3. Amend paragraphs 230-10-45-4 through 45-5 and 230-10-45-24, with a link to transition paragraph 230-10-65-3, as follows:

Statement of Cash Flows—Overall

Other Presentation Matters

> Form and Content

> > Cash and Cash Equivalents

230-10-45-4 A statement of cash flows shall explain the change during the period in

the total of cash, cash and

cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. The statement shall use descriptive terms such as cash or cash and cash equivalents rather than ambiguous terms such as funds.

The total amounts of cash and cash equivalents at the beginning and end of the period shown in the statement of cash flows shall be the same amounts as similarly titled line items or subtotals shown in the statements of financial position as of those dates

.

When cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents are presented in more than one line item within the statement of financial position, an entity shall provide the disclosures required in paragraph 230-10-50-8.

230-10-45-5 Cash purchases and sales of items commonly considered to be cash equivalents generally are part of the entity's cash management activities rather than part of its operating, investing, and financing activities, and details of those transactions need not be reported in a statement of cash flows. In addition, transfers between cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents are not part of the entity's operating, investing, and financing activities, and details of those transfers are not reported as cash flow activities in the statement of cash flows.

> Classification

> > Reporting Operating, Investing, and Financing Activities

230-10-45-24 A statement of cash flows for a period shall report net cash provided or used by operating, investing, and financing activities and the net effect of those flows on

the total of cash, cash and

cash equivalents

, and amounts generally described as restricted cash or restricted cash equivalents during the period

. The statement of cash flows shall report that information in a manner that reconciles beginning and ending

totals of cash, cash and

cash equivalents

, and amounts generally described as restricted cash or restricted cash equivalents.

4. Add paragraphs 230-10-50-7 through 50-8 and their related heading, with a link to transition paragraph 230-10-65-3, as follows:

Disclosure

> Restrictions on Cash and Cash Equivalents

230-10-50-7 An entity shall disclose information about the nature of restrictions on its cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. An entity within the scope of Topic 958 on not-for-profit entities also shall provide the disclosures required in paragraph 958-210-50-3.

230-10-50-8 When cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents are presented in more than one line item within the statement of financial position, an entity shall, for each period that a statement of financial position is presented, present on the face of the statement of cash flows or disclose in the notes to the financial statements, the line items and amounts of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents reported within the statement of financial position. The amounts, disaggregated by the line item in which they appear within the statement of financial position, shall sum to the total amount of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents at the end of the corresponding period shown in the statement of cash flows. This disclosure may be provided in either a narrative or a tabular format.

5. Amend paragraphs 230-10-55-10, 230-10-55-13, and 230-10-55-19 through 55-20 (by adding item q) and their pending content and add paragraphs 230-10-55-12A and 230-10-55-18A, with a link to transition paragraph 230-10-65-3, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Example 1: Direct and Indirect Method for a Manufacturing Entity

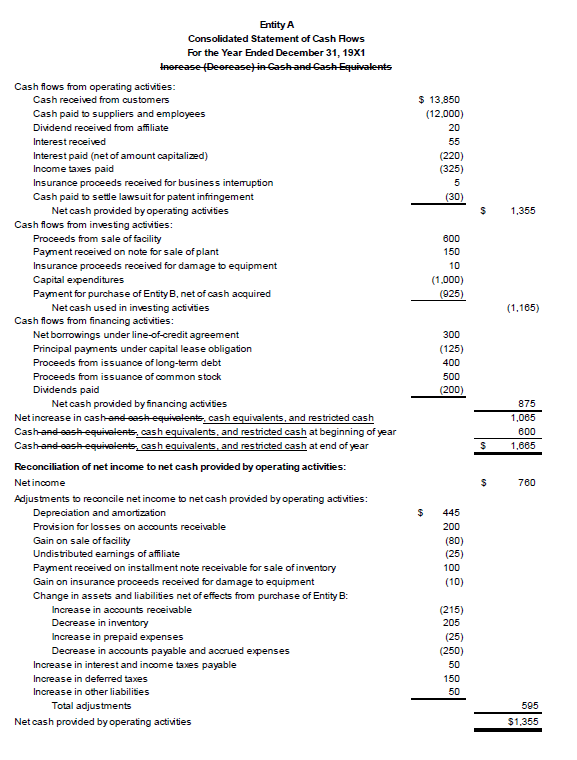

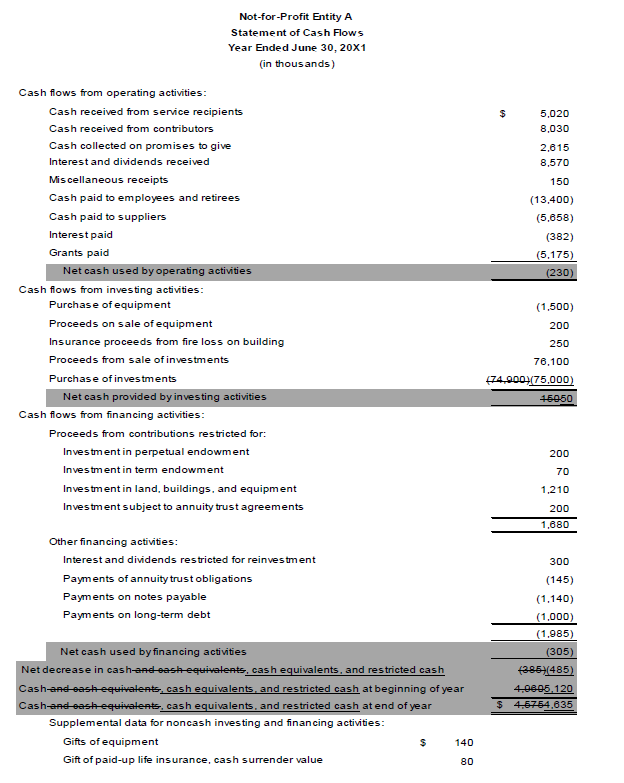

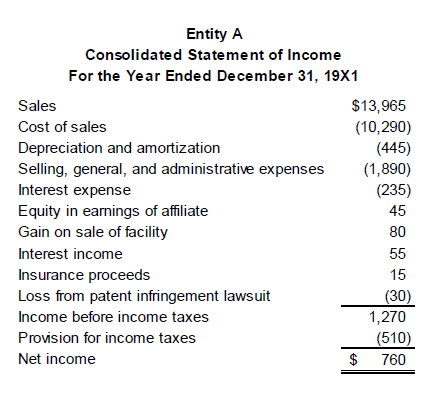

230-10-55-10 The following is a statement of cash flows for the year ended December 31, 19X1, for Entity A, a U.S. corporation engaged principally in manufacturing activities. This statement of cash flows illustrates the direct method of presenting cash flows from operating activities, as encouraged in paragraph 230-10-45-25.

In addition, amend the following pending content for paragraph 230-10-55-10, with no additional link to transition:

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2019 | Transition Guidance: 842-10-65-1

230-10-55-10

The following is a statement of cash flows for the year ended December 31, 19X1, for Entity A, a U.S. corporation engaged principally in manufacturing activities. This statement of cash flows illustrates the direct method of presenting cash flows from operating activities, as encouraged in paragraph 230-10-45-25.

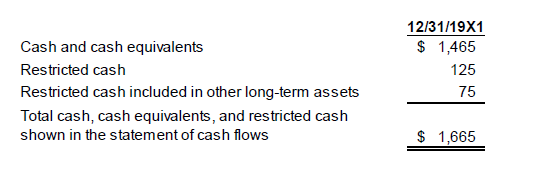

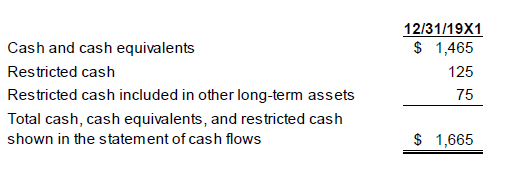

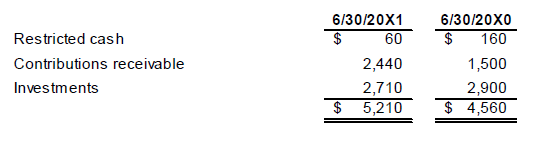

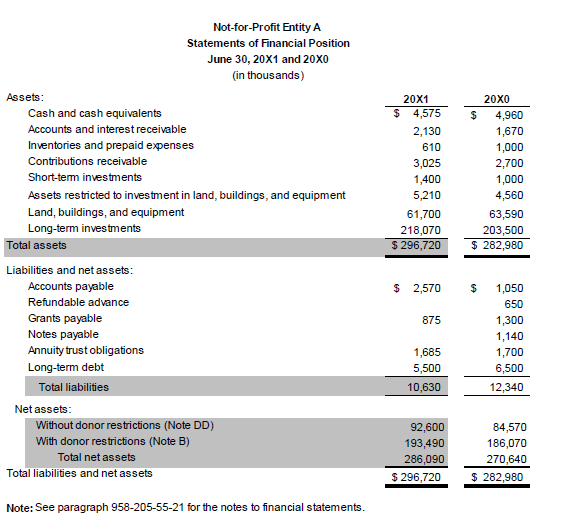

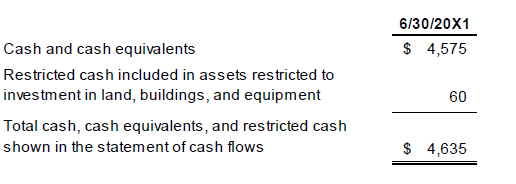

230-10-55-12A Shown below is an illustrative disclosure of the nature of restrictions on cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents required by paragraph 230-10-50-7, as well as an illustrative disclosure of the line items and amounts of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents reported within the statement of financial position that sum to the total of the same such amounts at the end of the period shown in the statement of cash flows as required by paragraph 230-10-50-8 (in this illustrative example, assume Entity A has no restricted cash equivalents). Comparative statements of financial position are provided in the illustrative example in paragraph 230-10-55-19 only to facilitate understanding of the statement of cash flows. For purposes of applying paragraphs 230-10-50-7 through 50-8 to this illustrative example, assume that the year ended December 31, 19X1, is the only period for which a statement of financial position is presented.

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported within the statement of financial position that sum to the total of the same such amounts shown in the statement of cash flows.

[For ease of readability, the new table is not underlined.]

Amounts included in restricted cash represent those required to be set aside by a contractual agreement with an insurer for the payment of specific workers' compensation claims. Restricted cash included in other long-term assets on the statement of financial position represents amounts pledged as collateral for long-term financing arrangements as contractually required by a lender. The restriction will lapse when the related long-term debt is paid off.

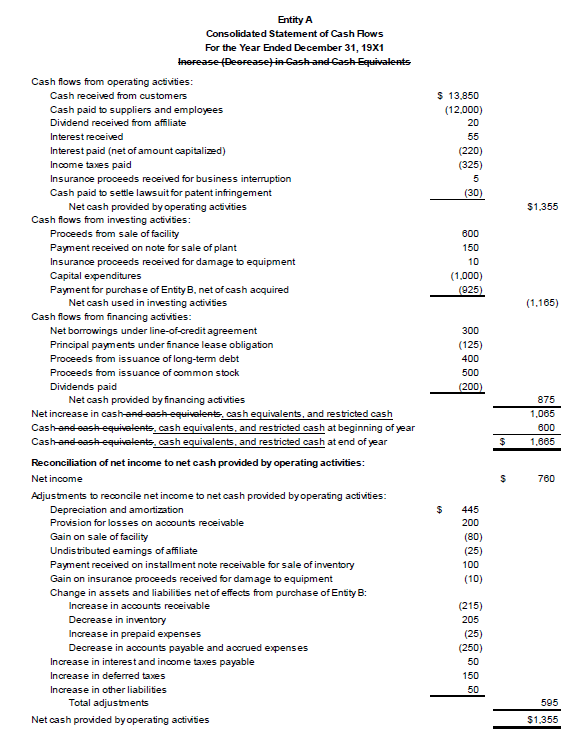

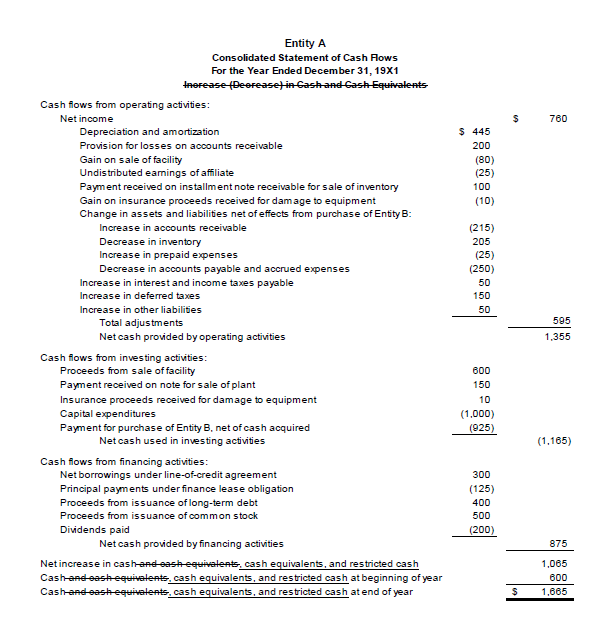

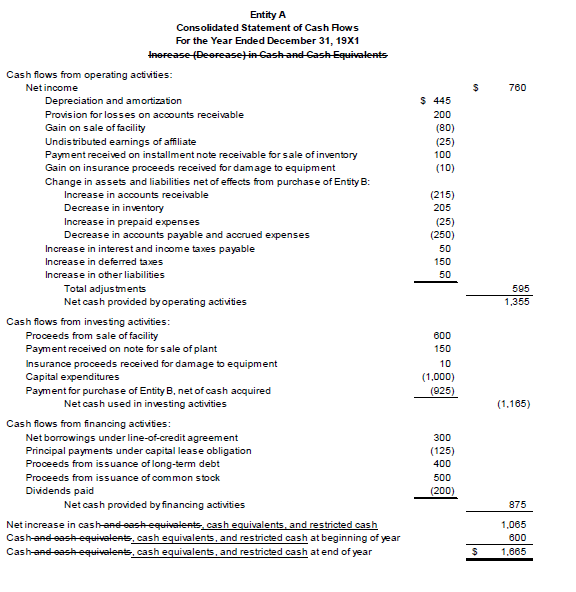

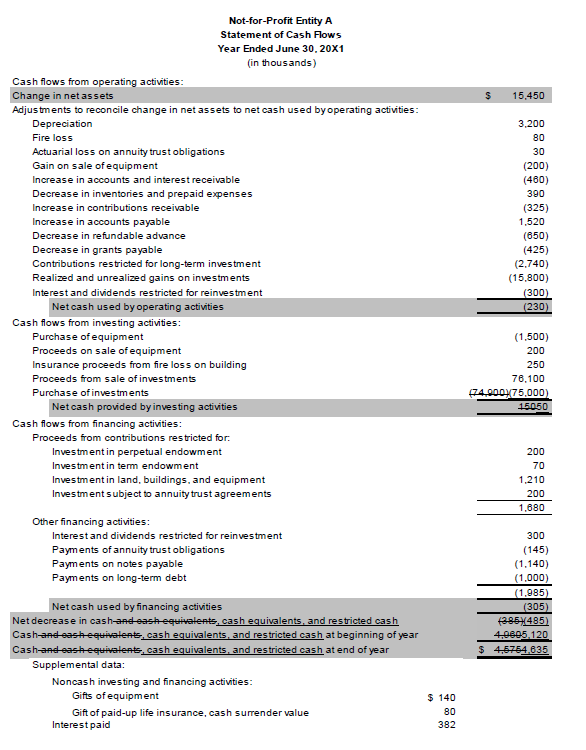

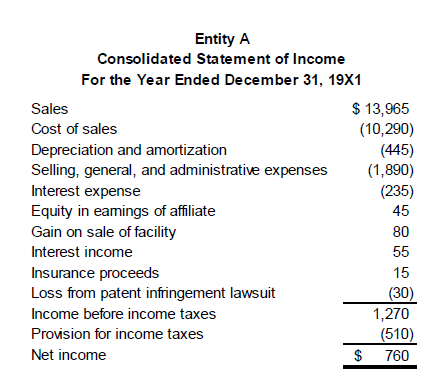

230-10-55-13 The following is Entity A's statement of cash flows for the year ended December 31, 19X1, prepared using the indirect method, as described in paragraph 230-10-45-28.

In addition, amend the following pending content for paragraph 230-10-55-13, with no additional link to transition:

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2019 | Transition Guidance: 842-10-65-1

230-10-55-13 The following is Entity A's statement of cash flows for the year ended December 31, 19X1, prepared using the indirect method, as described in paragraph 230-10-45-28.

230-10-55-18A Shown below is an illustrative disclosure of the nature of restrictions on cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents required by paragraph 230-10-50-7, as well as an illustrative disclosure of the line items and amounts of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents reported within the statement of financial position that sum to the total of the same such amounts at the end of the period shown in the statement of cash flows as required by paragraph 230-10-50-8 (in this illustrative example, assume Entity A has no restricted cash equivalents). Comparative statements of financial position are provided in the illustrative example in paragraph 230-10-55-19 only to facilitate understanding of the statement of cash flows. For purposes of applying paragraphs 230-10-50-7 through 50-8 to this illustrative example, assume that the year ended December 31, 19X1, is the only period for which a statement of financial position is presented.

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported within the statement of financial position that sum to the total of the same such amounts shown in the statement of cash flows.

[For ease of readability, the new table is not underlined.]

Amounts included in restricted cash represent those required to be set aside by a contractual agreement with an insurer for the payment of specific workers' compensation claims. Restricted cash included in other long-term assets on the statement of financial position represents amounts pledged as collateral for long-term financing arrangements as contractually required by a lender. The restriction will lapse when the related long-term debt is paid off.

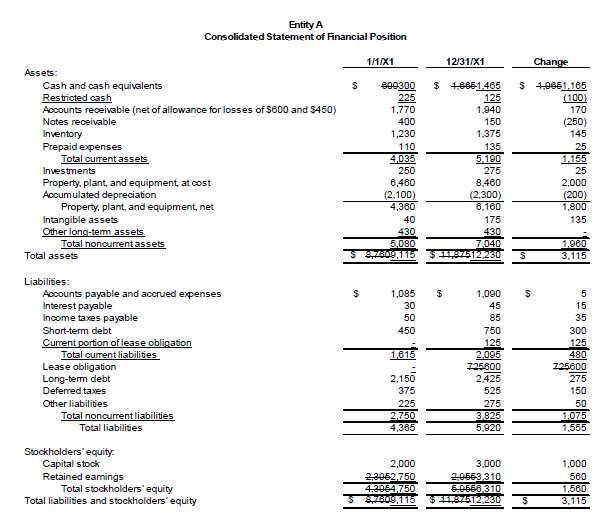

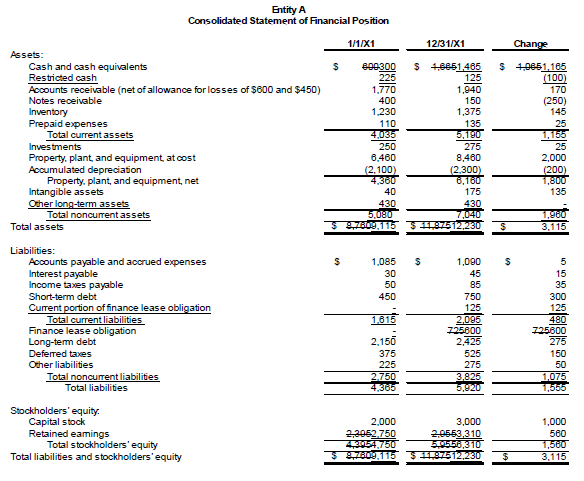

230-10-55-19 The following summarizes financial information for the current year for Entity A, which provides the basis for the statements of cash flows presented in paragraphs 230-10-55-10 through

55-18

55-18A.

In addition, amend the following pending content for paragraph 230-10-55-19, with no additional link to transition:

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2019 | Transition Guidance: 842-10-65-1

230-10-55-19 The following summarizes financial information for the current year for Entity A, which provides the basis for the statements of cash flows presented in paragraphs 230-10-55-10 through

55-18

55-18A.

230-10-55-20 The following transactions were entered into by Entity A during 19X1 and are reflected in the preceding financial statements:

q. Entity A paid $100 from its restricted cash for workers' compensation claims accrued before January 1, 19X1. Before January 1, 19X1, Entity A's insurer required $225 to be set aside by a contractual arrangement for the payment of specific workers' compensation claims.

In addition, amend the following pending content for paragraph 230-10-5520, with no additional link to transition:

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2019 | Transition Guidance: 842-10-65-1

230-10-55-20 The following transactions were entered into by Entity A during 19X1 and are reflected in the preceding financial statements:

q. Entity A paid $100 from its restricted cash for workers' compensation claims accrued before January 1, 19X1. Before January 1, 19X1, Entity A's insurer required $225 to be set aside by a contractual arrangement for the payment of specific workers' compensation claims.

6. Add paragraph 230-10-65-3 and its related heading as follows:

> Transition Related to Accounting Standards Update No. 2016-18,Statement of Cash Flows (Topic 230): Restricted Cash

230-10-65-3 The following represents the transition and effective date information related to Accounting Standards Update No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash:

- For public business entities, the pending content that links to this paragraph shall be effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years.

- For all other entities, the pending content that links to this paragraph shall be effective for financial statements issued for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

- An entity shall apply the pending content that links to this paragraph retrospectively to all periods presented.

- Earlier application of the pending content that links to this paragraph is permitted, including adoption in an interim period. If an entity early adopts the pending content that links to this paragraph in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period.

- An entity shall provide the disclosures in paragraphs 250-10-50-1(a) and (b)(1) and 250-10-50-2, as applicable, in the first interim and annual period the entity adopts the pending content that links to this paragraph.