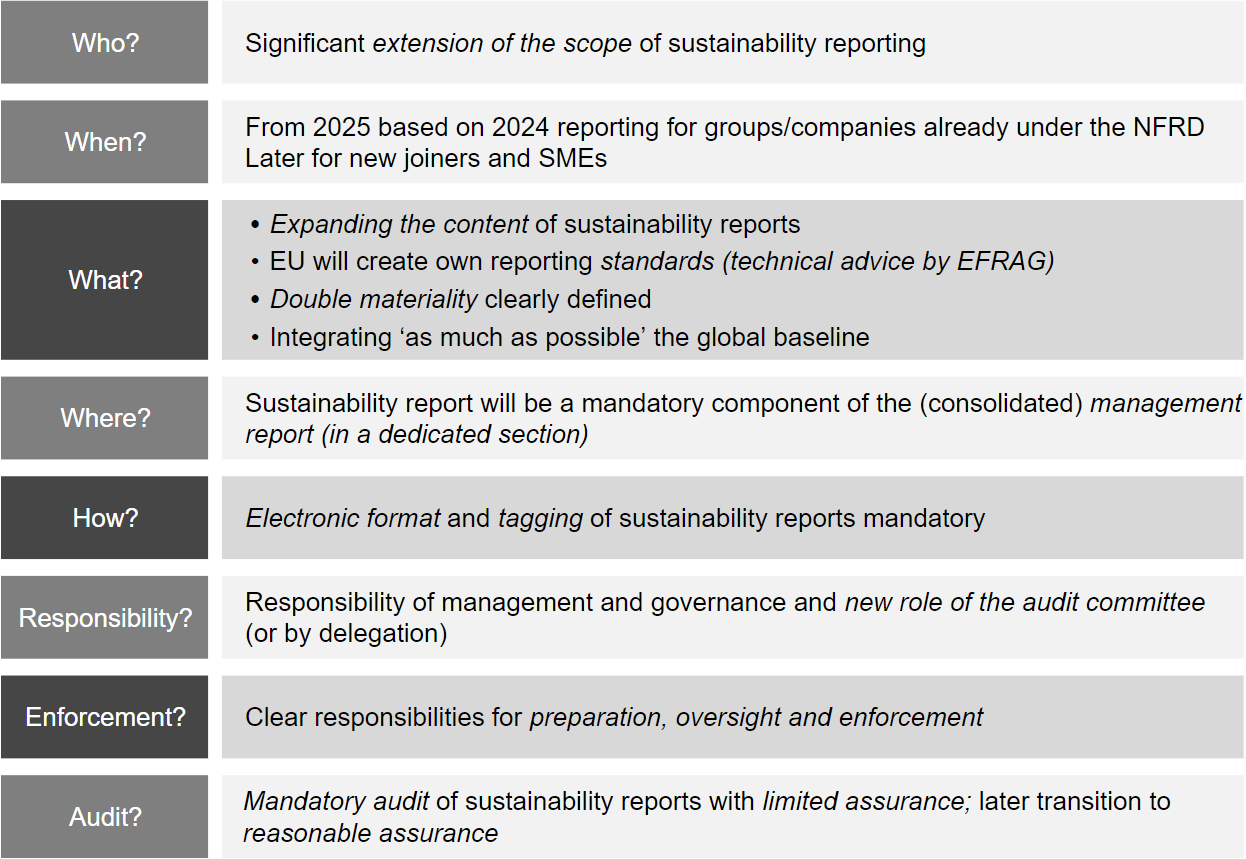

More detailed disclosures

Undertakings subject to the CSRD will be required to provide more information than under the NFRD. Undertakings falling within its scope will be required to include the following disclosures in their management report:

- information necessary to understand the undertaking's impacts on sustainability matters, that is, environmental, social and governance matters; and

- information necessary to understand how sustainability matters affect the undertaking's development, performance and position (double materiality).

In particular, undertakings will need to provide:

- a brief description of their business model and strategy, including:

- the resilience of the undertaking's business model and strategy to risks related to sustainability matters;

- the opportunities related to sustainability matters;

- the plans of the undertaking to ensure that its business model and strategy are compatible with the transition to a sustainable economy. This means the limiting of global warming to 1.5 °C in line with the Paris Agreement, the objective of achieving climate neutrality by 2050 and the exposure to coal-, oil- and gas-related activities.

- a description of the time-bound targets related to sustainability matters set by the undertaking. These include absolute greenhouse gas emission reduction targets for at least 2030 and 2050 and a description of the progress the undertaking has made towards achieving those targets;

- a description of the role of the administrative, management and supervisory bodies in sustainability matters and of the expertise and skills they need to fulfil this role or of their access to such expertise and skills;

- a description of the undertaking's policies in relation to sustainability matters;

- information about the existence of incentive schemes offered to members of the administrative, management and supervisory bodies which are linked to sustainability matters;

- a description of:

- the due diligence process implemented by the undertaking with regard to sustainability matters and where applicable in line with EU requirements;

- the principal actual or potential adverse impacts connected with the undertaking's own operations and its value chain, including products and services, business relationships and supply chain;

- any actions taken by the undertaking, and the result of such actions, to prevent, mitigate, remediate or bring an end to actual or potential adverse impacts.

- a description of the principal risks to the undertaking related to sustainability matters, including the undertaking's principal dependencies on such matters and how the undertaking manages those risks; and

- indicators relevant to the disclosures referred to above.

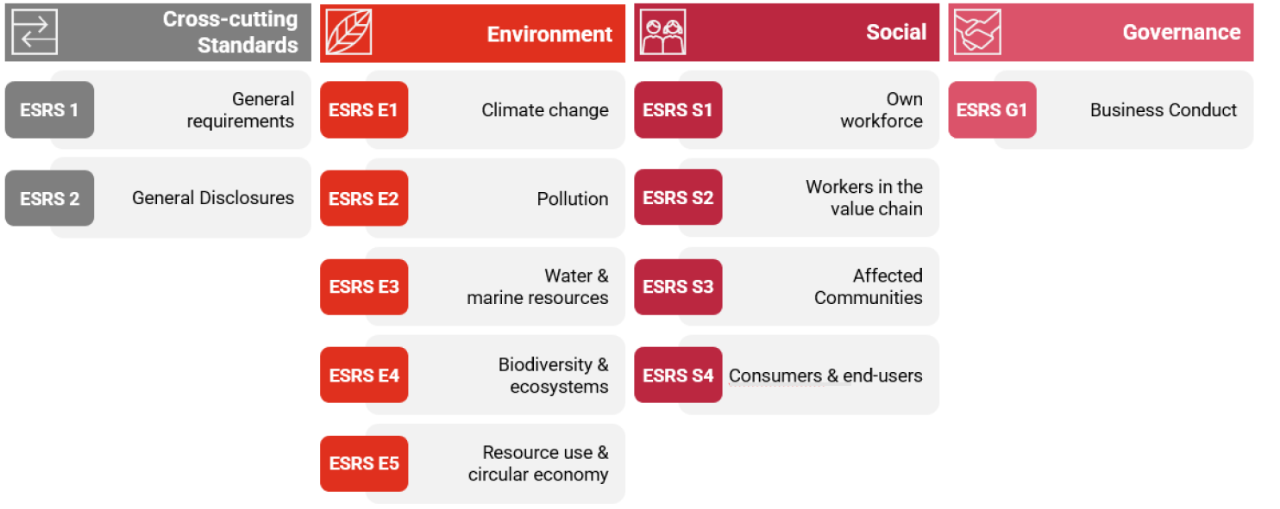

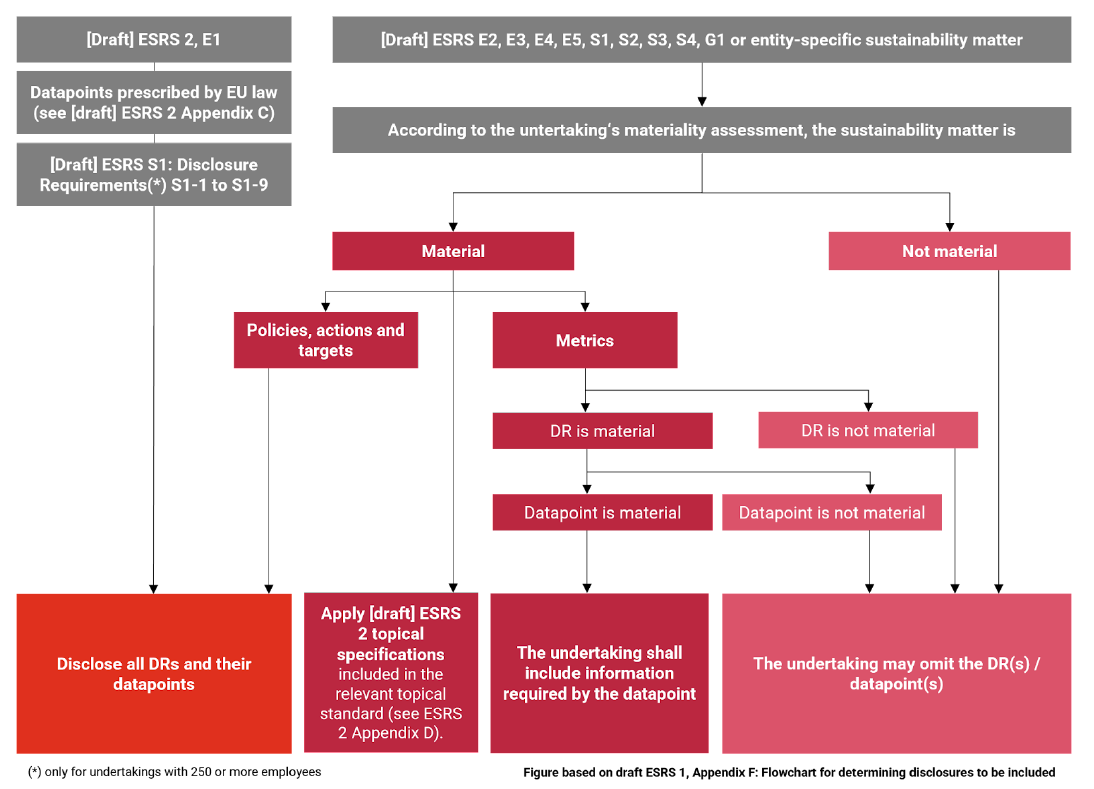

This information will need to be prepared in accordance with the European Sustainability Reporting Standards, which will further expand disclosure requirements (for example in the area of pollution).

Progressive requirements for value chain disclosures in certain cases

Where applicable, the information referred to in the previous page shall contain details about the undertaking's own operations and about its value chain. This includes products and services, business relationships and supply chain.

For the first three years of the application of the CSRD, in the event that not all the necessary information regarding the value chain is available, the undertaking shall explain the efforts made to obtain the information about its value chain, the reasons why this information could not be obtained, and the plans of the undertaking to obtain such information in the future.

Simplified sustainability reporting requirements for listed SMEs

The CSRD created SME-specific sustainability reporting standards for listed SMEs. Listed SMEs may limit their sustainability reporting to the following information:

- a brief description of the undertaking's business model and strategy;

- a description of the undertaking's policies in relation to sustainability matters;

- the principal actual or potential adverse impacts of the undertaking with regards to sustainability matters and any actions taken to identify, monitor, prevent, mitigate or remediate such impacts;

- the principal risks to the undertaking related to sustainability matters and how the undertaking manages those risks; and

- indicators necessary to the disclosures referred to above.

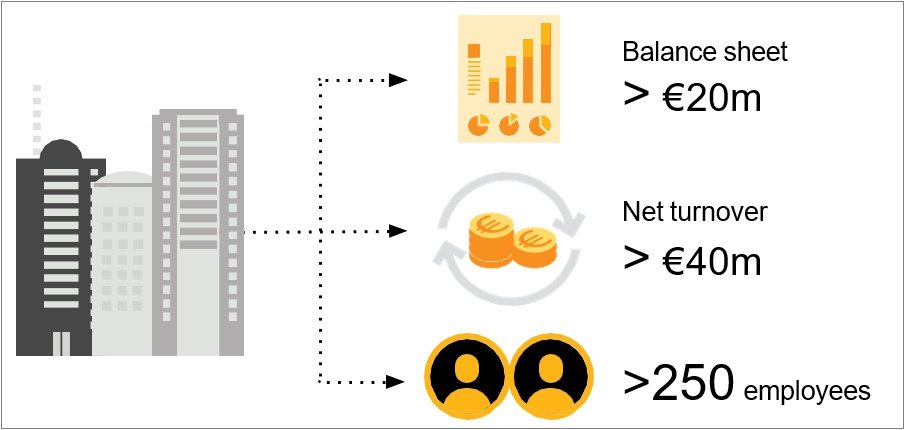

As a reminder, the EU defines an SME as an undertaking that does not exceed at least two of the three following criteria:

- balance sheet total: €20m;

- net turnover: €40m;

- average number of employees during the financial year: 250;

Standardised sustainability reporting

The CSRD provides for the adoption by the European Commission of a set of European Sustainability Reporting Standards (ESRS), which will standardise sustainability disclosures and make information easier to compare.

In November 2022, EFRAG submitted draft European Sustainability Reporting Standards to the European Commission. The drafts will be followed by final standards after adoption by the European Commission, expected in June 2023.

The 12 draft ESRS correspond to the first set of reporting standards (see article on ESRS).

The CSRD provides for the adoption of the sector-specific and SME-proportionate standards as well as of standards for third country undertakings by 30 June 2024.

Sustainability reporting standards for SMEs The CSRD provides for the adoption by the European Commission of specific sustainability reporting standards for SMEs. These are proportionate to their capacities and resources, and relevant to the scale and complexity of their activities.

Sustainability statement is to be included in a specific section of the management report

In order to make it easier to read and identify sustainability information, undertakings will have to disclose sustainability information in a dedicated section of their management report, or in the group’s management report of parent undertakings.

Mandatory publication of the management report

To ensure that sustainability information is publicly available, the CSRD provides that all undertakings required to report sustainability information must publish their management report, with no possible exemptions.

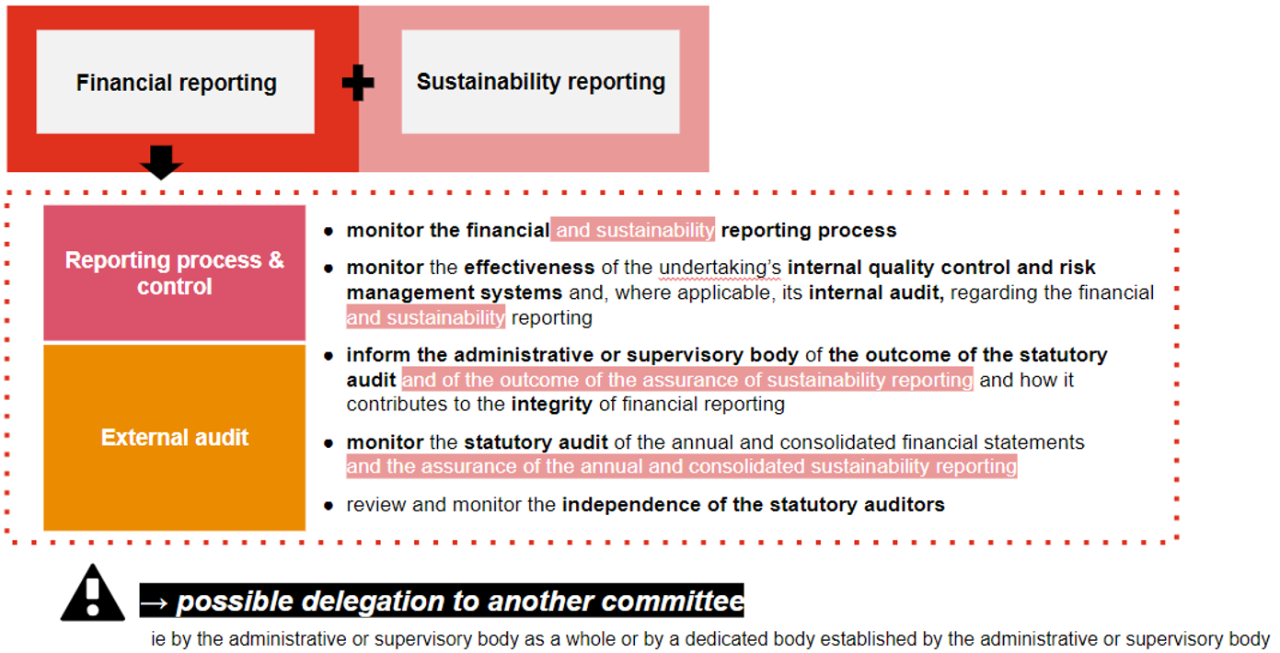

New role of audit committee

The CSRD extends the role and responsibilities of a public interest entity’s audit committee to the sustainability reporting.

The management report must be prepared in the European Single Electronic Format (ESEF)

In order to enable sustainability information to be used more efficiently, the CSRD provides that undertakings required to report sustainability information shall prepare their management report (or group management report) in the single European Single Electronic Format, i.e. the XHTML format that is already required for the preparation of annual financial reports by undertakings listed on EU-regulated markets.

In addition, undertakings are required to mark-up their sustainability reporting including the disclosures of Art. 8 Taxonomy Regulation (‘digital tagging’).

There is no exemption for undertakings not listed on a regulated market.

A digital taxonomy to the EU sustainability reporting standards and the Art. 8 Taxonomy Regulation disclosures will therefore be necessary to enable undertakings to tag the reported information in accordance with these standards.

Who will verify the sustainability statement?

To be considered reliable, the CSRD requires sustainability information in the management report to be reviewed by the statutory auditor or the audit firm that audits the financial statements.

Under the NFRD, the verification of non-financial information was an optional requirement at the discretion of individual Member States.

The statutory auditor will be required to issue an opinion based on a limited assurance engagement (and in the future based on a reasonable assurance engagement in order to have a similar level of assurance for financial and sustainability information) on:

- the compliance of the sustainability reporting with the requirements of the CSRD, including the compliance of the sustainability reporting with European reporting standards;

- the process carried out by the undertaking to identify the information reported pursuant to those reporting standards; and

- the compliance with the requirement to mark-up sustainability reporting and as regards the compliance with the reporting requirements of article 8 of the Taxonomy Regulation.

Member States may provide in their legislation that this task may also be entrusted to:

- a statutory auditor other than that carrying out the statutory audit of financial statements; or

- an independent assurance services provider.

Limited and reasonable assurance are both on the table:

October 2026: On or before 1 October 2026, the Commission will provide limited assurance standards for auditors to use when assessing the assurance of sustainability statement.

October 2028: On or before 1 October 2028, reasonable assurance standards should be provided.

When will the new CRSD come into force?

In order to give undertakings sufficient time to adapt to the new requirements of the CSRD, implementation will take place in four stages:

- 1 January 2024 for undertakings already subject to the NFRD (reporting in 2025 on 2024 data);

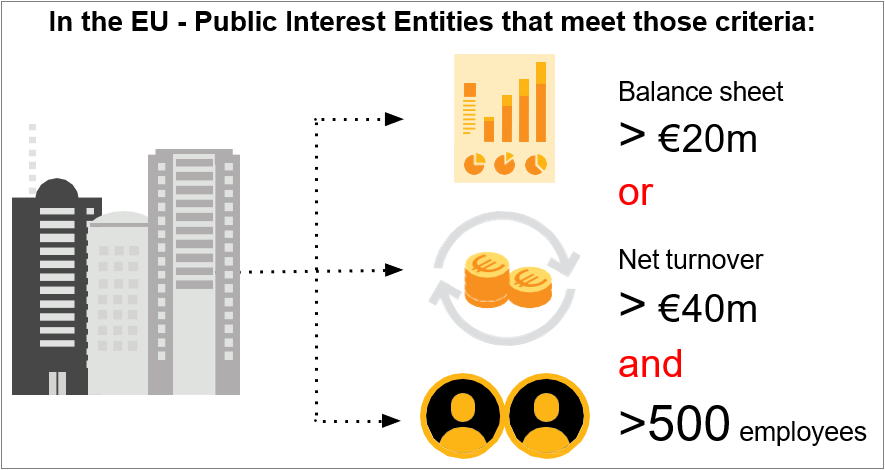

- 1 January 2025 for large undertakings not currently subject to the NFRD (reporting in 2026 on 2025 data);

- 1 January 2026 for listed SMEs, as well as for small and non-complex credit institutions and captive insurance undertakings (reporting in 2027 on 2026 data). However, under the directive, listed SMEs may opt out from the reporting requirements until 2028, provided that they state in their management report why the sustainability information has not been provided;

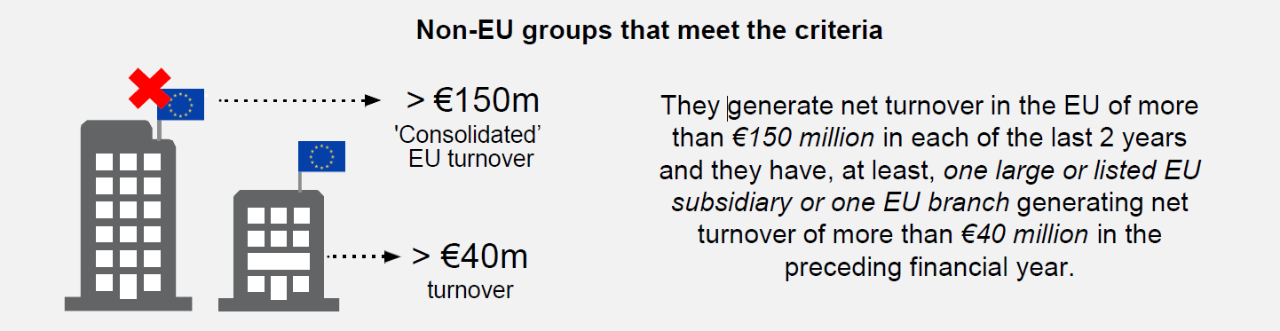

- 1 January 2028 for non-EU undertakings (reporting in 2029 on 2028 data).

The CSRD will need to be transposed into the various national laws of the Member States of the European Union. Each State has the possibility to provide for national provisions that are more stringent than those provided for in the directive and/or to decide on the provisions left to the discretion of Member States.

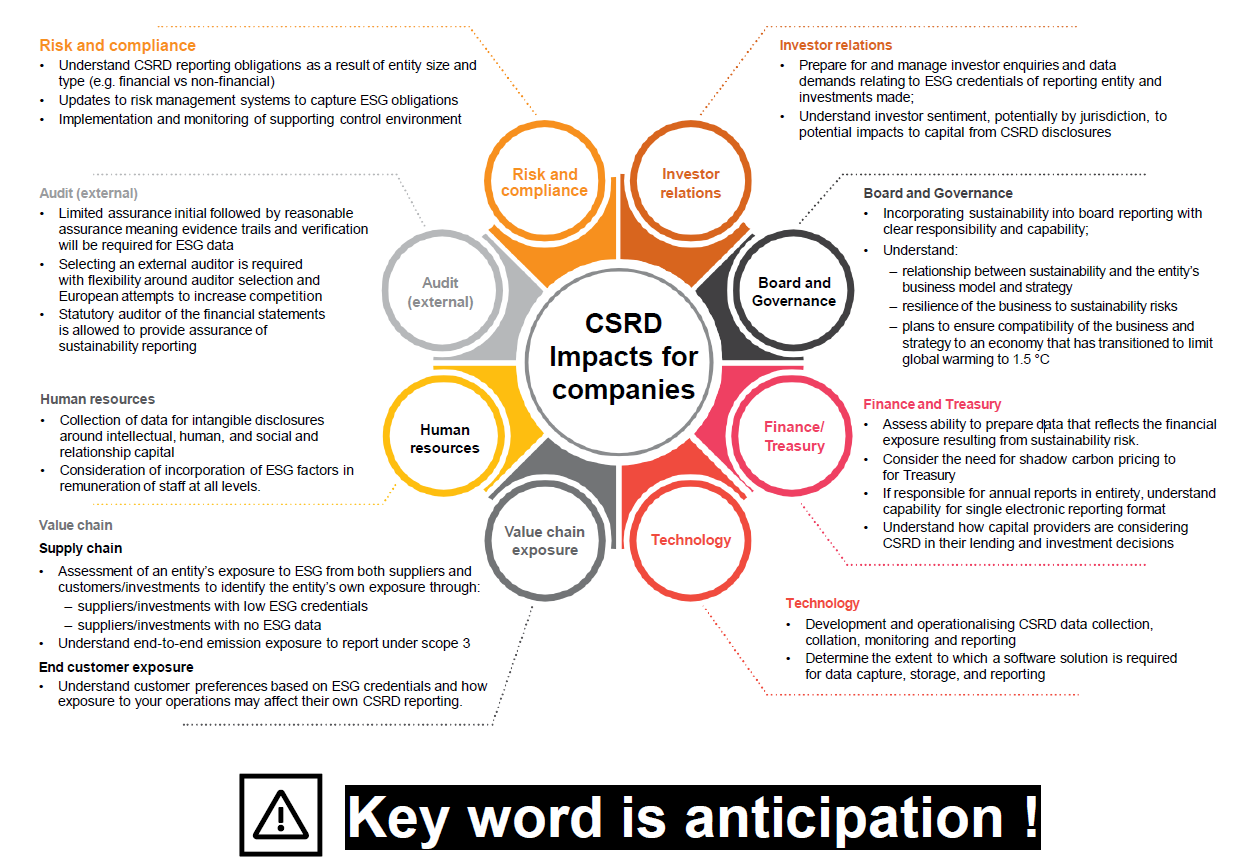

CSRD Impacts for companies

The CSRD is expected to impact almost every part of an organisation. While the ESRS are still under construction the below map reflects the expected impacts.

View image

View image