of a public business entity solely because its financial statements or financial information is included in another entity's filing with the SEC. In that case, the entity is only a public business entity for purposes of financial statements that are filed or furnished with the SEC.

Rate Implicit in the Lease

The rate of interest that, at a given date, causes the aggregate present value of (a) the lease payments and (b) the amount that a lessor expects to derive from the underlying asset following the end of the lease term to equal the sum of (1) the fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and (2) any deferred initial direct costs of the lessor.

Related Parties

Related parties include:

- Affiliates of the entity

- Entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of Section 825-10-15, to be accounted for by the equity method by the investing entity

- Trusts for the benefit of employees, such as pension and profit-sharing trusts that are managed by or under the trusteeship of management

- Principal owners of the entity and members of their immediate families

- Management of the entity and members of their immediate families

- Other parties with which the entity may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests

- Other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

Remote

The chance of the future event or events occurring is slight.

Residual Value Guarantee

A guarantee made to a lessor that the value of an underlying asset returned to the lessor at the end of a lease will be at least a specified amount.

Right-of-Use Asset

An asset that represents a lessee's right to use an underlying asset for the lease term.

Sales-Type Lease

From the perspective of a lessor, a lease that meets one or more of the criteria in paragraph 842-10-25-2.

Selling Profit or Selling Loss

At the commencement date, selling profit or selling loss equals:

- The fair value of the underlying asset or the sum of (1) the lease receivable and (2) any lease payments prepaid by the lessee, if lower; minus

- The carrying amount of the underlying asset net of any unguaranteed residual asset; minus

- Any deferred initial direct costs of the lessor.

Short-Term Lease

A lease that, at the commencement date, has a lease term of 12 months or less and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

Standalone Price

The price at which a customer would purchase a component of a contract separately.

Sublease

A transaction in which an underlying asset is re-leased by the lessee (or intermediate lessor) to a third party (the sublessee) and the original (or head) lease between the lessor and the lessee remains in effect.

Underlying Asset

An asset that is the subject of a lease for which a right to use that asset has been conveyed to a lessee. The underlying asset could be a physically distinct portion of a single asset.

Unguaranteed Residual Asset

The amount that a lessor expects to derive from the underlying asset following the end of the lease term that is not guaranteed by the lessee or any other third party unrelated to the lessor, measured on a discounted basis.

Variable Interest Entity

A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsections of Subtopic 810-10.

Variable Lease Payments

Payments made by a lessee to a lessor for the right to use an underlying asset that vary because of changes in facts or circumstances occurring after the commencement date, other than the passage of time.

Warranty

A guarantee for which the underlying is related to the performance (regarding function, not price) of nonfinancial assets that are owned by the guaranteed party. The obligation may be incurred in connection with the sale of goods or services; if so, it may require further performance by the seller after the sale has taken place.

Recognition

General

> Lease Classification

842-10-25-1 An entity shall classify each separate lease component at the commencement date. An entity shall not reassess the lease classification after the commencement date unless the contract is modified and the modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8. In addition, a lessee also shall reassess the lease classification after the commencement date if there is a change in the lease term or the assessment of whether the lessee is reasonably certain to exercise an option to purchase the underlying asset.

842-10-25-2 A lessee shall classify a lease as a finance lease and a lessor shall classify a lease as a sales-type lease when the lease meets any of the following criteria at lease commencement:

- The lease transfers ownership of the underlying asset to the lessee by the end of the lease term.

- The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

- The lease term is for the major part of the remaining economic life of the underlying asset. However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease.

- The present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments in accordance with paragraph 842-10-30-5(f) equals or exceeds substantially all of the fair value of the underlying asset.

- The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term.

842-10-25-3 When none of the criteria in paragraph 842-10-25-2 are met:

a. A lessee shall classify the lease as an operating lease.

b. A lessor shall classify the lease as either a direct financing lease or an operating lease. A lessor shall classify the lease as an operating lease unless both of the following criteria are met, in which case the lessor shall classify the lease as a direct financing lease:

1. The present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments in accordance with paragraph 842-10-30-5(f) and/or any other third party unrelated to the lessor equals or exceeds substantially all of the fair value of the underlying asset.

2. It is probable that the lessor will collect the lease payments plus any amount necessary to satisfy a residual value guarantee.

842-10-25-4 A lessor shall assess the criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1) using the rate implicit in the lease. For purposes of assessing the criterion in paragraph 842-10-25-2(d), a lessor shall assume that no initial direct costs will be deferred if, at the commencement date, the fair value of the underlying asset is different from its carrying amount.

842-10-25-5 If a single lease component contains the right to use more than one underlying asset (see paragraphs 842-10-15-28 through 15-29), an entity shall consider the remaining economic life of the predominant asset in the lease component for purposes of applying the criterion in paragraph 842-10-25-2(c).

842-10-25-6 When classifying a sublease, an entity shall classify the sublease with reference to the underlying asset (for example, the item of property, plant, or equipment that is the subject of the lease) rather than with reference to the right-of-use asset.

842-10-25-7 See paragraphs 842-10-55-2 through 55-15 for implementation guidance on lease classification.

> Lease Modifications

842-10-25-8 An entity shall account for a modification to a contract as a separate contract (that is, separate from the original contract) when both of the following conditions are present:

- The modification grants the lessee an additional right of use not included in the original lease (for example, the right to use an additional asset).

- The lease payments increase commensurate with the standalone price for the additional right of use, adjusted for the circumstances of the particular contract. For example, the standalone price for the lease of one floor of an office building in which the lessee already leases other floors in that building may be different from the standalone price of a similar floor in a different office building, because it was not necessary for a lessor to incur costs that it would have incurred for a new lessee.

842-10-25-9 If a lease is modified and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8, the entity shall reassess the classification of the lease as of the effective date of the modification based on its modified terms and conditions and the facts and circumstances as of that date (for example, the fair value and remaining economic life of the underlying asset as of that date).

842-10-25-10 An entity shall account for initial direct costs, lease incentives, and any other payments made to or by the entity in connection with a modification to a lease in the same manner as those items would be accounted for in connection with a new lease.

> > Lessee

842-10-25-11 A lessee shall reallocate the remaining consideration in the contract and remeasure the lease liability using a discount rate for the lease determined at the effective date of the modification if a contract modification does any of the following:

- Grants the lessee an additional right of use not included in the original contract (and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8)

- Extends or reduces the term of an existing lease (for example, changes the lease term from five to eight years or vice versa), other than through the exercise of a contractual option to extend or terminate the lease (as described in paragraph 842-20-35-5)

- Fully or partially terminates an existing lease (for example, reduces the assets subject to the lease)

- Changes the consideration in the contract only.

842-10-25-12 In the case of (a), (b), or (d) in paragraph 842-10-25-11, the lessee shall recognize the amount of the remeasurement of the lease liability for the modified lease as an adjustment to the corresponding right-of-use asset.

842-10-25-13 In the case of (c) in paragraph 842-10-25-11, the lessee shall decrease the carrying amount of the right-of-use asset on a basis proportionate to the full or partial termination of the existing lease. Any difference between the reduction in the lease liability and the proportionate reduction in the right-of-use asset shall be recognized as a gain or a loss at the effective date of the modification.

842-10-25-14 If a finance lease is modified and the modified lease is classified as an operating lease, any difference between the carrying amount of the right-ofuse asset after recording the adjustment required by paragraph 842-10-25-12 or 842-10-25-13 and the carrying amount of the right-of-use asset that would result from applying the initial operating right-of-use asset measurement guidance in paragraph 842-20-30-5 to the modified lease shall be accounted for in the same manner as a rent prepayment or a lease incentive.

> > Lessor

842-10-25-15 If an operating lease is modified and the modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8, the lessor shall account for the modification as if it were a termination of the existing lease and the creation of a new lease that commences on the effective date of the modification as follows:

- If the modified lease is classified as an operating lease, the lessor shall consider any prepaid or accrued lease rentals relating to the original lease as a part of the lease payments for the modified lease.

- If the modified lease is classified as a direct financing lease or a salestype lease, the lessor shall derecognize any deferred rent liability or accrued rent asset and adjust the selling profit or selling loss accordingly.

842-10-25-16 If a direct financing lease is modified and the modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8, the lessor shall account for the modified lease as follows:

- If the modified lease is classified as a direct financing lease, the lessor shall adjust the discount rate for the modified lease so that the initial net investment in the modified lease equals the carrying amount of the net investment in the original lease immediately before the effective date of the modification.

- If the modified lease is classified as a sales-type lease, the lessor shall account for the modified lease in accordance with the guidance applicable to sales-type leases in Subtopic 842-30, with the commencement date of the modified lease being the effective date of the modification. In calculating the selling profit or selling loss on the lease, the fair value of the underlying asset is its fair value at the effective date of the modification and its carrying amount is the carrying amount of the net investment in the original lease immediately before the effective date of the modification.

- If the modified lease is classified as an operating lease, the carrying amount of the underlying asset equals the net investment in the original lease immediately before the effective date of the modification.

842-10-25-17 If a sales-type lease is modified and the modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8, the lessor shall account for the modified lease as follows:

- If the modified lease is classified as a sales-type or a direct financing lease, in the same manner as described in paragraph 842-10-25-16(a)

- If the modified lease is classified as an operating lease, in the same manner as described in paragraph 842-10-25-16(c).

842-10-25-18 See Examples 15 through 22 (paragraphs 842-10-55-159 through 55-209) for illustrations of the requirements on lease modifications.

> Contract Combinations

842-10-25-19 An entity shall combine two or more contracts, at least one of which is or contains a lease, entered into at or near the same time with the same counterparty (or related parties) and consider the contracts as a single transaction if any of the following criteria are met:

- The contracts are negotiated as a package with the same commercial objective(s).

- The amount of consideration to be paid in one contract depends on the price or performance of the other contract.

- The rights to use underlying assets conveyed in the contracts (or some of the rights of use conveyed in the contracts) are a single lease component in accordance with paragraph 842-10-15-28.

Initial Measurement

General

> Lease Term and Purchase Options

842-10-30-1 An entity shall determine the lease term as the noncancellable period of the lease, together with all of the following:

- Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option

- Periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option

- Periods covered by an option to extend (or not to terminate) the lease in which exercise of the option is controlled by the lessor.

842-10-30-2 At the commencement date, an entity shall include the periods described in paragraph 842-10-30-1 in the lease term having considered all relevant factors that create an economic incentive for the lessee (that is, contractbased, asset-based, entity-based, and market-based factors). Those factors shall be considered together, and the existence of any one factor does not necessarily signify that a lessee is reasonably certain to exercise or not to exercise an option.

842-10-30-3 At the commencement date, an entity shall assess an option to purchase the underlying asset on the same basis as an option to extend or not to terminate a lease, as described in paragraph 842-10-30-2.

842-10-30-4 See paragraphs 842-10-55-19 through 55-21 for implementation guidance on commencement date and paragraphs 842-10-55-23 through 55-27 for implementation guidance on lease term and purchase options. See Examples 23 through 24 (paragraphs 842-10-55-210 through 55-224) for illustrations of the requirements on purchase options.

> Initial Measurement of the Lease Payments

842-10-30-5 At the commencement date, the lease payments shall consist of the following payments relating to the use of the underlying asset during the lease term:

- Fixed payments, including in substance fixed payments, less any lease incentives paid or payable to the lessee (see paragraphs 842-10-55-30 through 55-31).

- Variable lease payments that depend on an index or a rate (such as the Consumer Price Index or a market interest rate), initially measured using the index or rate at the commencement date.

- The exercise price of an option to purchase the underlying asset if the lessee is reasonably certain to exercise that option (assessed considering the factors in paragraph 842-10-55-26).

- Payments for penalties for terminating the lease if the lease term (as determined in accordance with paragraph 842-10-30-1) reflects the lessee exercising an option to terminate the lease.

- Fees paid by the lessee to the owners of a special-purpose entity for structuring the transaction. However, such fees shall not be included in the fair value of the underlying asset for purposes of applying paragraph 842-10-25-2(d).

- For a lessee only, amounts probable of being owed by the lessee under residual value guarantees (see paragraphs 842-10-55-34 through 55-36).

842-10-30-6 Lease payments do not include any of the following:

- Variable lease payments other than those in paragraph 842-10-30-5(b)

- Any guarantee by the lessee of the lessor's debt

- Amounts allocated to nonlease components in accordance with paragraphs 842-10-15-33 through 15-42.

842-10-30-7 Paragraph 410-20-15-3(e) addresses the scope application of Subtopic 410-20 on asset retirement obligations to obligations of a lessee in connection with a lease (see paragraph 842-10-55-37).

842-10-30-8 See Example 25 (paragraphs 842-10-55-225 through 55-234) for an illustration of the requirements on lessee accounting for variable lease payments and Example 26 (paragraphs 842-10-55-235 through 55-238) for an illustration of the requirements on termination penalties.

> > Initial Direct Costs

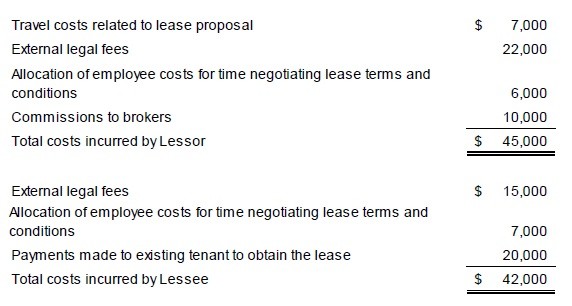

842-10-30-9 Initial direct costs for a lessee or a lessor may include, for example, either of the following:

- Commissions

- Payments made to an existing tenant to incentivize that tenant to terminate its lease.

842-10-30-10 Costs to negotiate or arrange a lease that would have been incurred regardless of whether the lease was obtained, such as fixed employee salaries, are not initial direct costs. The following items are examples of costs that are not initial direct costs:

- General overheads, including, for example, depreciation, occupancy and equipment costs, unsuccessful origination efforts, and idle time

- Costs related to activities performed by the lessor for advertising, soliciting potential lessees, servicing existing leases, or other ancillary activities

- Costs related to activities that occur before the lease is obtained, such as costs of obtaining tax or legal advice, negotiating lease terms and conditions, or evaluating a prospective lessees financial condition.

Subsequent Measurement

General

> Lease Term and Purchase Options

842-10-35-1 A lessee shall reassess the lease term or a lessee option to purchase the underlying asset only if and at the point in time that any of the following occurs:

- There is a significant event or a significant change in circumstances that is within the control of the lessee that directly affects whether the lessee is reasonably certain to exercise or not to exercise an option to extend or terminate the lease or to purchase the underlying asset.

- There is an event that is written into the contract that obliges the lessee to exercise (or not to exercise) an option to extend or terminate the lease.

- The lessee elects to exercise an option even though the entity had previously determined that the lessee was not reasonably certain to do so.

- The lessee elects not to exercise an option even though the entity had previously determined that the lessee was reasonably certain to do so.

842-10-35-2 See paragraphs 842-10-55-28 through 55-29 for implementation guidance on reassessing the lease term and lessee options to purchase the underlying asset.

842-10-35-3 A lessor shall not reassess the lease term or a lessee option to purchase the underlying asset unless the lease is modified and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8. When a lessee exercises an option to extend or terminate the lease or purchase the underlying asset, the lessor shall account for the exercise of that option in the same manner as a lease modification.

> Subsequent Measurement of the Lease Payments

842-10-35-4 A lessee shall remeasure the lease payments if any of the following occur:

a. The lease is modified, and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8.

b. A contingency upon which some or all of the variable lease payments that will be paid over the remainder of the lease term are based is resolved such that those payments now meet the definition of lease payments. For example, an event occurs that results in variable lease payments that were linked to the performance or use of the underlying asset becoming fixed payments for the remainder of the lease term.

c. There is a change in any of the following:

1. The lease term, as described in paragraph 842-10-35-1. A lessee shall determine the revised lease payments on the basis of the revised lease term.

2. The assessment of whether the lessee is reasonably certain to exercise or not to exercise an option to purchase the underlying asset, as described in paragraph 842-10-35-1. A lessee shall determine the revised lease payments to reflect the change in the assessment of the purchase option.

3. Amounts probable of being owed by the lessee under residual value guarantees. A lessee shall determine the revised lease payments to reflect the change in amounts probable of being owed by the lessee under residual value guarantees.

842-10-35-5 When a lessee remeasures the lease payments in accordance with paragraph 842-10-35-4, variable lease payments that depend on an index or a rate shall be measured using the index or rate at the remeasurement date.

842-10-35-6 A lessor shall not remeasure the lease payments unless the lease is modified and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8.

Implementation Guidance and Illustrations

General

> Implementation Guidance

> > Identifying a Lease

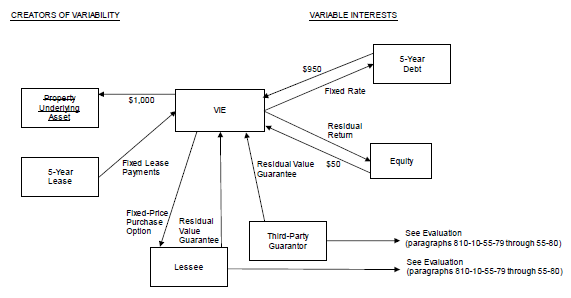

842-10-55-1 The following flowchart depicts the decision process to follow in identifying whether a contract is or contains a lease. The flowchart does not include all of the guidance on identifying a lease in this Subtopic and is not intended as a substitute for the guidance on identifying a lease in this Subtopic.

> > Lease Classification

842-10-55-2 When determining lease classification, one reasonable approach to assessing the criteria in paragraphs 842-10-25-2(c) through (d) and 842-10-25-3(b)(1) would be to conclude:

- Seventy-five percent or more of the remaining economic life of the underlying asset is a major part of the remaining economic life of that underlying asset.

- A commencement date that falls at or near the end of the economic life of the underlying asset refers to a commencement date that falls within the last 25 percent of the total economic life of the underlying asset.

- Ninety percent or more of the fair value of the underlying asset amounts to substantially all the fair value of the underlying asset.

842-10-55-3 In some cases, it may not be practicable for an entity to determine the fair value of an underlying asset. In the context of this Topic, practicable means that a reasonable estimate of fair value can be made without undue cost or effort. It is a dynamic concept; what is practicable for one entity may not be practicable for another, what is practicable in one period may not be practicable in another, and what is practicable for one underlying asset (or class of underlying asset) may not be practicable for another. In those cases in which it is not practicable for an entity to determine the fair value of an underlying asset, lease classification should be determined without consideration of the criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1).

> > > Transfer-of-Ownership Criterion

842-10-55-4 The criterion in paragraph 842-10-25-2(a) is met in leases that provide, upon the lessee's performance in accordance with the terms of the lease, that the lessor should execute and deliver to the lessee such documents (including, if applicable, a bill of sale) as may be required to release the underlying asset from the lease and to transfer ownership to the lessee.

842-10-55-5 The criterion in paragraph 842-10-25-2(a) also is met in situations in which the lease requires the payment by the lessee of a nominal amount (for example, the minimum fee required by the statutory regulation to transfer ownership) in connection with the transfer of ownership.

842-10-55-6 A provision in a lease that ownership of the underlying asset is not transferred to the lessee if the lessee elects not to pay the specified fee (whether nominal or otherwise) to complete the transfer is an option to purchase the underlying asset. Such a provision does not satisfy the transfer-of-ownership criterion in paragraph 842-10-25-2(a).

> > > Alternative Use Criterion

842-10-55-7 In assessing whether an underlying asset has an alternative use to the lessor at the end of the lease term in accordance with paragraph 842-10-25-2(e), an entity should consider the effects of contractual restrictions and practical limitations on the lessor's ability to readily direct that asset for another use (for example, selling it or leasing it to an entity other than the lessee). A contractual restriction on a lessor's ability to direct an underlying asset for another use must be substantive for the asset not to have an alternative use to the lessor. A contractual restriction is substantive if it is enforceable. A practical limitation on a lessor's ability to direct an underlying asset for another use exists if the lessor would incur significant economic losses to direct the underlying asset for another use. A significant economic loss could arise because the lessor either would incur significant costs to rework the asset or would only be able to sell or re-lease the asset at a significant loss. For example, a lessor may be practically limited from redirecting assets that either have design specifications that are unique to the lessee or that are located in remote areas. The possibility of the contract with the customer being terminated is not a relevant consideration in assessing whether the lessor would be able to readily direct the underlying asset for another use.

> > > Effect of Investment Tax Credits

842-10-55-8 When evaluating the lease classification criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1), the fair value of the underlying asset should exclude any related investment tax credit retained by the lessor and expected to be realized by the lessor.

> > > Residual Value Guarantees for a Portfolio of Underlying Assets

842-10-55-9 Lessors may obtain residual value guarantees for a portfolio of underlying assets for which settlement is not solely based on the residual value of the individual underlying assets. In such cases, the lessor is economically assured of receiving a minimum residual value for a portfolio of assets that are subject to separate leases but not for each individual asset. Accordingly, when an asset has a residual value in excess of the "guaranteed" amount, that excess is offset against shortfalls in residual value that exist in other assets in the portfolio.

842-10-55-10 Residual value guarantees of a portfolio of underlying assets preclude a lessor from determining the amount of the guaranteed residual value of any individual underlying asset within the portfolio. Consequently, no such amounts should be considered when evaluating the lease classification criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1).

> > > Lease of an Acquiree

842-10-55-11 In a business combination or an acquisition by a not-for-profit entity, the acquiring entity should retain the previous lease classification in accordance with this Subtopic unless there is a lease modification and that modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8.

> > > Lease of a Related Party

842-10-55-12 Leases between related parties should be classified in accordance with the lease classification criteria applicable to all other leases on the basis of the legally enforceable terms and conditions of the lease. In the separate financial statements of the related parties, the classification and accounting for the leases should be the same as for leases between unrelated parties.

> > > Lease Involving Facilities Owned by a Government Unit or Authority

842-10-55-13 Because of special provisions normally present in leases involving terminal space and other airport facilities owned by a governmental unit or authority, the economic life of such facilities for purposes of classifying a lease is essentially indeterminate. Likewise, it may not be practicable to determine the fair value of the underlying asset. If it is impracticable to determine the fair value of the underlying asset and such leases also do not provide for a transfer of ownership or a purchase option that the lessee is reasonably certain to exercise, they should be classified as operating leases. This guidance also applies to leases of other facilities owned by a governmental unit or authority in which the rights of the parties are essentially the same as in a lease of airport facilities. Examples of such leases may be those involving facilities at ports and bus terminals. The guidance in this paragraph is intended to apply to leases only if all of the following conditions are met:

a. The underlying asset is owned by a governmental unit or authority.

b. The underlying asset is part of a larger facility, such as an airport, operated by or on behalf of the lessor.

c. The underlying asset is a permanent structure or a part of a permanent structure, such as a building, that normally could not be moved to a new location.

d. The lessor, or in some circumstances a higher governmental authority, has the explicit right under the lease agreement or existing statutes or regulations applicable to the underlying asset to terminate the lease at any time during the lease term, such as by closing the facility containing the underlying asset or by taking possession of the facility.

e. The lease neither transfers ownership of the underlying asset to the lessee nor allows the lessee to purchase or otherwise acquire ownership of the underlying asset.

f. The underlying asset or equivalent asset in the same service area cannot be purchased or leased from a nongovernmental unit or authority. An equivalent asset in the same service area is an asset that would allow continuation of essentially the same service or activity as afforded by the underlying asset without any appreciable difference in economic results to the lessee.

842-10-55-14 Leases of underlying assets not meeting all of the conditions in paragraph 842-10-55-13 are subject to the same criteria for classifying leases under this Subtopic that are applicable to leases not involving government-owned property.

> > > Lessee Indemnification for Environmental Contamination

842-10-55-15 A provision that requires lessee indemnification for environmental contamination, whether for environmental contamination caused by the lessee during its use of the underlying asset over the lease term or for preexisting environmental contamination, should not affect the classification of the lease.

> > Lease Modifications

> > > Lease Modifications in Connection with the Refunding of Tax-Exempt Debt

842-10-55-16 In some situations, tax-exempt debt is issued to finance construction of a facility, such as a plant or hospital, that is transferred to a user of the facility by lease. A lease may serve as collateral for the guarantee of payments equivalent to those required to service the tax-exempt debt. Payments required by the terms of the lease are essentially the same, as to both amount and timing, as those required by the tax-exempt debt. A lease modification resulting from a refunding by the lessor of tax-exempt debt (including an advance refunding) should be accounted for in the same manner (that is, in accordance with paragraphs 842-10-25-8 through 25-18) as any other lease modification. For example, if the perceived economic advantages of the refunding are passed through to the lessee in the form of reduced lease payments, the lessee should account for the modification in accordance with paragraph 842-10-25-12, while the lessor should account for the modification in accordance with the applicable guidance in paragraphs 842-10-25-15 through 25-17.

> > > Master Lease Agreements

842-10-55-17 Under a master lease agreement, the lessee may gain control over the use of additional underlying assets during the term of the agreement. If the agreement specifies a minimum number of units or dollar value of equipment, the lessee obtaining control over the use of those additional underlying assets is not a lease modification. Rather, the entity (whether a lessee or a lessor) applies the guidance in paragraphs 842-10-15-28 through 15-42 when identifying the separate lease components and allocating the consideration in the contract to those components. Paragraph 842-10-55-22 explains that a master lease agreement may, therefore, result in multiple commencement dates.

842-10-55-18 If the master lease agreement permits the lessee to gain control over the use of additional underlying assets during the term of the agreement but does not commit the lessee to doing so, the lessee's taking control over the use of an additional underlying asset should be accounted for as a lease modification in accordance with paragraphs 842-10-25-8 through 25-18.

> > Commencement Date

842-10-55-19 In some lease arrangements, the lessor may make the underlying asset available for use by the lessee (for example, the lessee may take possession of or be given control over the use of the underlying asset) before it begins operations or makes lease payments under the terms of the lease. During this period, the lessee has the right to use the underlying asset and does so for the purpose of constructing a lessee asset (for example, leasehold improvements).

842-10-55-20 The contract may require the lessee to make lease payments only after construction is completed and the lessee begins operations. Alternatively, some contracts require the lessee to make lease payments when it takes possession of or is given control over the use of the underlying asset. The timing of when lease payments begin under the contract does not affect the commencement date of the lease.

842-10-55-21 Lease costs (or income) associated with building and ground leases incurred (earned) during and after a construction period are for the right to use the underlying asset during and after construction of a lessee asset. There is no distinction between the right to use an underlying asset during a construction period and the right to use that asset after the construction period. Therefore, lease costs (or income) associated with ground or building leases that are incurred (earned) during a construction period should be recognized by the lessee (or lessor) in accordance with the guidance in Subtopics 842-20 and 842-30, respectively. That guidance does not address whether a lessee that accounts for the sale or rental of real estate projects under Topic 970 should capitalize rental costs associated with ground and building leases.

> > > Master Lease Agreements

842-10-55-22 There may be multiple commencement dates resulting from a master lease agreement. That is because a master lease agreement may cover a significant number of underlying assets, each of which are made available for use by the lessee on different dates. Although a master lease agreement may specify that the lessee must take a minimum number of units or dollar value of equipment, there will be multiple commencement dates unless all of the underlying assets subject to that minimum are made available for use by the lessee on the same date.

> > Lease Term and Purchase Options

842-10-55-23 An entity should determine the noncancellable period of a lease when determining the lease term. When assessing the length of the noncancellable period of a lease, an entity should apply the definition of a contract and determine the period for which the contract is enforceable. A lease is no longer enforceable when both the lessee and the lessor each have the right to terminate the lease without permission from the other party with no more than an insignificant penalty.

842-10-55-24 If only a lessee has the right to terminate a lease, that right is considered to be an option to terminate the lease available to the lessee that an entity considers when determining the lease term, as described in paragraph 842-10-30-1. If only a lessor has the right to terminate a lease, the noncancellable period of the lease includes the period covered by the option to terminate the lease.

842-10-55-25 The lease term begins at the commencement date and includes any rent-free periods provided to the lessee by the lessor.

> > > Reasonably Certain

842-10-55-26 At the commencement date, an entity assesses whether the lessee is reasonably certain to exercise or not to exercise an option by considering all economic factors relevant to that assessment—contract-based, asset-based, market-based, and entity-based factors. An entity's assessment often will require the consideration of a combination of those factors because they are interrelated. Examples of economic factors to consider include, but are not limited to, any of the following:

a. Contractual terms and conditions for the optional periods compared with current market rates, such as:

1. The amount of lease payments in any optional period

2. The amount of any variable lease payments or other contingent payments, such as payments under termination penalties and residual value guarantees