Search within this section

Select a section below and enter your search term, or to search all click Business combinations and noncontrolling interests, global edition

Favorited Content

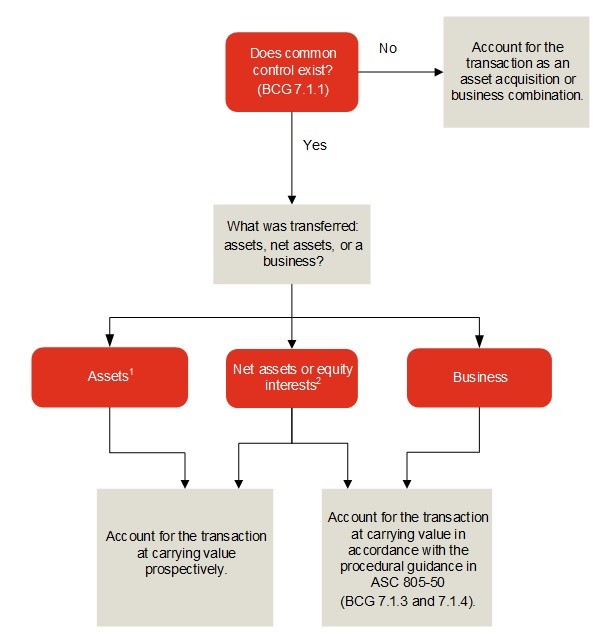

If the primary beneficiary of a variable interest entity (VIE) and the VIE are under common control, the primary beneficiary shall initially measure the assets, liabilities, and the noncontrolling interest of the VIE at amounts at which they are carried in the accounts of the reporting entity that controls the VIE (or would be carried if the reporting entity issued financial statements prepared in conformity with generally accepted accounting principles [GAAP]).

1When nonrecurring transactions (e.g., transfers of long-lived assets) involving entities under common control occur, any nonfinancial assets are recorded at the parent’s historical carrying values in such assets by the receiving entity. However, for recurring transactions for which valuation is not in question, such as routine inventory transfers, the exchange price is normally used regardless of whether a common control relationship exists. Depending on the nature of the transaction, nonrecurring transfers of financial assets may be at fair value (i.e., qualify for sale accounting) or at historical cost at the subsidiary level, by the receiving entity. See BCG 7.1.2.1 for more information on transfers of financial assets involving entities under common control.

2As discussed further below, the determination of whether to account for the transaction prospectively or retrospectively will depend on whether the nature of the net assets or equity interests is more similar to assets or a business.

|

ASC Master Glossary

The financial statements of the receiving entity should report results of operations for the period in which the transfer occurs as though the transfer of net assets or exchange of equity interests had occurred at the beginning of the period. Results of operations for that period will thus comprise those of the previously separate entities combined from the beginning of the period to the date the transfer is completed and those of the combined operations from that date to the end of the period. By eliminating the effects of intra-entity transactions in determining the results of operations for the period before the combination, those results will be on substantially the same basis as the results of operations for the period after the date of combination. The effects of intra-entity transactions on current assets, current liabilities, revenue, and cost of sales for periods presented and on retained earnings at the beginning of the periods presented should be eliminated to the extent possible.

The nature of and effects on earnings per share (EPS) of nonrecurring intra-entity transactions involving long-term assets and liabilities need not be eliminated. However, paragraph 805-50-50-2 requires disclosure.

Similarly, the receiving entity shall present the statement of financial position and other financial information as of the beginning of the period as though the assets and liabilities had been transferred at that date.

Financial statements and financial information presented for prior years also shall be retrospectively adjusted to furnish comparative information. All adjusted financial statements and financial summaries shall indicate clearly that financial data of previously separate entities are combined. However, the comparative information in prior years shall only be adjusted for periods during which the entities were under common control.

The notes to the financial statements of the receiving entity shall disclose the following for the period in which the transfer of assets and liabilities or exchange of equity interests occurred:

The receiving entity also shall consider whether additional disclosures are required in accordance with Section 850-10-50, which provides guidance on related party transactions and certain common control relationships.

Fair value |

Net book value |

|

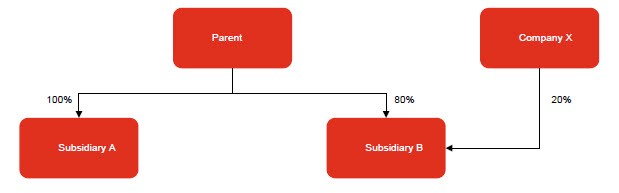

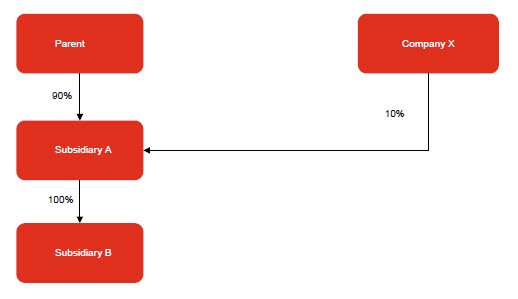

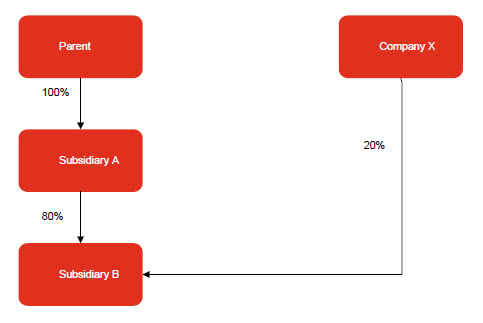

Subsidiary A |

$500 |

$200 |

Subsidiary B |

$500 |

$300 |

NCI—subsidiary B |

$60 1 |

|

Equity/APIC—parent |

$10 2 |

|

NCI—subsidiary A |

$50 3 |

|

1Elimination of Company X’s noncontrolling interest in Subsidiary B.

2The net increase in Parent’s equity in the consolidated financial statements as a result of the transaction with the noncontrolling interest is calculated as follows: |

||

Net book value |

20% NCI in Subsidiary B |

10% NCI in Subsidiary A |

Total adjustment |

||||

Subsidiary A |

$200 |

— |

$20 |

$20 |

|||

Subsidiary B |

$300 |

$(60) |

30 |

(30) |

|||

Adjustment to Parent’s APIC |

$(60) |

$50 |

$(10) |

||||

The effect of the $60 reduction in the noncontrolling interest in Subsidiary B and $50 increase in the noncontrolling interest in Subsidiary A results in a net $10 increase in Parent’s equity in the consolidated financial statements. The changes in the carrying value of the noncontrolling interests are accounted for through equity/APIC. The noncontrolling interest is only recorded at fair value at the date of a business combination.

3Recording of the new noncontrolling interest in Subsidiary A (consolidated net book value of $500 x 10%).

|

|||||||

In some instances, the entity that receives the net assets or equity interests (the receiving entity) and the entity that transferred the net assets or equity interests (the transferring entity) may account for similar assets and liabilities using different accounting methods. In such circumstances, the carrying amounts of the assets and liabilities transferred may be adjusted to the basis of accounting used by the receiving entity if the change would be preferable. Any such change in accounting method should be applied retrospectively, and financial statements presented for prior periods should be adjusted unless it is impracticable to do so. Section 250-10-45 provides guidance if retrospective application is impracticable.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Select a section below and enter your search term, or to search all click Business combinations and noncontrolling interests, global edition