7. Amend paragraph 205-20-05-1 and add paragraph 205-20-05-2, with a link to transition paragraph 205-20-65-1, as follows:

Presentation of Financial Statements—Discontinued Operations

Overview and Background

205-20-05-1 This Subtopic provides guidance on

the presentation and disclosure requirements for discontinued operations. A discontinued operation may include a component of an entity or a group of components of an entity, or a business or nonprofit activity.

when the results of operations of a component of an entity that either has been disposed of or is classified as held for sale would be reported as a discontinued operation in the financial statements of the entity. It also addresses the allocation of interest and overhead to discontinued operations. Subtopic 360-10 establishes held for sale criteria in paragraphs 360-10-45-9 through 45-14.

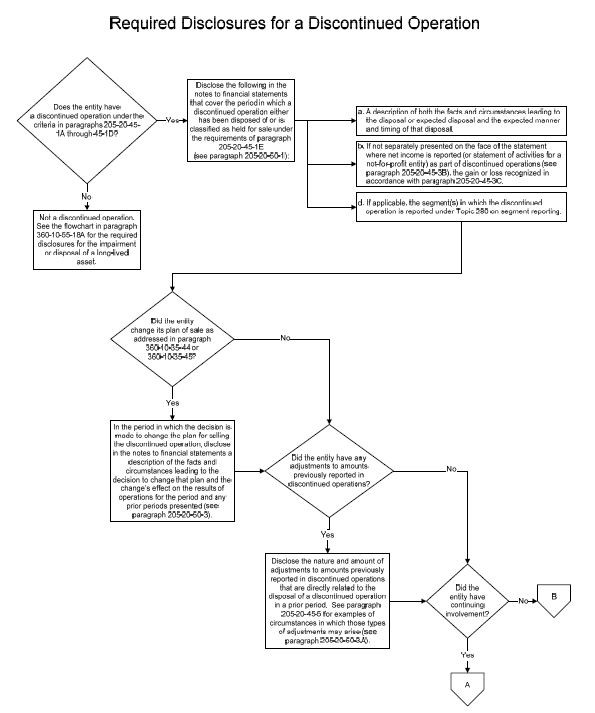

205-20-05-2 The required disclosures about discontinued operations vary depending on the nature of the discontinued operation. For example, if a discontinued operation includes a component or group of components of an entity that is not an equity method investment, a more comprehensive set of disclosures about the discontinued operation is required. If the discontinued operation includes an equity method investment, or a business or nonprofit activity that is classified as held for sale on acquisition, a more limited set of disclosures is required (see the flowchart in paragraph 205-20-55-82 for an illustration).

8. Amend paragraphs 205-20-15-1 through 15-2 and add paragraph 205-20-15-3 and its related heading, with a link to transition paragraph 205-20-65-1, as follows:

Scope and Scope Exceptions

> Overall Guidance

205-20-15-1 This Subtopic follows the same Scope and Scope Exceptions as outlined in

both

the Overall Subtopic; see Section 205-10-15,

and paragraph 360-10-15-5,

with specific transaction qualifications noted below.

> Transactions

205-20-15-2 The guidance in this Subtopic applies to

either of the following

transactions and activities

:

- A component

Components

of an entity or a group of components of an entity that is disposed of or is classified as held for sale that have been disposed of, or alternatively, have been classified as held for sale under the requirements of paragraph 360-10-45-9

.

- A business or nonprofit activity that, on acquisition, is classified as held for sale.

> Entities

205-20-15-3 The guidance in this Subtopic does not apply to oil and gas properties that are accounted for using the full-cost method of accounting as prescribed by the U.S. Securities and Exchange Commission (SEC) (see Regulation S-X, Rule 4-10, Financial Accounting and Reporting for Oil and Gas Producing Activities Pursuant to the Federal Securities Laws and the Energy Policy and Conservation Act of 1975).

9. Supersede paragraphs 205-20-45-1 through 45-2 and their related heading, amend paragraph 205-20-45-3 and add its related heading, and add paragraphs 205-20-45-1A through 45-1G and their related headings and 205-20-45-3A through 45-3C, with a link to transition paragraph 205-20-65-1, as follows:

Other Presentation Matters

> Reporting Discontinued Operations

205-20-45-1 Paragraph superseded by Accounting Standards Update 2014-08.The results of operations of a component of an entity that either has been disposed of or is classified as held for sale under the requirements of paragraph 360-10-45-9, shall be reported in discontinued operations in accordance with paragraph 205-20-45-3 if both of the following conditions are met:

The operations and cash flows of the component have been (or will be) eliminated from the ongoing operations of the entity as a result of the disposal transaction.

The entity will not have any significant continuing involvement in the operations of the component after the disposal transaction.

> What Is a Discontinued Operation?

205-20-45-1A A discontinued operation may include a component of an entity or a group of components of an entity, or a business or nonprofit activity.

> > A Discontinued Operation Comprising a Component or a Group of Components of an Entity

205-20-45-1B A disposal of a component of an entity or a group of components of an entity shall be reported in discontinued operations if the disposal represents a strategic shift that has (or will have) a major effect on an entity’s operations and financial results when any of the following occurs:

- The component of an entity or group of components of an entity meets the criteria in paragraph 205-20-45-1E to be classified as held for sale.

- The component of an entity or group of components of an entity is disposed of by sale.

- The component of an entity or group of components of an entity is disposed of other than by sale in accordance with paragraph 360-10-4515 (for example, by abandonment or in a distribution to owners in a spinoff).

205-20-45-1C Examples of a strategic shift that has (or will have) a major effect on an entity’s operations and financial results could include a disposal of a major geographical area, a major line of business, a major equity method investment, or other major parts of an entity (see paragraphs 205-20-55-83 through 55-101 for Examples).

> > A Discontinued Operation Comprising a Business or Nonprofit Activity

205-20-45-1D A business or nonprofit activity that, on acquisition, meets the criteria in paragraph 205-20-45-1E to be classified as held for sale is a discontinued operation.

> > Initial Criteria for Classification of Held for Sale

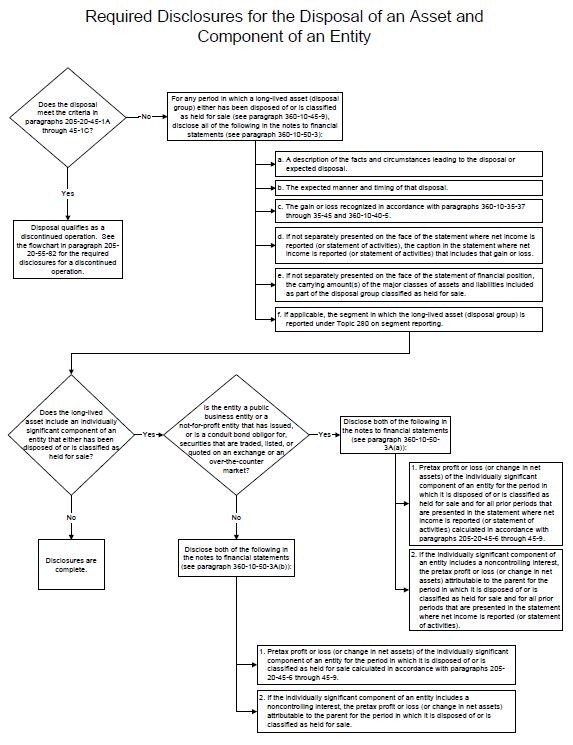

205-20-45-1E A component of an entity or a group of components of an entity, or a business or nonprofit activity (the entity to be sold), shall be classified as held for sale in the period in which all of the following criteria are met:

- Management, having the authority to approve the action, commits to a plan to sell the entity to be sold.

- The entity to be sold is available for immediate sale in its present condition subject only to terms that are usual and customary for sales of such entities to be sold. (See Examples 5 through 7 [paragraphs 360-10-55-37 through 55-42], which illustrate when that criterion would be met.)

- An active program to locate a buyer or buyers and other actions required to complete the plan to sell the entity to be sold have been initiated.

- The sale of the entity to be sold is {add link to 2nd definition}probable{add link to 2nd definition}, and transfer of the entity to be sold is expected to qualify for recognition as a completed sale, within one year, except as permitted by paragraph 205-20-45-1G.(See Example 8 [paragraph 360-10-55-43], which illustrates when that criterion would be met.)

- The entity to be sold is being actively marketed for sale at a price that is reasonable in relation to its current fair value. The price at which an entity to be sold is being marketed is indicative of whether the entity currently has the intent and ability to sell the entity to be sold. A market price that is reasonable in relation to fair value indicates that the entity to be sold is available for immediate sale, whereas a market price in excess of fair value indicates that the entity to be sold is not available for immediate sale.

- Actions required to complete the plan indicate that it is unlikely that significant changes to the plan will be made or that the plan will be withdrawn.

205-20-45-1F If at any time the criteria in paragraph 205-20-45-1E are no longer met (except as permitted by paragraph 205-20-45-1G), an entity to be sold that is classified as held for sale shall be reclassified as held and used and measured in accordance with paragraph 360-10-35-44.

205-20-45-1G Events or circumstances beyond an entity’s control may extend the period required to complete the sale of an entity to be sold beyond one year. An exception to the one-year requirement in paragraph 205-20-45-1E(d) shall apply in the following situations in which those events or circumstances arise:

a. If at the date that an entity commits to a plan to sell an entity to be sold, the entity reasonably expects that others (not a buyer) will impose conditions on the transfer of the entity to be sold that will extend the period required to complete the sale and both of the following conditions are met:

1. Actions necessary to respond to those conditions cannot be initiated until after a firm purchase commitment is obtained.

2. A firm purchase commitment is probable within one year. (See Example 9 [paragraph 360-10-55-44], which illustrates that situation.)

b. If an entity obtains a firm purchase commitment and, as a result, a buyer or others unexpectedly impose conditions on the transfer of an entity to be sold previously classified as held for sale that will extend the period required to complete the sale and both of the following conditions are met:

1. Actions necessary to respond to the conditions have been or will be timely initiated.

2. A favorable resolution of the delaying factors is expected. (See Example 10 [paragraph 360-10-55-46], which illustrates that situation.)

c. If during the initial one-year period, circumstances arise that previously were considered unlikely and, as a result, an entity to be sold previously classified as held for sale is not sold by the end of that period and all of the following conditions are met:

1. During the initial one-year period, the entity initiated actions necessary to respond to the change in circumstances.

2. The entity to be sold is being actively marketed at a price that is reasonable given the change in circumstances.

3. The criteria in paragraph 205-20-45-1E are met. (See Example 11 [paragraph 360-10-55-48], which illustrates that situation.)

205-20-45-2 Paragraph superseded by Accounting Standards Update 2014-08. Examples 1 through 9 (see paragraphs 205-20-55-28 through 55-79) illustrate disposal activities that do or do not qualify for reporting as discontinued operations.

> Statement in Which Net Income Is Reported

205-20-45-3 In a period in which a component of an entity either has been disposed of or is classified as held for sale, the

The statement in which net income

statement

of a business entity

is reported or

the statement of activities of a not-for-profit entity (NFP) for current and prior periods shall report the results of operations of the

discontinued operationcomponent

, including any gain or loss recognized in accordance with

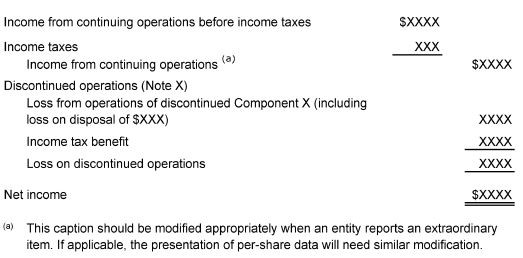

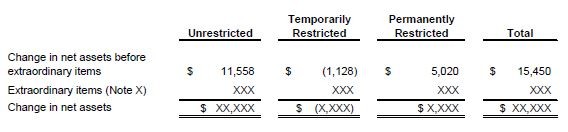

paragraph 205-20-45-3C, in the period in which a discontinued operation either has been disposed of or is classified as held for sale.paragraphs 360-10-35-40 and 360-10-40-5, in discontinued operations. The results of operations of a component classified as held for sale shall be reported in discontinued operations in the period(s) in which they occur. The results of discontinued operations, less applicable income taxes (benefit), shall be reported as a separate component of income before extraordinary items (if applicable). For example, the results of discontinued operations may be reported in the income statement of a business entity as follows.

A gain or loss recognized on the disposal shall be disclosed either on the face of the income statement or in the notes to financial statements (see paragraph 205-20-50-1(b)).

[Content amended and moved to paragraphs 205-20-45-3A and 205-20-45-3B] 205-20-45-3A The results of

all discontinued operations, less applicable income taxes (benefit), shall be reported as a separate component of income before extraordinary items (if applicable). For example, the results of

all discontinued operations may be reported in the

income

statement

where net income of a business entity

is reported as follows.

[Note: For ease of readability, the new table is not underlined. ]

[Content amended as shown and moved from paragraph 205-20-45-3]

205-20-45-3B A gain or loss recognized on the disposal

(or loss recognized on classification as held for sale) shall be

disclosed either

presented separately on the face of the

income

statement

where net income is reported or

disclosed in the notes to financial statements (see paragraph 205-20-50-1(b)).

[Content amended as shown and moved from paragraph 205-20-45-3]

205-20-45-3C A gain or loss recognized on the disposal (or loss recognized on classification as held for sale) of a discontinued operation shall be calculated in accordance with the guidance in other Subtopics. For example, if a discontinued operation is within the scope of Topic 360 on property, plant, and equipment, an entity shall follow the guidance in paragraphs 360-10-35-37 through 35-45 and 360-10-40-5 for calculating the gain or loss recognized on the disposal (or loss on classification as held for sale) of the discontinued operation.

10. Amend paragraphs 205-20-45-4 through 45-5 and 205-20-45-10 and its related heading and add paragraph 205-20-45-11, with a link to transition paragraph 205-20-65-1, as follows:

205-20-45-4 Adjustments to amounts previously reported in discontinued operations

that are directly related to the disposal of a component of an entity

in a prior period shall be

presentedclassified

separately in the current period in

the discontinued operations

section of the statement where net income is reported.

205-20-45-5 Examples of circumstances in which those types of adjustments may arise include the following:

- The resolution of contingencies that arise pursuant to the terms of the disposal transaction, such as the resolution of purchase price adjustments and indemnification issues with the purchaser

- The resolution of contingencies that arise from and that are directly related to the operations of the

component prior to

discontinued operation before its disposal, such as environmental and product warranty obligations retained by the seller

- The settlement of employee benefit plan obligations (pension, postemployment benefits other than pensions, and other postemployment benefits), provided that the settlement is directly related to the disposal transaction. A settlement is directly related to the disposal transaction if there is a demonstrated direct cause-and-effect relationship and the settlement occurs no later than one year following the disposal transaction, unless it is delayed by events or circumstances beyond an entity’s control (see paragraph 205-20-45-1G

360-10-45-11

).

> Disposal Group Classified as Held for Sale

Statement of Financial Position

205-20-45-10 The assets and liabilities of a disposal group

In the period(s) that a discontinued operation is classified as held for sale

and for all prior periods presented, the assets and liabilities of the discontinued operation shall be presented separately in the asset and liability sections, respectively, of the statement of financial position. Those assets and liabilities shall not be offset and presented as a single amount.

If a discontinued operation is part of a disposal group that includes other assets and liabilities that are not part of the discontinued operation, an entity may present the assets and liabilities of the disposal group separately in the asset and liability sections, respectively, of the statement of financial position. If a discontinued operation is disposed of before meeting the criteria in paragraph 205-20-45-1E to be classified as held for sale, an entity shall present the assets and liabilities of the discontinued operation separately in the asset and liability sections, respectively, of the statement of financial position for the periods presented in the statement of financial position before the period that includes the disposal. When an entity separately presents in prior periods the assets and liabilities of a discontinued operation, the entity shall not apply the guidance in paragraph 360-10-35-43 as if those assets and liabilities were held for sale in those prior periods.The major classes of assets and liabilities classified as held for sale shall be separately disclosed either on the face of the statement of financial position or in the notes to financial statements (see paragraph 205-20-50-1(a)).

205-20-45-11 For any discontinued operation initially classified as held for sale in the current period, an entity shall either present on the face of the statement of financial position or disclose in the notes to financial statements (see paragraph 205-20-50-5B(e)) the major classes of assets and liabilities of the discontinued operation classified as held for sale for all periods presented in the statement of financial position. Any loss recognized on a discontinued operation classified as held for sale in accordance with paragraphs 205-20-45-3B through 45-3C shall not be allocated to the major classes of assets and liabilities of the discontinued operation.

11. Amend paragraphs 205-20-50-1 and its related heading and 205-20-50-3; supersede paragraphs 205-20-50-2 and its related heading, 205-20-50-4 and amend its related heading, and 250-20-50-5 and its related heading; and add paragraphs 205-20-50-3A and its related heading and 205-20-50-4A through 50-4B, with a link to transition paragraph 205-20-65-1, as follows:

Disclosure

> Assets Sold or Held for Sale

Disclosures Required for All Types of Discontinued Operations

205-20-50-1 The following shall be disclosed in the notes to financial statements that cover the period in which a

discontinued operation long-lived asset (disposal group)

either has been

disposed ofsold

or is classified as held for sale under the requirements of paragraph

205-20-45-1E360-10-45-9

:

a. A description of both of the following:

1.

the

The facts and circumstances leading to the

disposal or expected

disposaldisposal,

2.

the

The expected manner and timing of that

disposal. disposal, and, if not separately presented on the face of the statement, the carrying amount(s) of the major classes of assets and liabilities included as part of a disposal group

b.

If not separately presented on the face of the statement where net income is reported (or statement of activities for a not-for-profit entity) as part of discontinued operations (see paragraph 205-20-45-3B), The

the gain or loss recognized in accordance with

paragraph 205-20-45-3C.paragraphs 360-10-35-40 and 360-10-40-5 and if not separately presented on the face of the income statement, the caption in the income statement or the statement of activities that includes that gain or loss

d. If applicable, the

segment(s)segment

in which the

discontinued operation long-lived asset (disposal group)

is reported under Topic 280

on segment reporting.

> Long-Lived Asset or Disposal Group Classified as Held for Sale

205-20-50-2 Paragraph superseded by Accounting Standards Update 2014-08. As indicated in paragraph 205-20-45-10, the major classes of assets and liabilities classified as held for sale shall be separately disclosed either on the face of the statement of financial position or in the notes to financial statements (see item a in paragraph 205-20-50-1(a)).

> Change to a Plan of Sale

205-20-50-3 If either

An entity may change its plan of sale as addressed in paragraphparagraphs

360-10-35-44 or

360-10-35-45 applies,

paragraph 360-10-35-45. In the period in which the decision is made to change the plan for selling the discontinued operation, an entity shall disclose in the notes to financial statements a description of the facts and circumstances leading to the decision to change

the

that plan

to sell the long-lived asset (disposal group)

and

the change'sits

effect on the results of operations for the period and any prior periods presented

shall be disclosed in the notes to financial statements that include the period of that decision

.

> > Adjustments to Previously Reported Amounts

205-20-50-3A The nature and amount of adjustments to amounts previously reported in discontinued operations that are directly related to the disposal of a

component of an entity

discontinued operation in a prior period shall be disclosed

(see paragraph 205-20-45-5 for examples of circumstances in which those types of adjustments may arise).

[Content amended as shown and moved from paragraph 205-20-50-5]

> Continuing InvolvementCash Flows

205-20-50-4 Paragraph superseded by Accounting Standards Update 2014-08.The following information shall be disclosed in the notes to financial statements for each discontinued operation that generates continuing cash flows:

The nature of the activities that give rise to cash flows

The period of time continuing cash flows are expected to be generated

The principal factors used to conclude that the expected continuing cash flows are not direct cash flows of the disposed component.

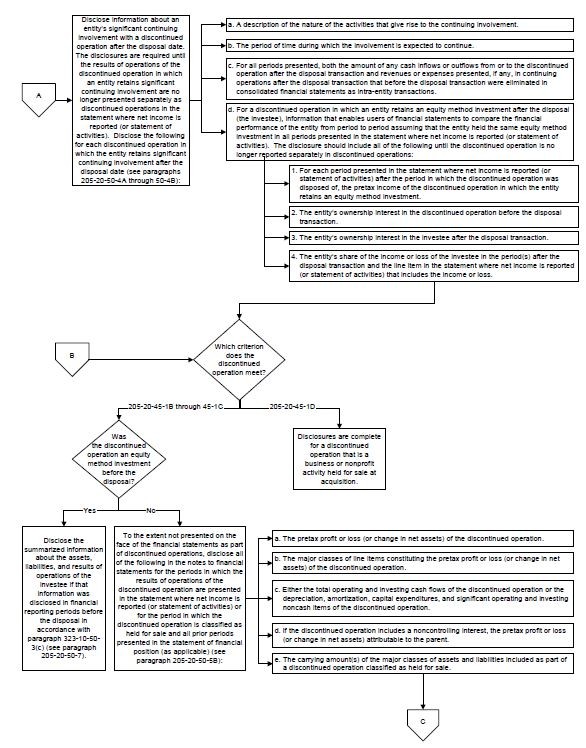

205-20-50-4A An entity shall disclose information about its significant continuing involvement with a discontinued operation after the disposal date. Examples of continuing involvement with a discontinued operation after the disposal date include a supply and distribution agreement, a financial guarantee, an option to repurchase a discontinued operation, and an equity method investment in the discontinued operation. The disclosures are required until the results of operations of the discontinued operation in which an entity retains significant continuing involvement are no longer presented separately as discontinued operations in the statement where net income is reported (or statement of activities for a not-for-profit entity).

205-20-50-4B An entity shall disclose the following in the notes to financial statements for each discontinued operation in which the entity retains significant continuing involvement after the disposal date:

a. A description of the nature of the activities that give rise to the continuing involvement.

b. The period of time during which the involvement is expected to continue.

c. For all periods presented, both of the following:

1. The amount of any cash inflows or outflows from or to the discontinued operation after the disposal transaction

2. Revenues or expenses presented, if any, in continuing operations after the disposal transaction that before the disposal transaction were eliminated in consolidated financial statements as intra-entity transactions.

d. For a discontinued operation in which an entity retains an equity method investment after the disposal (the investee), information that enables users of financial statements to compare the financial performance of the entity from period to period assuming that the entity held the same equity method investment in all periods presented in the statement where net income is reported (or statement of activities for a not-for-profit entity). The disclosure shall include all of the following until the discontinued operation is no longer reported separately in discontinued operations:

1. For each period presented in the statement where net income is reported (or statement of activities for a not-for-profit entity) after the period in which the discontinued operation was disposed of, the pretax income of the investee in which the entity retains an equity method investment

2. The entity’s ownership interest in the discontinued operation before the disposal transaction

3. The entity’s ownership interest in the investee after the disposal transaction

4. The entity’s share of the income or loss of the investee in the period(s) after the disposal transaction and the line item in the statement where net income is reported (or statement of activities for a not-for-profit entity) that includes the income or loss.

> Adjustments to Previously Reported Amounts

205-20-50-5 Paragraph superseded by Accounting Standards Update 2014-08. The nature and amount of adjustments to amounts previously reported in discontinued operations that are directly related to the disposal of a component of an entity in a prior period shall be disclosed.

[Content amended and moved to paragraph 205-20-50-3A]

12. Add paragraphs 205-20-50-5A through 50-5D and their related heading and 205-20-50-7 and its related heading and supersede paragraph 205-20-50-6 and its related heading, with a link to transition paragraph 205-20-65-1, as follows:

> Disclosures Required for a Discontinued Operation Comprising a Component or Group of Components of an Entity

205-20-50-5A Paragraphs 205-20-50-5B through 50-5D provide disclosures required for discontinued operations that meet the criteria in paragraphs 205-20-45-1B through 45-1C except for a discontinued operation that was an equity method investment before the disposal. For disclosures required for discontinued operations that were equity method investments before the disposal, see paragraph 205-20-50-7.

205-20-50-5B An entity shall disclose, to the extent not presented on the face of the financial statements as part of discontinued operations, all of the following in the notes to financial statements:

a. The pretax profit or loss (or change in net assets for a not-for-profit entity) of the discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported (or statement of activities for a not-for-profit entity).

b. The major classes of line items constituting the pretax profit or loss (or change in net assets for a not-for-profit entity) of the discontinued operation (for example, revenue, cost of sales, depreciation and amortization, and interest expense) for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported (or statement of activities for a not-for-profit entity).

c. Either of the following:

1. The total operating and investing cash flows of the discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported (or statement of activities for a not-for-profit entity)

2. The depreciation, amortization, capital expenditures, and significant operating and investing noncash items of the discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported (or statement of activities for a not-for-profit entity).

d. If the discontinued operation includes a noncontrolling interest, the pretax profit or loss (or change in net assets for a not-for-profit entity) attributable to the parent for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported (or statement of activities for a not-for-profit entity).

e. The carrying amount(s) of the major classes of assets and liabilities included as part of a discontinued operation classified as held for sale for the period in which the discontinued operation is classified as held for sale and all prior periods presented in the statement of financial position. Any loss recognized on the discontinued operation classified as held for sale in accordance with paragraphs 205-20-45-3B through 45-3C shall not be allocated to the major classes of assets and liabilities of the discontinued operation.

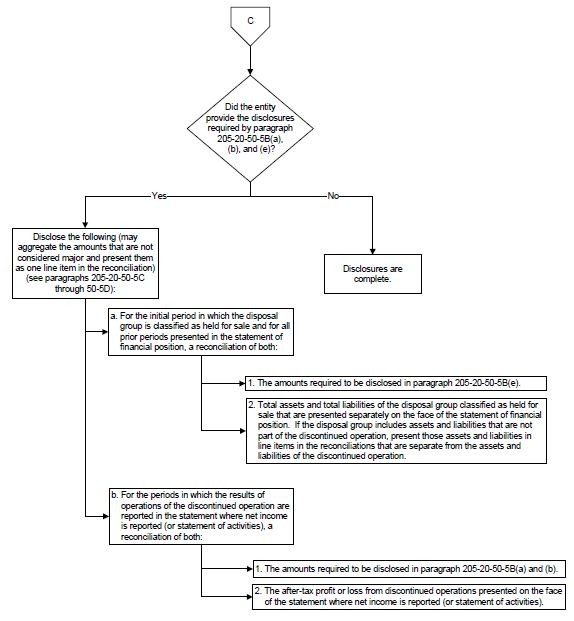

205-20-50-5C If an entity provides the disclosures required by paragraph 205-20-50-5B(a), (b), and (e) in the notes to financial statements, the entity shall disclose the following:

a. For the initial period in which the disposal group is classified as held for sale and for all prior periods presented in the statement of financial position, a reconciliation of both of the following:

1. The amounts disclosed in paragraph 205-20-50-5B(e)

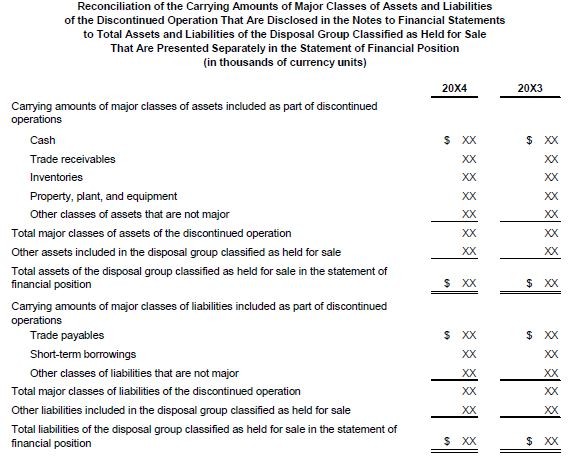

2. Total assets and total liabilities of the disposal group classified as held for sale that are presented separately on the face of the statement of financial position. If the disposal group includes assets and liabilities that are not part of the discontinued operation, an entity shall present those assets and liabilities in line items in the reconciliations that are separate from the assets and liabilities of the discontinued operation (see paragraph 205-20-55-102 for an Example).

b. For the periods in which the results of operations of the discontinued operation are reported in the statement where net income is reported (or statement of activities for a not-for-profit entity), a reconciliation of both of the following:

1. The amounts disclosed in paragraph 205-20-50-5B(a) and (b)

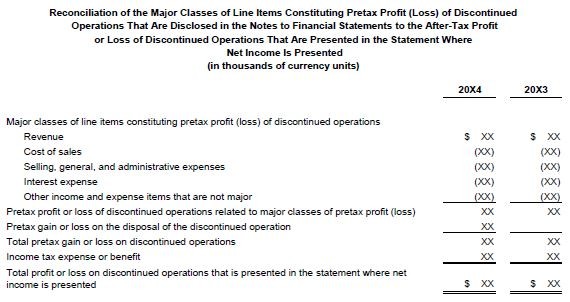

2. The after-tax profit or loss from discontinued operations presented on the face of the statement where net income is reported (or statement of activities for a not-for-profit entity) (see paragraph 205-20-55-103 for an Example).

205-20-50-5D For purposes of the reconciliation in paragraph 205-20-50-5C(a) or (b), an entity may aggregate the amounts that are not considered major and present them as one line item in the reconciliation.

> Continuing Involvement by Ongoing Entity

205-20-50-6 Paragraph superseded by Accounting Standards Update 2014-08. For each discontinued operation in which the ongoing entity will engage in a continuation of activities with the disposed component after its disposal and for which the amounts presented in continuing operations after the disposal transaction include a continuation of revenues and expenses that were intra-entity transactions (eliminated in consolidated financial statements) before the disposal transaction, intra-entity amounts before the disposal transaction shall be disclosed for all periods presented. The types of continuing involvement, if any, that the entity will have after the disposal transaction shall be disclosed. That information shall be disclosed in the period in which operations are initially classified as discontinued.

> Disclosures Required for a Discontinued Operation Comprising an Equity Method Investment

205-20-50-7 For an equity method investment that meets the criteria in paragraphs 205-20-45-1B through 45-1C, an entity shall disclose summarized information about the assets, liabilities, and results of operations of the investee if that information was disclosed in financial reporting periods before the disposal in accordance with paragraph 323-10-50-3(c).

13. Supersede paragraphs 205-20-55-1 through 55-81 and their related headings and add paragraphs 205-20-55-82 through 55-103 and their related headings, with a link to transition paragraph 205-20-65-1, as follows:

[Note: For ease of readability, the superseded paragraphs are not shown here.]

Implementation Guidance and Illustrations

> Implementation Guidance

205-20-55-82 The following flowchart provides an overview of the disclosures required for discontinued operations.

> Illustrations

205-20-55-83 Examples 1 through 3 provide illustrations of the guidance in paragraphs 205-20-45-1B through 45-1C on disposals of groups of components of an entity representing strategic shifts that have a major effect on the entity’s operations and financial results and are reported in discontinued operations.

> > Example 1: Consumer Products Manufacturer

205-20-55-84 An entity manufactures and sells consumer products that are grouped into five major product lines. Each product line includes several brands that comprise operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. Therefore, for that entity, each major product line includes a group of components of the entity.

205-20-55-85 The entity has experienced high growth in its discount cleaning product line that has lower price points than its premium cleaning product line. Total revenues from the discount cleaning product line are 15 percent of the entity’s total revenues; however, the discount cleaning product line will require significant future investments to increase its profits. Therefore, the entity decides to shift its strategy of selling cleaning products at multiple price points and focus solely on selling cleaning products at a premium price point. As a result, the entity decides to sell the discount cleaning product line.

205-20-55-86 Because the entity shifts its strategy of offering discount cleaning products to consumers and because the discount cleaning product line is one of five major product lines that is a major part of the entity’s operations and financial results, the disposal represents a strategic shift that is reported in discontinued operations.

> > Example 2: Processed and Packaged Goods Manufacturer

205-20-55-87 An entity manufactures and sells food products that are grouped into five major geographical areas (Europe, Asia, Africa, the Americas, and Oceania). Each major geographical area includes several brands that comprise operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. Therefore, for that entity, each major geographical area includes a group of components of the entity.

205-20-55-88 The entity has experienced slower growth in its operations located in the Americas, which accounts for 20 percent of the entity’s total assets. Therefore, the entity decides to shift its strategy of selling food products in that geographical area and focus its resources on manufacturing and marketing food products in its other four higher growth geographical areas. As a result, the entity decides to sell its operations in the Americas.

205-20-55-89 Because the entity’s operations in the Americas is one of five major geographical areas that is a major part of the entity’s operations and financial results, the disposal represents a strategic shift that is reported in discontinued operations.

> > Example 3: General Merchandise Retailer

205-20-55-90 An entity that is a general merchandise retailer operates 1,000 retail stores in 2 different store formats—malls and supercenter stores— throughout the United States. The entity divides its stores into five major geographical regions: the Northwest, Southwest, Midwest, Northeast, and Southeast. For that entity, each retail store comprises operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. Therefore, for that entity, each retail store is a component of the entity.

205-20-55-91 The entity has experienced declining net income at its 200 stores located in malls across all 5 major geographical regions. Historically, net income from the 200 stores in malls has been in a range of 30 to 40 percent of the entity’s total net income. Total net income from the 200 stores in malls is down to 15 percent of the entity’s total net income because of declining customer traffic in malls. Therefore, the entity decides to shift its strategy of selling products in malls and sell the 200 stores located in malls.

205-20-55-92 Because the entity decides to shift its strategy of selling products in malls and focus solely on its supercenter stores and because the 200 stores located in malls are a major part of the entity’s operations and financial results, the disposal represents a strategic shift that is reported in discontinued operations.

> > Example 4: Oil and Gas Entity

205-20-55-93 This Example provides an illustration of the guidance in paragraphs 205-20-45-1B through 45-1C. In this Example, the entity disposes of a component of an entity that is an equity method investment representing a strategic shift that has a major effect on the entity’s operations and financial results and is reported in discontinued operations.

205-20-55-94 An entity that follows the successful-efforts method of accounting produces oil and gas in two major geographical areas (Europe and Africa) that are each divided into several regions. Each region comprises operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. Therefore, for that entity, each major geographical area includes a group of components of the entity.

205-20-55-95 In its operations located in Africa, the entity operates through a joint venture with another entity that is accounted for by the reporting entity as an equity method investment. The entity’s carrying amount of its investment in the joint venture is 20 percent of the entity’s total assets. Because of significant investments needed in its operations in Europe, the entity decides to shift its strategy of operating in Africa to focus on its operations in Europe and sell its stake in the joint venture.

205-20-55-96 Because the entity shifts its strategy of operating a joint venture to focus on its operations in Europe where it maintains full control and because its operations in Africa are a major part of the entity’s operations and financial results, its disposal represents a strategic shift that is reported in discontinued operations.

> > Example 5: Sports Equipment Manufacturer

205-20-55-97 This Example provides an illustration of the guidance in paragraphs 205-20-45-1B through 45-1C. In this Example, the entity sells 80 percent of a group of components of an entity representing a strategic shift that has a major effect on the entity’s operations and financial results and is reported in discontinued operations.

205-20-55-98 An entity that manufactures and sells sports equipment has two product lines that serve the football and baseball markets. Each product line includes several different brands that each comprise operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity. Therefore, for that entity, each product line includes a group of components of the entity.

205-20-55-99 The entity decides to shift its strategy of trying to sell products to the baseball equipment market, which accounts for 40 percent of its revenues, and focus more on serving its customers in the football equipment market. However, the entity decides to retain some exposure to the baseball equipment market by selling only 80 percent of the group of components in its product line that serves the baseball market to another entity.

205-20-55-100 Because the entity decides to shift its strategy of trying to sell products to the baseball equipment market by selling 80 percent of the group of components of the entity in that product line and because the portion sold comprises a major part of the entity’s operations and financial results, its disposal represents a strategic shift that is reported in discontinued operations.

205-20-55-101 Because of the entity’s significant continuing involvement after the disposal date, the entity provides the disclosures required by paragraphs 205-20-50-4A through 50-4B.

> > Reconciliation of the Carrying Amounts of Major Classes of Assets and Liabilities of Discontinued Operations to Total Assets and Liabilities Classified as Held for Sale

205-20-55-102 The table in this illustration provides one example of how to disclose the reconciliation required by paragraph 205-20-50-5C(a).

[For ease of readability, the new table is not underlined.]

> > Reconciliation of the Major Classes of Line Items Constituting Pretax Profit or Loss of Discontinued Operations to After-Tax Profit or Loss Reported in Discontinued Operations

205-20-55-103 The table in this illustration provides one example of how to disclose the reconciliation required by paragraph 205-20-50-5C(b).

[For ease of readability, the new table is not underlined.]