Search within this section

Select a section below and enter your search term, or to search all click IFRS In depths

Favorited Content

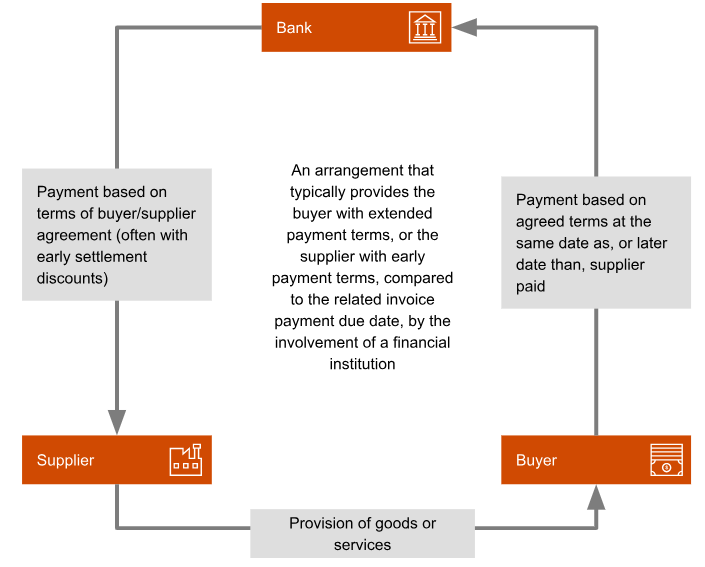

(1) to extend the buyer’s payment terms, by having a payment date to the bank later than the original due date of the invoice; |

(2) for the bank to act as the buyer’s paying agent, and to pay the buyer’s suppliers on its behalf on the date the payables are due; |

(3) to provide liquidity to the buyer’s suppliers seeking payment before the due date. |

PwC Observation |

|---|

Investors want to understand the size and key terms of supplier finance arrangements. It will be important for companies to take this into consideration when assessing whether these arrangements are material. |

What guidance? |

When was it issued? |

When does it apply? |

|---|---|---|

Supplier finance–how derecognition and presentation requirements apply

(IFRS Interpretations Committee agenda decision) |

December 2020 |

After December 2020 |

Supplier finance–disclosure requirements

(IASB amendments to IAS 7 and IFRS 7) |

May 2023 |

1 January 2024, with reliefs in the first year |

PwC Observation |

|---|

While analysing whether an arrangement is a supplier finance arrangement, it might be helpful to keep the following points in mind:

- The reporting requirements in this In depth are for the buyer (although there are typically three parties involved in these arrangements, including the buyer).

- Arrangements under which the buyer does not have a liability are not supplier finance arrangements.

- The arrangement has a financing purpose either for the buyer or the supplier.

The IASB had extensive discussions about the scope of the disclosures requirements for supplier finance arrangements. It decided to confine the scope to arrangements that finance amounts an entity owes its suppliers, and therefore concluded that an entity is not required to identify other actions its suppliers might have taken to finance their receivables (for example, factoring of receivables).

Paragraphs 31- 33 of the Basis for Conclusions on IAS 7 provide further information on the IASB’s rationale.

|

PwC Observation |

|---|

While the derecognition analysis should consider all the indicators mentioned in FAQ 44.101.1 in totality, some indicators might carry more weight than others – for example, the inclusion of jointly and severally liable or cross-default clauses or guarantees is an important indicator that the original trade payable should be derecognised.

|

PwC Observation |

|---|

When considering the classification and presentation of supplier finance arrangements in the statement of financial position and cash flow statement, entities should also consider the views of securities regulators in their respective jurisdictions.

For example, we understand that the US SEC staff’s view is that if the economic substance of the trade payable has changed as a result of a supplier finance arrangement, an in-substance financing will be deemed to have occurred. The trade payable should therefore be reclassified to debt on the balance sheet. In this situation, the US SEC’s staff position is that the reporting entity should reflect (impute) an operating cash outflow and financing cash inflow related to the affected trade payable.

Additionally, where the buyer does not reflect an operating cash outflow and a financing cash inflow (unlike the US SEC staff’s views described above), but presents the liabilities that are part of the supplier finance arrangement as finance payables, clear disclosures about this non-cash transfer should be provided. This is because non-cash transfers can have significant ramifications for the investor’s analysis of operating cash flows or free cash flows, and transparency on these transfers should be provided in the notes.

|

Statement of financial position |

|||

|---|---|---|---|

Balance as at:

|

1 January

Trade payable is recognised |

1 February

Trade payable becomes part of SFA |

31 May

Buyer pays finance provider |

Trade payable |

50 |

- |

- |

Short-term loan |

- |

50 |

- |

Cash flow statement |

||||

|---|---|---|---|---|

Cash flows recorded on: |

1 February

Trade payable becomes part of SFA |

31 March

Finance provider pays supplier |

31 May

Buyer pays finance provider |

Total for period ending 30 June |

Operating cash flows |

No cash flow exists- non-cash transfer |

-50 |

- |

-50 |

Financing cash flows |

+50 |

-50 |

- |

|

Total cash flows |

-50 |

|||

Cash flow statement |

||||

|---|---|---|---|---|

Cash flows recorded on: |

1 February

Trade payable becomes part of SFA |

31 March

Finance provider pays supplier |

31 May

Buyer pays finance provider |

Total for period ending 30 June |

Operating cash flows |

No cash flow exists- non-cash transfer |

A cash payment takes place, but it is not a cash flow for the buyer |

- |

- |

Financing cash flows |

-50 (*) |

-50 |

||

Total cash flows |

-50 |

|||

PwC Observation |

|---|

In this example, the timing of derecognition of the trade payable and recognition of a short term loan is different from the timing of occurrence of the cash flows in the cash flow statement. In practice, entities might apply a practical expedient and record a cash flow in the cash flow statement at the same date as the derecognition of the trade payable and the recognition of the short term loan. An entity might apply such a practical expedient when it reasonably expects that application of the expedient would not differ materially from the accounting demonstrated in the example above.

|

For reporting periods beginning before 1 January 2024, IFRS Accounting Standards do not provide explicit disclosure requirements for supplier finance arrangements. However, general disclosure requirements, including the requirements of IAS 1, apply and need to be considered. Entities need to apply judgement to decide the disclosure required for this period. The 2020 Committee agenda decision includes consideration in this regard.

|

PwC Observation |

|---|

The qualitative information can be presented on an aggregated basis when the characteristics of the arrangements are similar. Judgement might be required to assess whether a specific arrangement is dissimilar in nature to other arrangements. An arrangement would be dissimilar if it has unusual or unique terms and conditions. Examples of an arrangement that might be disaggregated could include a specific arrangement for one supplier with bespoke terms, such as an unusual interest rate, which a buyer might enter into in addition to other supplier finance arrangements with similar terms.

In addition, entities should consider whether the aggregation meets the objective of providing information about concentrations of liquidity risk with supplier finance providers. For example, consider a situation where there are five supplier finance arrangements that all have similar terms, but there is a significant concentration with a single provider amongst the five. In this case additional disclosure might be necessary to meet the requirements in paragraph 39(c) of IFRS 7 to provide information about management of liquidity risk, since concentrated funding sources are provided as an example of a liquidity risk factor in paragraph B11F(d) of IFRS 7 and also highlighted in paragraph IG18A(a)(iv) of IFRS 7.

|

PwC Observation |

|---|

Entities might face challenges initially in obtaining the information needed to disclose the carrying amounts for which suppliers have already been paid, and in setting up appropriate controls over the completeness and accuracy of that information. Entities should engage with their finance provider as soon as possible to ensure that they have access to the information needed on a timely basis and are able to put in place appropriate processes and controls over that information. |

PwC Observation |

|---|

The disclosure of non-cash changes is a critical element of the disclosure requirements. When the IASB developed these requirements, it received a clear message from investors that they need information to understand the impact of supplier finance arrangements on an entity’s cash flows. Without specific disclosures about non-cash changes, the cash flow impact would not always be apparent. |

Note X-Supplier Finance Arrangements |

|||

|---|---|---|---|

A |

The entity entered into arrangements with the following terms and conditions:

|

||

Carrying amount of liabilities

|

Reporting date 20X5

|

Reporting date 20X4

|

|

Presented within trade and other payables |

CU1,500

|

CU1,000

|

|

|

CU1,050

|

CU800

|

|

B |

Presented within finance payables

|

CU1,000

|

CU750

|

|

CU900

|

CU650

|

|

Range of payment due dates |

|||

C |

Liabilities that are part of the arrangement

|

85–90 days after invoice date

|

80–90 days after invoice date

|

Comparable trade payables that are not part of an arrangement

|

60–70 days after invoice date

|

60–65 days after invoice date

|

|

D |

Non-cash changes

|

||

There were no material business combinations or foreign exchange differences in either period. There were non-cash transfers from trade payables to finance payables of CU1,200 and CU900 in 20X2 and 20X1.

|

|||

PwC Observation |

|---|

The liquidity risk disclosures should consider:

|

© #year# PricewaterhouseCoopers LLP. This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under licence.

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP, its subsidiaries or affiliates.

Select a section below and enter your search term, or to search all click IFRS In depths