Key points

The European Commission (EC) has issued 12 'near final' European Sustainability Reporting Standards (ESRS) for public feedback.

- The 12 'near final' ESRS specify the new sustainability reporting requirements based on the Corporate Sustainability Reporting Directive (CSRD), covering the full range of sustainability matters (environment, social and governance).

- The revised drafts contain significant changes compared to the November 2022 version prepared by EFRAG.

- There is a four-week feedback period, with a deadline of 7 July 2023. Interested stakeholders are encouraged to respond.

- The aim is for the final standards to be passed as law at the end of July 2023 and no later than the end of August 2023.

- The first companies within the scope of CSRD will have to apply ESRS for periods beginning on or after 1 January 2024.

- For further information, see below.

What is the issue?

Under the

Corporate Sustainability Reporting Directive (CSRD), which marks a new era of sustainability reporting in the EU, companies will soon have to report on a wide range of environmental, social and governance matters. The ESRS specify the detailed reporting requirements as set out by CSRD.

- a draft delegated act, through which the ESRS will become law in the EU;

- an Appendix I, containing the revised draft ESRS; and

- an Appendix II, containing a list of acronyms and a glossary of terms.

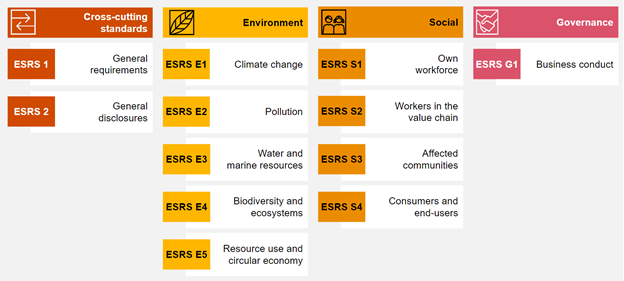

The 12 draft ESRS comprise include the following:

- two cross-cutting standards which apply to all sustainability matters; and

- ten topical standards covering a wide range of environmental, social and governance matters.

These are updates to the 12 previous

draft ESRS that were submitted by the European Financial Reporting Advisory Group (EFRAG) in November 2022.

Responses are due by 7 July 2023. Given that this is the final time that the standards will be available for feedback, stakeholders are encouraged to respond in order to help shape the final standards.

What is the impact?

The CSRD and the ESRS disclosure requirements are designed to bring sustainability reporting on a par with financial reporting over time. ESRS aim to provide a large panel of stakeholders with relevant, comparable and reliable information about a company’s sustainability-related impacts, risks and opportunities. Due to the tight ESRS adoption timeframe, with the first companies having to report using ESRS starting from FY 2024, companies need to set out to develop new systems, data-gathering processes, and controls necessary to comply with new reporting requirements.

How have the draft ESRS changed since the November 2022 submission by EFRAG?

The EC has assessed whether the draft ESRS submitted by EFRAG comply with CSRD and deliver on the EU’s policy objectives in the context of the European Green Deal. This assessment did not result in any changes to the overall structure, with the reporting structure of governance, strategy, impact, risk and opportunity management, and metrics and targets, and the broad scope of the environmental, social and governance topics covered.

However, the EC has made a number of changes with the aim of reducing the reporting burden and easing the first-time application of the standards.

View image

View image

- Materiality assessment

All standards, with the exception of ESRS 2, 'General disclosures', are subject to materiality assessment. Companies must determine which in terms of information (standard, disclosure requirement, or data point) are to be considered material on the basis of their materiality assessment. Previously, the EFRAG drafts had mandatory disclosures, independent of any materiality assessment, such as all climate-related disclosures in ESRS E1. These are no longer required if not material. Only the 'General disclosures' in ESRS 2 will be mandated.

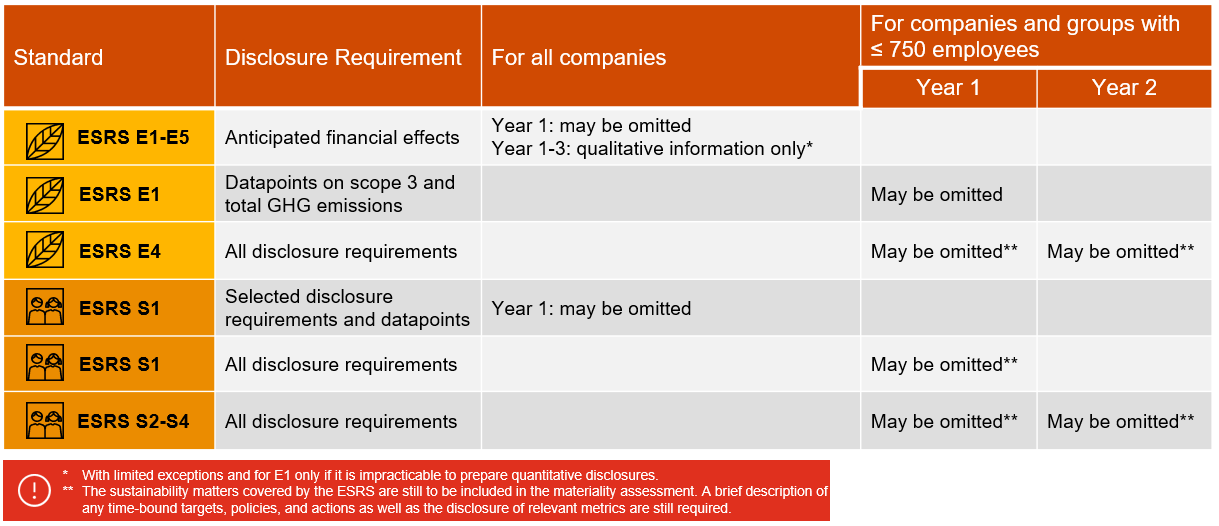

- Additional phase-in provisions

The EC has introduced additional phase-in provisions to those proposed by EFRAG, and it has further streamlined the phase-in provisions for reporting on anticipated financial effects;

- In their first reporting year, companies will be allowed to omit reporting on anticipated financial effects from all climate and other environment-related impacts, risks and opportunities.

- In addition, companies may limit their disclosures on anticipated financial effects to qualitative disclosures for the first three years of reporting (with limited exceptions and, in the case of climate-related financial effects only if it is impracticable to prepare quantitative disclosures).

- Furthermore, selected disclosure requirements and data points included in ESRS S1, 'Own workforce', related to social protection, employees with disabilities, health and safety, and work-life balance, can be omitted for the first reporting year.

- Special relief has been introduced for companies and groups not exceeding the average number of 750 employees:

- For the first reporting year, they may omit all of the ESRS S1, 'Own workforce' disclosure requirements and their scope 3 GHG emissions (data point of ESRS E1, 'Climate change').

- For the first two reporting years, they may omit reporting on biodiversity and ecosystems (ESRS E4), workers in the value chain (ESRS S2), affected communities (ESRS S3), and consumers and end-users (ESRS S4).

However, the sustainability matters covered by the ESRS mentioned above are still to be included in the materiality assessment. In addition, a brief description of any time-bound targets, policies and actions, as well as the disclosure of relevant metrics, are still required.

- Voluntary disclosures

Some disclosures are now voluntary. Examples include the transition plan for biodiversity and ecosystems (ESRS E4) and information on non-employee workers in ESRS S1 (for example, with respect to adequate wages, social protection, and health and safety). An explanation of why certain sustainability topics have been classified as not material is now also a voluntary disclosure.

- Flexibility in certain disclosures

One example is the change in wording from “potential financial effects” to “anticipated financial effects” arising from environment-related impacts, risks and opportunities. Furthermore, ESRS S1 now allows more flexibility with regards to the disclosure of key characteristics of employees by adjusting the threshold for country-specific disclosures from "countries with 50 or more employees" to "countries with 50 or more employees representing at least 10% of total employees". Disclosure requirements on the topics of corruption and bribery, as well as protection of whistleblowers (ESRS G1), have had their wording adjusted in order to avoid a conflict with the protection against self-incrimination.

With respect to interoperability with global standard-setting initiatives, the EC states that it has engaged closely with International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI) to ensure a high degree of interoperability with ESRS, and further modifications to the draft ESRS have been made in light of that engagement. Once the final ISSB standards have been released (likely to be for 26 June 2023), a detailed analysis of interoperability will have to be undertaken to identify the extent to which duplication in reporting is avoided.

When does it apply?

ESRS apply to all companies within the scope of CSRD. The first companies within the scope of CSRD will have to apply ESRS starting FY 2024 – that is, periods beginning on or after 1 January 2024 (reporting in 2025).

Where should the information be reported and should it be audited?

The sustainability statement prepared following the ESRS will be in a dedicated section of the management report. To enhance the reliability of reported information, CSRD has introduced an assurance obligation for sustainability information, including ESRS compliance. Initially, limited assurance will be required, with a planned transition to reasonable assurance in following years.

What are the next steps?

The feedback period of the 'near final' ESRS ends on 7 July 2023. Responses can be sent using the feedback template via the

European Commission website (free registration required).

The final ESRS will be passed as EU law through the adoption of a delegated act by the EC, making ESRS directly applicable to all companies that are subject to CSRD. This is expected by the end of July 2023 / beginning of August 2023. According to CSRD, the adoption of the delegated act will need to take place before the end of August 2023 in order for ESRS to be applicable for financial years beginning on or after 1 January 2024. The adoption is followed by a two-month (extendable to four months) scrutiny period by the European Parliament and the Council. If no objections are raised, ESRS will apply from 1 January 2024. If objections are raised, the standards cannot be changed, but the process for the first set of ESRS would need to start from scratch.

The standards provided are sector-agnostic standards. Additional sector-specific (that is, industry-focused) standards, ESRS specific to small and medium-sized enterprises (SMEs) and ESRS specific to non-EU companies will be released in phases over the next few years. In parallel, EFRAG is also working on developing guidance to support the application of sector-agnostic standards; this guidance is expected to cover the materiality assessment and the inclusion of value chain information. EFRAG has stated that its tentative plan is to issue deliverables in Summer 2023. In addition, the EC has announced that it will put in place an interpretation mechanism to provide formal interpretation of the standards.

Where do I get more details?

You can find more information on the recent sustainability reporting initiatives in the EU: