Search within this section

Select a section below and enter your search term, or to search all click IFRS In depths

Favorited Content

Example 1 – Seller-lessee accounting for a right-of-use asset and lease liability at the commencement date in a sale and leaseback transaction with variable lease payments that do not depend on an index or a rate

|

|||

|---|---|---|---|

An entity (seller-lessee) sells a building to another entity (buyer-lessor) for cash of C1,800,000 (the fair value of the building at the date of sale). Immediately before the transaction, the building is carried at a cost of C1,000,000.

At the same time, the seller-lessee enters into a contract with the buyer-lessor for the right to use the building for an initial period of five years.

Lease payments (which are at market rates), payable annually, comprise fixed payments and variable payments that do not depend on an index or a rate.

The terms and conditions of the transaction are such that the transfer of the building by the seller-lessee satisfies the requirements of IFRS 15 to be accounted for as a sale of the building. Accordingly, the seller-lessee accounts for the transaction as a sale and leaseback.

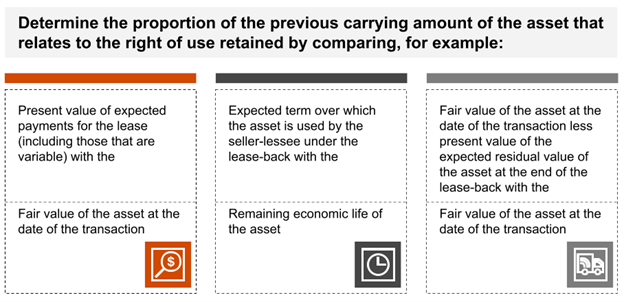

Determining the proportion of the right of use retained

Applying paragraph 100(a) of IFRS 16, the seller-lessee is required to determine the proportion of the building transferred to the buyer-lessor that relates to the right of use that it retains. Paragraph 100(a) does not prescribe a particular method for determining that proportion.

The seller-lessee could determine this proportion by comparing, for example, the present value of expected payments for the lease (including those that are variable) with the fair value of the building at the date of the transaction. Assume that the seller-lessee estimates the expected payments over the lease term, and it discounts those expected payments using the incremental borrowing rate (since the rate implicit in the lease cannot be readily determined), resulting in a present value of the expected payments for the lease of C450,000. In this example, the proportion of the building that relates to the right of use retained is 25%, calculated as C450,000 (that is, the present value of expected payments for the lease) divided by C1,800,000 (that is, the fair value of the building).

Examples of other possible methods that might be appropriate, depending on the facts and circumstances, include:

Under all of the approaches, the lease liability is the balancing figure based on the amount of gain that can be recognised.

Determining the gain on rights transferred

If, for example, the seller-lessee determines that the proportion of the building transferred to the buyer-lessor that relates to the right of use that it retains is 25%, at the commencement date, the seller-lessee accounts for the transaction as follows.

|

|||

Cash |

C1,800,000 |

||

Right-of-use asset (C1,000,000 × 25%) |

C250,000 |

||

Building |

C1,000,000 |

||

Lease liability |

C450,000 |

||

Gain on rights transferred ((C1,800,000 – C1,000,000) × 75%) |

C600,000 |

||

Example 2 – Subsequent measurement of a right-of-use asset and lease liability in a sale and leaseback transaction with variable lease payments that do not depend on an index or a rate |

|||||||

|---|---|---|---|---|---|---|---|

The facts are the same as in Example 1. In addition, the interest rate implicit in the lease cannot be readily determined. The seller-lessee’s incremental borrowing rate is 3% per annum.

The seller-lessee expects to consume the right-of-use asset’s future economic benefits evenly over the lease term, and so it depreciates the right-of-use asset on a straight-line basis.

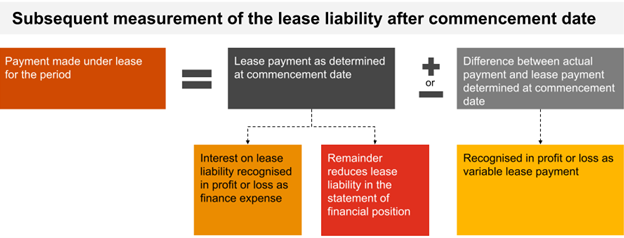

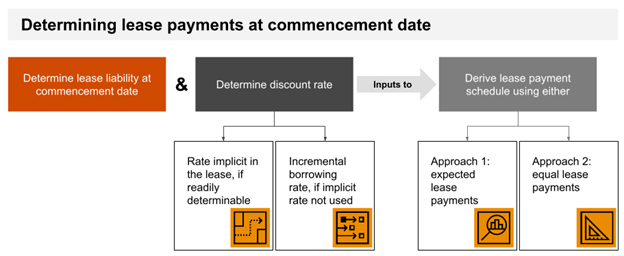

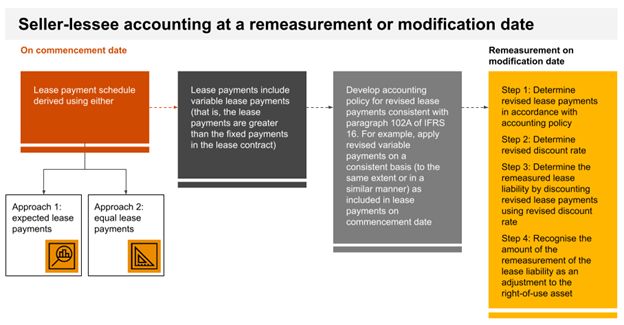

In subsequently measuring the lease liability, the seller-lessee develops an accounting policy for determining ‘lease payments’ in a way that it would not recognise any amount of the gain that relates to the right of use that it retains. Depending on the circumstances and the method that the seller-lessee used for determining the measurement of the right-of-use asset and the gain recognised on the transaction at the commencement date (see Example 1), either Approach 1 or Approach 2 described below could meet the requirements in paragraph 102A. Paragraph 102A of IFRS 16 requires the seller-lessee to determine ‘lease payments’ or ‘revised lease payments’ in a way that it would not recognise any amount of the gain or loss that relates to the right of use retained by the seller-lessee.

Approach 1: Expected lease payments at the commencement date

The seller-lessee determines ‘lease payments’ to reflect the timing and amount of the expected lease payments at the commencement date. These payments, when discounted using the entity’s incremental borrowing rate, result in the carrying amount of the lease liability at that date of C450,000. Under this approach, the seller-lessee reduces the carrying amount of the lease liability with ‘lease payments’ that reflect the expected lease payments estimated at the commencement date. The lease liability is not remeasured to account for changes in the lessee’s expectations for future lease payments subsequent to the commencement date.

The lease liability and the right-of-use asset recognised over the leaseback term would be:

|

|||||||

Lease liability |

Right-of-use asset |

||||||

Year |

Beginning balance |

Lease payments |

Interest expense (3%) |

Ending balance |

Beginning balance |

Depreciation charge |

Ending balance |

C |

C |

C |

C |

C |

C |

C |

|

1 |

450,000 |

(95,902) |

13,500 |

367,598 |

250,000 |

(50,000) |

200,000 |

2 |

367,598 |

(98,124) |

11,028 |

280,502 |

200,000 |

(50,000) |

150,000 |

3 |

280,502 |

(99,243) |

8,415 |

189,674 |

150,000 |

(50,000) |

100,000 |

4 |

189,674 |

(100,101) |

5,690 |

95,263 |

100,000 |

(50,000) |

50,000 |

5 |

95,263 |

(98,121) |

2,858 |

0 |

50,000 |

(50,000) |

0 |

The seller-lessee recognises, in profit and loss, the difference between the payments actually due under the lease and the lease payments that reduce the carrying amount of the lease liability. For example, if the seller-lessee pays C99,321 for the use of the building in Year 2, it recognises C1,197 (C99,321 – C98,124) in profit or loss for that year.

This approach might be challenging to apply if the proportion of the rights retained by the seller-lessee was calculated using a method other than one that determines the present value of expected payments for the lease – for example, where the right-of-use asset at the commencement date is determined by comparing the expected term over which the asset is used by the seller-lessee under the leaseback with the remaining economic life of the asset (see Example 1).

Approach 2: Equal lease payments over the lease term

An alternative approach is for the seller-lessee to determine ‘lease payments’ to reflect equal periodic payments over the lease term that, when discounted using its incremental borrowing rate, result in the carrying amount of the lease liability at the commencement date of C450,000. Under this approach, the seller-lessee reduces the carrying amount of the lease liability by the ‘lease payments’ that reflect the equal periodic payments over the lease term.

The lease liability and the right-of-use asset recognised over the leaseback term would be:

|

|||||||

Lease liability |

Right-of-use asset |

||||||

Year |

Beginning balance |

Lease payments |

Interest expense (3%) |

Ending balance |

Beginning balance |

Depreciation charge |

Ending balance |

C |

C |

C |

C |

C |

C |

C |

|

1 |

450,000 |

(98,260) |

13,500 |

365,240 |

250,000 |

(50,000) |

200,000 |

2 |

365,240 |

(98,260) |

10,957 |

277,938 |

200,000 |

(50,000) |

150,000 |

3 |

277,938 |

(98,260) |

8,338 |

188,017 |

150,000 |

(50,000) |

100,000 |

4 |

188,017 |

(98,260) |

5,641 |

95,398 |

100,000 |

(50,000 |

50,000 |

5 |

95,398 |

(98,260) |

2,862 |

0 |

50,000 |

(50,000) |

0 |

The seller-lessee recognises, in profit and loss, the difference between the payments actually made for the lease and the lease payments that reduce the carrying amount of the lease liability. For example, if the seller-lessee pays C99,321 for the use of the building in Year 2, it recognises C1,061 (C99,321 – C98,260) in profit or loss.

|

|||||||

Example 3 – Accounting by a seller-lessee for remeasurement/modification subsequent to the commencement date where the expected lease payment approach is applied to subsequently measure the lease liability

|

|||||||

|---|---|---|---|---|---|---|---|

The facts are the same as in Example 1. In addition:

The proportion of the building transferred to the buyer-lessor that relates to the right of use that it retains was determined to be 25% by comparing the present value of expected payments for the lease, including those that are variable (which equals C450,000), with the fair value of the building at the date of the transaction. A lease liability of C450,000 is recognised at the commencement date which is determined as a balancing figure.

The seller-lessee elects to determine ‘lease payments’ to reflect the timing and amount of the expected lease payments at the commencement date. These payments, when discounted using the entity’s incremental borrowing rate, result in the carrying amount of the lease liability at that date of CU450,000. Under this approach, the seller-lessee reduces the carrying amount of the lease liability with ‘lease payments’ that reflect the expected lease payments estimated at the commencement date.

At the commencement date:

|

|||||||

Year |

Estimated revenue |

Estimated variable lease payment (1% of estimated revenue) |

Fixed lease payment |

Total expected lease payments |

|||

C |

C |

C |

C |

||||

1 |

4,590,200 |

45,902 |

50,000 |

95,902 |

|||

2 |

4,812,400 |

48,124 |

50,000 |

98,124 |

|||

3 |

4,924,300 |

49,243 |

50,000 |

99,243 |

|||

4 |

5,010,100 |

50,101 |

50,000 |

100,101 |

|||

5 |

4,812,100 |

48,121 |

50,000 |

98,121 |

|||

The lease liability and the right-of-use asset recognised over the leaseback term would be:

|

|||||||

Lease liability |

Right-of-use asset |

||||||

Year |

Beginning balance |

Lease payments |

Interest expense (3%) |

Ending balance |

Beginning balance |

Depreciation charge |

Ending balance |

C |

C |

C |

C |

C |

C |

C |

|

1 |

450,000 |

(95,902) |

13,500 |

367,598 |

250,000 |

(50,000) |

200,000 |

2 |

367,598 |

(98,124) |

11,028 |

280,502 |

200,000 |

(50,000) |

150,000 |

3 |

280,502 |

(99,243) |

8,415 |

189,674 |

150,000 |

(50,000) |

100,000 |

4 |

189,674 |

(100,101) |

5,690 |

95,263 |

100,000 |

(50,000) |

50,000 |

5 |

95,263 |

(98,121) |

2,858 |

0 |

50,000 |

(50,000) |

0 |

The lease payments at the commencement date include variable lease payments that do not depend on an index or a rate, because the lease payments per annum exceed the fixed lease payment of C50,000 per annum.

Scenario 1: Change in lease term at the end of the first year of the lease

At the end of the first year of the lease, a significant change in circumstances, that is within the lessee’s control, occurs in the lessee’s business that indicates that the lessee is reasonably certain to exercise the extension option. The lessee reassesses the extension option in accordance with paragraph 20 of IFRS 16 and determines that the remaining lease term is six years.

Assume that the revised discount rate (the seller-lessee’s incremental borrowing rate) at the remeasurement date is 7.5%.

To be consistent with the measurement of the lease liability at the commencement date, both fixed lease payments and variable lease payments that do not depend on an index or a rate are included in ‘revised lease payments’ and are discounted using the revised discount rate.

At the remeasurement date:

At the end of the first year, the seller-lessee’s expectation of revenue over the remaining lease term has changed. The seller-lessee used its revised estimates of revenue at the remeasurement date to calculate its expected ‘revised lease payments'.

|

|||||||

Year |

Revised estimated revenue |

Revised estimated variable lease payment (1% of estimated revenue) |

Fixed lease payment |

Total revised expected lease payments |

|||

C |

C |

C |

C |

||||

2 |

4,331,160 |

43,312 |

50,000 |

93,312 |

|||

3 |

4,431,870 |

44,319 |

50,000 |

94,319 |

|||

4 |

4,509,090 |

45,091 |

50,000 |

95,091 |

|||

5 |

4,330,890 |

43,309 |

50,000 |

93,309 |

|||

6 |

4,200,000 |

42,000 |

50,000 |

92,000 |

|||

7 |

4,100,000 |

41,000 |

50,000 |

91,000 |

|||

Since both fixed lease payments and expected variable lease payments that do not depend on an index or a rate are included in ‘revised lease payments’ and discounted using the revised discount rate, the remeasured lease liability would be C437,881 (calculated by discounting the ‘total revised lease payments’, as determined in the table above using the revised discount rate of 7.5%) at the remeasurement date. |

|||||||

Lease liability |

|||||||

Year |

Beginning balance |

Revised lease payments |

Interest expense (7.5%) |

Ending balance |

|||

C |

C |

C |

C |

||||

2 |

437,881 |

(93,312) |

32,841 |

377,410 |

|||

3 |

377,410 |

(94,319) |

28,306 |

311,397 |

|||

4 |

311,397 |

(95,091) |

23,355 |

239,661 |

|||

5 |

239,661 |

(93,309) |

17,975 |

164,327 |

|||

6 |

164,327 |

(92,000) |

12,324 |

84,651 |

|||

7 |

84,651 |

(91,000) |

6,349 |

0 |

|||

The remeasurement of the lease liability would be recognised as follows:

|

|||||||

Right-of-use asset |

C70,283 |

||||||

Lease liability (C437,881 – C367,598) |

C70,283 |

||||||

Scenario 2: Lease modification at the end of the first year of the lease; change in lease consideration with no change in scope

At the end of the first year, the lease is amended such that the fixed lease payment is modified to C75,000 a year for the remaining lease term, and the variable lease payment is 0.5% of the seller-lessee’s revenue for the remainder of the lease term.

Assume that the revised discount at the modification date is 7.5%.

Consistent with the commencement date, both fixed lease payments and variable lease payments are included in ‘revised lease payments’ and are discounted using the revised discount rate.

At the modification date:

At the end of the first year, the seller-lessee’s expectation of revenue over the remaining lease term has changed. The seller-lessee used its revised estimates of revenue at the modification date to calculate its expected ‘revised lease payments’.

|

|||||||

Year |

Revised estimated revenue |

Revised estimated variable lease payment (0.5% of estimated revenue) |

Fixed lease payment |

Total revised expected lease payments |

|||

C |

C |

C |

C |

||||

2 |

4,331,160 |

21,656 |

75,000 |

96,656 |

|||

3 |

4,431,870 |

22,159 |

75,000 |

97,159 |

|||

4 |

4,509,090 |

22,545 |

75,000 |

97,545 |

|||

5 |

4,330,890 |

21,654 |

75,000 |

96,654 |

|||

If both fixed lease payments and variable lease payments that do not depend on an index or a rate are included in ‘revised lease payments’ and discounted using the revised discount rate, the remeasured lease liability would be C324,883 (calculated by discounting the ‘total revised lease payments’, as determined in the table above using the revised discount rate of 7.5%) at the modification date:

|

|||||||

Lease liability |

|||||||

Year |

Beginning balance |

Revised lease payments |

Interest expense (7.5%) |

Ending balance |

|||

C |

C |

C |

C |

||||

2 |

324,883 |

(96,656) |

24,366 |

252,593 |

|||

3 |

252,593 |

(97,159) |

18,944 |

174,378 |

|||

4 |

174,378 |

(97,545) |

13,078 |

89,911 |

|||

5 |

89,911 |

(96,654) |

6,743 |

0 |

|||

The remeasurement of the lease liability would be recognised as follows: |

|||||||

Lease liability (C367,598 – C324,883) |

C42,715 |

||||||

Right-of-use asset |

C42,715 |

||||||

While this results in a lower lease liability and right-of-use asset (and reduced depreciation expense going forward), the treatment complies with the sale and leaseback amendments, since it does not reflect any recognition of a gain on the right of use retained by the seller-lessee. This is because the reduction in the lease liability is due to the increase in the discount rate since the commencement date and the reduction in estimated revenue over the lease term.

Conversely, if the seller-lessee did not include any amount for variable lease payments within the revised lease payments on the remeasurement date and, consequently, a larger adjustment was recognised to reduce the lease liability and right-of-use asset, we believe that this incremental adjustment would not be considered to comply with the sale and leaseback amendments, because it results from measuring the lease liability on an inconsistent basis at the remeasurement date compared to the commencement date.

|

|||||||

© #year# PricewaterhouseCoopers LLP. This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under licence.

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP, its subsidiaries or affiliates.

Select a section below and enter your search term, or to search all click IFRS In depths