Search within this section

Select a section below and enter your search term, or to search all click Nonpublic companies

Favorited Content

ASU No. | Standard name | Effective date | Early adoptable | PwC resources |

|---|---|---|---|---|

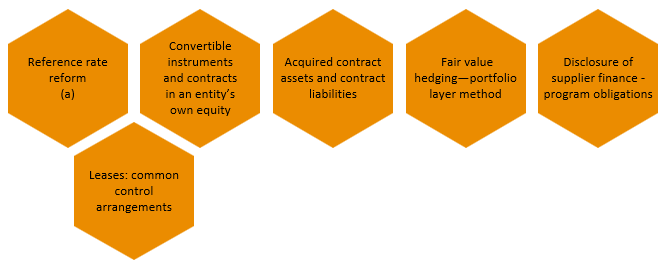

Reference Rate Reform (Topic 848): Scope

| Upon issuance (January 7, 2021) through December 31, 2024, as amended by ASU 2022-06 | Not applicable

| ||

Reference Rate Reform (Topic 848): Deferral of the Sunset Date of Topic 848

| Upon issuance (December 21, 2022) through December 31, 2024

| Not applicable

| ||

Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging —Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity

| Fiscal years beginning after December 15, 2023, and interim periods within those fiscal years

| Yes, but only as of the beginning of a fiscal year beginning after December 15, 2020.

| ||

Business Combinations (Topic 805): Accounting for Contract Assets and Contract Liabilities from Contracts with Customers

| Fiscal years beginning after December 15, 2023, and interim periods within those fiscal years

| Yes

| ||

Derivatives and Hedging (Topic 815): Fair Value Hedging—Portfolio Layer Method

| Fiscal years beginning after December 15, 2023, and interim periods within those fiscal years.

| Early adoption is permitted if ASU 2017-12 has already been adopted for the corresponding period.

| ||

Liabilities—Supplier Finance Programs (Subtopic 405-50): Disclosure of Supplier Finance Program Obligations

| Amendment on rollforward information is effective for fiscal years beginning after December 15, 2023.

| Yes

| ||

Leases (Topic 842): Common Control Arrangements

| Fiscal years beginning after December 15, 2023, and interim periods within those fiscal years

| Yes

|

ASU No. | Standard name | Effective date | Early adoptable | PwC resources |

|---|---|---|---|---|

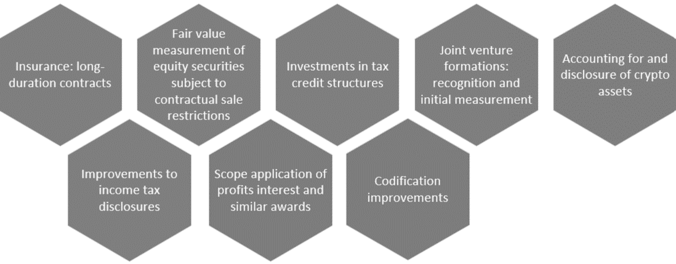

Financial Services—Insurance (Topic 944): Targeted Improvements to the Accounting for Long-Duration Contracts

| As amended by ASU 2020-11, fiscal years beginning after December 15, 2024, and interim periods within fiscal years beginning after December 15, 2025

| Yes

| ||

Financial Services—Insurance (Topic 944): Effective Date

| As amended by ASU 2020-11, effective for fiscal years beginning after December 15, 2024, and interim periods within fiscal years beginning after December 15, 2025

| Not applicable

| ||

Financial Services—Insurance (Topic 944): Effective Date and Early Application

| Effective for fiscal years beginning after December 15, 2024, and interim periods within fiscal years beginning after December 15, 2025

| Yes - early transition relief available

| ||

Financial Services—Insurance (Topic 944): Transition for Sold Contracts

| Effective for fiscal years beginning after December 15, 2024, and interim periods within fiscal years beginning after December 15, 2025

| Yes - early transition relief available

| ||

Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions

| Fiscal years beginning after December 15, 2024, and interim periods within those fiscal years

| Yes

| ||

Investments—Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method

| Fiscal years beginning after December 15, 2024, and interim periods within those fiscal years

| Yes

| ||

Business Combinations—Joint Venture Formations (Subtopic 805-60): Recognition and Initial Measurement

| Effective prospectively for all joint venture formations with a formation date on or after January 1, 2025.

| Early adoption is permitted in any interim or annual period in which financial statements have not yet been issued (or made available for issuance), either prospectively or retrospectively.

| ||

Intangibles—Goodwill and Other—Crypto Assets (Subtopic 350-60): Accounting for and Disclosure of Crypto Assets

| Fiscal years beginning after December 15, 2024, including interim periods within those fiscal years.

| Yes

| ||

Income Taxes (Topic 740): Improvements to Income Tax Disclosures

| Fiscal years beginning after December 15, 2025.

| Early adoption is permitted in any annual period in which financial statements have not yet been issued (or made available for issuance), either prospectively or retrospectively.

| ||

Compensation—Stock Compensation (Topic 718): Scope Application of Profits Interest and Similar Awards

| Fiscal years beginning after December 15, 2025, including interim periods within those fiscal years.

| Early adoption is permitted in any interim or annual period in which financial statements have not yet been issued (or made available for issuance), either prospectively or retrospectively.

| ||

Codification Improvements—Amendments to Remove References to the Concepts Statements

| Fiscal years beginning after December 15, 2025, including interim periods within those fiscal years.

| Early adoption is permitted in any interim or annual period in which financial statements have not yet been issued (or made available for issuance), either prospectively or retrospectively.

|

PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

Select a section below and enter your search term, or to search all click Nonpublic companies