Key points

This In brief highlights some key treasury topics for corporate entities, such as classification of foreign exchange differences, derivatives gains and losses and income and expenses on other financial instruments.

What’s the issue?

In April 2024, the IASB issued

IFRS 18, 'Presentation and Disclosure in Financial Statements' in response to investors’ concerns about comparability and transparency of entities’ performance reporting. IFRS 18 introduces new requirements to increase comparability of similar entities, especially related to how ‘operating profit or loss’ is defined.

IFRS 18 will replace IAS 1 ‘Presentation of financial statements', whilst retaining many of the principles from IAS 1 with limited changes. IFRS 18 will not impact:

- the recognition or measurement of items in the financial statements; or

- which items are presented in other comprehensive income or how.

Key IFRS 18 treasury topics from the perspective of a corporate entity, include:

Structure of the statement of profit or loss

IFRS 18 introduces a defined structure for the statement of profit or loss. The goal is to reduce diversity, so as to help investors to understand the information and make better comparisons between entities. The structure is composed of categories and required subtotals.

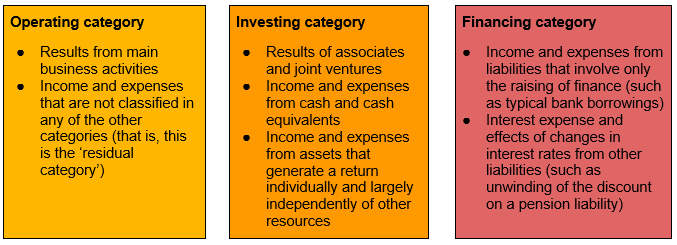

Items in the statement of profit or loss will be classified into one of five categories: operating; investing; financing; income taxes; and discontinued operations.

The classification of items into these categories can differ depending on the main business activity of the entity. This In brief discusses the requirements for a corporate entity that does not have a main business activity of providing financing to customers or investing in assets. Additional considerations apply for entities such as banks or insurers that have one of these main business activities. A treasury entity preparing individual financial statements applying IFRS 18 might conclude that it provides financing to customers as a main business activity. Our separate In brief,

IFRS 18 - Insights for financial services companies, takes a closer look at the new standard from the perspective of entities that provide financing to customers or invest in assets as main business activities.

PwC observation - main business activity assessment |

The assessment of main business activity is performed at the reporting entity level. This means the conclusion at group level might differ from that at the subsidiary level, resulting in some income and expenses needing to be reclassified on consolidation.

Some entities, particularly conglomerates, might need to apply judgement to assess whether they provide financing to customers or invest in assets as main business activities. IFRS 18 provides examples of evidence that could indicate the main business activities of an entity. This assessment is based on facts, and not purely an assertion for accounting purposes.

|

The three main categories in IFRS 18 are operating, investing and financing. For a corporate entity, these will typically include the following:

Typically an entity receives financing through issuing debt or its own equity instruments. A transaction is considered to involve only the raising of financing when an entity:

- receives cash and at a later date repays the financing through cash or its own equity instruments;

- has a liability that is extinguished in exchange for another liability or by issuing its own equity instruments, for example when an entity refinances an existing debt instrument; or

- issues its own equity instruments or repurchases its own equity instruments for cash.

Liabilities that do not arise from ‘transactions that involve only the raising of finance’ will be categorised as ‘other liabilities’ including, for example, trade payables, lease liabilities and commodity loans.

PwC observations - categorising income and expenses |

- Profit or loss compared to cash flow statement - the IFRS 18 classification of income and expenses in the statement of profit or loss might not align with how the related cash flows are presented in the cash flow statement, applying IAS 7. For example, in a lease arrangement the cash outflow (principal and interest) will be presented as financing cash flow, applying IAS 7 (refer to ‘Other changes introduced by IFRS 18’ below). Applying IFRS 18, depreciation expenses on the right of use asset will be classified in the operating category while interest expenses on the lease liability will be classified in the financing category.

- ‘Financing liabilities’ compared to financial liabilities - liabilities arising from ‘transactions that involve only the raising of finance’, as described by IFRS 18, consist of only a subset of financial liabilities as defined by IAS 32. This means that some income and expenses from liabilities within the scope of IFRS 9 will be classified in the operating category.

- Hybrid contracts - classification of gains and losses on a hybrid contract with a host liability (financial or non-financial) that includes an embedded derivative will be complex and depends on:

- whether the embedded derivative is required to be separated;

- whether the liability arises from a transaction that involves only the raising of finance; and

- how the hybrid contract is classified

.

|

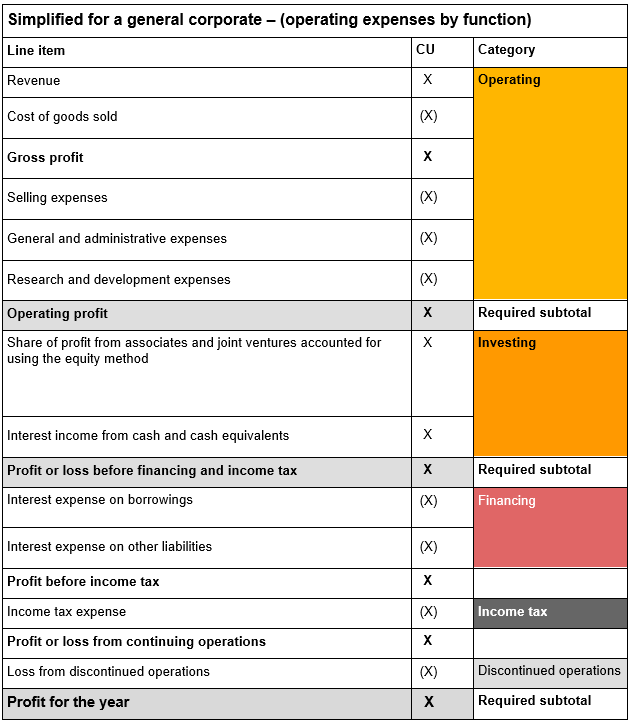

IFRS 18 requires entities to present specified totals and subtotals. The main change is the mandatory inclusion of 'Operating profit or loss' - defined as the result from the operating category. The other required subtotals are ‘Profit or loss before financing and income taxes’ and ‘Profit or loss’ as shown in this

illustrative example.

Classification of foreign exchange differences

IFRS 18 introduces detailed requirements for classifying foreign exchange (FX) differences recognised in the statement of profit or loss applying IAS 21. FX differences will be classified in the same category as the income and expenses from the items that resulted in the FX differences (unless this would involve undue cost or effort). For example, FX differences arising:

- on a foreign-currency denominated receivable for goods and services will be classified in the operating category; and

- on a foreign-currency denominated liability that arises from a transaction that involves only the raising of finance will be classified in the financing category.

PwC observations - FX differences |

- Line items - many entities today present FX gains and losses in a single line item, often as part of operating profit. IFRS 18 might now require FX differences to be presented across the different categories in the statement of profit or loss. An entity will also need to consider the revised principles of aggregation and disaggregation to determine the appropriate line item within the particular category in which to present it.

- Cash - a corporate entity applying IFRS 18 will present FX differences on cash in the investing category. If foreign currency is held in a bank account as an economic hedge of an FX-denominated borrowing, there will be a ‘classification mismatch’ with the FX differences on the borrowing being classified in the financing category. An entity could avoid this mismatch either by designating the cash as a hedging instrument, or by using derivatives instead of cash for economic hedging purposes.

|

Classification of gains and losses on derivatives and designated hedging instruments

Entities enter into financial instruments, including derivatives, for different reasons - for example, to manage specific risks or for trading. Applying IFRS 18, gains and losses on financial instruments are classified depending on why the entity enters into and holds the instruments.

Financial instruments used to manage identified risks

For financial instruments used to manage identified risks (for example, to mitigate an exposure to FX risk, commodity price risk or interest rate risk), gains and losses are classified as follows:

Financial instrument

| Gains and losses on: |

| Derivatives | Non-derivative financial instruments |

Designated as a hedging instrument applying IFRS 9 or IAS 39

|

Classify in the same category as the income and expenses affected by the risks the financial instrument is used to manage. However, if doing so would require the grossing up of gains and losses, instead classify all such gains and losses in the operating category.

|

Not designated in hedging relationships

|

Classify in the same category as the income and expenses affected by the risks the entity manages. However, if doing so would require the grossing up of gains or losses or involve undue cost or effort—instead classify in the operating category.

|

Classify for each asset or liability applying the ordinary classification requirements for assets and liabilities.

|

Derivatives not used to manage identified risks

Gains and losses on derivatives not used to manage identified risks are classified in the financing category, if the derivative relates to a transaction that involves only the raising of finance. Otherwise, they are classified in the operating category.

PwC observations - derivative gains and losses |

- Grossing up of gains and losses - An entity using a single derivative to hedge both the net FX risk on revenue (presented in the operating category) and FX risk on interest expenses (presented in the financing category) will classify gains or losses on the derivative in the operating category applying IFRS 18. Splitting the gains/losses on the derivative and presenting those parts in each category would result in the entity grossing up the derivative’s fair value and presenting a higher gain/loss in each category than what occurred on the derivative.

- Line items - IFRS® Accounting Standards do not currently specify where in the statement of profit or loss to present derivative gains and losses, resulting in diverse practices. On transition to IFRS 18, some entities will need to change their accounting policies.

IFRS 18 does not prescribe the line item in profit or loss in which to present derivative gains and losses, nor does it override the requirements in other standards. It does however prescribe the category of profit or loss in which to classify such gains and losses. In addition, an entity will need to consider the revised principles for aggregation and disaggregation to determine the appropriate line item to present these gains and losses.

|

Other changes introduced by IFRS 18

- disclosure requirements for ‘management-defined performance measures’.

- guidance and disclosures relating to presentation of operating expenses by nature, by function or both.

- enhanced requirements on aggregation and disaggregation.

- changes to IAS 7 Statement of Cash Flows, including removing the existing optionalities for presentation of interests and dividends paid and received. Applying IAS 7, as amended, a corporate entity that does not have a main business activity of providing financing to customers or investing in assets presents dividends paid as financing cash flows, interests and dividends received as investing cash flows and interests paid as financing cash flows.

Who is impacted?

All entities reporting applying IFRS Accounting Standards will be impacted.

When does it apply?

The new standard will be effective for annual reporting periods beginning on or after 1 January 2027, including for interim financial statements. An entity is required to restate comparative information on initial application.

Where do I get more details?

Watch this space for more guidance on the new standard. In the meantime, for more information about IFRS 18, contact your local PwC contact or

Marie Kling and

Gary Berchowitz.

Appendix - Illustrative example for a general corporate entity