Key points

In August 2023, the IASB amended IAS 21 to add requirements to help entities to determine whether a currency is exchangeable into another currency, and the spot exchange rate to use when it is not. These new requirements will apply from 2025, with early application permitted.

What is the issue?

IAS 21 sets out the exchange rate that an entity uses when it reports foreign currency transactions in the functional currency or translates the results of a foreign operation in a different currency. Until now, IAS 21 set out the exchange rate to use when exchangeability between two currencies is temporarily lacking, but not what to do when lack of exchangeability is not temporary.

- assess exchangeability between two currencies; and

- determine the spot exchange rate, when exchangeability is lacking

What is the impact and for whom?

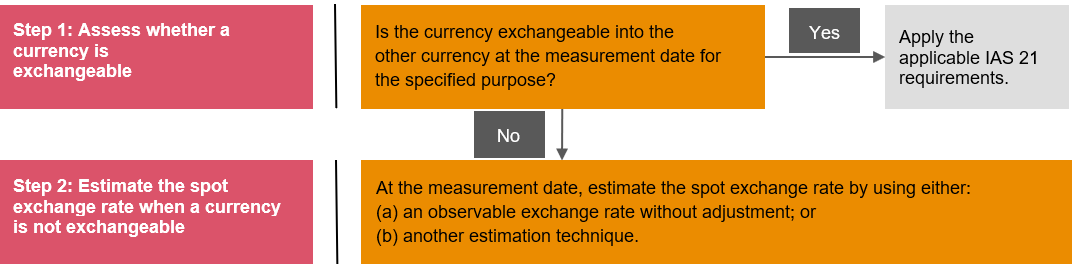

An entity is impacted by the amendments when it has a transaction or an operation in a foreign currency that is not exchangeable into another currency at a measurement date for a specified purpose. A currency is exchangeable when there is an ability to obtain the other currency (with a normal administrative delay), and the transaction would take place through a market or exchange mechanism that creates enforceable rights and obligations.

Assessing exchangeability between two currencies requires an analysis of different factors; such as the time frame for the exchange, the ability to obtain the other currency, markets or exchange mechanisms, the purpose of obtaining the other currency, and the ability to obtain only limited amounts of the other currency.

When a currency is not exchangeable into another currency, the spot exchange rate needs to be estimated. The objective in estimating the spot exchange rate at a measurement date is to determine the rate at which an orderly exchange transaction would take place at that date between market participants under prevailing economic conditions.

The amendments to IAS 21 do not provide detailed requirements on how to estimate the spot exchange rate. Instead, they set out a framework under which an entity can determine the spot exchange rate at the measurement date using:

- an observable exchange rate without adjustment, for example:

- a spot exchange rate for a purpose other than that for which an entity assesses exchangeability; or

- the first exchange rate at which an entity is able to obtain the other currency for the specified purpose after exchangeability of the currency is restored.

- another estimation technique, for example, that could be any observable exchange rate adjusted as necessary to meet the objective of the new requirements.

In developing these amendments, the IASB decided not to set a hierarchy of observable exchange rates to use in estimating a spot exchange rate. Whilst a hierarchy generally has a benefit of increasing consistency, in this case, it might have imposed additional costs without providing more useful information. The combination of a clear objective for the estimation, and a choice of what approach to take to make the estimation, allows entities to decide on a cost-effective approach considering their specific circumstances.

|

The following diagram was added to the amendments to help entities to assess the requirements:

The amendments include accompanying new disclosures to help investors to understand the effects, risks and estimated rates and techniques used when a currency is not exchangeable.

When does it apply?

The new requirements will be effective for annual reporting periods beginning on or after 1 January 2025, with earlier application permitted.

What are the transition requirements?

When an entity first applies the new requirements, it is not permitted to restate comparative information. Instead, the entity is required to translate the affected amounts at estimated spot exchange rates at the date of initial application, with an adjustment to retained earnings (if between foreign and functional currency) or to the reserve for cumulative translation differences (if between functional and presentation currency).

Where do I get more details?