Background

On March 21, the SEC proposed sweeping new rules to enhance public company disclosures related to the risks and impact of climate change. New disclosures would be required for almost all public companies and would include climate-related financial metrics in the audited financial statements as well as disclosure of scope 1 and scope 2 greenhouse gas (GHG) emissions. Some registrants would also be required to disclose scope 3 emissions. Large accelerated and accelerated filers would be required to obtain assurance on scope 1 and scope 2 GHG emissions, on a phased basis. Adoption of the rules would also be phased, starting with large accelerated filers. As proposed, if the rules are adopted in 2022, the disclosures for large accelerated filers would be effective in 2023.

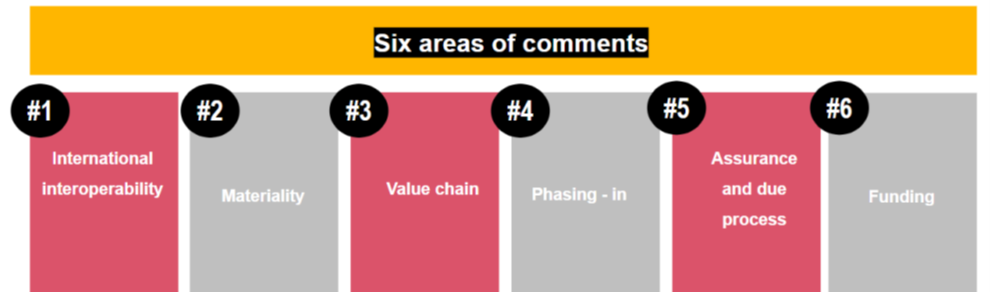

On June 17, we submitted the firm’s

comment letter in response to the SEC’s proposal on climate disclosures. This article summarizes the key themes included in our response letter.

Overall perspective

Our response letter supports the need for mandated climate disclosures; however, we recommend changes to improve operability for preparers while also meeting the following objectives:

- We believe the increased transparency provided by quality climate information is important for the liquidity and efficiency of the capital markets.

- We believe that greater integration of climate information with broader disclosures about a registrant’s business and financial information enhances value by providing context for both climate and financial data; integrated high-quality data is the foundation of effective climate disclosures.

- Change management and consensus developed through transparent and inclusive transition activities will advance reliability and confidence in the new disclosures.

We highlight effective implementation as a critical factor in the ultimate success of the new disclosure regime. To that end, we advocate for the establishment of a transparent, inclusive climate disclosure implementation group, under the leadership of the SEC staff, to support quality in disclosures through the timely identification, discussion and resolution of application matters both prior to and after the effective date of the proposed rules. We believe this group would improve disclosure comparability and usefulness, while reducing the cost of the compliance process.

Scope of application

What are our views on application of the proposed rules to foreign private issuers?

The proposed rules would scope in foreign private issuers (FPIs), with no provision for application of an alternative reporting regime. There are however a number of other active climate proposals — including the development of new European reporting requirements under the Corporate Sustainability Reporting Directive (CSRD), proposed standards from the International Sustainability Standards Board (ISSB) and mandates to apply the Task Force on Climate-related Financial Disclosures (TCFD) in a number of countries — and various constituencies responded to the SEC proposal advocating an alternative reporting provision for FPIs. Further, many letters expressed support for the ISSB’s potential role in developing a global framework and suggested looking to those standards as a reporting alternative. We agree that an alternative reporting regime would enhance the operability of the proposed rules for FPIs, and potentially US multinationals.

We support alignment among global frameworks as we believe alignment will decrease costs of compliance, improve information quality and comparability, and enhance disclosure effectiveness.

Why do we support inclusion of climate disclosures in annual filings, but recommend excluding registration statements from the proposed rule?

We support the proposed inclusion of the climatechange disclosures in annual Exchange Act filings as well as the proposed periodic update requirements. We believe however that the time and cost of preparing this information may be viewed as onerous and a barrier to entry to the capital markets by a company whose resources are already stretched by the compliance obligations of an initial public offering or acquisition.

We recommend excluding registration statements from the proposed climate disclosure requirements (specifically, Forms S-1, F-1, S-4, F-4, S-11), except as incorporated by reference from another filing (for example, a Form 10-K incorporated in a Form S-3). The initial exemption would allow more time to focus on the preparation of the financial information included in the filing. Further, we recommend the SEC provide transition relief for newly public companies (including de-SPAC transactions) as well as newly acquired entities. A transition period would reduce the burden on these companies by allowing them to defer implementation or integration until after a successful offering, or acquisition, respectively.

Investor-grade information

Investors expect quality data and are entitled to the same confidence in climate information as they currently expect from financial disclosures. Our comment letter encourages the SEC to make changes we believe would enhance data quality.

What are our views on the proposed effective dates?

We support the phased approach to adoption and agree with the suggested phasing. Nonetheless, although large accelerated filers may be better equipped to adopt these new requirements, they may also have additional challenges given the scope of their operations. We recommend a delay in the adoption date of the standard by one year to provide time for companies to develop appropriate processes and procedures. Although many companies provide voluntary sustainability reporting in some form, climate disclosure processes and controls are often nascent and may not be applied with the same rigour as those related to the production of financial information. Companies may need to develop or enhance their systems, processes and controls to produce information of the scope required by the proposed disclosures at a level of quality commensurate with that expected in an SEC filing.

Additionally, we recommend that reporting of historical periods be phased-in, with only the current fiscal year reported in the initial year of adoption, with comparative information phased in over subsequent years.

Why do we support reasonable assurance on scope 1 and scope 2 GHG disclosures for large accelerated and accelerated filers?

Confidence in the financial and non-financial information disclosed by registrants is a critical component of efficient capital markets. Consistent with this perspective, in our global investor survey completed in fall 2021, 79% of respondents reported having more trust in ESG information if it has been assured.

Further, almost three-quarters (73%) of investors surveyed think ESG metrics should be assured at the same level as the financial statement audit.

For large accelerated and accelerated filers, the SEC proposes that scope 1 and scope 2 information would initially be provided with no assurance, followed by limited assurance, with reasonable assurance in the fourth year and thereafter. Some argue that the additional time between initial reporting and reasonable assurance is needed for registrants to implement processes and procedures necessary to prepare data of the quality commensurate with an SEC filing. Others suggest that the delay in reasonable assurance would provide time for conventions to develop around the approach to these audits.

We have concerns that investors will not appreciate the difference in the confidence provided by the different levels of assurance, especially when presented in the same filing as the audited financial statements. Investors may place disproportionate reliance on disclosures subject only to the review procedures of a limited assurance engagement, creating an expectations gap.

Hence, as long as the adoption date is extended (as discussed previously), we believe reasonable assurance should be required over scope 1 and scope 2 emissions information beginning in the first year of disclosure for impacted filers.

Operability

How would we improve the operability of the proposed physical and transition risk disclosures?

Some of what we heard from preparers during the comment letter process included questions about how to determine the scope of the climate risks, concerns about what is in scope, concerns that transition risks are too broad and difficult to delineate from business as usual, and other objections in the same vein. We also had concerns that a broad requirement to disclose all climate-related risks that are “reasonably likely to have a material impact on the registrant” may trigger a long list of boilerplate disclosures — particularly given the uncertainty surrounding climate change over the long term.

To address many of these concerns, we recommend an approach that leverages the principle of allowing investors to look at a company “through the eyes of management,” tailoring disclosure of risks through the application of a management lens. Focusing disclosures on the climate information that the registrant’s management uses to make strategic decisions would improve its usefulness, while simultaneously reducing the burden on registrants.

How would we improve the operability of the proposed 1% threshold for financial and expenditure metrics?

The SEC proposal would require financial and expenditure impact disclosures of severe weather events and other natural conditions and transition activities in the financial statement footnotes if the absolute value impact on a financial statement line item is greater than a 1% bright-line threshold.

Opposition to the 1% “bright-line” threshold is one of the most — if not the most — universal criticisms of the SEC proposal. We agree that the 1% threshold (or any bright-line threshold) is inoperable and inconsistent with the concepts of materiality applied to the financial statements. In our view, the proposed 1% bright-line threshold for financial statement line item disclosure may elicit a volume of information that is not meaningful to investors.

To address these issues, we believe the SEC should consider an alternative approach, requiring disclosure of only those climate events or risks that materially impact the financial statements. Alignment with existing materiality concepts would provide more cohesive disclosures and greater focus on information that would be meaningful to investors.

What is our position on scope 3 greenhouse gas disclosures?

The proposal would require a registrant (except smaller reporting companies) to disclose total scope 3 emissions — across all categories — if material or if the registrant has a target or goal that includes scope 3 emissions. We recognize that investors may benefit from some information about GHG disclosures associated with a company’s value chain, especially in circumstances when the value chain includes emissions intensive activities. We agree however with concerns that these disclosures may be onerous to prepare and yield information that is not meaningful. Further, there is currently no framework for determining the materiality of emissions disclosures, and it is unclear how investors would view these disclosures through a traditional materiality lens.

We recommend that the Commission require all registrants - including smaller reporting companies - to disclose scope 3 emissions if the registrant has announced a target or goal; however, we believe those disclosures should be limited to only those scope 3 categories included within the stated target or goal. When the registrant has not set a target or goal, the Commission should refine the required disclosure to narrow the number of categories required to be reported.

Find out more

For more information on the proposed rules, refer to PwC’s In the loop, The SEC wants me to disclose what?.