Search within this section

Select a section below and enter your search term, or to search all click IFRS In depths

Favorited Content

This publication was originally released in February 2021 as a Spotlight and has been updated in September 2021 to amend the Example for credit cards with insurance coverage in section 2.5. This has been further updated in November 2022, when it was converted to an In depth, to give more background in the introduction, to add the example on ‘Roadside assistance contracts’, to amend the sections ‘Financial guarantee and performance guarantee contracts’ and ‘3.4 Additional criteria to consider’, and to include the section ‘2.6 Separation of distinct goods and services from an insurance contract’.

|

Key points

Implementing IFRS 17 can be challenging and might require significant time and resources

|

|---|

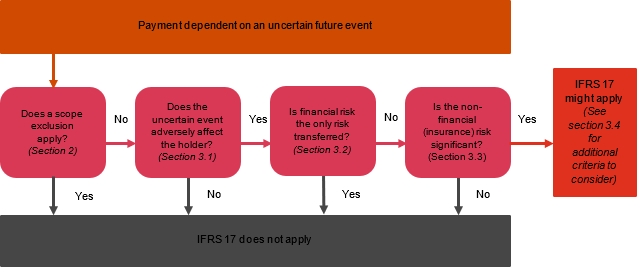

The effective date of IFRS 17 is imminent and identifying which contracts (including existing contracts at the transition date) meet the definition of insurance contracts and which of these fall within the scope of IFRS 17 (that is, those not eligible for a scope exception) can be challenging and might require significant time and resources to work through the implementation.

Where IFRS 17 applies to the insurance contracts, an entity might have to:

|

Example – Scope exclusion for warranty contracts

|

|---|

A consumer electronics company provides to its customers, at the time of the sale of its electronics products, a three-year free of charge warranty to cover repairs due to manufacturing defects. In addition, for a fixed price, the customer can purchase a further two-year extended warranty repair cover, which is offered through a warranty subsidiary of the manufacturing company.

Question 1: Is either of these two warranty products an insurance contract within the scope of IFRS 17 in the consolidated group’s financial statements?

No. From a group perspective, the electronic products, the three-year warranty, and the two-year extended warranty are provided by the same reporting entity. There will be insurance risk in the contract, because either the number of services to be performed or the nature of those services, or both, is uncertain. Both the warranty and the extended warranty contracts provide protection to the customer against an 'uncertain future event' and, assuming that the risk is significant, would meet the ‘insurance contract’ definition. However, since both types of warranty are available at the time of the sale, they will meet the scope exclusion for warranties provided by a manufacturer, dealer or retailer in connection with the sale of its goods or services to a customer.

Question 2: Would the answer change if the extended warranty contract is provided at a later date, and the terms of the original sale did not provide for the future purchase of the warranty at a fixed price?

Yes. If the extended warranty is provided at a later stage and not in conjunction with the sale (that is, the terms of the original sale did not provide for the future purchase of the warranty at a fixed price), it will not meet the scope exclusion in IFRS 17, because it is not 'in connection with the sale'. However, this product might meet the fixed-fee service contract criteria in section 2.2.

Question 3: Would the answer change at the level of the subsidiary providing the extended warranty services?

Yes. For the separate financial statements of the subsidiary that provides the extended warranty cover, the scope exclusion in paragraph 7(a) of IFRS 17 would not apply, because the repairs and maintenance are provided by a party other than the manufacturer, retailer, or dealer. The fixed-fee service contract criteria in section 2.2 would need to be considered at the subsidiary level.

|

Example – Optional scope exemption for fixed-fee contracts

|

|---|

When is a fixed-fee property maintenance contract an insurance contract within the scope of IFRS 17?

Entity P owns a portfolio of properties. It outsources its property maintenance and repair on all of these properties to entity S, a property management entity, for a five-year period for a fixed fee. This fee covers both property management and the cost of repair work. All repairs and maintenance required to maintain the properties to an agreed standard, based on the condition on inception of the contract, are now the responsibility of entity S. In entering into this contract, entity S made an assessment of the risks and likely repairs that would be required in respect of the specific portfolio of properties owned by entity P. This included normal wear and tear and certain other conditions (such as dry rot and damp, should they be discovered in the course of any remedial work). The price was fixed at the outset. Repairs required as a result of external events, such as fire or storm damage, continue to be covered by entity P’s property insurance arrangements with a regulated insurance entity.

Where either the number of services to be performed over a period or the nature of those services is not pre-determined, there can be significant insurance risk. There is uncertainty in the situation above in the following areas:

There is a specified uncertain event, because it is uncertain when or if any particular repair will be required and how much it might cost. The significance of the insurance risk for entity S is assessed, on a contract-by-contract basis, under IFRS 17. Insurance risk could be significant, even though there might be a minimal probability of material losses for entity S arising from all of its property management contracts, because a significant loss could arise on any one contract, such as the contract with entity P. If the insurance risk is significant, IFRS 17 will apply. Since entity S priced the contract based on an assessment of the risk associated with the customer’s (entity P’s) properties, this contract is not eligible for the fixed-fee contract scope exemption, and it is within the scope of IFRS 17.

|

Example – Roadside assistance contract

|

|---|

In developing IFRS 17, the IASB specifically considered the example of roadside assistance programmes in which the service provider agrees to repair specified equipment after a malfunction. Such contracts meet the definition of an insurance contract because:

In practice, a service provider might charge a fixed fee in the initial year in which case, the fixed-fee service exemption is available on the initial contract. However, on renewals, the service provider might consider the risks associated with an individual customer (for example, amount of assistance requested in the previous period) and might reflect the individual risk assessment in the renewal price. Therefore, the fixed-fee service exemption would not be available for the renewal contracts. For simplicity, the service provider can choose to account for all such contracts as insurance contracts from the outset of the contract rather than IFRS 15 for the initial contracts and IFRS 17 for the renewals. Further, when applying IFRS 17 to such contracts, the simpler premium allocation approach measurement model, which is somewhat aligned with IFRS 15 revenue recognition principles, might be available.

|

IFRS 9 might be easier than IFRS 17 to apply to loans with death waivers

|

|---|

The scope choice for loans with death waivers applies to contracts such as equity release mortgages (see section 3.2 for an example). Under IFRS 4, many entities account for these mortgages using IAS 39 principles (as allowed under IFRS 4), and so electing IFRS 9 on transition to IFRS 17 might be operationally less disruptive.

|

Potential impact on non-insurers

|

|---|

Entities that already apply IFRS 9 to financial guarantees issued are not impacted by IFRS 17. Under IFRS 9, an entity should initially recognise a financial guarantee when it becomes party to the contractual provisions and measure it at fair value. [IFRS 9 para 3.1.1]. [IFRS 9 para 5.1.1]. Subsequent measurement also follows the provisions of IFRS 9, which requires the financial liability recognised by the issuer to be reassessed at each reporting period and recorded at the higher of the loss allowance for expected credit losses and the initial fair value less any income recognised. The simplified approach for measuring expected credit losses is not available to financial guarantee contracts. Applying the expected credit loss requirements, including consideration of multiple scenarios and forward-looking information, could be complex where financial guarantees cover long periods of time.

However, in practice, many entities are already applying IFRS 4 and do not reflect financial guarantees issued on their balance sheets until a guarantee is triggered (that is, applying the IFRS 4 liability adequacy test consistent with IAS 37 principles).

On transition to IFRS 17 from IFRS 4, an entity applies the requirements in IFRS 17 for the first time and, consequently, it can choose to apply either IFRS 17 or IFRS 9 to such contracts. Given the complexities with IFRS 17 accounting, we expect that many non-insurers will choose to apply IFRS 9 instead. However, entities that are not already applying IFRS 9 to financial guarantees should be aware that significant work might be required to calculate the IFRS 9 liability in accordance with the three-stage model for expected credit losses. Either way, for issuers of financial guarantee contracts, which might include inter-company guarantees, this could be a significant change in accounting policy that would need to be applied retrospectively.

|

Example – Financial guarantee provided by a parent to a subsidiary’s banks

|

|---|

A shipping company (Company X) plans to acquire a new vessel and, in order to do so, needs to obtain external financing. It establishes two wholly owned subsidiaries:

Subsidiary B will issue a loan note to Bank Y and will pass the funds received on to Subsidiary A to enable that entity to acquire the vessel. Revenue earned by Subsidiary A is expected to provide it with sufficient cash flows to repay the interest and principal on the loan to Subsidiary B. Subsidiary B will use the interest income earned from Subsidiary A to repay its interest and principal on the loan note from Bank Y.

However, Bank Y is not willing to lend the money directly to either subsidiary A or B without a guarantee from Company X that they will step in and pay the interest and principal if various ‘events of default’ occur such as non-payment of interest due for more than 90 days.

The guarantee provided by Company X to Bank Y is a financial guarantee contract. Assuming that Company X has previously asserted that any financial guarantees issued are accounted for as insurance contracts under IFRS 4, in its stand-alone financial statements Company X should revisit its accounting policy choice when IFRS 17 becomes effective and elect to account for the financial guarantee in accordance with IFRS 9 or 17.

On a consolidated basis, such financial guarantees are not recognised as a separate contract but are part of the group’s liability to a third party (Bank Y) (see FAQ 40.75.8).

Bank Y is the holder of the financial guarantee contract, and the adoption of IFRS 17 will not impact its accounting for this loan note.

Subsidiary B might have benefited from a lower interest rate than it could have achieved without the existence of the parental guarantee, and it should consider an appropriate accounting policy to reflect this in its stand-alone financial statements. IFRS 9 and IFRS 17 do not address the accounting by the borrower in these situations; in practice, subsidiaries recognise the fair value of the guaranteed loan as noted in FAQ 42.92.2.

Note that, if Company X had simply provided a letter of comfort to Subsidiary B, rather than providing a formal guarantee to the bank, this would not be a financial guarantee contract (see FAQ 40.75.5).

|

Example – Development performance guarantee contract

|

|---|

A property developer (Company X) agrees to undertake a development and, in order to do so, establishes two wholly owned subsidiaries:

- Subsidiary A, the ‘Developer’; and

- Subsidiary B, the ‘Guarantor’.

Several agreements have been entered into for the development, including where Subsidiary B will guarantee Subsidiary A’s performance to Company X. Under this agreement, if Subsidiary A defaults (that is, fails to perform under the development contract), Subsidiary B must procure the performance of the relevant obligation through another developer and/or pay financial compensation to the customer.

In Company X’s consolidated financial statements, payments under the performance guarantee can be viewed as penalties and liquidated damages payable to the customer for failure to comply with the terms of the contract. Such amounts are generally accounted for as variable consideration under IFRS 15. This is discussed further in EX 11.77.1.

However, in Subsidiary B’s stand-alone financial statements, the performance guarantee meets the definition of an insurance contract and needs to be accounted for under IFRS 17.

|

Example – Credit card with insurance coverage

|

|---|

A bank issues a credit card (or other similar contract) to a customer. Under the credit card contract, a customer is protected against the purchase of goods or services that are faulty or not delivered to the customer as well as fraud protection for the cardholder against the misuse of the card. In addition, the customer is protected against any additional costs incurred related to the purchase (which could be higher than just merely refunding the purchase price). The bank does not charge any fees to the cardholder that reflects an assessment of the cardholder’s individual risk associated with the protection provided.

The scope exclusions in IFRS 9 have been amended for financial instruments arising under credit card contracts, or similar contracts that provide credit or payment arrangements (effective 1 January 2023).

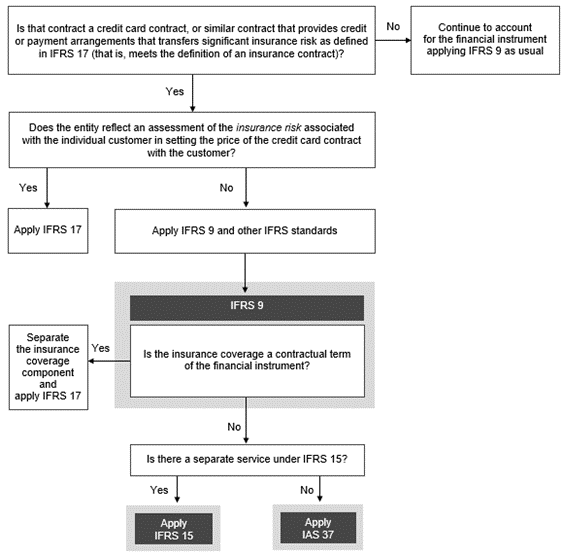

Does the bank apply IFRS 17 to the contract with the cardholder?

The bank will need to assess whether the contract is an insurance contract as defined in IFRS 17. Both the faulty goods or services / failure to deliver goods or services and potential fraud are uncertain future events which adversely affect the cardholder. In addition, the customer is protected against any additional costs incurred related to the purchase (which could be higher than just merely refunding the purchase price). The risk transferred to the bank is an insurance risk. If there is significant insurance risk as defined in IFRS 17, the contract meets the definition of an insurance contract in IFRS 17.

The following diagram sets out the typical questions that the bank will need to consider in determining the accounting for credit card contracts, or similar contracts that provide credit or payment arrangements:

The following paragraphs analyse each of these questions for the specific fact pattern included in the question.

Does the bank reflect an assessment of the insurance risk associated with the individual customer in setting the price of the credit card contract with the customer?

The bank will need to consider the IFRS 17 scope exclusion relating to credit card contracts that meet the definition of an insurance contract. This example meets the criteria for the scope exclusion, because the bank does not charge any fees to the cardholder that reflect an assessment of the cardholder’s individual risk.

Is the insurance coverage a contractual term of the financial instrument?

Applying IFRS 9, the bank will need to determine whether the insurance coverage is a contractual term of the financial instrument. The interpretation of ‘contractual term’ should be consistent with IFRS 9 (since the contract is within the scope of IFRS 9). In particular the interpretation should be consistent with that applied in interpreting paragraph B4.1.13 of IFRS 9 that clarifies that, where payments arise only as a result of legislation that gives the regulatory authority power to impose changes to an instrument, they should be disregarded when assessing the SPPI criterion, because that power is not part of the contractual terms of a financial instrument. Instrument E in paragraph B4.1.13 of IFRS 9 specifically refers to bail-in instruments as an example that might meet the SPPI criterion.

A clause should not be taken into account, when assessing the SPPI criterion, where the clause merely acknowledges the existence of legislation (that is, the clause does not create additional rights or obligations that would not have existed in the absence of such a clause). Applying that conclusion to insurance coverage, the insurance coverage clause should not be considered to be part of ‘contractual terms of such a financial instrument’ where the clause merely acknowledges the existence of the insurance coverage legislation. For this to be the case, it is necessary for:

In some situations, it might be appropriate to obtain legal advice to determine whether or not the contractual terms included create additional rights or obligations that would not have existed in the absence of such a clause.

If the bank concludes that the insurance coverage is a contractual term of the financial instrument, IFRS 9 requires the insurance coverage component to be separated from the contract and accounted for under IFRS 17. [IFRS 17 para 7(h)]. [IFRS 9 para 2.1(e)(iv)].

However, if the insurance coverage is not a contractual term of the financial instrument, it will not be within the scope of IFRS 9, and the bank will need to consider other applicable IFRS standards as discussed below.

Is there a separate service under IFRS 15?

In paragraph BC94C of the Basis for Conclusions on IFRS 17, the IASB noted that other IFRS standards, such as IFRS 15 or IAS 37, might apply to other components of the contract, such as other service components or insurance components required by law or regulation.

Under IFRS 15, promises in a contract can be explicit, or implicit if they create a valid expectation that the entity will provide a good or service based on the entity’s customary business practices, published policies or specific statements. [IFRS 15 para 24]. Warranties might be written in the contract, or they might be implicit as a result of either customary business practices or legal requirements. The bank will need to assess whether the insurance coverage for faulty goods or services / failure to deliver goods or services and fraud are separate performance obligations to be accounted for under IFRS 15. This assessment requires judgement; however, we think that generally:

As a result, where the insurance coverage for fraud and for faulty goods or services / failure to deliver goods or services is not part of the contractual terms of the financial instrument, the insurance coverage will generally be accounted for under IAS 37. [IFRS 15 App B para B30].

|

Example – Weather derivatives

|

|---|

An entity has a contract under which it will receive payments if rainfall is below average during monsoon months. Could this be an insurance contract?

No. Contracts that require a payment based only on climatic variables (sometimes described as ‘weather derivatives’), or on other geological or other physical variables, are not insurance contracts, even if the policyholder uses the contract to mitigate an underlying risk exposure. Such contracts do not require an adverse effect on the policyholder as a precondition of payment, and the risk transferred arises from a non-financial variable that is not specific to either party to the contract. Examples of contracts based on climatic variables that are not insurance contracts include a weather derivative that is triggered by its 'underlying' and pays even if the holder has not suffered any damage from the weather (for example, a contract under which an entity will receive payments if rainfall is below average during the monsoon months).

In contrast, if the contract was based on a climatic variable that is specific to a party to the contract (for example, reduced crop yields from land that is owned and farmed by the holder of the contract as a result of below-average rainfall in the region during the monsoon months), the contract might be within the scope of IFRS 17, and the issuer should proceed as in section 3.2 below.

|

Example – Savings plan with cash prizes

|

|---|

An entity issues a contract whereby the customer pays monthly deposits of CU100 under a 60-month saving plan, with a guaranteed annual interest of approximately 6% (equivalent to market rates applicable to saving accounts or other inflation index). Interest is only accrued for those monthly deposits which are not withdrawn after the first 12 months of the plan. These plans are sometimes referred to as 'capitalisation plans'.

Customers are entered, during the term of the plan, into monthly lotteries that award a cash prize equivalent to 1,000 times the amount of the last deposit made (that is, cash prize equals CU100,000). Each customer receives a certificate with a numerical identification that might coincide with the winning numbers from the National Lottery. Every month, there will be one winner amongst all participants in the plan.

The deposits are redeemable in full, plus interest, only after one year. If the customer redeems the monthly deposits before one year, it will be subject to a surrender penalty. Surrender penalties are applied during the whole term of the contract, and they vary from 90% at inception of the contract to 0% after the 60 months, in order to encourage customers to keep their funds with the entity for a longer period of time.

At the inception of the contract, all customers nominate a beneficiary that will receive the prize or the accumulated surrender value of the deposits in the event of the customer’s death.

Is the saving plan, with rights to receive cash awards based on lottery-type draws, an insurance contract under IFRS 17?

No, this is not an insurance contract, as defined in Appendix A to IFRS 17. Although it is clear that there is a substantial benefit to be paid to a customer who wins the monthly lottery, the fact that the customer has the winning lottery numbers does not qualify as an insured event, because the event does not affect the customer adversely. This is a gambling contract.

|

If a contract does not transfer insurance risk, it might be a derivative

|

|---|

The definition of financial risk above is consistent with part of the definition of a derivative in IFRS 9. If a contract does not meet the definition of an insurance contract in IFRS 17 because it transfers financial risk rather than insurance risk, it might contain a derivative within the scope of IFRS 9. In some cases, it will not be a derivative either (for example, if there is a significant initial net investment), but this should be considered further.

|

Example – Embedded EBITDA guarantee

|

|---|

An entity agrees to provide hotel management services to the owner of a hotel for 20 years, in return for a variable fee determined as a percentage of gross hotel revenue. In addition, the contract contains an embedded guarantee that guarantees the hotel owner a specified level of earnings before interest, tax depreciation and amortisation (‘EBITDA’). To the extent that actual EBITDA is below 85% of projected EBITDA, the service provider is obligated to make payments to the owner of the hotel to cover the shortfall.

There are no limitations relating to the events that might give rise to an eligible EBITDA shortfall other than material disruption to business (such as force majeure, or refurbishment). Accordingly, the service provider is exposed to risks other than its own poor performance – for example, an over-supply of hotel accommodation in that location and other general market risks. Furthermore, the amount payable under the guarantee might exceed the amount of the revenue-based fee receivable, such that the service provider might be required to make a net payment to the hotel owner.

The embedded EBITDA guarantee compensates the hotel owner if EBITDA is lower than expected, which is an uncertain event that adversely affects the hotel owner; also, it is not a financial risk, because it is specific to the hotel owner. The transferred risk is therefore insurance risk. However, not all EBITDA guarantees are necessarily in scope of IFRS 17, because they are only in scope if the insurance risk transferred is significant (see section 3.3 below). If IFRS 17 applies the entity should also consider whether the hotel management service can be separated from the insurance component of the contract as a distinct service and accounted for under IFRS 15 as set out in section 2.6 above.

If the insurance risk transferred is not significant, the EBITDA guarantee in the contract might represent variable consideration to be accounted for under IFRS 15.

|

Example – Equity release mortgage

|

|---|

An entity issues an equity release mortgage (also commonly referred to as a ‘lifetime’ or ‘reverse’ mortgage) with a ‘no negative equity’ guarantee. The contractual terms secure the mortgage against the borrower’s property. Interest is accrued. Principal and accrued interest are payable when the borrower dies or moves into long-term care. The property is then sold, and the proceeds are used to repay the mortgage balance (including any accrued interest). The entity is not entitled to any excess of the sales proceeds over the amount due, but it bears any shortfall where the sales proceeds are not sufficient to repay the principal and accrued interest. Assume that the entity holds the equity release mortgage within a ‘hold to collect’ business model, and that the contract contains no other features that could cause it to fail the SPPI test in IFRS 9.

Does the contract transfer insurance risk?

Yes. The contract exposes the entity, amongst other risks, to the risk of changes in fair value of the borrower’s property (a non-financial asset). That is not a financial risk, because the fair value of the property reflects not only changes in market prices for properties in general (a financial variable) but also the physical condition of the specific asset (a non-financial variable). The contract therefore transfers insurance risk, as well as financial risk, from the borrower to the entity.

This contract might meet the optional scope exclusion explained in section 2.3, because the maximum shortfall is the mortgage balance (that is, the benefit to the borrower is limited to the amount otherwise required to settle their obligation). If the entity does not elect to apply IFRS 9, the contract might be within the scope of IFRS 17 and the entity should proceed as in section 3.3 below.

|

Example – Unlikely scenario

|

|---|

An entity has a contract which requires an insurer to reimburse it for the value of a property that it owns in the event of the property being destroyed by a hurricane. The likelihood of a hurricane destroying a building is low (although the scenario has commercial substance), but the payment by the insurer would be substantial. In all other scenarios, a similar payment would not be made. The contract therefore contains significant insurance risk.

|

Liabilities might be recognised earlier under IFRS 17 than under some other accounting standards

|

|---|

A liability might be recognised under IFRS 17, even if the adverse event is very unlikely. This might result in liabilities being recognised sooner than would be the case applying IAS 37. Where the entity does not have a class of similar items, under IAS 37 it might only recognise a liability when an outflow is probable.

|

Example – Is the policyholder’s loss insignificant?

|

|---|

A contract requires the issuer to pay CU1 million to the holder if an asset suffers physical damage causing an insignificant economic loss of CU1 to the holder. The holder transfers to the insurer only the insignificant loss of losing CU1. In addition, the requirement in the contract for the issuer also to pay CU999,999 if the physical damage occurs creates non-insurance risk. Because the issuer does not accept significant insurance risk from the holder, this contract is not an insurance contract.

|

Criteria

|

Explanation

|

|---|---|

Does a contract exist under IFRS 17?

|

A contract is an agreement between two or more parties that creates enforceable rights and obligations. Contracts can be written, oral or implied by customary business practices. Contractual terms can be either explicit or implicit, including those terms that are imposed by law or regulation. An entity should consider its substantive rights and obligations arising from a contract, law or regulation.

|

Is the transferred risk a pre-existing risk?

|

Insurance risk must be a pre-existing risk that is transferred from the policyholder to the entity as a result of the contract, and it must not be a new risk created by the contract.

For example, an entity leases a car to a customer, and the lessor provides optional insurance coverage to the customer for damage to third-party vehicles caused by the customer driving the leased car.

The transferred risk relates to damage caused by the customer driving the car, which is not a risk created by the insurance contract, and so it will meet the definition of insurance risk.

|

Is the transferred risk from a third party?

|

Entities must accept risk from another party (a separate entity) in order for insurance risk to exist. This is considered further in the example below of a captive insurance entity within a group.

|

Are there any new disclosures?

|

IFRS 17 retains most of the existing IFRS 4 disclosures but also expands these further and introduces a number of new disclosure requirements, including transitional disclosures. Entities should not underestimate the extent of work required to comply with these requirements, even if eligible for the simplified premium allocation approach. Appendix A to our Illustrative IFRS 17 financial statements provides a comprehensive outline of these IFRS 17 disclosure requirements.

|

Example – captive insurance entity within a group

|

|---|

Self-insurance through a captive insurance subsidiary

If a non-insurance group self-insures through a captive insurance subsidiary, this arrangement falls outside the scope of IFRS 17 in the group’s consolidated financial statements. A non-insurance group can self-insure, using a captive insurance subsidiary to give insurance cover to all of the members of the group for risks to which those group members are exposed through their business activities. This allows the captive insurer to pool the risks of the members of the group. The pooled risk might mean that the captive can insure (or reinsure) the pooled risks more cheaply with an insurer (or reinsurer) external to the group.

However, if the captive insurance subsidiary presents separate IFRS financial statements and assumes significant insurance risks under the contracts with the other members of the group, it treats those as insurance contracts under IFRS 17. The transactions between the captive and the other members of the group are eliminated on consolidation, as are all other intra-group transactions. If the captive holds a reinsurance contract with a third party reinsurer, in the consolidated financial statements of the group, this ‘reinsurance contract’ would be treated as an insurance contract held from the group’s perspective. Because the group does not issue an insurance contract, IFRS 17 does not apply to this contract in the group’s consolidated financial statements.

Entities in the group that are insured by the captive should, in their stand-alone financial statements, record any provisions that might arise from their activities (such as product recall, workers’ compensation and general liability) gross of any amounts that might be recoverable from the captive. The existence of a captive in the group structure and/or the purchase of commercial insurance from a third party might result in a separate asset being recorded if reimbursement is virtually certain, but this does not reduce the related liabilities themselves in the individual entities.

Self-insurance through a captive insurance associate/joint venture

In some group structures, a non-insurance group might self-insure by pooling its risks with other unrelated groups such that the captive meets the definition of an associate or joint venture under IFRS. The captive itself might not be reporting under IFRS. However, the group reflects its interest in the captive in its consolidated financial statements applying the IAS 28 equity method of accounting as follows:

Other more complex captive structures

Certain captive structures are more complex, and the accounting at both the group and captive level might require significant analysis and judgement. For example, due to regulatory requirements, the risks might be ‘fronted’, such that the group might purchase insurance coverage from an unrelated commercial insurer who, in turn, enters into a reinsurance contract with the group’s captive insurer. This is discussed further in FAQ 50A.30.2.

|

© #year# PricewaterhouseCoopers LLP. This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under licence.

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PwC. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

Select a section below and enter your search term, or to search all click IFRS In depths