Search within this section

Select a section below and enter your search term, or to search all click IFRS In briefs

Favorited Content

Key points

The IASB has issued IFRS 18, the new standard on presentation and disclosure in financial statements, with a focus on updates to the statement of profit or loss. The key new concepts introduced in IFRS 18 relate to:

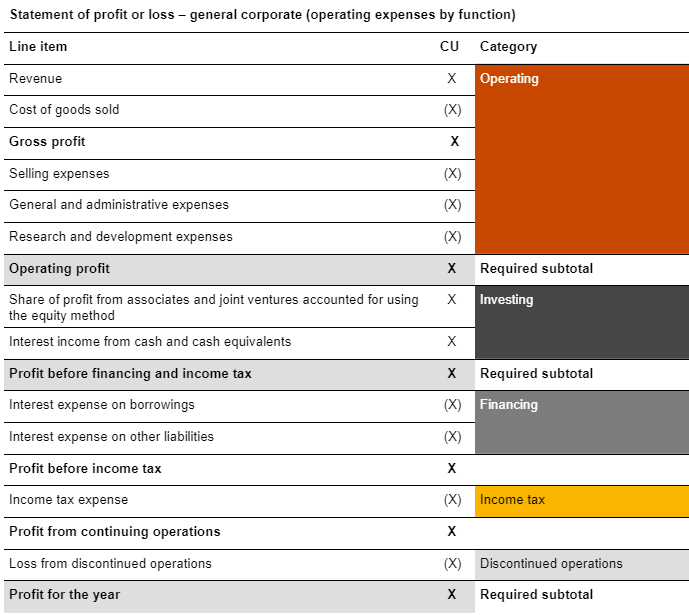

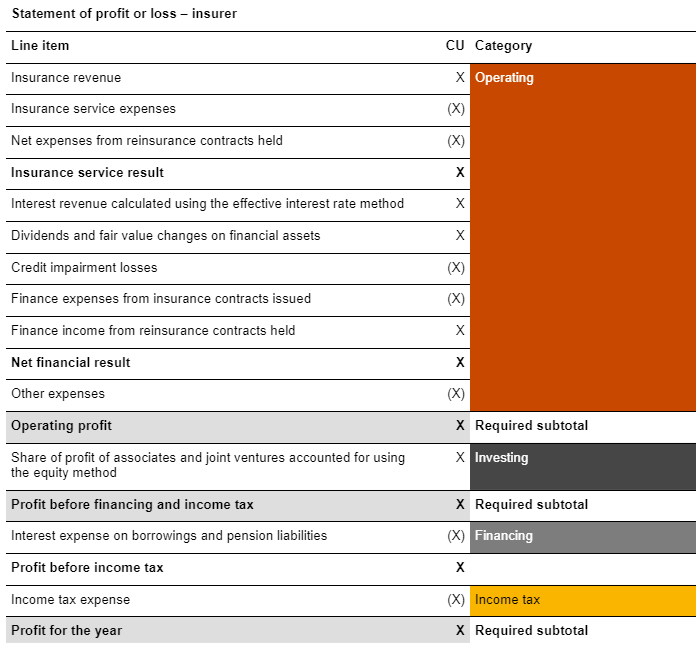

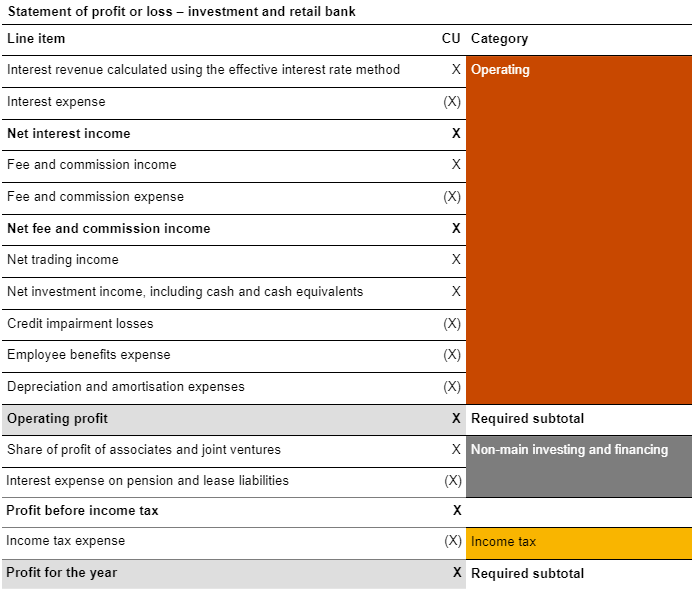

IFRS 18 will replace IAS 1; many of the other existing principles in IAS 1 are retained, with limited changes. IFRS 18 will not impact the recognition or measurement of items in the financial statements, but it might change what an entity reports as its ‘operating profit or loss’. IFRS 18 will apply for reporting periods beginning on or after 1 January 2027 and also applies to comparative information. The changes in presentation and disclosure required by IFRS 18 might require system and process changes for many entities, so entities should focus now to be ready for adoption.

|

View image

View image

PwC Observation |

|---|

The guidance on aggregation and disaggregation has changed. This will require entities to reconsider their chart of accounts to evaluate whether their existing presentation is still appropriate or whether improvements can be made to the way in which line items are grouped and described in the primary financial statements. In addition, changes in the structure of the statement of profit or loss and additional disclosure requirements might require an entity to make significant changes to its systems, charts of accounts, mappings etc. The level of operational change required by the new standard should not be underestimated, and entities should start thinking about the operational challenges as soon as possible.

It might be difficult to identify MPMs, and extensive procedures might be required by auditors to assess completeness.

|

© #year# PricewaterhouseCoopers LLP. This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under licence.

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP, its subsidiaries or affiliates.

Select a section below and enter your search term, or to search all click IFRS In briefs