Vanessa A. Countryman Secretary Securities and Exchange Commission 100 F Street, NE Washington, DC 20549-1090

RE: File No. S7-26-19

Dear Ms. Countryman:

We appreciate the opportunity to comment on the Securities and Exchange Commission’s (SEC or “the Commission”) proposed rule, Amendments to Rule 2-01, Qualifications of Accountants (the “proposal”).

Independence is a bedrock principle of the auditing profession and, as noted by the Commission in the proposal, a robust and relevant regimen “contributes to both investor protection and investor confidence.” We agree with this view and recognize audit quality as our top priority. Therefore, we maintain a constant emphasis on our purpose, values, and controls that address independence. Exercising impartiality and objectivity in our audits is vital to what we do as we are committed to our qualification as independent in both fact and appearance with respect to all of our audit clients. As such, we support the Commission’s efforts to maintain the ongoing relevance and effectiveness of its auditor independence requirements as set forth in Rule 2-01 of Regulation S-X.

In our view, the Commission’s decision to modernize certain aspects of its auditor independence rules is warranted for sensible reasons, including that, since the rules were established in the early 2000’s, there have been relevant changes (noted in the proposed rulemaking) in the securities markets and business that have an impact on the design and administration of auditor independence rules. We take note also of the Commission’s statement that the proposal is informed by regulatory experience gained in administering the independence rules. Similarly, as we note below, we have incorporated our practice experience developed over time into the observations and recommendations here.

Our observations and recommendations with respect to the proposal are organized into the following topical areas in the Appendix and are based on our experiences with complying with the Commission’s auditor independence rules.

I. Proposed amendments to definitions

II. Proposed amendments to loans or debtor-creditor relationships

III. Proposed amendment to the business relationships rule

IV. Proposed amendments for inadvertent violations for mergers and acquisitions

V. Proposed amendments for miscellaneous updates

VI. Other considerations and suggested amendments

We appreciate the opportunity to express our views and would be pleased to discuss our comments or answer any questions that the SEC staff or the Commission may have. Please contact Samuel L. Burke at samuel.l.burke@pwc.com if we can provide you with any additional information or assistance regarding our observations and recommendations.

Sincerely,

PricewaterhouseCoopers LLP

APPENDIX

I. Proposed amendments to definitions

a. Proposed amendments to “affiliate of the audit client”

The Commission is proposing to modify its definition of an “affiliate of the audit client” in Rule 2-01(f)(4) with respect to operating companies to include a materiality qualifier as it relates to entities under common control (“sister entities”) with the audit client. As such, sister entities would be considered affiliates of an audit client if they are material to the controlling entity. Given the expansive scope of the current definition—which does not include a materiality threshold—this proposed change is, in our view, an important and appropriate element of the Commission’s effort to modernize its rules.

We share the Commission’s view that relationships with immaterial sister entities do not typically pose a threat to an auditor’s objectivity and impartiality. We have found this to be true given the inherent degree of separation that commonly exists between the audit client and sister entities (typically different management and separate, unrelated financial statements). Coupled with the requirement to assess all relevant facts and circumstances involving relationships with sister entities—pursuant to the Commission’s general standard of independence in Rule 2- 01(b)—we see this proposed change as being consistent with achieving the dual goals of investor protection and confidence through objective and impartial audits.

The change, if adopted as proposed, would give greater and appropriate prominence to the concept of materiality in a manner consistent with how this principle is applied in both the accounting and auditing literature. It would also bring this aspect of the SEC’s independence rules into closer alignment with both domestic and international independence affiliate criteria, thus yielding the benefits of convergence.

Align the common control prong with the corresponding AICPA and IESBA affiliate criteria

Although we support this proposed change, we note that it does not fully align with the corresponding common control element of the definitions of “affiliate” and “related entity” set forth, respectively, in the American Institute of Certified Public Accountants’ (AICPA) Code of Professional Conduct

and the International Ethics Standards Board for Accountants’ (IESBA) International Code of Ethics for Professional Accountants (including International Independence Standards).

Both the AICPA and IESBA affiliate criteria for sister entities require the materiality assessment to include both the sister entity and the audit client. That is, a sister entity will only be considered an “affiliate” (or a “related entity” in IESBA’s terminology) of the audit client if both the sister entity and the audit client are material to the controlling entity. Indeed, the Commission acknowledges that “the proposed amendment may not result in the same number of sister entities being deemed material to the controlling entity under our rules and the AICPA rules” because (in part) the “proposed amendment only focuses on the materiality of the sister entity to the controlling entity."

It’s been our experience that services to or relationships with unaudited sister entities—when the entity under audit is not material to the controlling entity—do not typically create threats with respect to the auditor’s objectivity or impartiality, particularly when the auditor does not also audit the controlling entity. Given that the AICPA and IESBA independence frameworks, which embrace this premise, are high quality, widely used and accepted, and well understood independence standards, convergence with the common control affiliate criteria across the domestic and global frameworks will help to reduce the existing complexity of unnecessary regulatory fragmentation in this area, facilitate compliance and comprehension, and promote greater efficiency in the global capital markets. Accordingly, we recommend that the Commission consider further modifying the common control prong in proposed Rule 2- 01(f)(4)(i)(B) so that it fully aligns with the AICPA and IESBA affiliate criteria for sister entities.

Align the definition of control with how that term is defined in the AICPA and IESBA standards

We recommend that the Commission consider further alignment with the AICPA and IESBA affiliate criteria by anchoring the concept of “control” more closely to the accounting literature for purposes of determining affiliates under proposed Rule 2-01(f)(4)(i)(A) and (B). We recognize that the proposal identifies the definition of “control” as an existing difference between the SEC and AICPA’s affiliate frameworks, explaining that “in defining control the AICPA uses the accounting standards adopted by the Financial Accounting Standards Board, whereas our rules define control in Rule 1-02(g) of Regulation S-X.” However, we suggest the Commission give further consideration to the benefits of convergence in this area as the use of different definitions of control often creates practical and regulatory complexity and operational challenges for auditors and audit clients engaging, for example, in an initial public offering. Linking the definition of “control” more directly to the accounting literature would also be consistent with the Commission’s own approach of using the concept of “significant influence” in the proposed amendments to Rule 2-01(c)(3)

and the recent amendments to the Loan Provision

to refer to the principles set forth in the Financial Accounting Standards Board’s ASC Topic 323, Investments – Equity Method and Joint Ventures.

b. Proposed amendments to “Investment Company Complex” (ICC)

With respect to investment company complexes, the Commission is proposing to modify the definition of “affiliate of the audit client” in Rule 2-01(f)(4) to clarify that, when the entity under audit is an investment company or an investment adviser or sponsor, the auditor and the audit client should look solely to the definition of “investment company complex” in Rule 2-01(f)(14) to identify affiliates of the audit client. Additionally, the Commission is proposing to amend the ICC definition to focus on the entity under audit and to align certain portions of the definition with the proposed revisions to the affiliate definition (e.g., incorporating materiality qualifiers in certain common control provisions). We support the Commission’s proposal and offer the following observations and recommendations to enhance the clarity of the amended ICC definition.

Address whether the investment adviser/fund relationship should be treated as a control relationship

The proposed ICC definition includes the investment adviser of an investment company under audit as well as any investment company that has an investment adviser included in the definition by virtue of prongs (f)(14)(i)(A) through (f)(14)(i)(D). In our view, the determination of whether an advisory relationship represents a control relationship is critical to performing the affiliate analysis under the affiliate and ICC definitions.

In describing the attributes of the relationship between an investment company and its adviser, the PCAOB’s ISB Standard No. 2, Certain Independence Implications of Audits of Mutual Funds and Related Entities (ISB No. 2), explains that “the typical mutual fund/adviser relationship is not that of a subsidiary/parent,” but that “while not having voting control of a fund, the investment adviser usually provides the fund’s officers and performs substantially all services required in its operations, and thus plays an important, even controlling, role in its policies and operations” [emphasis added]. In addition, the proposal notes that the Commission “continue[s] to believe that the nature of the relationship between an investment adviser or sponsor and the investment companies it advises is such that once an investment adviser or sponsor is included within the proposed ICC definition, the investment companies it advises should be included as well.”

We suggest the Commission consider further expanding on these views and those provided in ISB No. 2 to specifically address whether the investment adviser/fund relationship should indeed be treated as a control relationship. This type of clarity would be helpful, for example, in determining whether an unregistered fund advised by an adviser controlled by an issuer audit client should be treated as an affiliate of the issuer audit client. In this regard, the Commission may wish to address the matter in the adopting release accompanying the final rule by way of one or more illustrative examples showing the application of the amended definitions.

Align with the Loan Provision’s “sister fund” exception and clarify the treatment of commodity pools

Pursuant to proposed Rule 2-01(f)(14)(i)(F), any investment company that has an investment adviser or sponsor that is in the ICC is also included as part of the ICC, regardless of whether such investment company is material to the controlling entity. However, we note that the Commission’s recent amendments to the Loan Provision, particularly as it applies to a fund under audit, exclude from the definition of “audit client” any other fund (e.g., a “sister fund”) that otherwise would be considered an affiliate of the audit client.

The exclusion of sister funds from the audit client definition “also excludes entities that would otherwise be included in the audit client definition solely by virtue of their association with an excluded sister fund,” including any downstream portfolio investments of the excluded sister funds. Therefore, we suggest the Commission consider “carving out” entities in which a sister fund invests (that is, downstream portfolio companies) from the affiliate and ICC definitions. As noted by the Commission in the Loan Provision Adopting Release, these entities “have an even more attenuated relationship to [the] fund audit client” and lack the “ability to exert significant influence over the entity under audit” and, “therefore, should not be treated as an audit client.”

Another area in which the proposal potentially differs from the Loan Provision is the treatment of commodity pools. The Commission’s recent amendments to the Loan Provision define “fund,” as it relates to the Loan Provision, to also include commodity pools.

We suggest the Commission clarify whether commodity pools are also included within the meaning of the term “investment company” for the purposes of applying the ICC definition.

c. Evaluating materiality

The Commission has solicited views on whether auditors and audit clients face challenges in applying the materiality concept in the context of the common control prong of the “affiliate of the audit client” definition. In response, we note that such challenges exist with diversity of viewpoint and application in practice, despite the fact that materiality is a familiar concept to auditors and audit clients and well established in the current affiliate definition. For example, analyses based solely on specific balance sheet and income statement thresholds are susceptible to inaccurate and inconsistent conclusions in practice regarding materiality. Guided by experience over time and regulatory statements such as footnote 1 of Staff Accounting Bulletin (SAB) No. 99, we believe the assessment should also be attentive to the nature of the relationship, the governance structure of the entity, the other business and financial relationships of the entity, and other relevant qualitative considerations. Materiality is a highly judgmental area with foreseeable variation in approaches. We believe that the application of professional judgment that considers the foregoing factors continues to be the appropriate response to the challenges in the determination of materiality.

Further, we note that there are particular challenges in applying the materiality concept in connection with portfolio companies controlled by private equity firms. For purposes of determining whether sister entities within a private equity complex are affiliates, the proposed amendments to the affiliate definition include the qualifier that an entity under common control with the audit client is an affiliate “...unless the entity is not material to the controlling entity” [emphasis added]. However, neither the proposal nor the proposed amendments to Rule 2- 01(f)(4) make clear which entity would be considered the controlling entity for a specific portfolio company of a private equity fund given the organization of the typical private equity firm, as described in detail below.

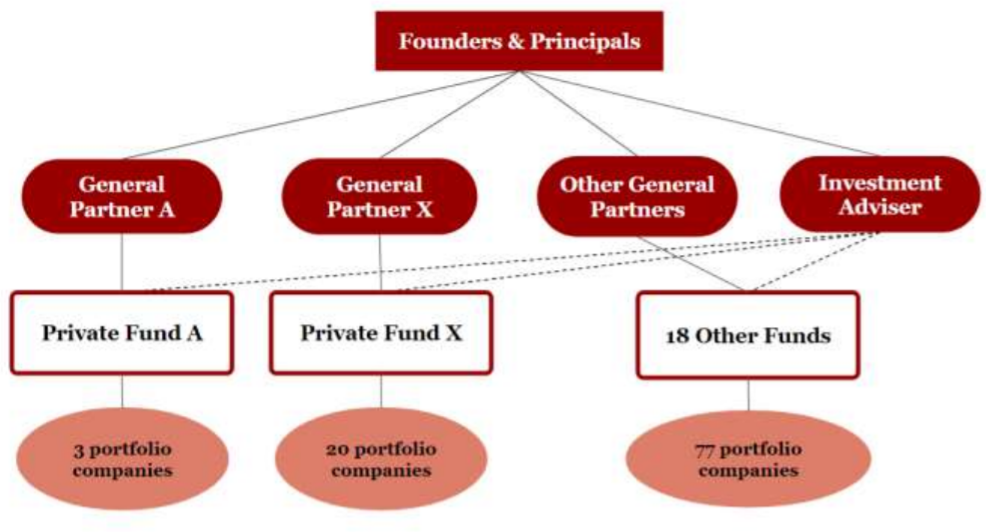

Consider the construct of a typical private equity fund complex

Private equity firms sponsor and manage private equity funds (most frequently organized as limited partnerships) which invest in operating companies (i.e., “portfolio companies”). The funds are typically closed-end commingled investment vehicles with a limited expected term, commonly 8-12 years. The lifecycle of a fund begins with an “investment period,” when capital is called from investors to make investments. Conversely, as the fund matures, the fund’s investments are sold, the proceeds are returned to investors, and the fund is liquidated. At any given time, a private equity firm has a number of funds active, at varying stages of their respective lifecycles, as well as multiple funds that may be at the same or similar stages, but focused on different strategies, industries, or geographies. Some funds are being organized, some are investing, others are selling investments while others may be liquidating. It is not unusual for even a modest sized private equity firm to have dozens of active funds investing in portfolio companies.

Each fund structured as a limited partnership has a general partner (“GP”). The GP for a given fund is typically owned and controlled by the founders and principals of the private equity firm. The GP has control over the fund, although certain activities may be performed by a registered investment adviser, which is owned and controlled by some of the same individuals who own the GP. It is the collection of these funds that represents the entirety of the private equity firm as a business enterprise. The business is conducted by the GP entities and certain affiliates (including registered investment advisers), all of which are under common control of the firm’s founders and principals.

As a group, a private equity firm may control dozens, or even hundreds, of companies. However, given the limited life cycle of the funds, during certain points in time — often early and later in the life cycle — a fund may have very few (sometimes only one) significant investments.

Consider defining the “controlling entity” as the collective private equity house for materiality assessments

While the private equity fund is the vehicle created to pool investment capital used to acquire an interest in the portfolio company, the GPs (and, indirectly, the founders and principals) are responsible for the execution and operation of the investment. Therefore, it would be appropriate to consider that control over a portfolio company resides at a level above the private equity funds; specifically, with the founders and principals who control the GP as a group.

A framework for evaluating materiality to the controlling entity that we believe may provide for proper consideration to the business model of the typical private equity firm could entail defining the “controlling entity” as the collective private equity house. By way of example, in the structure illustrated below, a private equity firm may have $10 billion of “assets under management,” which, for purposes of this example, equals the net asset value of its 20 active funds. The oldest fund, Fund A, is at the end of its lifecycle and has 3 investments and a net asset value of $100 million, while the largest fund, Fund X, has 20 investments and a net asset value of $4 billion. The other funds have another collective 77 investments and total net asset value of $5.9 billion.

For illustrative purposes, consider a portfolio company audit client that is controlled by Fund X. We presume that, for purposes of determining potential affiliates, all 100 investments across the private equity house are in scope of the analysis since they are under common control. To that end, when determining whether other sister portfolio company investments held within Fund X or any other fund in the complex are material to the “controlling entity,” we believe that it would be reasonable to define the “controlling entity” for such calculations as the overall private equity firm. Accordingly, for a materiality calculation in such an instance, it would be reasonable to utilize total net asset value as the denominator in any materiality calculations. Conversely, if Fund A were to be defined as the “controlling entity” in this instance (and, therefore, it is more than likely for any one individual investment to be material to Fund A), the objectives intended by the Commission with the introduction of a materiality qualifier in proposed Rule 2- 01(f)(4)(i)(B), would not be achieved in this situation.

As immaterial, otherwise unrelated investee companies are less likely to bear on the auditor’s objectivity and impartiality, we believe the materiality approach described above would be consistent with the Commission’s stated objective of “more effectively focus[ing] the definition of affiliate of the audit client on those relationships and services that are most likely to threaten auditor objectivity and impartiality.”

We welcome the opportunity to work with the Commission and the profession to develop a framework for evaluating materiality as it relates to independence considerations. This would ensure that the benefits of the proposed amendments to the affiliate definition are achieved.

Emphasize the shared responsibility for obtaining the necessary information for materiality evaluations

We suggest that, in the adopting release accompanying the final rule, the Commission address the shared responsibility of auditors, audit committees, and client management to obtain the information necessary for materiality determinations in the identification of affiliates. In fact, the audit client is best positioned to access relevant information about its investors and investees and should share this information with the auditor in a timely manner. The Commission’s staff has previously acknowledged

the audit client’s responsibility to work together with the auditor in identifying and monitoring affiliates. We recommend that this be emphasized in the adopting release.

Consider establishing a transition framework for unforeseen changes in materiality evaluations

As described further in Section IV of this letter, we believe it may be helpful for the Commission to consider establishing a transition framework similar to that proposed in Rule 2-01(e) to address inadvertent independence violations that might arise when a materiality threshold is crossed as a result of unforeseen changes in facts and circumstances, thereby resulting in a change in the population of affiliates of an entity under audit.

Exclude aggregation of sister entities and apply materiality assessment with respect to the controlling entity only

With respect to the Commission’s request for comments on aggregating sister entities in the materiality assessment, we note that a requirement for auditors to aggregate sister entities when determining materiality would negate some of the benefits (e.g., an increase in choice and competition for audit and non-audit services) that, according to the proposal, will be created by the addition of a materiality qualifier to the common control prong of the affiliate definition. Aggregation would compound the challenges associated with materiality assessments and make the new affiliate model for entities under common control more difficult to operationalize. The assessment should be performed on an individual basis and only focus on whether the sister entity is material to the controlling entity (rather than both the controlling entity and the entity under audit).

d. Proposed application of the general standard in Rule 2-01(b)

We observe that the proposal includes several references to the general standard of independence, including, notably, in the context of the discussion of the proposed amendments to the definitions in Rule 2-01(f). The Commission explains that the proposed amendments to the definitions of “affiliate of the audit client” and “investment company complex” “do not alter the application of the general standard in Rule 2-01(b).” According to the proposal, while the proposed amendments exclude entities that are currently considered affiliates but would no longer be deemed affiliates due to, for example, the addition of a materiality threshold for sister entities, relationships and services between the auditor and such entities would still be subject to the general standard and a requirement for the auditor and audit client to consider “all relevant facts and circumstances.”

The proposal’s references to the general standard may be understood in practice as a change in the application and operation of Rule 2-01(b)

Invoking the general standard in this manner (and with the degree of frequency in which it is cited in the proposal) may be understood as a change in view from the earlier discussion in the Commission’s 2000 Adopting Release

regarding the application and operation of the standard. We question whether the references to the general standard within the proposal’s discussion of changes to specific provisions of Rule 2-01(f) might represent a shift in the operation of the basic test of auditor independence from what the Commission originally intended in the 2000 rulemaking and, if so, necessitate further guidance. We note that, although the 2000 Adopting Release indicates that “Rule 2-01(c) ties the general standard of paragraph (b) to specific applications,”

it does not (unlike the proposal) explicitly invoke the general standard in the discussion of the application of the definitions in Rule 2-01(f).

The proposal appears to establish an expectation of continued monitoring of non-affiliates

A requirement to continue evaluating services to and relationships with entities that are not affiliates would make it necessary for both auditors and audit clients to continue to undertake proactive tracking of such entities in order to satisfy Rule 2-01(b). This would effectively reduce the benefits, efficiencies, and cost savings that would otherwise be gained from the proposed amendments to the affiliate and ICC definitions. Indeed, the Commission recognizes this in the proposal, explaining that “audit firms and their clients may continue to incur some costs to consider such entities as part of their independence analysis.”

Additionally, the proposal is silent regarding the identification of any specific population of possible non-affiliate entities that would still be subject to an independence analysis pursuant to the general standard and potentially have to be monitored for possible independence-impairing relationships and services. Relevant facts and circumstances might exist in relation to services and relationships with other non-affiliate entities, not just those specific entities that are excluded from the affiliate and ICC definitions under the proposal.

The intent of the “easily known” test for relationships with non-affiliates and the expectations around continued monitoring are unclear

With respect to the application of the general standard to entities that would fall outside of the definition of “affiliate of the audit client,” the Commission notes that:

“...for the relationships and services that might nevertheless impact the auditor’s independence under the general standard in Rule 2-01(b), we would expect those relationships and services individually or in the aggregate would be easily known by the auditor and the audit client because such services and relationships are most likely to threaten an auditor’s objectivity and impartiality due to the nature, extent, relative importance or other aspects of the service or relationship.” [emphasis added]

We request that the Commission consider clarifying whether this guidance, particularly the reference to “easily known,” should be interpreted to mean that the independence analysis pursuant to the general standard should be undertaken with respect to those services and relationships that the auditor knows or has reason to believe might impact objectivity and impartiality. To this end, we recommend that the Commission consider utilizing an established approach, such as the “knows or has reason to believe” test (as set forth in the AICPA Code of Professional Conduct), for evaluating relationships with and services to sister entities that would not be deemed affiliates under the modified definitions in Rule 2-01(f). A “knows or has reason to believe” test would provide an appropriate measure for focusing the independence analysis on those relationships that might actually impact objectivity and impartiality across the spectrum of client-related entities that are not considered affiliates. In addition to clarifying the intent of the test being imposed, we also request that the Commission make clear whether auditors and audit clients would be expected to monitor entities that are not otherwise affiliates under Rule 2- 01(f)(4) and (f)(14).

e. Proposed amendment to “Audit and Professional Engagement Period”

For audits of foreign private issuers that file a registration statement or report with the Commission for the first time, the current definition of the “audit and professional engagement period” in Rule 2-01(f)(5)(iii) requires the auditor to comply with SEC independence rules during the most recent year of audited financial statements included in the initial filing, provided that the auditor has complied with “home country” independence standards in all prior periods covered by the registration statement or report. In contrast, auditors of domestic first time filers are required to comply with Rule 2-01 for all years of audited financial statements included in the registration statement (typically, two or three). As acknowledged by the Commission in the proposal, this requirement for a two or three year look-back period may result in potentially costly and burdensome outcomes for domestic private companies contemplating an IPO, such as the need to delay the offering or engage a new auditor that is independent under Rule 2-01 for all prior years to re-audit the financial statements included in the registration statement.

The Commission is proposing to amend the definition so that the one year look-back provision would apply to all first-time filers, both domestic issuers and foreign private issuers. We agree with the Commission that this proposal is, in essence, “leveling the playing field” for domestic first-time filers in that such companies, and their auditors, would be afforded the same time as foreign private issuers to transition to SEC requirements. We agree that, if adopted as proposed, the change will encourage capital formation for domestic issuers without the risk associated with shortening the look-back provision for their auditors (who will still be required to comply with applicable — generally, AICPA — independence standards in all prior periods). As such, we support the proposed amendment to the definition of the “audit and professional engagement period.”

II. Proposed amendments to loans or debtor-creditor relationships

a. Proposed amendment to exempt student loans

The Commission is proposing to amend the Loan Provision in Rule 2-01(c)(1)(ii)(A) to establish a new exception for certain student loans obtained for a covered person’s educational expenses. The student loan debt burden in America has reached almost $1.5 trillion in overall indebtedness.

The Commission’s proposal to exempt certain pre-existing student loans is therefore in the public interest. Importantly, the proposed exception is also consistent with the current exception for covered persons’ pre-existing home mortgages. As such, we support this proposed amendment to the Loan Provision, while offering the following suggestions.

Apply the proposed exception to all pre-existing student loans

We believe that the exception should apply to all pre-existing student loans held by a covered person. In our view, it would not be appropriate to limit the exception to loans for accounting and auditing educational expenses since the nature of expenses for education by covered persons goes beyond accounting and auditing to include educational backgrounds in other fields — such as computer engineering, finance, and actuarial specialists

on the audit engagement team — that would not qualify for the exception and thus be placed at a regulatory burden. This could potentially limit the ability of audit firms to recruit and place the most capable and qualified professionals on audit engagements. Further, we recommend that the Commission clarify whether the exception also includes expenses incurred with respect to room and board, books, educational supplies, etc. as these costs are often an unavoidable part of obtaining an undergraduate or graduate degree and, therefore, may also be paid for with funds from student loans.

Apply the proposed exception to student loans obtained by immediate family members

In addition, we suggest that the SEC reconsider the aspect of the proposal that limits the relief to student loans obtained to pay for the covered person’s own educational expenses. The proposal states that the exception would not encompass student loans obtained by a covered person’s immediate family members. We view this approach to be inconsistent with the application of the current exceptions to the Loan Provision for other forms of indebtedness (e.g., mortgages, automobile loans and leases, credit card balances of $10,000 or less). Accordingly, we believe the Commission should expand the proposed exception to student loans to include those held by a covered person’s immediate family members.

b. Proposed amendment to clarify the reference to “a mortgage loan”

We agree with the Commission’s proposed amendment to Rule 2-01(c)(1)(ii)(A)(1)(iv) to clarify that the reference to “a mortgage loan” includes all loans secured by a covered person’s primary residence. We believe this clarification is consistent with the original intent of the exception for pre-existing home mortgages and the manner in which the exception has been applied since it was adopted by the Commission.

c. Proposed amendment to revise the credit card rule to refer to “consumer loans”

The Commission is proposing to amend the Credit Card Provision in Rule 2-01(c)(1)(ii)(E) to broaden the current exception for a covered person’s credit card debt of $10,000 or less to other consumer loans obtained from a lender that is an audit client. We agree with this proposed amendment as it builds on the underlying principle that “… not all creditor or debtor relationships threaten an auditor’s objectivity and impartiality,” as exemplified by the lending relationships that are exempt from the existing prohibition on loans (e.g., home mortgages, automobile loans, credit cards). Further, the change, if adopted, would help to avoid the types of situations described by the SEC in the Loan Provision Adopting Release

whereby:

“... auditors and audit committees may feel obligated to devote substantial resources to evaluating potential instances of non-compliance ... which could distract auditors’ and audit committees’ attention from matters that may be more likely to bear on the auditor’s objectivity and impartiality.”

Incorporate a definition of a “consumer loan” into Rule 2-01

Although the Commission’s views as to what would constitute a “consumer loan” are articulated in the proposal, the Commission has not proposed to carry those examples forward to Rule 2-01. For purposes of clarity and to promote consistency in the application of the exception, we suggest that those examples (i.e., loans that are “…routinely obtained for personal consumption, such as retail installment loans, cell phone installment plans, and home improvement loans that are not secured by a mortgage on a primary residence…”) be added to Rule 2-01(c)(1)(ii)(E) or Rule 2-01(f) as a definition of a “consumer loan.” Further, we recommend that the Commission retain the current reference to “credit cards” in Rule 2-01(c)(1)(ii)(E), again for improved clarity and to promote consistent application. The reference could either be retained in Rule 2- 01(c)(1)(ii)(E) itself or added as an element of the “consumer loan” definition as we’ve suggested.

Increase the outstanding balance limit for permitted consumer loans to reflect inflation

The Commission has solicited views regarding whether the outstanding balance limit of $10,000 continues to be appropriate. We suggest that the Commission consider increasing this dollar threshold for permitted consumer loans in light of the inflation that has occurred since the Credit Card Provision was first adopted in 2000.

Therefore, an increase in the outstanding balance limit to match inflation over the past two decades would be consistent with the Commission’s stated goal of modernizing the auditor independence requirements without, in our view, creating a higher risk to the covered person’s objectivity and impartiality since the inflation adjustment would merely reflect current buying power.

Establish a dollar threshold for other common types of consumer financial arrangements

We suggest that the Commission consider whether a similar dollar threshold might be applied to other consumer financial arrangements, such as (but not limited to):

insurance policies (e.g., vacation and travel insurance, cell phone insurance),

leases (e.g., leases for apartments and home furniture/appliances),

overdraft lines of credit, and

deposit account balances that exceed the FDIC insurance limit or are not subject to FDIC or similar insurance.

Such a threshold would represent a more reasonable measure of significance for evaluating the impact on independence of other common types of personal consumer relationships as well as provide a more meaningful and effective way to focus audit committee attention on “…matters that may be more likely to bear on the auditor’s objectivity and impartiality….”

For example, with respect to uninsured deposits with an audit client, we suggest that the Commission consider establishing an exception to Rule 2-01(c)(1)(ii)(B) for savings/checking (or similar) account balances that exceed the FDIC insurance limit by an immaterial amount and for de minimis digital wallet deposit balances that are entered into under normal and customary consumer terms and requirements. Digital wallets allow purchases and money transfers without the use of cash, checks, or credit/debit cards, but balances kept in the “wallet” are generally not covered by FDIC or similar insurance. This means that any balance held by a covered person in the digital wallet — for any length of time (e.g., overnight) — would represent a technical breach of Rule 2- 01(c)(1)(ii)(B) and have to be reported to the audit committee, even if the amount is so clearly de minimis that a reasonable investor would conclude that the covered person is capable of exercising objective and impartial judgment.

III. Proposed amendment to the business relationships rule

a. Proposed amendment to the reference to “substantial stockholder”

The Commission is proposing to replace the reference to “substantial stockholders” in the Business Relationships Provision in Rule 2-01(c)(3) with the phrase “beneficial owners (known through reasonable inquiry) of the audit client’s equity securities where such beneficial owner has significant influence over the audit client.” We support the Commission’s aim of providing clarity regarding the shareholders that are implicated by the Business Relationships Provision and agree with the proposal, which more appropriately identifies relationships that could be more likely to threaten an auditor’s objectivity and impartiality.

We believe the proposed amendment would make the Business Relationships Provision clearer and reduce complexity, given that “substantial stockholder” is not currently defined in Regulation S-X. We believe that the concept of beneficial owners with significant influence, as proposed, more appropriately identifies those relationships that are likely to impair an auditor’s objectivity and impartiality than does the current Business Relationships Provision. We also believe that, conceptually, there should be a consistent definition of non-affiliate shareholders to which the additional restrictions on business relationships and loans should apply, and the proposed amendment would achieve that.

Auditors and audit clients are familiar with the “significant influence” test and therefore will be able to more consistently apply it than the current “substantial stockholder in a decision-making capacity” test. The proposed change, if adopted, will also establish consistency in the population of non-affiliate shareholders who are implicated to the Loan Provision and the Business Relationships Provision, reducing complexity and lessening the compliance burden and costs for both audit clients and auditors. For these reasons, we support this aspect of the proposal.

Exclude entities that are under common control with or controlled by the beneficial owner

Furthermore, we note the Commission’s clarification in the Loan Provision Adopting Release that “entities that are under common control with or controlled by the beneficial owner of the audit client’s equity securities when such beneficial owner has significant influence over the audit client, are excluded from the scope of the Loan Provision.”

We suggest that, in the adopting release accompanying the final rule, the Commission also clarify whether this same exclusion applies to the Business Relationships Provision. We believe it would be appropriate for the Commission to conform the Business Relationships Provision with the Loan Provision in this regard so that there is a single, consistent standard – one with which auditors and audit clients are already familiar under the recently amended Loan Provision – for identifying the beneficial owners that are implicated by the SEC’s auditor independence rules.

b. Additional guidance on the reference to “audit client” when referring to persons associated with the audit client in a decision-making capacity

The Commission has provided clarifying guidance in the proposal that the independence analysis of business relationships with persons in a decision-making capacity should focus on whether the person has significant influence over the “entity under audit”

rather than the “audit client” (which, by definition, includes the audit client’s affiliates). Therefore, as it relates to beneficial owners who own equity securities of an affiliate, the focus of the analysis should be on whether the beneficial owner has significant influence over the “entity under audit.” Further, the proposal clarifies that the same guidance also applies to the recently amended Loan Provision in Rule 2- 01(c)(1)(ii)(A). We agree with the SEC’s rationale and believe this guidance will help auditors and audit committees focus on those business and lending relationships that have the potential to impact objectivity and impartiality.

Incorporate clarifying guidance on beneficial owners into Rule 2-01

We recommend that the Commission embed this clarifying guidance in Rule 2-01 itself. The references to the more expansive concept of “audit client” in the Business Relationships and Loan provisions as it relates to beneficial owners could be interpreted to conflict with the Commission’s guidance that the evaluation should focus on whether the significant influence exists at the “entity under audit.” To eliminate this potential conflict, the Commision should replace the relevant reference to “audit client” in both provisions with “entity under audit” instead, including in the proposed amendment to Rule 2-01(c)(3).

Clarify application of clarifying guidance to officers and directors

It is unclear whether the Commission’s clarifying guidance applies to beneficial owners only or also to officers and directors. Accordingly, we recommend that the Commission clarify whether the limitations in the Business Relationships and Loan provisions for officers and directors should also be evaluated in terms of their significant influence over (or their position with) the “entity under audit” only, or, alternatively, whether all officers and directors of affiliates of the entity under audit would also be subject to those limitations.

c. Independence considerations regarding multi-company arrangements

The Commission has solicited views regarding multi-company arrangements and their impact on an auditor’s objectivity and impartiality. We share the Commission’s understanding that it is more common today for businesses to enter into multi-company arrangements in delivering products or services and that audit firms may contribute to such arrangements, for example, through intellectual property or access to data using common technology platforms. These multicompany arrangements have grown along with advances in technology to become a much more significant component of the marketplace for many services and products.

These arrangements are varied in their objectives, participants, users, and structures. As a result, the evaluation as to whether participation of an audit firm would represent an impermissible business relationship or would otherwise represent a threat to the auditor’s objectivity and impartiality involves a high degree of judgment based on the facts and circumstances particular to that arrangement. The considerations include, amongst others:

the relationships between the participants in the multi-company arrangement,

the nature and importance of the contributions of each of the participants,

the nature of the service or product ultimately provided by the multi-company arrangement,

the beneficiaries or users of the service or product of the multi-company arrangement,

the appearance of the multi-company arrangement in the marketplace,

the revenue structure of the arrangement,

whether the terms and conditions are representative of those in the marketplace, and

the significance of the arrangement to the auditor and other participants that are audit clients.

We believe the dramatic changes in the business environment that have occurred since the adoption of the Business Relationships Provision warrant a broad re-examination of the scope and application of the rule. Multi-company arrangements represent just one area of several where the broadest interpretations of the rule’s general concepts may implicate relationships that do not pose a threat to the auditor’s objectivity and impartiality. Given the diverse and evolving nature of the marketplace for services, intellectual property, data, and products, we suggest that any amendments in this area be primarily principles-based, reflecting the general framework outlined by Rule 2-01(b).

IV. Proposed amendments for inadvertent violations for mergers and acquisitions

The Commission is proposing to amend Rule 2-01(e) to provide a transition framework to address inadvertent independence violations that arise out of an audit client’s involvement in a merger or acquisition. The proposed amendments enable the auditor and its client to transition out of prohibited services and relationships in an orderly manner provided that certain criteria are met.

We believe it is appropriate for the Commission to allow for a reasonable period of time subsequent to a transaction’s closing during which any relationships that are inconsistent with the SEC independence rules would not be considered to impair independence provided that they are restructured or terminated, as appropriate, in a timely fashion. Accordingly, we support the Commission’s proposed enhancements (particularly, given the prevalence and sometimes short timing of such transactions) and offer the following suggestions.

Incorporate the proposed six-month transition period into Rule 2-01(e)

The proposed framework requires that any such independence violations be corrected as “promptly as possible.” The proposal explains that, while what qualifies “as promptly as possible” depends on all relevant facts and circumstances, the Commission expects “all corrective action to be taken no later than six months after the effective date of the merger or acquisition that triggered the independence violation.” We recommend that the Commission incorporate this six-month transition threshold in Rule 2-01(e) itself for clarity and to promote consistency in the application of the proposed framework. Specifically, the Commission should consider revising proposed Rule 2-01(e)(ii) to state that the “lack of independence under this rule has been or will be corrected as promptly as possible under relevant circumstances, but no later than six months after the effective date of the merger or acquisition.”

Consider whether the proposed transition framework could be applied to other unforeseen changes in affiliate relationships

In addition to merger and acquisition scenarios covered by the proposed framework, we believe it may be helpful for the Commission to consider clarifying whether the same framework could also be applied to address inadvertent independence violations that arise out of an unexpected change in the population of affiliates for reasons other than a merger or acquisition. This could include, for example, situations in which a materiality threshold is crossed as a result of unforeseen changes in circumstances, or there is a change resulting in an investor unexpectedly having the ability to exercise significant influence or control.

Clarify that matters meeting the conditions of the proposed transition framework are not considered independence violations

With respect to the reference to independence “violations” in the proposal, we also recommend that the Commission clarify that matters arising from a merger or acquisition are not considered violations of Rule 2-01 when all of the conditions of the proposed framework are met. This would help to alleviate the need for auditors and audit committees to devote time and resources to evaluating instances of technical non-compliance that do not bear on independence and enable the audit committee to focus its attention on those relationships and services that actually pose threats to objectivity and impartiality. Such a clarification would also align the proposed framework with the IESBA International Code of Ethics for Professional Accountants (the “IESBA Code”), which provides a similar six-month transition period subsequent to a merger or acquisition during which relationships and services that are inconsistent with the IESBA Code would not be considered to impair independence provided that they are ended as soon as reasonably possible and the auditor takes certain other measures.

Eliminate the clause “but before the transaction has occurred” from proposed Rule 2- 01(e)(iii)(B)

The Commission has solicited views on whether the proposed criteria for the quality control requirement are sufficiently clear. The inclusion of the clause “but before the transaction has occurred” in proposed Rule 2-01(e)(iii)(B) might suggest to some that the transition relief under the proposed framework only applies if the auditor identifies the independence violation prior to the close of the transaction. As such, we request that the Commission clarify that auditors are permitted to apply the proposed transition framework to violations identified after the transaction has occurred provided that the auditor has established procedures and controls to allow for timely notification of mergers and acquisitions as well as prompt identification of potential violations.

In this regard, we note that there may be a number of practical challenges that auditors and audit clients face in accurately identifying the post-close legal entity structure necessary to obtain a full inventory of services and relationships prior to the transaction closing, particularly in situations involving complex “carve-outs” where entity names change or additional entities are formed. Accordingly, we recommend that the Commission amend proposed Rule 2-01(e)(iii)(B) to delete the clause “but before the transaction has occurred” such that the criterion would say “[p]rocedures and controls that allow for prompt identification of potential violations after initial notification of a potential merger or acquisition that may trigger independence violations.”

V. Proposed amendments for miscellaneous updates

We agree with the Commission’s proposed miscellaneous updates to Rule 2-01. The conforming changes to modify the existing references to “concurring partners” are appropriate and necessary since they are inconsistent with terminology used in current auditing standards. Similarly, we agree that the proposed deletion of the outdated transition and grandfathering provisions in Rule 2-01(e) and the proposed amendments to the “Preliminary Note” to Rule 2-01 as they too are appropriate.

VI. Other considerations and suggested amendments

a. Use of the term “entity under audit”

In addition to our suggestions in Section (III)(b) of this letter, we recommend more broadly that the Commission use “entity under audit” in any provisions of Rule 2-01 when the Commission expects auditors to perform the relevant independence analysis with respect to “the entity whose financial statements or other information is being audited, reviewed or attested,”

but not with respect to the entity’s affiliates. This would include replacing the references to “audit client” with “entity under audit” instead in prong (f)(4)(i) of the proposed affiliate definition (similar to what the Commission has already proposed in prong (f)(4)(ii)

). When referring to both the “entity under audit” and its “affiliates,” the Commission could continue to use the broader “audit client” (as currently defined in Rule 2-01(f)(6)). We believe this clarification would help to better define the Commission’s expectations and promote consistent application of Rule 2-01.

b. PCAOB rules and interim independence standards

In April 2003, the PCAOB adopted certain pre-existing independence requirements as its interim independence standards (“Interim Standards”). PCAOB Rule 3500T, Interim Ethics and Independence Standards, requires PCAOB-registered public accounting firms, and their associated persons, to comply with the Interim Standards

in connection with the preparation or issuance of any audit report for an issuer or SEC-registered broker-dealer. The Interim Standards were adopted by the PCAOB “...on an initial, transitional basis in order to assure continuity and certainty in the standards that govern audits of public companies...”

[emphasis added], and served as a transition from Generally Accepted Auditing Standards (including the AICPA independence requirements) when the PCAOB began to oversee public company audits.

Rule 3500T provides that:

“to the extent that a provision of the Commission's rule is more restrictive – or less restrictive – than the Board's Interim Independence Standards, a registered public accounting firm must comply with the more restrictive rule.” [emphasis added]

As such, if adopted, certain of the Commission’s proposed amendments to Rule 2-01, such as the exceptions for student and consumer loans, would be less restrictive than the relevant provisions of the Interim Standards. Therefore, action must presumably be taken with respect to the Interim Standards in order for registered public accounting firms to be able to implement the amendments to Rule 2-01. At a minimum, the Interim Standards would have to be modified to conform to the final amendments ultimately adopted by the Commission. Similarly, the definitions of “affiliate of the audit client,” “audit and professional engagement period,” and “investment company complex” in PCAOB Rule 3501, Definitions of Terms Employed in Section 3, Part 5 of the Rules, would also have to be amended to reflect the Commission’s final revisions to the definitions of those same terms in Rule 2-01.

Further, the proposal notes a requirement pursuant to the Regulatory Flexibility Act that the proposed amendments should not be “...duplicative, overlapping or conflicting of other Federal rules.” This may also call into question whether certain aspects of the Interim Standards, whether or not they are more restrictive than the proposed amendments, are consistent with that requirement. For example, as we’ve previously noted,

the recently amended Loan Provision in Rule 2-01(c)(1)(ii)(A) conflicts with the Interim Standards, which limit the application of the prohibition on loans to lending relationships with individuals, not entities, that are 10% owners. Accordingly, the Commission may wish to consider whether a re-evaluation of the Interim Standards is warranted at this time.

c. Treasury department advisory committee recommendations

Currently the Commission’s independence rules reside in multiple locations (i.e., Rule 2-01 and Section 602 of the SEC Codification of Financial Reporting Policies) with application guidance also set forth in the 2000 Adopting Release,

the 2003 Adopting Release,

the Loan Provision Adopting Release, and the Office of the Chief Accountant’s Application of the Commission's Rules on Auditor Independence — Frequently Asked Questions (for example, see our related comments above regarding the definition of “consumer loans” and the use of the term “entity under audit” in the Loan and Business Relationships Provisions). The PCAOB has also adopted its own separate independence requirements in the form of Section 3, Subpart I, Independence, of the Rules of the Board

and the Interim Standards (as discussed above).

Accordingly, we reiterate our suggestion

for the Commission to revisit the recommendations made by the US Treasury Department’s Advisory Committee in its Final Report of the U.S. Treasury Department’s Advisory Committee on the Auditing Profession to “...compile the SEC and PCAOB independence requirements into a single document and make this document website accessible.”

In doing so, the SEC could, at the same time, resolve any existing “...duplicative, overlapping, or conflicting…” guidance that exists between the SEC and PCAOB rules, in particular with respect to the PCAOB’s Interim Standards (as suggested above).

We believe that undertaking this exercise would improve the comprehension of and compliance with these rules, particularly with respect to smaller auditing firms and their audit committees, consistent with the intent of the proposal to modernize the SEC’s independence rules. We note that several domestic and international standard setters (e.g., the FASB, IESBA, AICPA’s Auditing Standards Board and Professional Ethics Executive Committee) have undertaken major projects in recent years to clarify and codify their authoritative standards and guidance (e.g., US GAAP) in a single location.

1See AICPA Code of Professional Conduct, ET section 0.400.02. The AICPA’s definition of “affiliate” includes 1) entities that a financial statement attest client can control, 2) entities that control a financial statement attest client when the financial statement attest client is material to such entity, and 3) sister entities of a financial statement attest client if the financial statement attest client and sister entity are each material to the entity that controls both.[emphasis added]

2See IESBA International Code of Ethics for Professional Accountants (including International Independence Standards), Glossary, definition of “Related entity.” The IESBA’s definition of “related entity” includes 1) entities that have direct or indirect control over the client if the client is material to such entity, 2) entities over which the client has direct or indirect control, and 3) entities that are under common control with the client (a “sister entity”) if the sister entity and the client are both material to the entity that controls both the client and sister entity.[emphasis added]

3See Section (II)(C)(1) of the proposal at 85 FR 2340, footnote 42. With respect to the proposed amendments to Rule 2-01(c)(3), the Commission explains that, “[c]onsistent with the recently adopted amendments discussed in the Loan Provision Adopting Release, the use of ‘significant influence’ in these proposed amendments is intended to refer to the principles in the Financial Accounting Standards Board’s (‘FASB’s’) ASC Topic 323, Investments – Equity Method and Joint Ventures.”

4See Section (II)(C)(3) (84 FR 32048) of Auditor Independence With Respect to Certain Loans or Debtor-Creditor Relationships, Release No. 33-10648 (June 18, 2019) [84 FR 32040 (July 5, 2019)] (hereafter referred to as “the Loan Provision Adopting Release”).

5 See Section (II)(E)(3) of the Loan Provision Adopting Release at 84 FR 32052.

6 See Section (II)(A) of the Loan Provision Adopting Release at 84 FR 32044.

7See, for example, Vassilios Karapanos, Remarks before the 2019 AICPA Conference on Current SEC and PCAOB Developments (December 9, 2019).

8 In addition to requesting comments on aggregation of sister entities, the Commission has also solicited views on whether materiality should “focus on whether sister entities are material to the entity under audit, in addition to whether they are material to the controlling entity ” [emphasis added] (see Section (II)(A)(1)(a) of the proposal at 85 FR 2335, question 2).

9Revision of the Commission’s Auditor Independence Requirements, Release No. 33-7919 (Nov. 21, 2000) [65 FR 76008 (Dec. 5, 2000)]

10See Section (IV)(D) of the 2000 Adopting Release at 65 FR 76031.

11 Friedman, Zack. “ Student Loan Debt Statistics In 2019: A $1.5 Trillion Crisis. ” Forbes, 25 Feb. 2019.

12 Specialists include, but are not limited to, actuaries, appraisers, engineers, environmental consultants, and geologists. See PCAOB AS 1210, Using the Work of a Specialist.

13See Section (I) of the Loan Provision Adopting Release at 84 FR 32042.

14 According to the US Bureau of Labor Statistics’ inflation calculator, $10,000 in November 2000 has the same buying power as $14,760 in December 2019, an inflation rate of nearly 50%. At the same time, there has also been a rise in personal debt levels since 2000, with spending methods having changed over this period of time to an increased use of credit cards over cash for the purchase of consumer goods.

15See section (I) of the Loan Provision Adopting Release at 84 FR 32042.

16See Section (II)(B)(3) of the Loan Provision Adopting Release at 84 FR 32046.

17 According to Section (II)(A)(1) (85 FR 2333, footnote 11) of the proposal, the Commission refers to “entity under audit” to mean, for purposes of the proposal’s discussion, “the entity whose financial statements or other information is being audited, reviewed or attested.”

18See IESBA International Code of Ethics for Professional Accountants (including International Independence Standards), paragraphs 400.70 A1—R400.76.

19See Section (II)(A)(1) of the proposal at 85 FR 2333, footnote 11.

20 Proposed Rule 2-01(f)(4)(ii).

21 The Interim Standards consist of (1) the AICPA Code of Professional Conduct’s Rule 101, and the interpretations and rulings thereunder, as in existence on April 16, 2003, to the extent not superseded or amended by the PCAOB; and (2) Standards Nos. 2 and 3, and Interpretation 99-1 of the Independence Standards Board, to the extent not superseded or amended by the PCAOB.

23SeeAuditor Independence with Respect to Certain Loans or Debtor-Creditor Relationships, Release No. 33-10491 (May 2, 2018) [83 FR 20753 (May 8, 2018)], Comment Letter from PwC dated June 29, 2018, page A10.

24Revision of the Commission’s Auditor Independence Requirements, Release No. 33-7919 (Nov. 21, 2000) [65 FR 76008 (Dec. 5, 2000)]

26Bylaws and Rules of the Public Company Accounting Oversight Board(as of January 29, 2019)

27See Auditor Independence with Respect to Certain Loans or Debtor-Creditor Relationships, Release No. 33-10491 (May 2, 2018) [83 FR 20753 (May 8, 2018)], Comment Letter from PwC dated June 29, 2018, page A8, footnote 8.

28See page VIII:18(a) of the final report.

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Add to favorites

Preparing TOC

Link copied

Add to favorites

Please ensure

that you select Print Background (colors and images)

when printing.