A sale and leaseback is a transaction in which the owner of an asset sells the asset and leases that asset back from the buyer for a period of time. The seller-lessee must determine if the transaction qualifies as a sale for which a gain (or loss) is recognised, or if the transaction is treated as a collateralised borrowing.

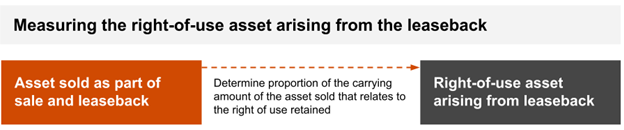

The accounting for sale and leaseback transactions under IFRS 16, ‘Leases’, depends on whether the transfer of the asset qualifies as a sale in accordance with IFRS 15, ‘Revenue from contracts with customers’. A sale and leaseback qualifies as a sale if the buyer-lessor obtains control of the underlying asset. Where the transfer of the asset qualifies as a sale, the seller-lessee also recognises the leaseback by recognising a lease liability, reflecting the payment terms of the leaseback and a right-of-use asset for the right of use retained. The seller-lessee recognises only the amount of any gain or loss that relates to the rights transferred to the buyer-lessor.

In March 2020, the IFRS Interpretations Committee (IFRS IC) discussed a submission about a sale and leaseback transaction with variable payments that do not depend on an index or a rate. The submitter asked how the seller-lessee measures the right-of-use asset arising from the leaseback and, thus, determines any gain or loss recognised at the date of the transaction. For example, if all of the lease payments in the leaseback depend on the future sales of the seller-lessee (that is, they are fully variable payments), the submitter questioned if it would be acceptable for the lessee to measure the right-of-use asset and lease liability at zero and, therefore, recognise a full gain or loss on the sale at the date of the transaction.

In June 2020, in response to the submission, the IFRS IC issued an

agenda decision addressing how a seller-lessee should measure the right-of-use asset arising from such a leaseback with variable lease payments. The agenda decision notes that, because the right of use that the seller-lessee retains is measured as a proportion of the previous carrying amount of the property, plant and equipment (PP&E), the amount of the gain or loss recognised must relate only to the rights transferred to the buyer-lessor. In other words, it would not be acceptable for the seller-lessee to recognise a full gain or loss at the date of the sale and leaseback transaction.

IFRS 16 requires a seller-lessee to account for a right-of-use asset arising from a sale and leaseback in this manner to reflect that, from an economic standpoint, the seller-lessee has sold only its interest in the value of the underlying asset at the end of the leaseback – it has retained its right to use the asset for the duration of the leaseback. The seller-lessee had already obtained that right to use the asset at the time when it purchased the asset, since the right of use is an embedded part of the rights that an entity obtains when it purchases, for example, an item of PP&E. Recognising only the amount of the gain or loss that relates to the rights transferred to the buyer-lessor – and thus not recognising the amount of the gain or loss that relates to the rights retained by the seller-lessee – appropriately reflects the economics of a sale and leaseback transaction.

The IFRS IC concluded that IFRS 16 provides an adequate basis for an entity to determine, at the date of the transaction, the accounting for the sale and leaseback transaction submitted. However, the IFRS IC’s discussions highlighted the improvements that could be made to IFRS 16 by adding subsequent measurement requirements for sale and leaseback transactions.

When originally issued, IFRS 16 included no specific subsequent measurement requirements for sale and leaseback transactions. Consequently, it was not always clear how to subsequently measure the liability arising from a leaseback, particularly where the payments for the lease include payments that do not meet the definition of ‘lease payments’ in IFRS 16 – for example, where the payments include variable lease payments that do not depend on an index or a rate. As a result, in September 2022, the IASB issued

Lease Liability in a Sale and Leaseback, which amends IFRS 16 to address the issue of subsequent measurement of the lease liability.