Overall architecture and interaction of standards

There are two cross-cutting standards:

- ESRS 1 General requirements providing general guidance on the conceptual requirements of the CSRD and laying a foundation of general reporting principles.

- ESRS 2 General disclosures providing DRs on general reporting issues, governance, strategy and business model and the double materiality assessment process of sustainability impacts, risks and opportunities.

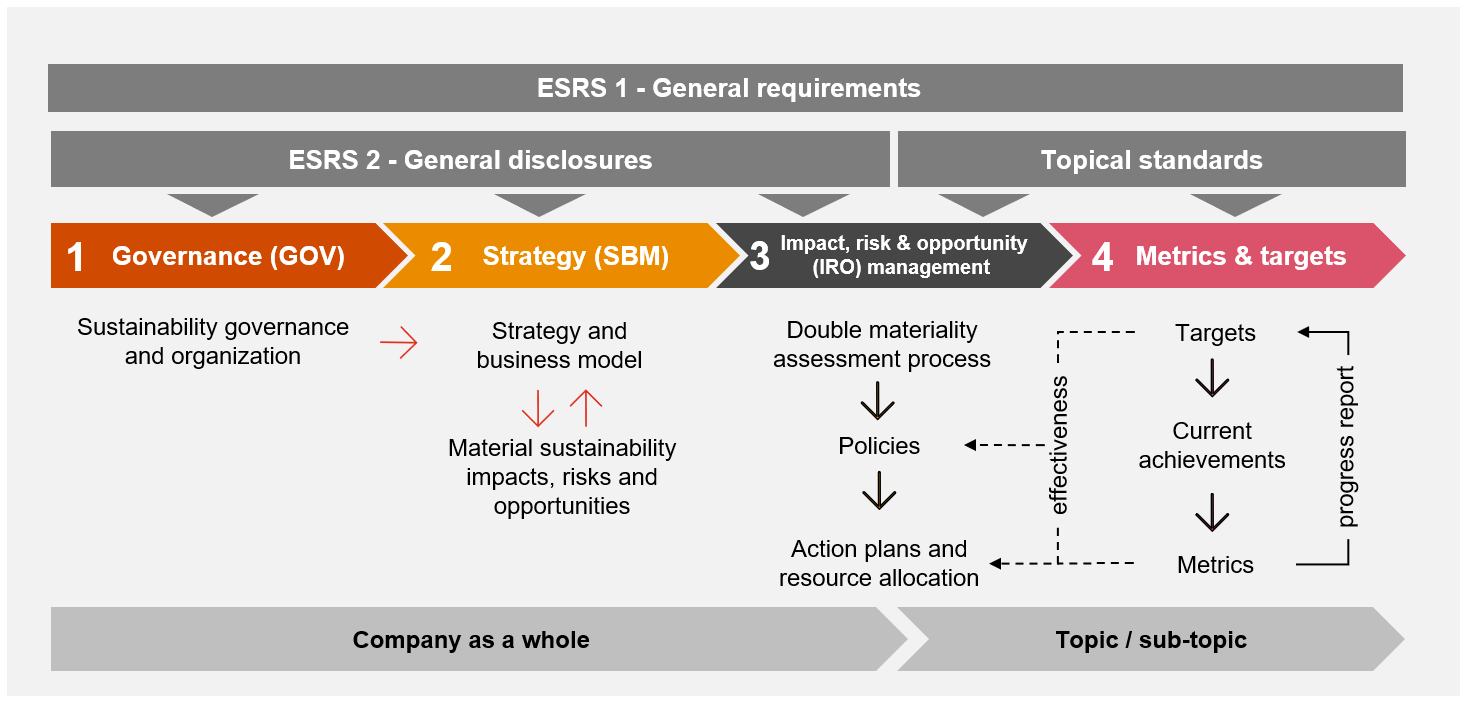

The two cross-cutting standards define the basic architecture of future sustainability reporting, general reporting principles and transversal disclosures. They apply to all companies across all sustainability matters and interact with the topical standards for the Environment, Social and Governance (ESG) (see illustration below).

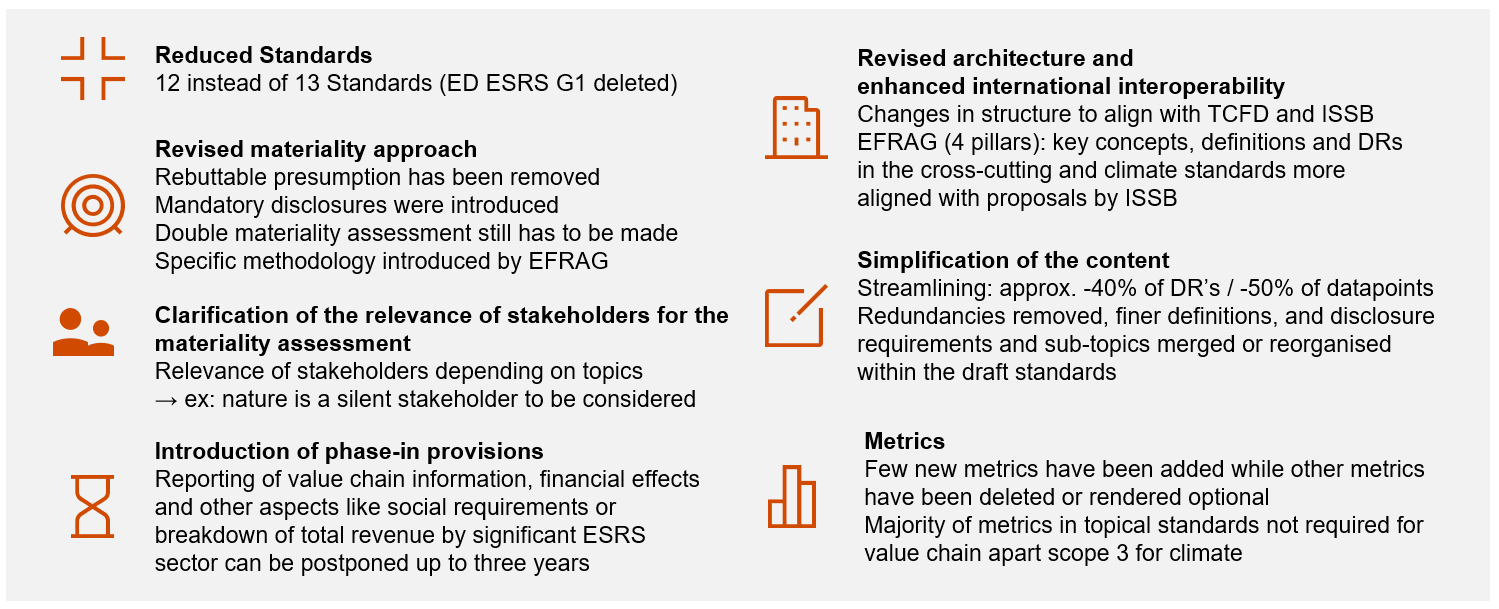

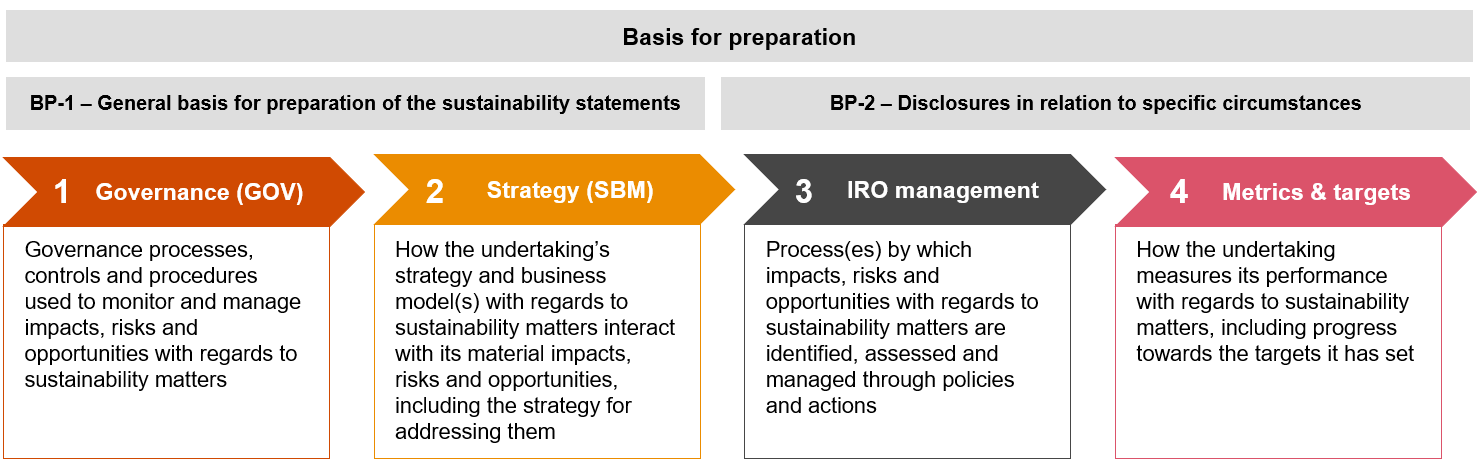

The previous three pillar structure of the ESRS EDs has been replaced by a new four pillar structure to enhance international interoperability: Governance, Strategy, Impact, risk and opportunity (IRO) management, and Metrics and targets. This is similar to the architecture of the TCFD and ISSB. All topical standards have been changed to mirror the new four pillar structure.

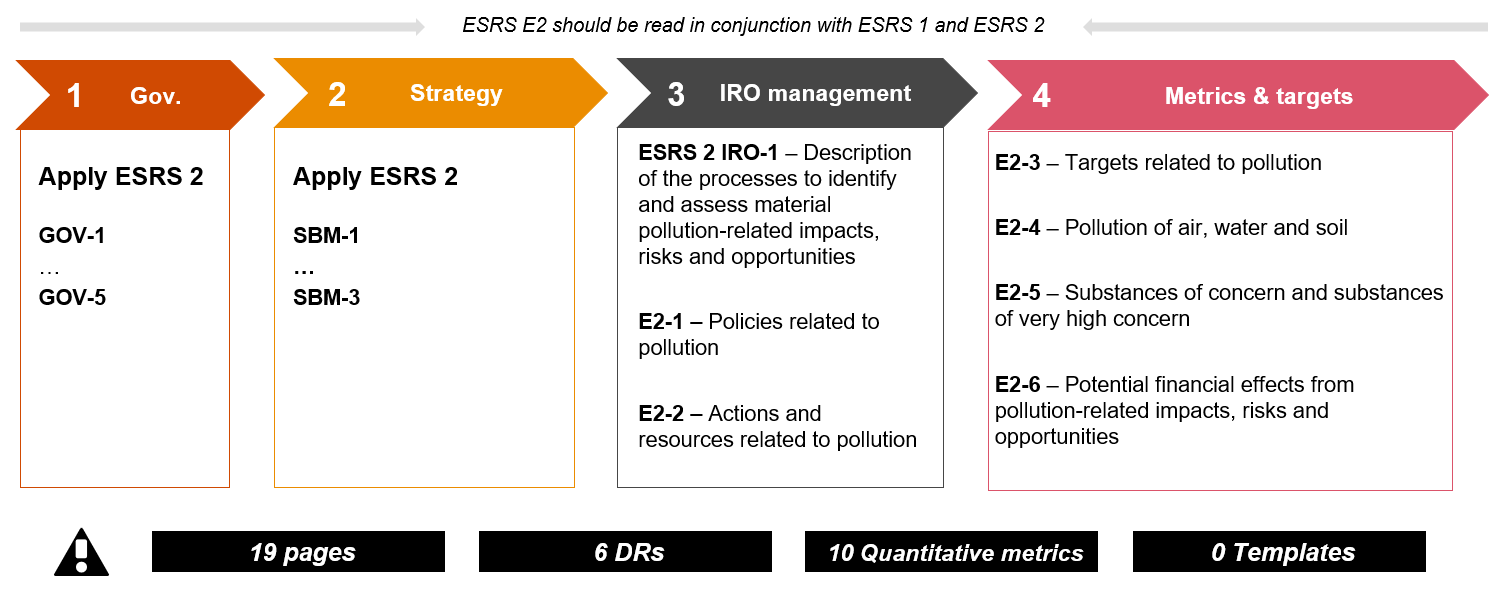

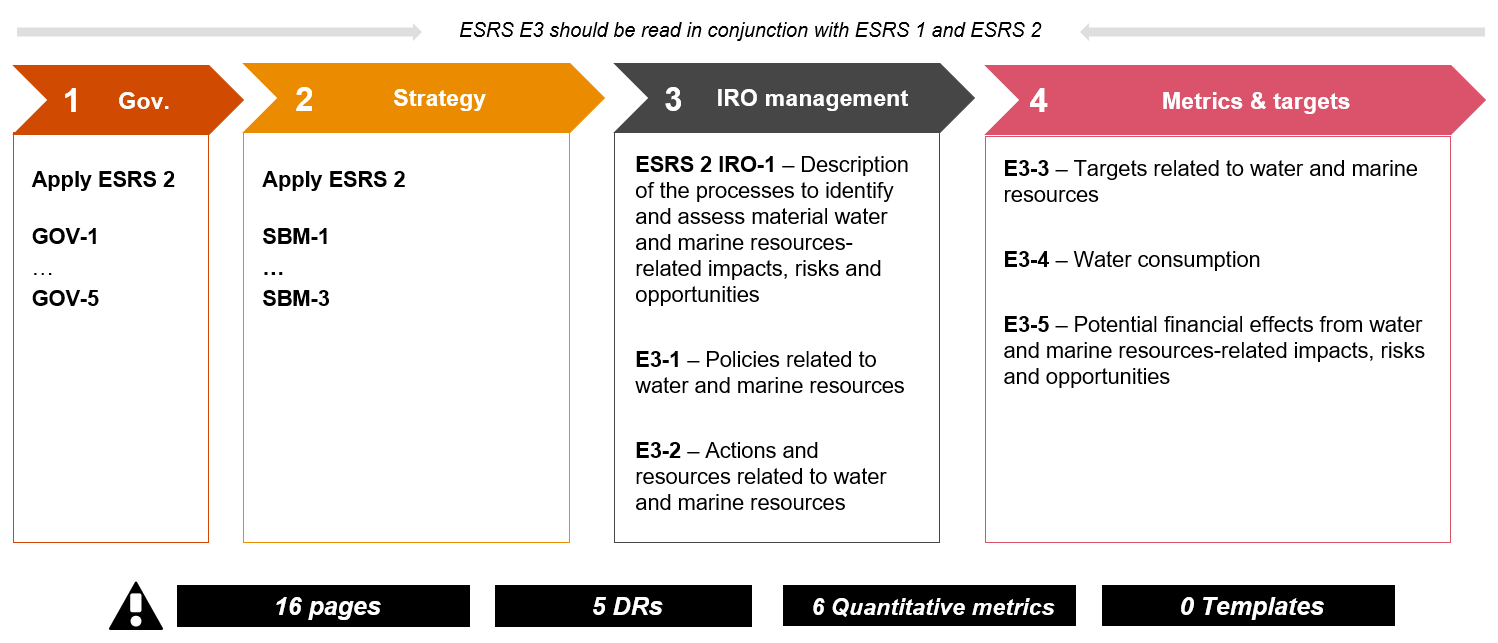

The first three reporting pillars ‘Governance’, ‘Strategy’ and ‘Impact, risk & opportunity (IRO) management’ are covered by ESRS 2 General disclosures. These should be assessed for the company as a whole. Each topical standard covers the policies and actions in the third reporting pillar 'Impact, risk & opportunity (IRO) management' and fourth reporting pillar 'Metrics & targets' on a topic/subtopic level. In addition, the topical standards refer back to ESRS 2 by providing additional focused DRs for the first three reporting pillars from a topical standpoint.

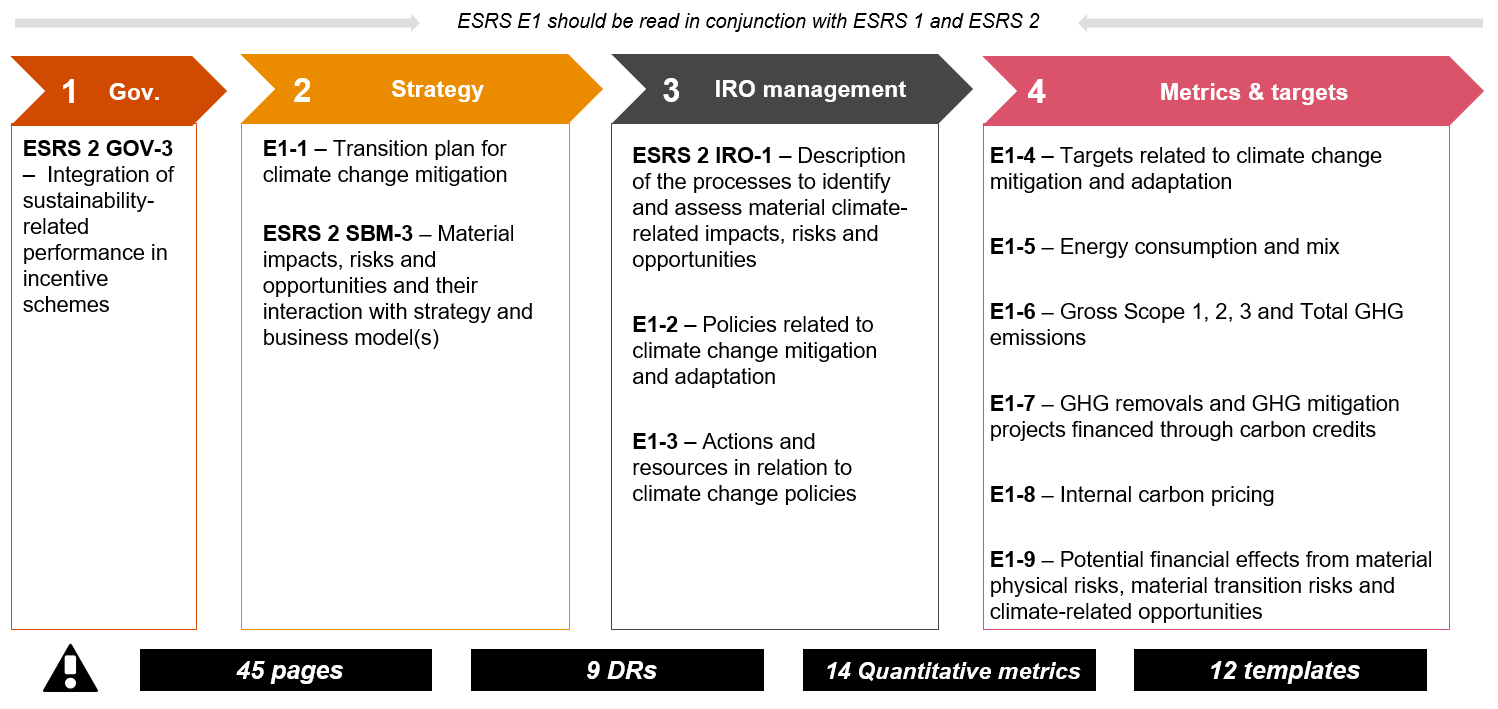

For example, ESRS E1 contains a topic-specific DR related to ESRS 2 and the Governance pillar (ESRS 2 GOV-3) requires the company to disclose whether the performance in incentive schemes of members of the administrative, management and supervisory bodies has been assessed against the GHG emission reduction targets.

ESRS 1 General requirements

ESRS 1 contains no DRs and sets out the general requirements that companies shall comply with when preparing and presenting sustainability- related information under the CSRD. This includes generally accepted reporting principles such as presenting comparative information, estimating under conditions of uncertainty and reporting errors in prior periods. Furthermore, ESRS 1 provides guidance on the application of the fundamental concepts of the CSRD like double materiality, reporting boundaries and value chain, as well as on the transitional provisions. Below are selected aspects in more depth.

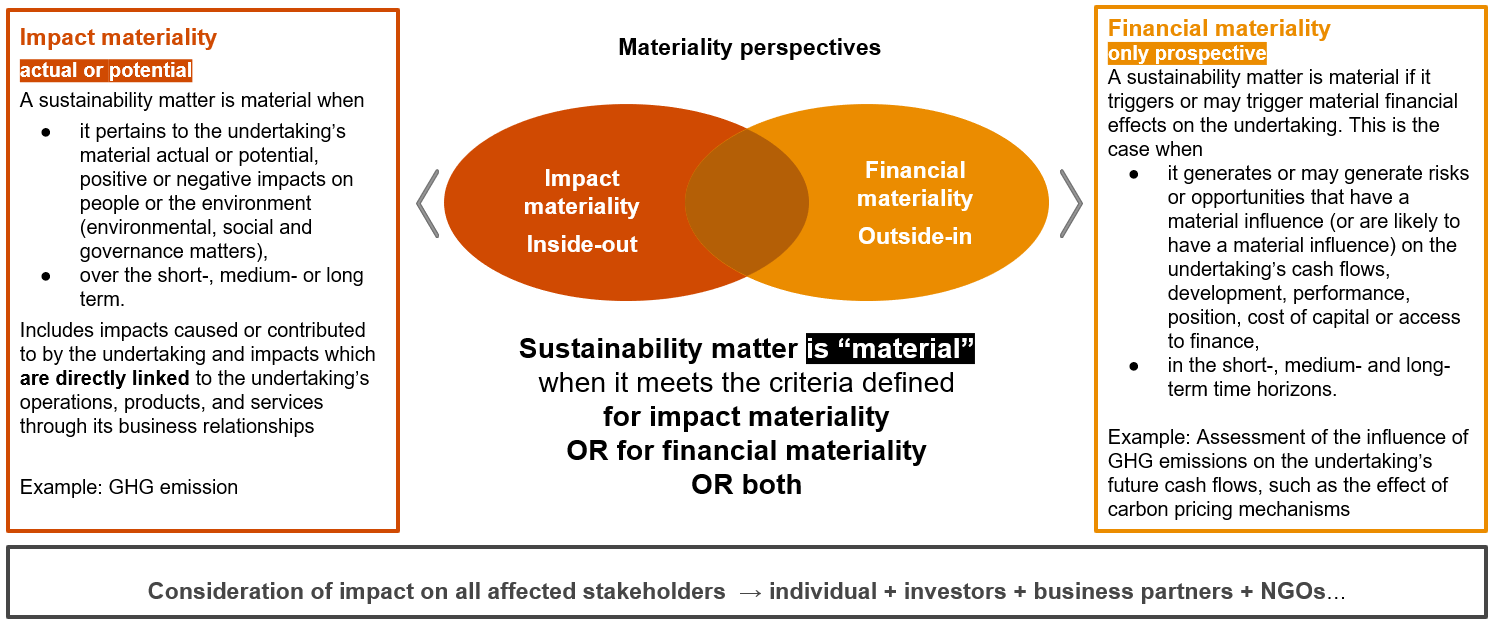

Double materiality

The central CSRD concept is double materiality. This remains unchanged compared to the ESRS EDs. A sustainability matter is considered ‘material’ when it meets the criteria defined for impact materiality or for financial materiality or both, as illustrated below.

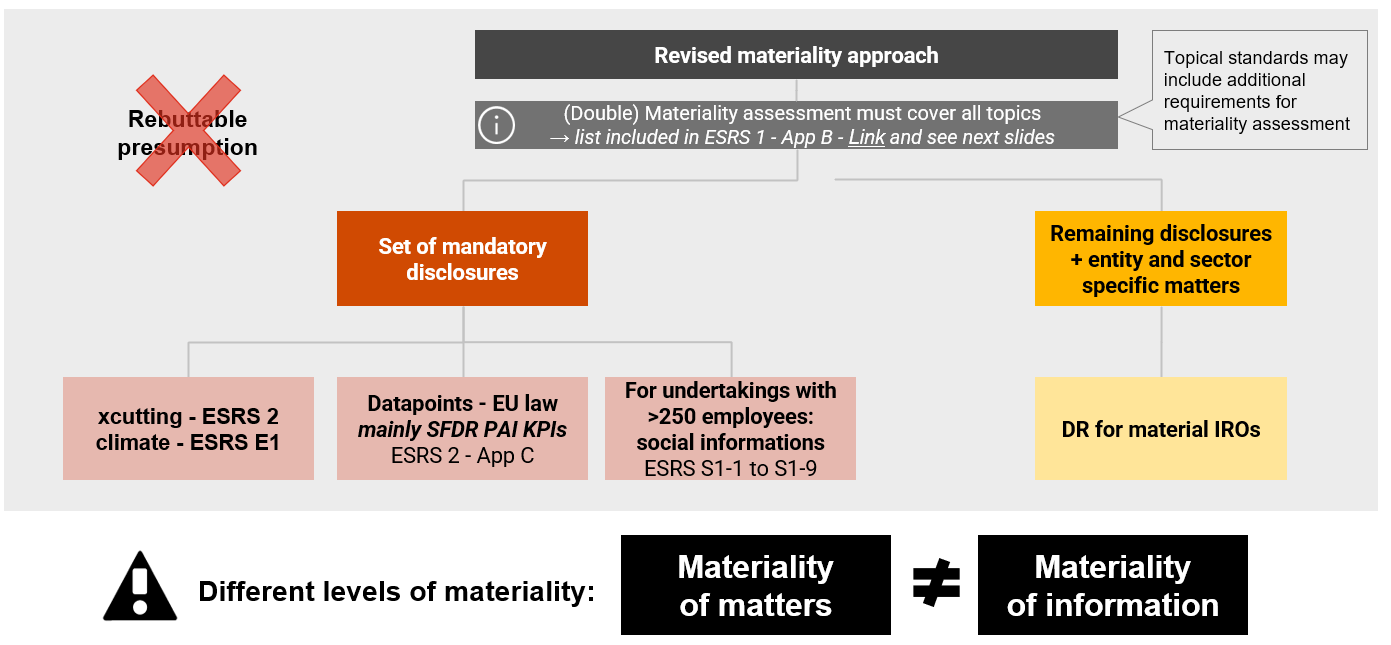

Revised materiality approach

The ‘rebuttable presumption’ has been removed compared to the ESRS EDs. This is when all DRs are presumed material unless the company has reasonable and supportable evidence to rebut this.

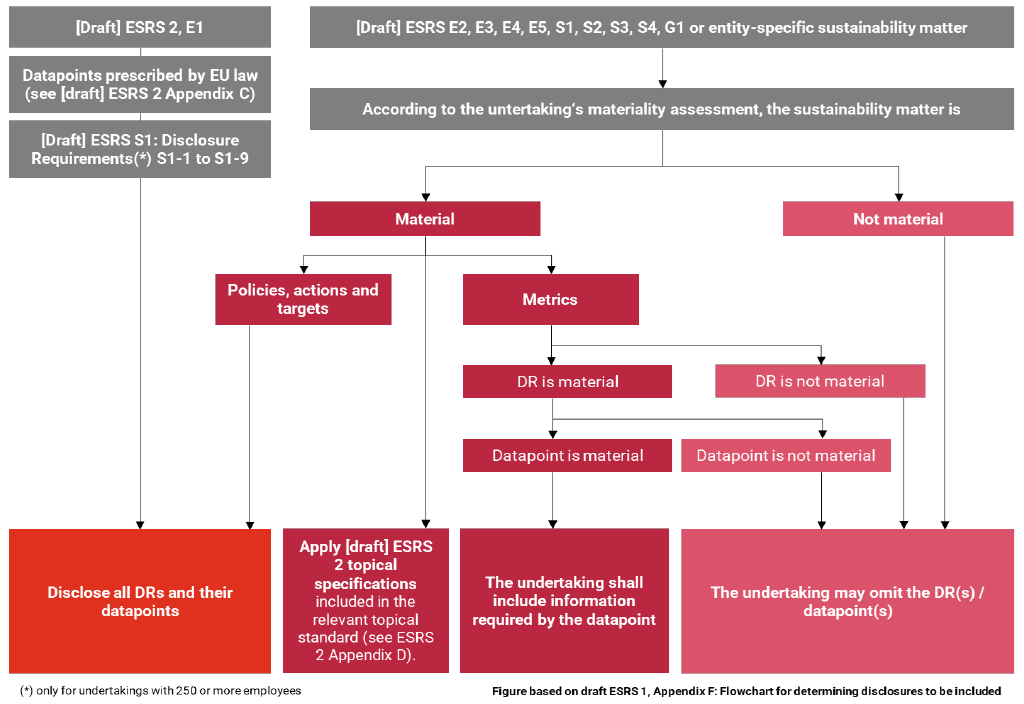

A materiality assessment must still be prepared but with a reduced scope since mandatory disclosures have been introduced. The mandatory disclosures that are to be reported irrespective of the outcome of the materiality assessment encompass:

- The entire cross-cutting standard ESRS 2 General disclosures and the entire topical standard ESRS E1 Climate change.

- Mandatory disclosures in cross-cutting and topical standards that emanate from relevant EU legislation, in particular the Sustainable Finance Disclosure Regulation (SFDR) (see ESRS 2, Appendix C).

- For companies with 250 or more employees, the DRs S1-1 to S1-9 in ESRS S1 Own workforce.

EFRAG provides guidance on how to do a materiality assessment:

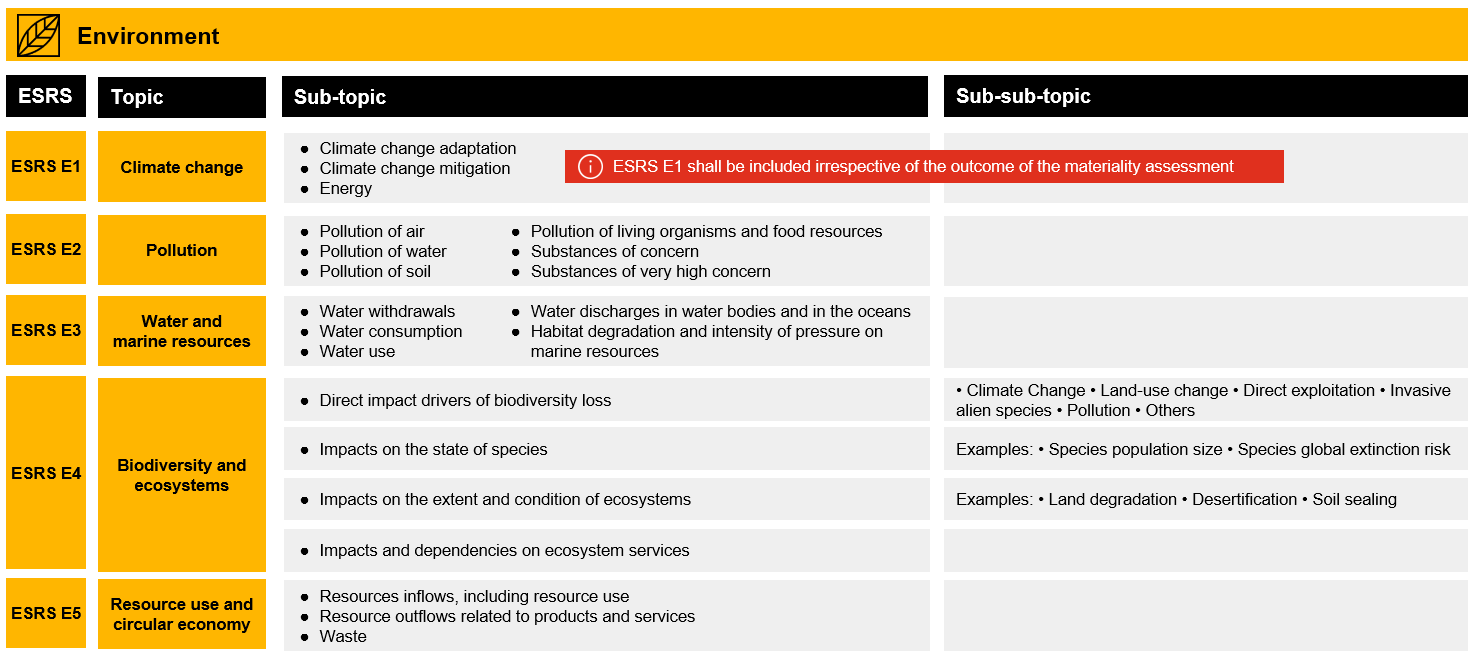

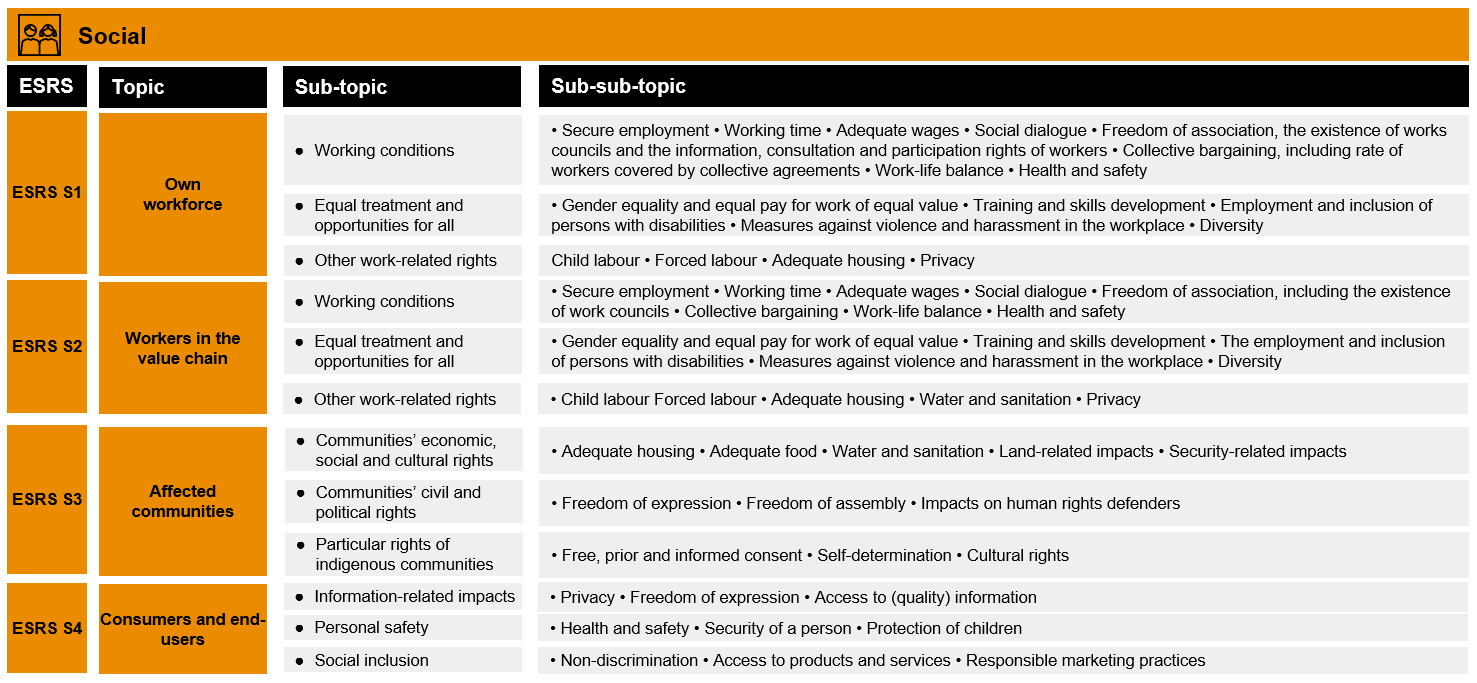

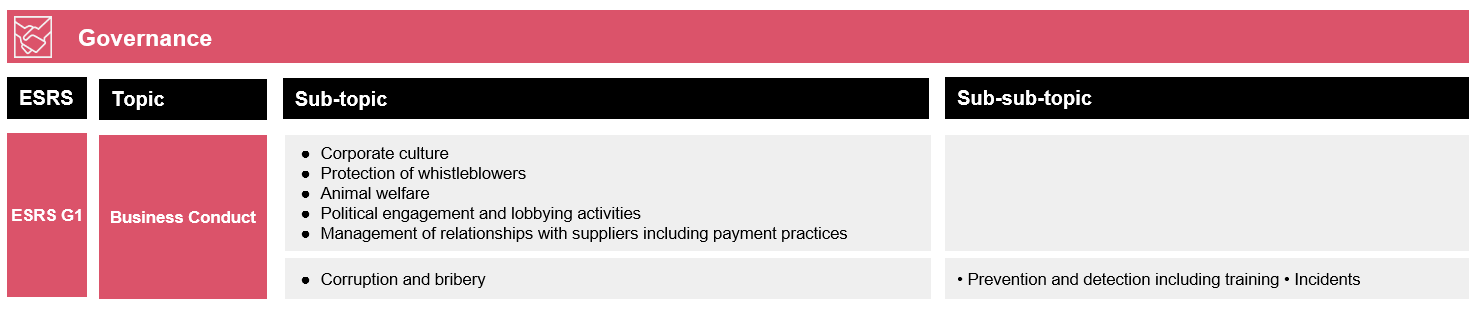

- There is a mandatory list of topics to go through (see in E, S and G sections the list of mandatory topics)

- The revised materiality approach has a list of sustainability matters to be included in the company’s materiality assessment (ESRS 1, Appendix B). See what needs to be included in the materiality assessment of the environmental, social and governance matters below.

- There are criteria to assess if a topic is material from the double materiality perspective:

- To assess impact materiality, for example the identification of actual negativei mpacts (determined by the severity of the impact) and potential negative impacts (determined by the severity and likelihood of the impact). During this process, the undertaking needs to engage with relevant stakeholders to understand the context in relation to its impacts. This includes its activities, business relationships, sustainability context and stakeholders. In addition, thresholds shall be adopted to determine the impacts to be covered in the sustainability statement.

- To assess financial materiality, an undertaking needs to consider the existence of triggers of iality of these triggers. Those triggers that generate risks or opportunities that have a material influence (or are likely to have a material influence) on the undertaking’s cash flows, development, performance, position, cost of capital or access to finance over short-, medium- and long-term time horizons.

- Impact materiality and financial materiality assessments are inter-related and the s shall be considered.

- The revised materiality approach contains a set of mandatory DRs and datapoints, to be disclosed irrespective of the outcome of the materiality assessment.

For the remaining disclosures and entity and sector specific matters, there are specific provisions to identify the information to be reported in the event that a sustainability matter is material according to the company’s materiality assessment (see illustration below).

If a company concludes that a certain sustainability matter is not material and omits all the DRs in a topical ESRS, it is required to explain the conclusions of its materiality assessment for the matter.

If a company comes to the conclusion that a certain sustainability matter is material, all DRs and datapoints related to policies, actions and targets shall be disclosed. If the company has no policies, actions or targets for the material sustainability matter, the company shall disclose this and it may report a timeframe to have these in place, as these DRs and datapoints can not be omitted. In addition, all ESRS 2 topic-specific DRs included in the relevant topical standard shall be applied.

When reporting on metrics, the company may omit specific DR(s) or datapoint(s), if the company assesses those not to be material. In this case, such information is considered to be implicitly reported as not material for the company.

Value chain

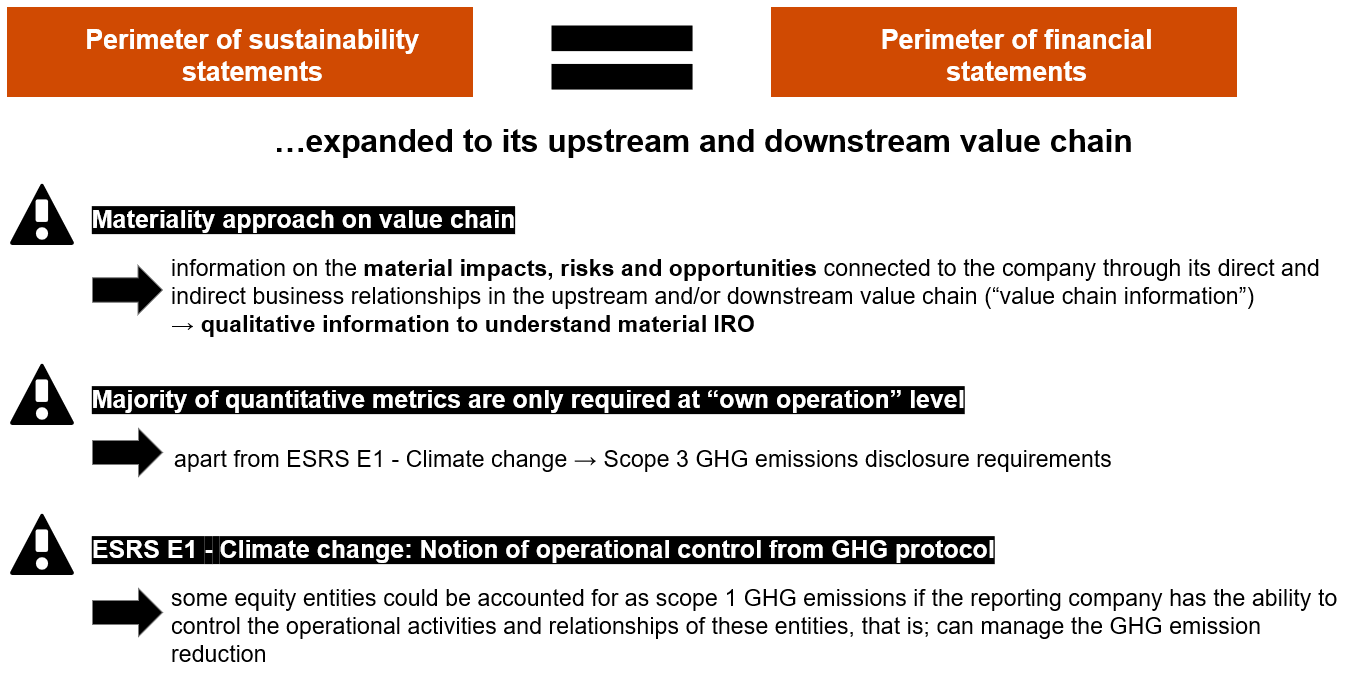

Compared to the ESRS EDs the approach to the value chain has been simplified and refocused (see illustration below).

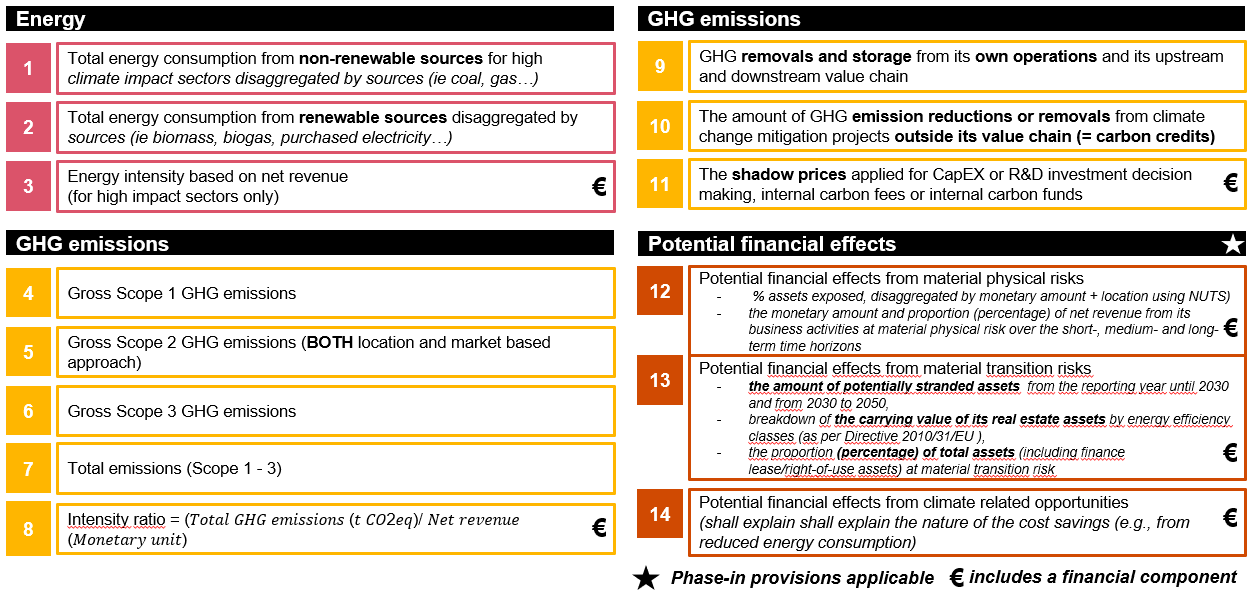

The reporting boundary would be based on the financial statements. It is expanded to cover material impacts, risks and opportunities related to the upstream (for example suppliers) and downstream (for example customers) value chain. This means that value chain information is not required for each disclosure, but only when specific provisions in the topical standards require it to do so. It is generally limited to material impacts, risk or opportunity, and most metrics only cover the company’s 'own operational' level. Exceptions to this can be found in ESRS E1 where value chain information is to be included for the disclosure of Scope 3 GHG emissions.

In addition, ESRS E1 foresees specific requirements for the assessment and disclosure of GHG emissions when a company has to apply the concept of 'operational control' to defining its value chain. If the company has operational control over an equity accounted entity (associate, joint venture or unconsolidated subsidiary) the full Scope 1 and 2 GHG emissions of this entity have to be included in the reporting company’s Scope 1 and 2 GHG emissions (see ESRS E1 paragraph 44). Operational control means that the company has the ability to control the operational activities and relationships of an entity and manage the GHG emission reduction.

The inclusion of value chain information may be postponed by three years, except for datapoints mandated by other EU regulation, ESRS 2 General Disclosure and ESRS E1 Climate change (see next page the section on 'Transitional provisions and phased-in disclosures').

Transitional provisions and phased-in disclosures

In order to support companies in the first years of implementation, transitional provisions have been introduced to various DRs and datapoints (see where they relate below).

ESRS 2 General disclosures

ESRS 2 contains the general disclosures that apply to all companies regardless of their sector of activity (sector agnostic) and apply across sustainability topics (cross-cutting).

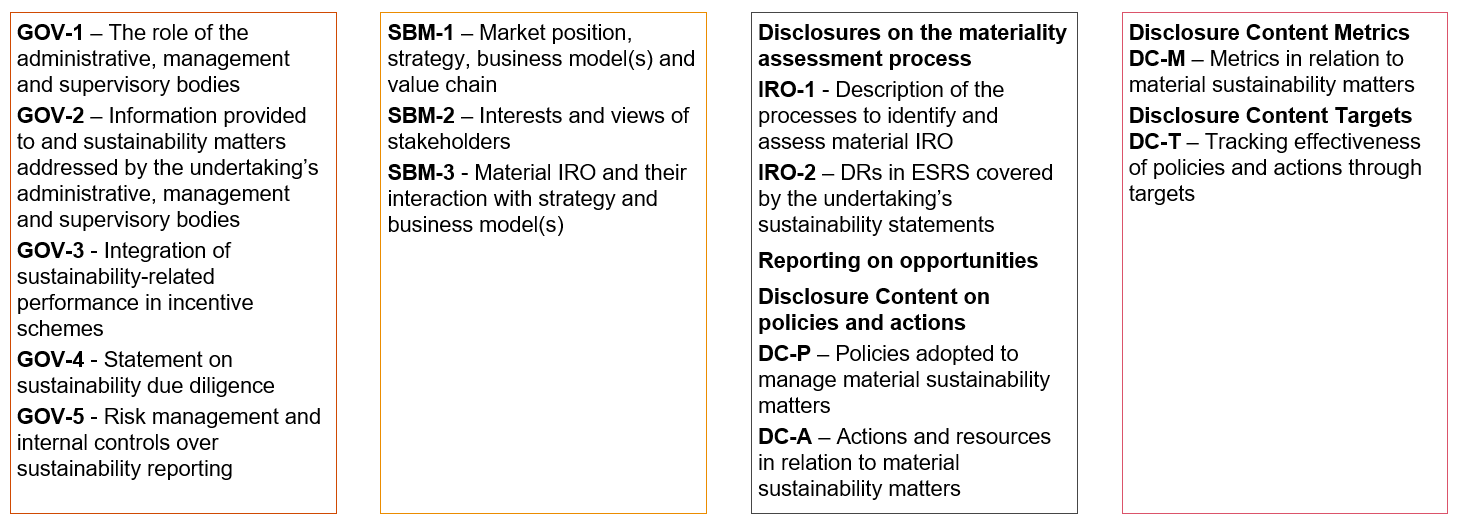

The number of DRs has been reduced from 22 DRs in the ED ESRS 2 to 12 DRs in ESRS 2. The reduction is due to a reorganisation where several DRs have been merged and simplified. The entire ESRS 2 is to be applied by all companies irrespective of the outcome of the materiality assessment.

The structure of ESRS 2 has changed according to the revised four pillar structure. See an overview of the content of ESRS 2 below.