Search within this section

Select a section below and enter your search term, or to search all click Sustainability reporting guide

Favorited Content

Entities in scope of CSRD |

Relevant section |

Applicable standards |

|---|---|---|

Excerpt from Accounting Directive Article 2(5)

‘Net turnover’ means the amounts derived from the sale of products and the provision of services after deducting sales rebates and value added tax and other taxes directly linked to turnover

Excerpt from the Accounting Directive Article 2

Size criteria |

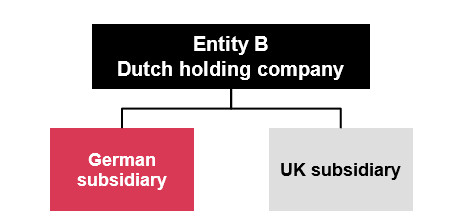

German sub |

UK sub |

Entity B consolidated |

|

|---|---|---|---|---|

20x3

|

||||

Balance sheet total

|

€1

|

€8

|

€1

|

€10

|

Net turnover

|

-

|

€52

|

€8

|

€60

|

Average number of employees

|

20

|

270

|

60

|

350

|

20x4

|

||||

Balance sheet total

|

€1

|

€11

|

€3

|

€15

|

Net turnover

|

-

|

€60

|

€15

|

€75

|

Average number of employees

|

20

|

280

|

100

|

400

|

Excerpt from the Transparency Directive Article 2(1)(d)

‘Issuer’ means a natural person, or a legal entity governed by private or public law, including a State, whose securities are admitted to trading on a regulated market. In the case of depository receipts admitted to trading on a regulated market, the issuer means the issuer of the securities represented, whether or not those securities are admitted to trading on a regulated market

Excerpt from the Markets in Financial Instruments Directive Article 4(1)(21)

‘Regulated market’ means a multilateral system operated and/or managed by a market operator, which brings together or facilitates the bringing together of multiple third-party buying and selling interests in financial instruments – in the system and in accordance with its non-discretionary rules – in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly and in accordance with Title III of this Directive;

Micro- undertakings |

Small undertakings |

Medium-sized undertakings |

|

|---|---|---|---|

Balance sheet total

|

€450 thousand

|

€5 million

|

€25 million

|

Net turnover

|

€900 thousand

|

€10 million

|

€50 million

|

Average number of employees during the financial year

|

10 employees

|

50 employees

|

250 employees

|

Excerpt from Accounting Directive Article 2(5)

‘Net turnover’ means … the revenue as defined by or within the meaning of the financial reporting framework on the basis of which the financial statements of the undertaking are prepared

Revenue in million € |

US Parent |

Italy sub |

UK sub |

US Parent consolidated |

|---|---|---|---|---|

20x7

|

||||

Sales to German customers

|

-

|

-

|

€30

|

€30

|

Sales to French customers

|

-

|

€105

|

-

|

€105

|

Sales to US customers

|

-

|

€50

|

-

|

€50

|

Total

|

-

|

€155

|

€30

|

€185

|

20x8

|

||||

Sales to German customers

|

-

|

-

|

€50

|

€50

|

Sales to French customers

|

-

|

€110

|

-

|

€110

|

Sales to US customers

|

-

|

€50

|

-

|

€50

|

Total

|

€160

|

€50

|

€210

|

Excerpt from the Insurance Directive Article 35:

Entities subject to CSRD |

First-time application date |

Relevant section |

|---|---|---|

Entities subject to the current NFRD requirements

|

Reporting on financial years beginning on or after 1 January 2024

|

|

‘Large’ non-EU entities that are (1) listed and (2) have more than 500 employees

|

Reporting on financial years beginning on or after 1 January 2024

|

|

‘Large’ EU undertakings that are (1) listed and (2) have more than 500 employees

|

Reporting on financial years beginning on or after 1 January 2024

|

|

All other ‘large’ EU undertakings and EU undertakings that are parents of a ‘large’ group

|

Reporting on financial years beginning on or after 1 January 2025

|

|

Certain small and non-complex credit institutions, captive insurance entity and captive reinsurance entity

|

Reporting on financial years beginning on or after 1 January 2026

|

|

Listed SMEs

|

Reporting on financial years beginning on or after 1 January 2026, with an optional deferral by two years (to 1 January 2028)

|

|

Non-EU entities with significant activities in the EU

|

Reporting on financial years beginning on or after 1 January 2028

|

© #year# PricewaterhouseCoopers LLP. This content is copyright protected. It is for your own use only - do not redistribute. These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under licence.

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP, its subsidiaries or affiliates.

Select a section below and enter your search term, or to search all click Sustainability reporting guide