IFRS Financial reporting considerations for entities participating in the voluntary carbon market

Publication date: 03 Mar 2023

uk In depth INT2023-02

Foreword

The voluntary carbon market (VCM) is growing. Consistent accounting practices for carbon offsets is relevant for companies that use carbon offsets to achieve their emission reduction targets, companies who develop carbon offsets and companies who trade or invest in carbon offsets.

There are no accounting standards or IFRS interpretations that directly address the accounting for carbon offsets and related projects. This publication considers how the accounting for carbon offset arrangements by the various counterparties can be addressed using current accounting standards and interpretations as at the date of publication. Note that interpretations are subject to change as the markets, standards and practices evolve.

In the compliance market, companies receive carbon emission allowance/credits from the government or purchase them to meet their compliance requirement on carbon emissions. There are common issues between compliance and voluntary carbon markets on the accounting for transferrable or tradable carbon credits. However, companies who receive carbon emission allowance/credits from the government in the compliance market also need to consider the accounting for the government grant and its emission provision. This publication only considers the accounting for carbon offsets in the voluntary carbon market. See PwC’s publication Emissions trading systems: the opportunities ahead for further details on implications of and accounting for compliance emission trading systems.

With the increasing focus on climate change and carbon emissions, companies are starting to take steps to reduce or absorb their carbon emissions. Complete elimination of carbon emissions from operations through mitigation methods is not always possible. This drives demand for carbon offsets to offset all or part of the remaining emissions generated by an entity’s operations or in its value chain.

1.1. What is a carbon credit?

A carbon credit is an emission unit issued by a carbon crediting programme that represents an emission reduction or removal of one metric tonne of CO2 or an equivalent amount of other greenhouse gases. They are uniquely serialised, issued, tracked and cancelled by means of an electronic registry.

Certified carbon credits typically take the form of transferable or tradable instruments and are certified by governments or independent certification bodies.

1.2. Compliance versus voluntary carbon markets

Carbon credits can be used by companies to meet:

compliance requirements, such as a net emission cap or the cap under an Emission Trading Scheme or ETS (also referred to as ‘cap and trade’) where companies are typically allocated emission allowances based on their targeted levels of emissions; or

voluntary emission targets. This is called the voluntary carbon market or VCM.

Carbon credits used to offset emissions voluntarily are often referred to as ‘carbon offset credits’ or ‘carbon offsets’. In this publication they will be referred to as carbon offsets.

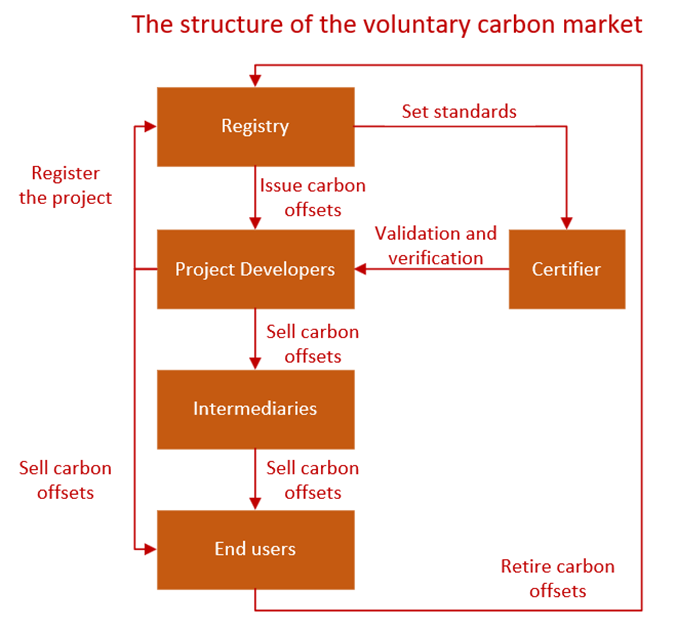

1.3. Life cycle of a carbon offset

The life cycle of a carbon offset in the VCM can be summarised as:

Generation of carbon offsets: A carbon offset project developer (Project Developer) registers an offset project with a carbon offset registry under a carbon offset program. The emissions reduction will be measured using a specified methodology. The Project Developer will implement the project and maintain records quantifying the emission reductions achieved. These are often validated and verified by government or independent certification bodies in order for the carbon offsets to be certified. Certified carbon offsets are issued by a carbon offset registry to the registry account of the Project Developer.

Transfer of carbon offsets: The carbon offsets are tradeable or transferable between accounts with the same registry. The ownership of the carbon offsets can be transferred from Project Developers to intermediaries and ultimate end users. These transactions are usually facilitated by carbon brokers, private carbon trading platforms and carbon exchanges.

Retirement of carbon offsets: The end user is required to instruct the registry to ‘retire’ the carbon offsets when they report them as a reduction of their emissions. This stops the carbon offsets from being used again by another entity.

The following diagram shows the VCM and the parties involved in a simple form.

Although relatively new, the carbon offset markets are growing. A certified carbon offset delivered in a transferable or tradeable format to the entity’s registry account can typically be resold for cash. A unit of certified carbon offset will meet the definition of an intangible asset under IAS 38, ‘Intangible Assets’, as “an identifiable non-monetary asset without physical substance”, if it is transferable or tradable. The reasons are:

it is a resource controlled by an entity (that is, the entity has the power to obtain the economic benefits that the asset will generate and to restrict the access of others to those benefits) as a result of past events and from which future economic benefits are expected to flow to the entity;

it is identifiable as it can be sold, exchanged or transferred individually;

it is not cash or a monetary asset; and

it has no physical form.

2.2. Classification, recognition and measurement

IAS 38 paragraph 2 states that it should not be applied for intangible assets that are within the scope of another standard. As such, IAS 38 accounting principles apply to carbon offsets only when they do not fall within the scope of another standard. This section considers the accounting implications of falling within the scope of IAS 2 or IAS 38 along with certain other classification and measurement issues.

2.2.1. Inventory accounting

Certified carbon offsets would meet the definition of inventories in IAS 2 under the following circumstances:

they are assets held for sale in the ordinary course of business; or

they are assets in the form of materials or supplies to be consumed in the production process or in the rendering of services.

Inventories are generally measured at the lower of cost and net realisable value in accordance with the measurement requirements of IAS 2. Where the inventory is made up of a large number of similar items, please refer to paragraphs 25.30 - 25.33 of the PwC Manual of Accounting. Also see FAQs 3.2.1 and 3.2.2 for discussion on when carbon offsets purchased might meet the definition of inventory and Section 4.1 for the accounting considerations around their costs of generation.

However, broker-trader entities that consider carbon offsets to be commodities can elect to measure them at fair value less costs to sell with changes in fair value recognised in profit or loss. See FAQ 2.2.1.1 below for further information.

The carbon offsets will not meet the definition of inventory if the entity holds carbon offsets only for investment purposes (that is, capital appreciation) over extended periods of time or sells carbon offsets outside of its ordinary course of business.

Carbon offsets that do not meet the inventory definition as discussed in the section above will be accounted for as intangible assets under IAS 38, provided they meet the definition and recognition criteria for intangible assets.

Under IAS 38, an intangible asset is recognised “if, and only if:

it is probable that the expected future economic benefits that are attributable to the asset will flow to the entity; and

the cost of the asset can be measured reliably.”

Purchased carbon offset intangibles that can be resold would meet both criteria. Entities that develop carbon offset intangibles for own use need to demonstrate that the offsets meet the intangibles definition (see Section 2.1) and recognition criteria above.

Carbon offset intangibles meeting the recognition criteria above are initially measured at cost. For each unit of carbon offset, there is generally no consumption of its economic benefits until it is derecognised. As such, each carbon offset would subsequently be carried at cost less any accumulated impairment losses (see FAQ 3.2.3) or, as permitted under IAS 38, measured using the revaluation model if an active market exists for the acquired carbon offsets. Where the quality and prices of certified carbon offsets vary widely, there might be little evidence to support the existence of an active market. See Section 2.3 for the relevant factors to consider.

For carbon offset intangibles measured using the revaluation model, the entity will need to determine an appropriate frequency for revaluing the assets. The timing of when an asset was last revalued is important when the asset is disposed of. This is because any difference between the carrying amount at the last revaluation date (less any subsequent accumulated amortisation or impairment losses) and the proceeds on the date of disposal will be recognised in profit or loss (refer to FAQ 21.88.1 in the PwC Manual of Accounting).

Entities involved in the VCM need to consider the appropriate accounting before obtaining or generating any carbon offsets. The range of possible classifications, as well as their associated measurement, shows the importance of understanding the entity’s business model/purpose for holding the asset. This increases the importance of implementing specific accounting policies, ensuring their consistent application to similar transactions and appropriate disclosures. Where an entity can evidence the existence of clearly distinguished portfolios of similar assets held for different purposes, different treatments might apply within an entity.

Examples of other activities that require careful consideration include:

Upfront investment in a Project Developer and the accounting for subsequent returns on the investment. The ‘investor’ and ‘developer’ should consider the appropriate accounting for the upfront payment. See Sections 3.1 and 4.4 for further details.

Agreements to acquire/sell carbon offsets in the future. Entities that are acquiring carbon offsets to offset their own emissions and project developers selling self-produced carbon offsets are likely to meet the ‘own use’ exemption under paragraph 2.4 of IFRS 9. However, entities engaged in trading carbon offsets need to consider whether the contracts to acquire and sell such carbon offsets are within the scope of IFRS 9. This would be as a result of the contract having a net settlement feature as explained in paragraph 2.6 of IFRS 9. Entities would, therefore, need to account for the contracts for future purchases and sales at fair value through profit or loss (FVTPL). See Sections 3.1 and 4.4 for further details.

Project Developers need to assess the appropriate accounting for their operational activities. For example:

Developers need to consider whether costs incurred in the development of carbon capture or other similar projects meet the criteria for capitalisation under IAS 16 or IAS 38. See Section 4.3 for further details

Carbon offsets could also result from forestry projects where trees are being held with the sole purpose of generating and selling carbon offsets. In such situations, the accounting for the offsets would depend on first determining the appropriate accounting for the trees, including whether they are in the scope of IAS 41. Some commonly witnessed scenarios are discussed in more detail from Section 4.2.

The role of the entity in the VCM and the intended use of the carbon offsets will also impact the classification of its cash flows in the cash flow statement.

There are further complications for entities that need to reference fair value when they account for carbon offsets. As noted above, this could include carbon offset commodities carried by broker-traders at fair value through profit or loss or carbon offset intangibles measured under the revaluation model.

IFRS 13, ‘Fair Value Measurement’, defines fair value as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date”, and it sets out a framework for determining fair values under IFRS.

Some high level factors to consider are included below:

Active market:

Appendix A to IFRS 13 defines an active market as one “in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis”.

A benchmark for evaluating the depth of a market could include active trading days within a given time period. A metric for volume that could also be considered is the average daily turnover ratio. This is calculated by dividing the average daily trading volume by the total amount of outstanding carbon offsets.

IFRS 13 does not define thresholds for frequency (such as active trading days) and volume (such as turnover ratio) to determine if an active market exists. This means that the conclusion requires professional judgement. In assessing whether an active market exists in a region for a particular type of carbon offsets, an entity should also consider whether reliable trading data is available.

In some cases, there might be several markets for a particular type of carbon offsets that meet the definition of an active market and each of those markets might have different prices at the measurement date. In these situations, IFRS 13 requires the entity to determine the principal market for the asset.

The principal market will be the market with the greatest volume and level of activity for the relevant type of carbon offsets that the entity holding the type of carbon offsets can access. IFRS 13 also contains a tiebreaker if there is not a clear principal market (that is, because there are several markets with approximately the same level of activity). In the case of a tie, IFRS 13 defaults to the most advantageous market within the group of active markets that the entity has access to with the highest activity levels.

If no active market exists, any carbon offsets held should not be fair valued. However, the entity may still be required to account for contracts to acquire the carbon offsets in the future at fair value, if such contracts have a net settlement feature and are not for the entity’s ‘own use’ (see Section 3.1). This would require the use of other directly or indirectly observable inputs (level 2 in the fair value hierarchy) or a valuation model (level 3).

Valuation techniques:

In many cases, the market approach [IFRS 13 para B5] will be the most appropriate technique for contracts to acquire carbon offsets in the future, because this would be used by a market participant. However, there might be particular facts and circumstances where an entity could demonstrate that a market participant would use a different approach. The cost approach [IFRS 13 para B8] or the income approach [IFRS 13 para B10] is likely to be rare in practice.

In determining an appropriate valuation technique, IFRS 13 indicates that the technique should be appropriate in the circumstances, and it should maximise the use of relevant observable inputs and minimise the use of unobservable inputs.

In general, a valuation model should be applied consistently from period to period. The market for carbon offsets is evolving rapidly and valuation techniques used by market participants are likely to evolve. IFRS 13 permits an entity to change valuation techniques (or change weightings amongst multiple valuation techniques) where the change results in a measurement that is equally, or more, representative of fair value, in the circumstances. The development of new markets, availability of new information or changing market conditions might result in changing valuation techniques.

Disclosure:

IFRS 13 contains a number of disclosure requirements. Given that markets for carbon offsets are rapidly evolving, determining the fair value can be complex. IFRS 13 provides advice on the level of detail necessary to satisfy the disclosure requirements, how much aggregation or disaggregation to undertake and whether users of financial statements will need additional information to evaluate the quantitative information disclosed.

2.4. Derecognition

Carbon offsets should be derecognised when they are sold, transferred or retired.

As discussed earlier, when carbon offsets are used to offset a company’s own emissions, the company is required to instruct the registry to ‘retire’ the carbon offsets. In some cases, the carbon offsets are simultaneously purchased and retired. See Section 3 below about the end users’ accounting when carbon offsets are retired.

3.1. Contracts to obtain carbon offsets in the future

Section 2 broadly sets out the accounting considerations for carbon offsets. Some entities will enter into contracts to obtain carbon offsets in the future instead of purchasing carbon offsets from the market based on spot price. Accounting treatment for these contracts can vary depending on the arrangement.

3.2. Carbon offsets held for ‘use’ in the business

Entities usually purchase carbon offsets from the voluntary carbon market to achieve their overall voluntary emission targets. Some entities also purchase carbon offsets to produce ‘carbon-neutral’ products. Some entities purchase carbon offsets that may be used for either purpose.

Entities should consider the specific facts and circumstances and apply the accounting principles as outlined in Section 2 above. Entities need to consider if the carbon offsets purchased shall be classified as an intangible asset under IAS 38 or inventories under IAS 2. Carbon offsets purchased by an entity that will be retired to achieve its overall emissions targets will usually be classified as intangible assets. See FAQs 3.2.1, 3.2.2 and 3.2.3 below for situations when they could be classified as inventories initially or subsequently. Refer to Section 2.2 for measurement. They are derecognised when the offsets are retired to offset emissions.

Entities should consider the accounting implications in Section 3.1 if they are entering into contracts to obtain carbon offsets in the future.

Intermediaries in the carbon market include many different types of entities with varying roles. Examples of intermediaries include:

Investors in product developers, whether private equity houses or individual corporate entities looking to secure access to a supply of carbon offsets. Such investors may provide funding upfront or over time and the contracts may be financial (equity, loan or a FVTPL financial asset including derivatives) or non-financial (a lease, an executory carbon offsets purchase contract (including a prepayment) or a purchase of an intangible asset) as discussed under Section 3.1. An investor will not be seen as an intermediary if it receives carbon offsets in return for its investment and intends to ‘use’ those in its own business.

Asset managers developing funds that either invest directly in product developers’ shares or in the carbon offsets themselves.

Broker-traders in carbon offsets. See Section 3.1 for factors to consider where carbon offsets are forward purchased or sold and Section 2.2.1 for the accounting required for carbon offsets held by such entities.

Other participants would include carbon offsets consultants and the carbon exchanges themselves.

The intermediaries above also need to assess whether they act as principals or agents of the carbon offsets transaction in accordance with IFRS 15.

For entities that act as principals (for example broker-traders and investors who obtain carbon offsets for sale), the carbon offsets they purchased from the market or obtained from investments will be recorded as inventories on acquisition (refer to Section 2.2 above for measurement). Please refer to Section 3.1 for further discussion on contracts to obtain carbon offsets in the future (as opposed to purchases at spot price).

For entities that act as agents for the carbon offset transactions, for example carbon offset consultants or carbon exchange, they should not report the carbon offset transactions as their own. However, they act as the principal for their relevant services and should account for their service revenue in accordance with IFRS 15. Sometimes such agents may receive a share of the carbon offsets as the consideration for their services provided. These carbon offsets received should be considered as non-monetary consideration and initially measured at their fair values. Subsequently if the carbon offsets are sold for cash, the sale might be reported as other revenue or other income.

3.4. Provisions

An entity participating in the voluntary carbon market needs to consider whether it should recognise a liability or a provision in accordance with IAS 37 as a result of its announcement(s) of its commitment to emission reduction targets. This is regardless of whether carbon offsets have been obtained (purchased or accessed otherwise).

IAS 37 defines a liability as “a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits”. An obligating event is an event that creates a legal or constructive obligation that results in an entity having no realistic alternative to settling that obligation.

An entity that makes an announcement of its emission reduction targets should consider whether the announcement creates a constructive obligation on it to carry out activities that consume resources to negate the emissions it generates. IAS 37 defines a constructive obligation as an obligation that derives from an entity’s actions where:

by an established pattern of past practice, published policies or a sufficiently specific current statement, the entity has indicated to other parties that it will accept certain responsibilities; and

as a result, the entity has created a valid expectation on the part of those other parties that it will discharge those responsibilities.

However, the existence of only a constructive obligation is not sufficient to recognise a liability. If it is determined the announcement creates a constructive obligation, the entity needs to further assess when the constructive obligation becomes a ‘present’ obligation without realistic alternatives as a result of past events. Generally the announcement of a commitment to reduce emissions by a future date does not result in a liability prior to the compliance period.

4. Accounting considerations for Project Developers

Carbon offsets can be produced by a variety of activities that reduce greenhouse gas emissions or increase carbon sequestration. In most cases, these activities are undertaken as discrete ‘projects’. A carbon offset project, for example, may involve:

renewable energy development (displacing fossil-fuel emissions from conventional power plants);

the capture and destruction of high-potency GHGs like methane, N2O, or HFCs; or

forestation or restoration of forests (trees planted to absorb carbon).

The Project Developer should carefully analyse the accounting considerations for the costs incurred for the underlying project that generates carbon offsets and their contracts to deliver carbon offsets in the future.

4.1. Costs incurred to generate carbon offsets

Project Developers may incur significant costs developing the appropriate technology and building assets that will enable carbon offset to take place and carbon offsets to be earned/generated. Please refer to Section 4.3 for accounting considerations for research and development and other costs.

The project activities often involve the use of certain physical assets, for example trees. Accounting for the underlying assets generating carbon offsets can be complex. Please refer to Section 4.2 for accounting for trees held to generate carbon offsets.

4.2. Accounting for trees held to generate carbon offsets

Project Developers that plant trees to absorb carbon to generate carbon offsets need to consider the accounting treatment for the trees. Considering the nature and intended use of the trees, entities need to determine whether the trees are

biological assets that should be accounted for in accordance with IAS 41; or

bearer plants that should be accounted for in accordance with IAS 16; or

assets not related to agricultural activity.

Trees meet the definition of a biological asset under IAS 41. Trees that relate to agricultural activity (except those that meet the definition of a bearer plant) should be accounted for in accordance with the requirements of IAS 41. IAS 41 defines agricultural activity as “the management by an entity of the biological transformation and harvest of biological assets for sale or for conversion into agricultural produce or into additional biological assets”. Agricultural produce is defined as “the harvested produce of the entity’s biological assets”.

Carbon sequestration is the process of capturing and storing atmospheric carbon dioxide. It is recognised as a key method for reducing the carbon in the earth’s atmosphere with the goal of reducing global climate change.

Carbon sequestration can happen in two basic forms: biologically or geologically. Biological carbon sequestration happens when carbon is stored in living plants. Geological carbon sequestration is technological and happens when carbon is stored in underground geological formations or rocks or depleted oil and gas reservoirs, deep unmineable coal beds, retired salt mines and so on.

An increasing number of entities are investing in developing technologies that would enable carbon capture and storage (CCS) at a massive scale. The majority of these projects are currently in research and development phases. The regulatory policies governing such projects vary between countries and the associated commercial models are still a work in progress in many cases. These factors introduce complexity and involve significant judgement in determining if the research and development costs incurred on such projects meet the capitalisation criteria under IAS 38 and/or IAS 16.

In the following sections, we discuss the accounting considerations related to the following topics:

the application of IAS 38 to research and development expenditure incurred in respect of a CCS project; and

the application of IAS 20 for accounting for government grants provided to a CCS project.

4.3.2 Research and development expenditure

The process of generating an intangible asset is generally divided into a research phase and a development phase. This applies to CCS projects where significant costs are incurred before the start of the construction of physical infrastructure. These costs are incurred on activities such as studies evaluating suitable technologies, producing conceptual project designs, pigging, seismic surveys, establishing technical, commercial and economic feasibility and evaluating potential locations for development. Whether these costs can be capitalised as intangible assets can involve significant judgement in determining if the activities amount to development and meet the criteria outlined in IAS 38.

IAS 38 defines research as the “original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding”. Paragraph 54 of IAS 38 stipulates that ‘expenditure on research (or the research phase of an internal project) should be recognised as an expense when it is incurred’. Two examples of research activities provided in IAS 38 are:

‘activities aimed at obtaining new knowledge; and

the search for, evaluation and final selection of, applications of research findings or other knowledge.’

In contrast, paragraph 57 of IAS 38 provides that an intangible asset arising from development (or from the development phase of an internal project) should be recognised provided certain criteria are met. Development is defined as “the application of research findings or other knowledge to a plan or design for the production of new or substantially improved materials, devices, products, processes, systems or services before the start of commercial production or use”.

4.3.3 The application of IAS 20 for accounting for government grants provided to a CCS project

Given the ever-increasing focus on reducing and mitigating carbon emissions, many governments are assisting the development of CCS and other green projects in one form or another. The nature and extent of government support may vary across jurisdictions and projects.

Entities need to assess whether the government support is a government grant or another form of government assistance based on the definition and scope of IAS 20. The distinction is important because the accounting requirements of IAS 20 only apply to government grants. In particular, the definition of government grants excludes the following forms of government assistance:

Assistance to which no value can reasonably be assigned.

Transactions with the government that cannot be distinguished from the normal trading transactions of the entity.

Paragraph 2 of IAS 20 also excludes grants related to income tax, biological assets measured at its fair value less costs to sell or government participation in the ownership of an entity from the scope of IAS 20.

The nature of government support in respect of CCS projects varies and a detailed analysis based on specific facts and circumstances will be required to determine the nature of support and, therefore, the applicable accounting standard and appropriate accounting treatment.

For example, the UK government’s Net Zero Strategy sets out policies and proposals for decarbonising all sectors of the UK economy by 2050. The nature of government assistance committed for CCS and other industries includes legislative changes, direct revenue support, contracts for differences schemes, dispatchable power agreements and so on. Each of these schemes would require an assessment based on their specific terms and conditions to determine the appropriate accounting treatment.

Legislative changes for example, that only provide indirect support to a particular industry would typically be outside the scope of IAS 20. This is on the basis that the definition of government assistance under the standard does not include “benefits provided only indirectly through actions affecting general trading conditions, such as the provision of infrastructure in development areas or the imposition of trading constraints on competitors”.

Governments also sometimes provide assistance through tax incentive schemes and entities need to analyse the requirements and terms of each tax offset or incentive to determine the applicable accounting standard.

4.4. Contracts to deliver carbon offsets in the future

Like the issues discussed under Section 3.1 from the investors’ perspective, Project Developers entering into contracts to deliver carbon offsets in the future should also carefully assess the contract to determine whether the nature of the arrangement is financial (equity, loan, a FVTPL financial instrument including derivatives), or non-financial (a lease, an executory carbon offsets sales contract (including a prepayment) or a sale of an intangible asset).

If the contract falls into IFRS 15 and an initial payment is received from the customer, the Project Developer will also need to assess whether a significant financing component exists.

Where contracts fall into IFRS 15 and include goods or services other than the carbon offsets (for example renewable electricity), the delivery of the carbon offsets will be considered a separate performance obligation. The PwC In depth on Accounting for Green/Renewable Power Purchase Agreements from the Buyer’s Perspective discussed the accounting considerations from the Renewable Energy Credits (REC) purchaser’s perspective. Similar considerations apply from Project Developer’s perspective.

FAQ 2.2.1.1 - How and when should an entity apply the commodity broker-trader exemption under IAS 2 for its holding of carbon offsets?

An entity might actively purchase carbon offsets principally with the purpose of selling in the near future to generate a profit from fluctuations in the price or traders’ margin. In this instance, the entity might want to consider whether the guidance in paragraph 3(b) of IAS 2, ‘Inventories’ for commodity broker-traders applies to the carbon offsets they trade, and if so, elect to measure the carbon offsets at fair value less costs to sell with changes in fair value recognised in profit or loss.

Question 1:What is the unit of account in assessing whether an entity qualifies for the IAS 2 commodity broker-trader exemption?

The standard requires that an entity can only apply the exemption under paragraph 3(b) of IAS 2 if the entity qualifies as a commodity broker-trader. As such, the accounting policy should be applied on a case-by-case basis. This means each type of carbon offset should be separately assessed for whether:

the type of carbon offsets held by the entity is within the scope of IAS 2;

the entity actively purchases such type of carbon offsets principally with the purpose of selling in the near future to generate a profit from fluctuations in the price or traders’ margin; and

the type of carbon offsets qualifies as a commodity (further explained below).

An entity can only apply the commodity broker-trader exemption where the separate type of offsets meets all of the criteria above. Where a condition changes which might impact whether the type of offsets meets the criteria above, the entity should reassess whether the exemption continues to apply.

Question 2:When would carbon offsets be considered as a form of commodity under IAS 2?

There is a lack of definitive guidance under as to what constitutes a commodity. Judgement should be exercised in determining whether a particular type of carbon offsets can be regarded as a commodity. Carbon offsets might be considered as a commodity if:

the type of carbon offsets is traded in an active market and a reliable value can be assigned to the asset; and

the type of carbon offsets is fungible.

Whether or not a type of carbon offsets is traded in an active market is subject to judgement. An entity should apply the principles of IFRS 13 in determining whether an active market exists for each type of carbon offset under consideration. See Section 2.3 for further details.

Question 3: When would an entity be considered to be carrying on business as a broker-trader for carbon offsets?

Paragraph 5 of IAS 2 notes that “Broker-traders are those who buy or sell commodities for others or on their own account”. It continues that “The inventories referred to in paragraph 3(b) are principally acquired with the purpose of selling in the near future and generating a profit from fluctuations in price or broker-traders' margin”. There is no other guidance to help identify who is a broker-trader. Surrounding facts and circumstances need to be considered, and the application of judgement might be necessary.

Assuming that the carbon offsets that the entity is trading qualify as a commodity (further explained in Question 2 above), the following are factors to consider when assessing whether the entity is carrying on business as a broker-trader:

The carbon offsets have been purchased with a view to resale, generating profit from fluctuations in price or broker-traders’ margin. The entity’s business model, investment policy and processes align with that profit objective – for example, the entity frequently enters into offsetting positions to lock in margin gains.

There is a past practice of frequent transactions (buy or sell). For example, the entity transacts within the short term, which might be a few days or, for some traders, it might be minutes or hours. The longer the carbon offsets are held, the more likely it is that they are held for long-term capital appreciation or for use in the business/to offset production-related emissions (that is, the entity is less likely to be considered a broker-trader).

Key management personnel assess performance of the business based on fair value (that is, not only realised profits).

FAQ 2.2.2.1 - How should carbon offsets classified as intangible assets assets measured at revalued amount be presented in the financial statements?

‘Revalued amount’ is defined as the assets’ fair value at the date of the revaluation less any subsequent accumulated amortisation and any subsequent accumulated impairment losses. If an entity measures intangible assets using the revaluation model, paragraph 85 of IAS 38 requires gains as a result of the revaluation to be recognised in other comprehensive income (‘OCI’) and accumulated in equity under the heading of ‘revaluation surplus’. Entities should note this difference in presentation for intangibles carried at a revalued amount versus carbon offsets included in inventory and carried at fair value through profit or loss if the broker-trader exemption is used.

Certain industries manage their business on a fair value basis and therefore may wish to provide additional fair value disclosures. If management decides to disclose separately the fair value, its financial impact (which will not have been included in net profit), or other management information regarding the carbon offsets outside the financial statements (a non-GAAP measurement), a reconciliation might be required (depending on local regulatory requirements) illustrating the differences between the IFRS balance and the non-GAAP measurement.

FAQ 2.2.2.2 - Should carbon offset intangible assets be classified as current or non-current assets?

IAS 1 para 67 states that the standard uses the term ‘non-current’ to include tangible, intangible and financial assets of a long-term nature. Intangible assets are generally classified as non-current assets on the balance sheet on the basis that they are usually consumed over a long term. However, unlike IAS 16, IAS 38 does not prescribe that intangible assets are expected to be used during more than one period. When entities hold carbon offsets with an expectation to retire them within 12 months (or the entity’s normal operating cycle) from the reporting date, such carbon offsets will meet the requirement under IAS 1 para 66 to be classified as current intangible assets on the balance sheet.

An entity may hold carbon offsets with the expectation that some of them will be retired within 12 months (or the entity’s normal operating cycle) from the reporting date and some will be retired later. Neither IAS 1 nor IAS 38 provides explicit guidance on the unit of account for determining current and non-current classification and therefore judgement needs to be applied. In such cases the carbon offsets can be split into current intangible assets and non-current intangible assets based on the expected timing of consumption.

FAQ 2.2.3.1 - How should cash outflows to purchase carbon offsets or obtain carbon offsets in the future be classified in the cash flow statement?

When carbon offsets meet the definition of inventories (see FAQs 3.2.1 and 3.2.2), the carbon offsets will be recorded in inventory initially or at some point and subsequently in cost of sales when retired. The cash outflows to acquire these carbon offsets are generally presented within operating cash flows. Commodity broker-traders also generally present cash inflows and outflows relating to the sale and purchase of carbon offsets within operating cash flows.

IAS 7 para 16 includes cash payments to acquire intangible assets and other long term assets as an example of an investing activity. Cash outflows to purchase intangible assets are generally classified as investing cash flows in the cash flow statement. This is on the basis that intangible assets are usually consumed over a long term. However, when entities purchase carbon offsets with the expectation to retire them within 12 months (or the entity’s normal operating cycle) from the reporting date, cash outflows to purchase carbon offsets in such a case might reasonably be classified as operating cash flows.

To the extent that an initial payment is made as part of a financial or non-financial investment to obtain carbon offsets in the future (see Section 3.1), the initial cash outflow is likely to be reported within investing cash flows in many cases. The settlement of the balance via the receipt of carbon offsets will not be a cash flow, but may require disclosure as a significant non-cash transaction.

FAQ 2.4.1 - How should an entity determine the cost of carbon offsets in the future?

An entity that classified its carbon offsets as intangible assets, measured using the cost model, needs to determine the cost of the assets upon their usage or disposal. IAS 38 has no guidance on determining the cost of an individual unit of intangible asset on its usage or disposal where the entity holds a large number of similar items.

Management should use its judgement in developing and applying an accounting policy in the absence of an IFRS that specifically applies to a transaction, other event or condition [IAS 8 paras 10-12]. As such, management of an entity can refer to the principles of IAS 2 in determining the cost of an individual carbon offset upon its usage or disposal where there are a large number of similar items. Techniques for arriving at cost, instead of using actual costs, can be used where there are a large number of similar items. The entity should consider the type of carbon offsets when assessing whether they are similar items. For further discussion regarding cost measurement under IAS 2, please refer to paragraphs 25.30 - 25.33 of the PwC Manual of Accounting.

FAQ 3.1.1 - How to account for contracts to obtain carbon offsets in the future?

Entities may invest directly in carbon offset projects by contracting with Project Developers. Typically, the investors will provide the project funding up front or over time and in return they may receive a share of the carbon offsets produced during the contract period. The investors should carefully assess the contract to determine whether the nature of the arrangement is financial (equity, loan, a FVTPL financial instrument including derivatives) or non-financial (a lease, an executory carbon offsets purchase contract (including a prepayment) or a purchase of an intangible asset that entitles the entity to a share of the output of a project).

As the investor(s) has the exposure or rights to the variable returns from the carbon offset project, it should evaluate the terms of the arrangement to assess whether it is involved in the relevant decisions of the project that may constitute control, joint control or significant influence according to IFRS 10, IFRS 11 and IAS 28 requirements.

If the investment does not constitute an interest in a subsidiary, joint arrangement or associate, the investor should further assess whether the contract contains a lease under IFRS 16. The contract is deemed to contain a lease if the entity has (i) the right to substantially all of the economic benefits generated from an identified asset (for example land or forest) during the term of the contract, and (ii) the right to direct the use of the identified asset. In such a case, the entity may be required to recognise a right-of-use asset and corresponding lease liability in accordance with IFRS 16.

Where the entity assesses that it has no control over the use of the project assets, further analysis depends on whether the contract has a net settlement feature and whether it is subject to any scope exceptions in IFRS 9. See FAQ 40.83.1 in PwC Manual of Accounting for more details.

FAQ 3.1.2 – When is a prepaid contract to purchase carbon offsets in the future within the scope of IFRS 9 for the buyer?

Background

Entity A wants to secure a long-term supply of carbon offsets. In order to obtain a sufficient supply, on 1 January 20X1, entity A enters into a streaming arrangement with entity B in which entity A will make an upfront non-refundable payment of C1 million to entity B and, in return, entity A will obtain the right to receive a fixed number of carbon offsets from entity B in the future.

Entity B will use the upfront payment received by entity A and other investors to fund its initiative (project R) to protect and preserve a tropical rainforest which has high carbon storage capacity.

Entity B will deliver 10,000 carbon offsets annually to entity A for a period of 10 years starting from 1 January 20X5 (C10 per offset). It is anticipated that the price of a carbon offset will exceed C10 per offset by 1 January 20X5.

There are no clauses in the contract that cause any variation of any cash flows over the contract’s term. No further payments are required over the life of the contract as the carbon offsets are delivered.

If entity B is unable to generate sufficient carbon offsets (from project R or any of its other projects), the contract requires entity B to purchase carbon offsets for delivery to entity A. There are no terms in the contract that permit entity A or entity B to settle the contract net in cash.

Entity A does not have past practice of settling similar contracts net in cash or a practice of taking delivery of the underlying in similar contracts and selling it within a short period of time to generate profit from short-term fluctuations in price or dealer’s margin.

Issue

Entity A should consider the guidance in FAQ 3.1.1 to determine the relevant accounting standards that apply to its contract with entity B.

Entity A determines that the contract does not give rise to control, joint control or significant influence over entity B or project R, because entity B makes all of the decisions related to project R, and consent from entity A is not required.

Entity A determines that the contract does not result in the purchase of an interest in any of entity B’s assets, because it does not provide entity A with an undivided interest in any of entity B’s projects. As such, by entering into the contract to purchase carbon offsets, entity A has not purchased a tangible or intangible asset.

Entity A determines that the contract does not contain a lease, because it does not provide entity A with the right to receive substantially all of the outputs from any identified asset linked to any of entity B’s projects.

IFRS 9 applies to contracts to buy or sell a non-financial item where the contracts can be settled net in cash or another financial instrument or by exchanging financial instruments in accordance with paragraph 2.6 of IFRS 9 (net settleable contracts). Contracts to buy or sell carbon offsets could be examples of such contracts.

Some net settleable contracts are outside the scope of IFRS 9 where the contract to purchase or sell the carbon offsets was entered into and continues to be for the entity’s expected purchase, sale or usage requirements in accordance with paragraph 2.4 of IFRS 9. This is commonly referred to as the ‘own use’ exception.

Please refer to the examples below with differing assumptions that consider whether the contract is within the scope of IFRS 9 (to be read in conjunction with the background information above).

Example A

Assume that entity A has readily access to a liquid spot market for carbon offsets in which transactions take place with sufficient frequency and volume and prices are available on an ongoing basis.

As part of a diversification strategy, entity A plans on selling the carbon offsets that it will receive in the liquid spot market, with a trading objective of generating a profit from increases in the price of a carbon offset.

Question

Would the contract described in this example be within the scope of IFRS 9 for entity A?

Answer

Entity A readily has access to a liquid spot market for carbon offsets, so the contract to purchase carbon offsets meets the requirement in paragraph 2.6(d) of IFRS 9 (refer to EX 40.83.2 in the PwC Manual of Accounting); that is, the carbon offsets are readily convertible to cash, so the contract with entity B can be settled net in cash.

Since entity A plans on selling the carbon offsets in the liquid spot market with a trading objective, as opposed to securing the carbon offsets to meet its expected sale, purchase or usage requirements, the contract with entity B will not qualify for the ‘own use’ exception. Therefore, the contract will be within the scope of IFRS 9 for entity A.

Entity A has determined that it does not meet the ‘own use’ exception at inception of the contract, so it would not be able to reclassify the contract if circumstances change, subsequent to inception, and the entity assesses that it would subsequently meet the ‘own use’ exception. Please refer to FAQ 40.81.1 in the PwC Manual of Accounting for further details.

The contract does not meet the definition of a derivative in Appendix A to IFRS 9, because the investment of C1 million is fully prepaid at inception. The prepaid amount will be accounted for as if it were a financial asset. Since entity A has the right to receive a fixed number of carbon offsets in the future, and the fair value of credits received will vary, the contract does not meet the solely payments of principal and interest requirements under IFRS 9 as noted in PwC Manual of Accounting FAQ 40.79.1. Therefore, the financial asset is measured at fair value through profit or loss.

Example B

Assume that entity A does not have access to a liquid spot market for carbon offsets.

Entity A intends to use the offsets to offset its own emissions to achieve its own net-zero targets. Entity A does not intend to sell the offsets. In other words, the contract was designed by entity A to be used solely for its own usage requirements.

Question

Is the contract described in this example within the scope of IFRS 9 for entity A?

Answer

The contract cannot be settled net in cash, because:

the terms of the contract do not permit either entity to settle the contract net;

entity A does not have a practice of settling similar contract net in cash;

entity A does not have a practice of taking delivery of the underlying in similar contracts and selling it within a short period of time to generate profit from short-term fluctuations in price or dealer’s margin; and

the carbon offsets are not readily convertible into cash, because entity A does not have access to a liquid spot market(refer to EX 40.83.2 in the PwC Manual of accounting).

Since the contract is not net-settleable, it does not fall within the scope of IFRS 9. Instead, the prepaid amount should be accounted for as a non-financial asset – that is, a prepayment representing the right to receive carbon offsets.

Even if, at inception, the contract is not within the scope of IFRS 9, it should still be assessed to identify if there are any separable embedded derivatives that should be accounted for under IFRS 9. In this example, because there are no non-closely related embedded derivatives in the contract between entity A and entity B, there are no separable embedded derivatives in the contract.

Example C

Assume that entity A readily has access to a liquid spot market for carbon offsets in which transactions take place with sufficient frequency and volume and prices are readily available on an ongoing basis.

Entity A intends to use the offsets to offset its own emissions to achieve its own net-zero targets. Entity A does not intend to sell the offsets. In other words, the contract was designed by entity A to be used solely for its own usage requirements.

Question

Is the contract described in this example within the scope of IFRS 9 for entity A?

Answer

Entity A readily has access to a liquid spot market for carbon offsets, so the contract to purchase carbon offsets meets the requirement in paragraph 2.6(d) of IFRS 9; that is, the carbon offsets are readily convertible to cash, so the contract with entity B can be settled net in cash.

However, since entity A intends to use all of the offsets solely to offset its own emissions to achieve its own net-zero targets and does not intend to sell any offsets, entity A concludes that the purchases are in accordance with its expected usage requirements. In this case, entity A can apply the ‘own use’ exception. Accordingly, the contract is not within the scope of IFRS 9 at inception. Instead, the prepaid amount should be accounted for as a non-financial asset – that is, a prepayment representing the right to receive carbon offsets.

If, subsequent to inception, circumstances change and the contract no longer continues to be held for ‘own use’, the contract will subsequently be within the scope of IFRS 9. Refer to FAQ 40.84.7 in the PwC Manual of Accounting for further details.

Embedded derivatives would be considered in a similar manner to the discussion in Example B.

FAQ 3.2.1 - How should an entity account for purchased carbon offsets that will be used in production of its carbon-neutral products?

Entities may sell products that are labelled as ‘carbon-neutral’. The ‘carbon-neutral’ feature is determined based on the entity’s calculation of the quantity of emissions generated in the production process and the purchase and retirement of equivalent carbon offsets to make the production process carbon-neutral. These products have higher costs due to the purchase of carbon offsets and are usually sold at a premium versus similar products that are not carbon-neutral.

Under IAS 2, inventories include “materials and other supplies held for use in the production of inventories” or “materials or supplies to be consumed in the production process or in the rendering of services”. When carbon offsets are purchased for the sole purpose of producing carbon-neutral products, although they are not physically consumed in the production process, they could be considered to be consumed together with the production of carbon-neutral products. They would, therefore, meet the definition of inventories. An entity might need to apply judgement in this case to determine the point in time that the offsets become part of inventory, that is, when purchased or when retired as part of the production process. It might be acceptable to conclude that such carbon offsets will be scoped out of IAS 38 and classified as inventories when purchased. The carbon offsets will effectively be a raw material until the products are labelled as carbon-neutral. The classification should be applied consistently and disclosed appropriately.

The costs of the carbon offsets will be included in the cost of the carbon-neutral products when they are retired for the carbon-neutral products and included in costs of goods sold when the carbon-neutral products are sold.

FAQ 3.2.2 - How should an entity account for fungible carbon offsets that may be used either for production of carbon-neutral products or voluntary emission targets?

As discussed under Section 2.2, IAS 38 accounting principles apply when the carbon offsets held do not fall within the scope of another standard. It might make sense to classify fungible carbon offsets that could be used either for production of carbon-neutral products or the achievement of overall voluntary emission targets as intangible assets at the time of purchase. This is because, at the time of purchase, the entity cannot reliably conclude that the carbon offsets will be used in the production of goods. Depending on their usage, entities could include their costs in the cost of the carbon-neutral products (see FAQ 3.2.1 above) or expense their costs in profit and loss when the offsets are retired to achieve overall voluntary emission targets.

However, if the group designates separate pools for its fungible carbon offsets with different purposes and have appropriate controls in place, it might also be considered acceptable to determine the classification separately for each pool of carbon offsets.

FAQ 3.2.3 - How should carbon offset intangible assets held for voluntary use with no constructive obligation be tested for impairment under IAS 36?

Carbon offsets usually don’t have an expiry date. If the entity holds carbon offsets only for investment purposes (that is, capital appreciation) over an extended period of time, their useful life may be considered indefinite. However, their useful life will be considered finite if they are held to be sold within a short period of time outside of the entity’s ordinary course of business. When carbon offsets are held for voluntary use, each offset has a limited usage of one retirement. In such cases, their useful life will also be considered finite.

Carbon offset intangible assets considered to have indefinite useful life need to be tested annually for impairment. Different types of carbon offset intangible assets may be tested for impairment at different times. However, carbon offset intangible assets initially recognised during the current annual period should be tested for impairment before the end of the current annual period.

For carbon offset intangible assets considered to have finite useful lives, entities should assess, at each reporting date, whether there is any indication that carbon offsets held for use might be impaired.

Carbon offsets held for voluntary use with no constructive obligation usually do not generate cash inflows that are largely independent from other assets. Entities should identify the cash-generating unit (CGU) that the carbon offsets belong to, considering the intended retirement of the offsets. For example, if the carbon offsets are intended to be retired against the emissions of a specific operation identified as a CGU for impairment testing purposes, value in use should be determined for that operation.

Carbon offsets that are part of general net zero commitments may meet the definition of corporate assets under IAS 36. This is because they are likely to contribute to future cash flows of multiple CGUs. They should be tested for impairment by applying the approach prescribed in IAS 36.102.

Other carbon offset intangible assets that are not held for use (for example held for investment purposes over an extended period of time, or sold within a short period of time outside of the ordinary course of business) generate independent cash inflows at the individual asset (unit) level and should be tested for impairment separately. Carbon offsets that meet the definition of inventories (see FAQ 3.2.1) are measured at the lower of their cost and net realisable value under IAS 2.

FAQ 4.1.1 – How do Project Developers account for costs incurred to generate carbon offsets that are not costs to build physical assets?

Cash and non-cash costs (for example depreciation of physical assets) that are not costs to build physical assets may be incurred to generate carbon offsets. Carbon offsets generated by the Project Developer for sale will be classified as inventories, which are intangible in nature. Accordingly, costs that are directly attributable to the generation of carbon offsets will be capitalised as part of the cost of the carbon offset inventories. Such costs will also include a systematic allocation of fixed and variable production overheads in accordance with IAS 2.

Determining the cost of the offsets generated in accordance with IAS 2 can be a complex exercise. It requires an understanding of the carbon absorption or avoidance process for the particular project. Further, quantifying the number of carbon offsets that are to be generated over the life of a project and allocating the period on period costs to the expected units from a project is often challenging.

Entities should also analyse operating and maintenance costs incurred to identify (i) costs that enhance the underlying assets and can therefore be capitalised, and (ii) maintenance costs that should be expensed. Additionally, some projects may generate two or more products or services (for example renewable energy and carbon offsets). Costs incurred on such projects typically need to be allocated to the multiple products they produce.

Entities should analyse the specific facts and circumstances for each such project to determine how to account for the costs incurred before allocating them to the costs of carbon offset inventories in accordance with IAS 2.

FAQ 4.2.1 - Do carbon offsets generated by forests fall within the definition of agricultural produce?

No. Carbon offsets generated by the trees do not meet the definition of agricultural produce because they are not a ‘harvested produce’ from the trees. By nature, carbon offsets lack physical substance. The certification of a carbon offset due to the capture of a tonne of carbon does not represent a harvest from the trees.

FAQ 4.2.2 – How do Project Developers account for trees held to only generate carbon offsets?

Trees that are planted to only generate carbon offsets will not be accounted for under IAS 41 or as a bearer plant under IAS 16 as the trees serve no other purpose. They are tangible assets held for use in the ‘production’ of carbon offsets over a long term and, therefore, meet the definition of property, plant and equipment under IAS 16 and will be accounted for in accordance with IAS 16.

Expenditures to establish and develop the trees and related borrowing costs need to be assessed against the capitalisation criteria under IAS 16 and IAS 23 based on specific facts and circumstances. Entities should estimate the residual value (for example scrap sales) and the useful lives of trees considering its economic life during which they can absorb carbon dioxide. They should determine an appropriate method of depreciation by considering the pattern in which carbon offsets are expected to be generated from them. The depreciation charge will be included in the cost of carbon offset inventories.

FAQ 4.2.2.1 – How should project developers classify trees that are managed primarily to generate carbon offsets, where they will be harvested and sold at the end of the project?

Background

A carbon offset project developer plants timber trees that generate carbon offsets during the project life. In many cases, project developers are allowed to harvest the trees after a required period. The trees will be harvested and sold as timber at the end of the project. The developer manages the forest in accordance with the practices required for the certification of carbon offsets – that is, to generate as many carbon offsets as possible.

Question

How should the project developer classify these trees that are managed primarily to generate carbon offsets, where they will be harvested and sold at the end of the project?

Answer

Trees that relate to agricultural activity (except those that meet the definition of a bearer plant) should be accounted for in accordance with the requirements of IAS 41. Carbon offsets are not agricultural produce (see FAQ 4.2.1), hence the trees that do not produce agricultural produce will not meet the definition of a bearer plant under IAS 16.

The developer should therefore consider whether the definition of agricultural activity is met. Agricultural activity is defined as the management by an entity of the biological transformation and harvest of biological assets for sale or for conversion into agricultural produce or into additional biological assets.

Management of the trees, even though primarily managed for carbon offsets, would typically relate to the biological transformation of the trees and contribute to the timber to be harvested at the end of the project.

IAS 41 does not provide guidance on the extent of harvest needed to qualify as an agricultural activity. In our view, the developer might analogise to the definition of a bearer plant under IAS 16 that permits incidental scrap sales (for example, fruit trees sold for firewood at the end of their lives) not to taint the definition of bearer plants. As such:

Where the expected proceeds from harvest are considered to be more than incidental scrap sales, the trees should be accounted for as a biological asset under IAS 41, and accordingly measured at fair value less costs to sell.

Where the proceeds from harvest are expected to be incidental scrap sales, it is acceptable for the trees to be accounted for as an item of property, plant and equipment under IAS 16 (see FAQ 4.2.2), by analogy with the definition of bearer plants.

Judgement will need to be exercised on what is considered ‘incidental scrap sales’ in the context of the project – for example, by comparing the present value of the timber with the present value of both outputs (the carbon offsets and timber) to be generated from the trees.

See FAQ 4.2.4 for initial measurement of the carbon offsets generated from trees accounted for under IAS 41; and FAQ 4.2.3 for measurement of carbon offsets generated from trees that are accounted for under IAS 16.

FAQ 4.2.3 – How do project developers measure the carbon offsets generated from trees accounted for under IAS 16?

When the trees are accounted for under IAS 16, the carbon offsets they produce are accounted for under IAS 2. They are initially measured at cost and this will include the depreciation of the trees.

FAQ 4.2.4 – How do project developers initially measure the carbon offsets generated from trees accounted for under IAS 41?

When the trees that can generate carbon credits fall into IAS 41, because they are managed for agricultural activities, they are accounted for as biological assets and measured at fair value less costs to sell. This will include economic benefits related to the carbon offsets to be generated (see FAQ 33.21.3 in PwC Manual of accounting). Carbon offsets are generated over the life of the trees and they are separately recognised. The fair value of the trees is reduced by the fair value less costs to sell off the carbon offsets as the future cash flows of the trees no longer include these carbon offsets. It is therefore appropriate to treat the reduction in the carrying amount of the trees when carbon credits are generated, that is the fair value less costs to sell of the carbon credits, as the initial cost of the carbon offsets generated. The accounting outcome is similar to agricultural produce harvested from biological assets at the point of harvest.

EX 4.3.2.1 – Application of development costs recognition criteria to ‘green’ solutions to climate change

An entity involved in developing new ‘green’ technology (such as Carbon Capture and Storage), might incur significant research and development costs. Following EX 21.32.1 – Application of recognition criteria to each stage of the product life cycle in PwC’s Manual of Accounting, management should consider the product life cycle and then apply the recognition criteria listed in paragraph 57 of IAS 38 at each stage of that cycle. There is no generic indicator of the commencement point for capitalising such internal development costs. Management needs to use judgement based on the facts and circumstances of each project.

Costs incurred in developing these new technologies may include studies regarding technological innovation, conceptual project design, technical, commercial and economic feasibility and potential locations. These activities occur before the entity moves onto more detailed front-end engineering and design (commonly known as FEED) of a pilot facility or pre-use prototype.

The entity may expect there to be significant growth opportunities in the market over the coming years since such projects are a major part of many countries’ net zero proposals. When evaluating whether these types of projects meet the recognition criteria listed in paragraph 57 of IAS 38,

“An intangible asset arising from development (or from the development phase of an internal project) should be recognised if, and only if, an entity can demonstrate all of the following:

the technical feasibility of completing the intangible asset so that it will be available for use or sale.

its intention to complete the intangible asset and use or sell it.

its ability to use or sell the intangible asset.

how the intangible asset will generate probable future economic benefits. Among other things, the entity can demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset.

the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset.

its ability to measure reliably the expenditure attributable to the intangible asset during its development.”

The following considerations are helpful:

In meeting criteria (a), whether there are doubts about the technical feasibility of the project due to the extent the technology or product has been previously proven to work. Understanding the probability of success may be easier, for example, where there are adaptations of previous technologies for a different purpose rather than entirely new technology.

In meeting criteria (d), whether there are barriers to generating economic benefits due to the need for approval by a government or regulator. Some regulatory requirements may be easier to meet than others. A failure to meet regulatory requirements with a completely new product, could mean that the entire project fails. However, in many cases entities may have received pre-approval for certain aspects or be on an accelerated regulatory approval process to progress a country’s climate goals.

In meeting criteria (e), whether the availability of financial resources is sufficient to achieve a commercial production stage or pilot facility. Often ‘single purpose’ companies may have financing available only to a certain stage of their research. This may be a good indication of how feasible investors perceive the project to be. However, this may be less of a constraint for a larger well capitalised company that is generating revenue from other projects.

If the conclusion around capitalising these development costs is judgemental an entity should consider whether this should be disclosed as a significant judgement under IAS 1 para 122 in the financial statements.

As well as these intangible development costs, physical assets with a possible alternative use may be purchased as part of the development phase. These should be separately assessed for capitalisation under the recognition and measurement requirements of IAS 16 ‘Property, plant and equipment’ and depreciated over their useful economic life.

FAQ 4.3.2.2 - Can an entity capitalise research costs incurred to investigate ‘green’ solutions to climate change by applying IFRS 6?

Question

IFRS 6 states that an entity should determine an accounting policy specifying which expenditures are recognised as exploration and evaluation assets. In practice many entities in the extractive industries, for example, mining, oil and gas, have developed a policy of capitalising certain exploration and evaluation assets.

Entity A is an oil and gas entity and has incurred significant costs on researching certain carbon capture projects and investigating the feasibility of using existing technology and facilities/infrastructure owned or developed by themselves and other extractive entities in these projects.

Since the entity is itself engaged in extractive activities would it be able to develop a policy for such carbon capture under IFRS 6?

Answer

Extractive activities include:

exploration and evaluation - acquisition of legal rights, exploratory drilling and feasibility studies;

development - development drilling, development of mine sites and construction of facilities;

production - extraction and on-site processing;

processing and transport - processing, treatment, storage and transportation; and

closure - rehabilitating the mine or production site, plugging of wells and removal of infrastructure.

In many cases, green projects may involve ‘storage’ of carbon or hydrogen in existing oil and gas facilities or rehabilitation of existing mines or production sites for such other purposes.

However, the definitions in IFRS 6 confirm that exploration and evaluation expenditures are those incurred in the search for mineral resources (including minerals, oil, natural gas and similar non-regenerative resources), and in the determination of the technical feasibility and commercial viability of extracting the mineral resource, after the entity has obtained the legal rights to explore a specific area.

Although Entity A’s carbon capture project will utilise certain extractives technology or assets, the project does not generally involve the search for or evaluation of mineral resources. This is because it involves the sequestration of a gas. Therefore, the expenditure is outside the scope of IFRS 6 and should be evaluated under IAS 38 ‘Intangible assets’, which has specific guidance on the accounting for research and development costs.

However, in some cases plans may include the use of the stored CO2 for enhanced recovery techniques (refer to the International Energy Agency website for information) of resources. To the extent an entity is incurring such costs as part of the exploration of an oil field, there may be limited instances where it can be argued that these costs relate to the exploration and evaluation of oil and qualify as exploration and evaluation expenditures.

IAS 38 requires activities conducted under the research phase outside the scope of IFRS 6 to be expensed as incurred. Research is defined as “original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding” [IAS 38 para 8].

Other than in the limited cases where such expenditures can be argued to be within the scope of IFRS 6, they would likely meet the definition of research and should therefore be expensed. Entity A could consider whether it is possible to capitalise any costs as development costs as the project progresses by evaluating the costs incurred each period using the criteria for development costs in IAS 38 discussed in EX 4.3.2.1.

FAQ 4.4.1 – When is a prepaid contract to sell carbon offsets in the future within the scope of IFRS 9 for the seller and what are the relevant classification considerations?

Background

Entity A is a carbon offset project developer and currently has multiple carbon offset projects in its portfolio at various stages of development. As an output of its ordinary activities, entity A sells carbon offsets that are generated from its various carbon offset projects.

Entity A is embarking on a new wind energy project (project W) that aims to harness wind energy potential to balance energy needs in a particular region.

Entity A enters into a long-term contract on 1 January 20X1 to deliver a fixed number of carbon offsets in the future to entity B. Entity B will make an upfront non-refundable payment of C1 million to entity A and in return entity B will obtain the right to receive 10,000 carbon offsets annually from entity A for a period of 10 years starting from 1 January 20X5 (C10 per offset). Entity B will not receive any electricity as part of the long-term contract.

If Entity A is unable to generate sufficient carbon offsets (from project W or any of its other projects), entity A will need to purchase carbon offsets for delivery to entity B. There are no terms in the contract that permit entity A or entity B to settle the contract net in cash.

Assume that entity A readily has access to a liquid spot market for carbon offsets in which transactions take place with sufficient frequency and volume and prices are available on an ongoing basis.

Also assume that there are no clauses in the contract that cause any variation of any cash flows over the contract’s term. No further payments are required over the life of the contract as the carbon offsets are delivered.

Issue

Entity A should consider the guidance in Section 4.4 to determine the relevant accounting standards that apply to its contract with entity B.

Entity A determines that the contract does not provide entity B with control, joint control or significant influence over entity A or project W because entity A makes all of the decisions related to project W, and consent from entity B is not required.

Entity A determines that the contract does not result in the sale of an interest in any of Entity A’s assets, because it does not provide Entity B with an undivided interest in any of Entity A’s projects. As such, by entering into the contract to sell carbon offsets, Entity A has not sold an intangible asset.

Entity A determines that the contract does not contain a lease because it does not provide entity B with the right to receive substantially all of the outputs from any identified asset linked to any of entity A’s projects.

IFRS 9 applies to contracts to buy or sell a non-financial item where the contracts can be settled net in cash or another financial instrument or by exchanging financial instruments in accordance with paragraph 2.6 of IFRS 9 (net settleable contracts). Contracts to buy or sell carbon offsets could be examples of such contracts.

Some net settleable contracts will be outside the scope of IFRS 9 where the contract to purchase or sell the carbon offsets was entered into and continues to be for the entity’s expected purchase, sale or usage requirements in accordance with paragraph 2.4 of IFRS 9. This is commonly referred to as the ‘own-use’ exception.

Assume Entity A’s accounting policy is to apply ‘interpretation B’ referred to in FAQ 41.22.1 in the PwC Manual of Accounting.

Please refer to the examples below with differing assumptions that consider whether the contract is within the scope of IFRS 9 (to be read in conjunction with the background information above).

Example A