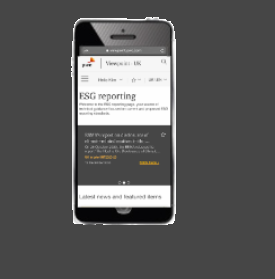

PwC Viewpoint mobile app

Bring the power & content of Viewpoint direct to your mobile device with PwC’s Viewpoint mobile app.

US Mobile app

Download now »

Download now »

Bring the power & content of Viewpoint direct to your mobile device with PwC’s Viewpoint mobile app.

US Mobile app

Download now »

Download now »