4.1 Determining the accounting acquirer

In a SPAC merger, an important accounting judgement is the determination of which entity is the accounting acquirer. The accounting acquirer is the entity that obtains control of the reporting entity, and it might be different from the legal acquirer.

If the SPAC merger consideration, paid to the OpCo’s shareholders, is equity or a combination of cash and equity, it might not be clear which entity is the accounting acquirer, or whether the arrangement is a capital reorganisation rather than a business combination. The cash might be retained within the combined business or paid to shareholders of the OpCo. These situations require consideration of all pertinent facts and circumstances. The guidance in IFRS 10, ‘Consolidated Financial Statements’, is used to identify the accounting acquirer (that is, the entity that obtains control of another entity, the acquiree). In some cases, it will be clear that the previous owners of the legal acquiree have obtained control of the SPAC. However, in other cases this might not be clear, in which case the factors in paragraphs

B14–B18 of IFRS 3, ‘Business combinations’, should be considered in making the determination.

If the SPAC merger is carried out primarily by transferring cash or other assets or by incurring liabilities, the SPAC can be the accounting acquirer (refer to

Example 2 of FAQ 29.39.1 and

IFRIC Rejection December 2005 – whether a new entity that pays cash can be identified as the acquirer). In the unlikely event that the SPAC is the accounting acquirer, it would apply acquisition accounting and recognise the assets and liabilities of the OpCo at fair value in accordance with IFRS 3.

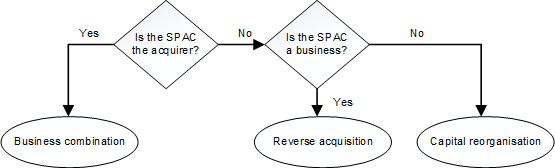

In a business combination effected primarily by exchanging equity interests, the acquirer is usually the entity that issues its equity interests. However, in some business combinations, commonly called 'reverse acquisitions' or ‘reverse listing’, the issuing entity (that is, the SPAC) is the acquiree.

The merger of an OpCo into a non-operating public shell corporation with nominal net assets typically results in:

- the owners of the private entity gaining control over the combined entity after the transaction; and

- the shareholders of the former public shell corporation continuing only as passive investors.

4.2 Reverse listing – capital reorganisation versus business combination

To account for a transaction under IFRS 3, an acquirer must always be identified and the acquiree must be a business. The acquirer is the entity that obtains control over the acquiree. As discussed in Section 4.1, in the SPAC transaction, the OpCo (the legal subsidiary) will often be identified as the accounting acquirer.

A SPAC merger is typically accounted for as a capital reorganisation, and the accounting is similar to a reverse acquisition under IFRS 3. This is because, in a SPAC merger, the OpCo will most likely be identified as the accounting acquirer, and the SPAC generally does not meet the definition of a business. Often, the SPAC’s only asset at the SPAC merger date is cash received from investors.

To account for the share-based payment, the deemed shares issued by the OpCo (that is, the consideration for the acquisition of the SPAC) are recognised at fair value and compared to the fair value of the net assets of the SPAC. Refer to

EX A1.49.1 – Reverse acquisition into shell company.

4.3 Determining the fair value of the consideration transferred in a reverse acquisition

The value of the consideration transferred by the accounting acquirer (OpCo) is based on the number of equity interests that the OpCo would have had to issue to the owners of the accounting acquiree (SPAC) in order to give the owners of the SPAC the same percentage of equity interests in the combined entity that results from the reverse acquisition.

So, the OpCo should fair value the consideration that a SPAC’s shareholders received (that is, the interest in the combined company that the SPAC shareholders retained) and the identifiable net assets of the SPAC that the accounting acquirer acquired. Any resulting difference would be unidentifiable goods or services, which should be expensed (refer to Section 4.2 above).

While it is possible to calculate the number of shares that the OpCo would have issued as consideration if it legally acquired the SPAC, in practice, it might be challenging to determine the fair value of the OpCo equity, because this entity is not listed. In this case, it might be appropriate to use the SPAC’s listed price and the number of shares owned by the existing SPAC shareholders to derive the fair value of the equity granted by the accounting acquirer. Judgement will need to be applied in making this assessment, and an entity should consider the outcome of applying this approach for reasonableness. Refer to

EX 29.61.1 – Consideration in a reverse acquisition.

4.4 Classification and measurement of contingent payments

In some cases, there might be uncertainty regarding the fair value of the OpCo (and, therefore, its shares). In other cases, the SPAC sponsors might agree to receive incremental value if the merger achieves a target return for the OpCo shareholders. One way of addressing this uncertainty is for the SPAC to enter into agreements with its sponsors, the selling shareholders of the OpCo, or employees whereby the combined entity will issue additional shares/warrants (or release existing shares from escrow or other restrictions) after the SPAC merger if certain performance measures (frequently based on share price) are met. These arrangements are commonly referred to as ‘contingent share payments'’ and might involve:

- contingent share payments to SPAC shareholders or sponsors;

- contingent share payments to shareholders of the OpCo;

- contingent share payments to employees of the SPAC or OpCo; or

- a combination of payments to various parties in the arrangement.

The assessment of the accounting acquirer in a SPAC merger should be performed prior to the evaluation of all other arrangements (refer to Section 4.1). If the transaction is accounted for as a business combination (that is, the SPAC is the accounting acquirer), the ‘normal’ guidance in IFRS 3 relating to contingent and deferred consideration applies for the consideration paid to the selling OpCo shareholders and employees (the flowchart in

FAQ 29.86.1 – What is the framework used to determine the classification of contingent consideration arrangements? illustrates the framework to determine the classification of contingent consideration arrangements). This is not the focus of the guidance that follows in this section.

The guidance that follows considers the implications of contingent payments in arrangements where the OpCo acquires a SPAC and the SPAC does not constitute a business. We consider the accounting implications, depending on the counterparty to the contingent share payments, as follows:

a. Contingent share payments with the SPAC shareholders or sponsors

As mentioned in Section 4.2 above, the transaction is within IFRS 2’s scope. The parties might agree that, if the listed price per share of the merged entity increases past a certain target, then as an incentive, the SPAC sponsors receive more shares as additional compensation for the successful listing. The commercial rationale of such a contingent payment is that the SPAC sponsors are receiving a bonus for a successful listing.

At the date of the SPAC merger, the transaction was within the scope of IFRS 2 for the OpCo. As part of that arrangement, there was an initial payment for the listing service, as well as a contingent additional payment, for which there is no service condition. The contingent payment feature therefore typically represents a non-vesting condition that is taken into account at the grant date and not subsequently updated. Therefore, at the date of the initial share-based payment, the entity would have needed to determine the grant date fair value of the potential incremental award.

b. Contingent share payments with shareholders of the OpCo

The parties might agree as part of the SPAC merger negotiation that if the listed price per share increases past a target price per share, then the merged entity will issue a bonus number of shares to the previous shareholders of the OpCo. In other words, the shareholders of the OpCo will receive more potential shares and possibly end up with a larger relative shareholding in the merged entity compared to the date of the SPAC merger. The commercial rationale of such payment is often to protect the shareholders of the OpCo where they believe that the business they have contributed to be more valuable than could be agreed with the SPAC shareholders at the time. Because the OpCo’s value is estimated, there is a risk that the OpCo will issue too much equity (ie overpay) for the listing service and net assets of the SPAC. The contingent share payment is one method to address this potential overpayment.

c. Contingent share payments with employees of the SPAC or OpCo

Where there are contingent share arrangements with employees or service providers of the SPAC or the OpCo, consideration should be given to whether the arrangement should be viewed as a compensation arrangement.

Share-based payments to employees might be provided for various reasons. The commercial rationale behind issuing the contingent shares to employees of the OpCo or SPAC might be to incentivise SPAC management to continue providing services after the merger. In addition, the SPAC sponsors can be provided free or discounted warrants at the time of the initial SPAC IPO, as an incentive to complete the SPAC merger.

SPAC transactions accounted for as a capital reorganisation might also include situations where holders of unvested restricted shares or unexercised share options of the OpCo receive the right to contingent shares. Depending on the terms, this could lead to additional compensation cost being recorded, and could also impact the subsequent accounting for the award. For example, an arrangement that requires continued employment or service in order to vest in, or be eligible for, the earn-out shares would typically result in treatment of the related cost as compensation cost (IFRIC January 2013 Update

IFRS 2 Share-based Payment – definition of vesting condition within Annual Improvements to IFRSs – 2010–2012 Cycle). Further, an earn-out provided in the form of modifying an existing share option agreement would also be a modification of the existing award, and any incremental fair value would be recognised as additional compensation cost. Guidance on modifications is considered in

EX 13.44.1 – Accounting treatment of modifications and

EX 13.43.1 – Modifications.

Additionally, even if the contingent share arrangement is independent of the existing share-based payment award and not dependent on continued employment, the entity would need to consider the facts and circumstances to determine the reason for providing employees with an incremental award. Typically, these would be accounted for as an incremental share-based payment.

4.5 Transaction costs

An entity typically incurs various costs in issuing or acquiring its own equity instruments, most of which are transaction costs. Transaction costs are incremental costs that are directly attributable to the equity transaction that otherwise would have been avoided if the equity instruments had not been issued. Transaction costs of an equity transaction should be accounted for as a deduction from equity, net of any related income tax benefit. [

IAS 32 para 35].

In many SPAC mergers, the transaction is, in substance, a listing and concurrent capital raise for the OpCo. This is because the OpCo issues its shares for both the cash in the SPAC and the listing service.

This might create a challenge. If an entity was only listing its existing equity, there would be no new equity issued, and the costs related to listing the existing equity would not be incremental costs related to the issuance of new equity. In this case, the costs would all be expensed through profit and loss. Conversely, if an entity issues equity in exchange for cash, it is likely that some of the costs related to that issuance would be incremental and recorded as a reduction of the proceeds. In many SPAC arrangements accounted for as a capital reorganisation, the OpCo is both issuing equity in exchange for cash and obtaining a listing of its existing equity. Transaction costs that relate jointly to more than one transaction (for example, costs of a concurrent offering of some shares and a stock exchange listing of other shares) are allocated to those transactions using a rational basis of allocation, which is consistent with similar transactions. [

IAS 32 para 38]. Refer to

FAQ 43.91.1 – How should transaction costs relating to more than one transaction be accounted for?.

4.6 Taxes

The tax implications of the SPAC merger would be based on whether the arrangement is a business combination and which entity is identified as the acquirer.

If the SPAC is the accounting acquiree, the OpCo is the acquirer and the SPAC does not meet the definition of a business (which is likely in a typical SPAC transaction). The transaction is therefore not a business combination. From the OpCo’s perspective, this is a capital reorganisation and a continuation of the OpCo as the reporting entity (that is, it is the initial recognition of the SPAC from the OpCo’s perspective. A deferred tax asset or liability is not recognised in respect of a temporary difference that arises on initial recognition of an asset or liability, in a transaction that is not a business combination, and the recognition does not affect accounting profit or taxable profit at the time of the transaction. A review of all specific facts and circumstances (including the existence of contingent payments and share-based payment agreements), as well as the tax implications of the arrangement, will be required to be able to conclude whether any deferred tax might arise as a result of the SPAC merger.

If the SPAC is the accounting acquirer, it would generally apply acquisition accounting and recognise the assets and liabilities of the OpCo at fair value in accordance with IFRS 3. Deferred taxes are provided on all of the temporary differences arising between the values assigned to identifiable assets and liabilities and their tax bases, subject to certain exceptions. The accounting treatment of income taxes in a business combination is addressed in detail in

chapter 14 of the PwC Manual of Accounting.

4.7 Comparative information in a reverse acquisition

If the transaction is accounted for as a capital reorganisation, the consolidated financial information for the SPAC will be presented as a continuation of the OpCo. In the year of the capital reorganisation, the comparative information presented in the consolidated financial statements of the SPAC should be that of the OpCo, and the historical financial information of the SPAC will not be included. Specifically:

- The assets and liabilities of the OpCo are recognised and measured in the consolidated financial statements at their pre-combination carrying amounts.

- The retained earnings and other equity balances recognised in the consolidated financial statements are those of the OpCo immediately before the reverse merger.

- The final equity structure (that is, the number and type of equity instruments issued) shown in the consolidated financial statements reflects the SPAC’s legal equity structure. The equity structure of the OpCo is used for the comparative period, and it is restated using the exchange ratio established in the reverse merger agreement to reflect the legal number of shares issued by the SPAC.

4.8 Earnings per share

The earnings per share calculations would be based on whether the arrangement is a business combination, and which entity is identified as the acquirer.

If the SPAC merger is a capital reorganisation, the earnings per share calculation would follow the one that is applied for a reverse acquisition. Therefore, the equity structure in the consolidated financial statements following the capital reorganisation reflects the equity structure of the SPAC, including the equity interests issued by the SPAC to effect the SPAC merger.

In calculating the weighted average number of ordinary shares outstanding (the denominator of the earnings per share calculation) during the period in which a reverse acquisition occurs:

- the number of ordinary shares outstanding, from the beginning of that period to the acquisition date, should be computed on the basis of the weighted average number of ordinary shares of the OpCo outstanding during the period multiplied by the exchange ratio established in the merger agreement; and

- the number of ordinary shares outstanding, from the acquisition date to the end of that period, should be the actual number of ordinary shares of the SPAC outstanding during that period.

If the SPAC is the accounting acquirer, it would apply acquisition accounting. Ordinary shares issued as part of the consideration transferred in a business combination are included in the weighted average number of shares from the acquisition date, because the acquirer incorporates into its statement of comprehensive income the acquiree's profits and losses from that date.

Any financial instruments or other contracts that might entitle their holder to ordinary shares in the future must be assessed, to determine if they are dilutive instruments or participating instruments. As mentioned in Section 4.4 above, the SPAC or the OpCo might enter into agreements with shareholders or employees, to issue additional shares after the transaction if specified targets are met. The possibility of ordinary shares being issued in future (these are called ‘contingently issuable ordinary shares’) could lead to an adjustment being required for diluted EPS purposes. Guidance in

paragraphs 52–57 of IAS 33 should be applied for contingently issuable ordinary shares, and in

paragraphs A13–A14 of IAS 33 for participating shares.

4.9 Accounting for shares and warrants issued in a merger