Search within this section

Select a section below and enter your search term, or to search all click ASU 2016-01—Financial instruments—Overall (Subtopic 825-10)

Favorited Content

Copyright © 2016 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government. |

If Disclosures for the Current Period Are: |

And Disclosures for Prior Periods Were: |

Then Disclosures for Prior Periods Presented in Comparative Statements Are: |

Optional |

Optional |

Optional |

Optional |

Required |

Optional |

Required |

Optional |

Optional |

Required |

Required |

Required |

Valuation allowance Investments |

$ 200 |

||

Change in net unrealized gains and losses on investments |

$ 200 |

||

Cash |

$ 400 |

||

Realized gain |

$ 300 |

||

Investments |

100 |

||

Change in net unrealized gains and losses on investments |

200 |

||

Valuation allowance Investments |

200 |

||

View image

View image

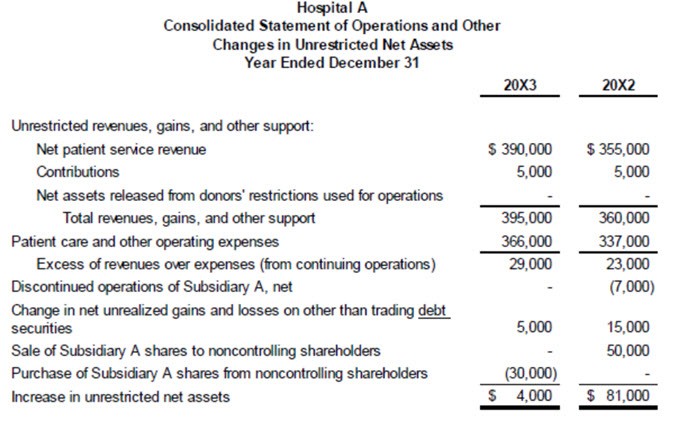

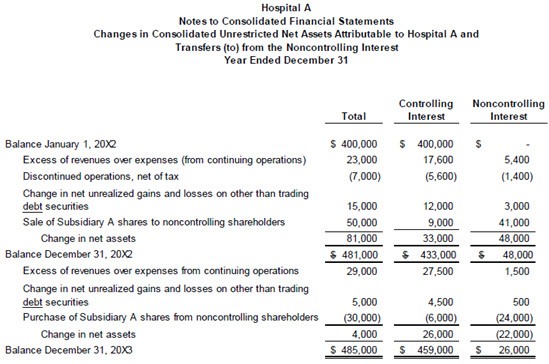

Cash |

$ 50,000 |

||

Unrestricted net assets (noncontrolling interest) |

$ 41,000 |

||

Unrestricted net assets (Hospital A) |

9,000 |

||

Paragraph |

Action |

Accounting Standards Update |

Date |

210-10-45-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

220-10-45-10A |

Amended |

2016-01 |

01/05/2016 |

220-10-55-5 |

Amended |

2016-01 |

01/05/2016 |

220-10-55-7 through 55-8A |

Amended |

2016-01 |

01/05/2016 |

220-10-55-9 |

Amended |

2016-01 |

01/05/2016 |

220-10-55-10A |

Amended |

2016-01 |

01/05/2016 |

220-10-55-15 through 55-15C |

Amended |

2016-01 |

01/05/2016 |

220-10-55-17C |

Amended |

2016-01 |

01/05/2016 |

220-10-55-17E |

Amended |

2016-01 |

01/05/2016 |

220-10-55-17F |

Amended |

2016-01 |

01/05/2016 |

220-10-55-19 |

Amended |

2016-01 |

01/05/2016 |

220-10-55-20 |

Amended |

2016-01 |

01/05/2016 |

220-10-55-21 through 55-23 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

230-10-45-11 through 45-13 |

Amended |

2016-01 |

01/05/2016 |

230-10-45-19 |

Amended |

2016-01 |

01/05/2016 |

230-10-45-21 |

Amended |

2016-01 |

01/05/2016 |

230-10-60-2 |

Amended |

2016-01 |

01/05/2016 |

230-10-60-2A |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

270-10-50-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

310-10-45-11 |

Amended |

2016-01 |

01/05/2016 |

310-10-50-26 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Equity Security (1st def.) |

Superseded |

2016-01 |

01/05/2016 |

Readily Determinable Fair Value |

Superseded |

2016-01 |

01/05/2016 |

320-10-05-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-05-2 |

Amended |

2016-01 |

01/05/2016 |

320-10-15-1 through 15-5 |

Amended |

2016-01 |

01/05/2016 |

320-10-15-7 |

Amended |

2016-01 |

01/05/2016 |

320-10-15-7A |

Added |

2016-01 |

01/05/2016 |

320-10-25-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-25-2 |

Amended |

2016-01 |

01/05/2016 |

320-10-30-1 through 30-4 |

Superseded |

2016-01 |

01/05/2016 |

320-10-35-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-35-2 |

Superseded |

2016-01 |

01/05/2016 |

320-10-35-3 through 35-5 |

Amended |

2016-01 |

01/05/2016 |

320-10-35-17 |

Amended |

2016-01 |

01/05/2016 |

320-10-35-20 |

Amended |

2016-01 |

01/05/2016 |

320-10-35-24 |

Amended |

2016-01 |

01/05/2016 |

320-10-35-25 through 35-29 |

Superseded |

2016-01 |

01/05/2016 |

320-10-35-32A |

Superseded |

2016-01 |

01/05/2016 |

320-10-35-33 |

Superseded |

2016-01 |

01/05/2016 |

320-10-35-34 |

Superseded |

2016-01 |

01/05/2016 |

320-10-45-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-45-3 through 45-6 |

Superseded |

2016-01 |

01/05/2016 |

320-10-50-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-50-4 |

Superseded |

2016-01 |

01/05/2016 |

320-10-50-6 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-1 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-2 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-4 |

Superseded |

2016-01 |

01/05/2016 |

320-10-55-5 |

Superseded |

2016-01 |

01/05/2016 |

320-10-55-6 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-7 |

Superseded |

2016-01 |

01/05/2016 |

320-10-55-9 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-22 |

Amended |

2016-01 |

01/05/2016 |

320-10-55-23 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Equity Security (1st def.) |

Added |

2016-01 |

01/05/2016 |

Fair Value (2nd def.) |

Added |

2016-01 |

01/05/2016 |

Holding Gain or Loss |

Added |

2016-01 |

01/05/2016 |

Market Participants |

Added |

2016-01 |

01/05/2016 |

Orderly Transaction |

Added |

2016-01 |

01/05/2016 |

Readily Determinable Fair Value |

Added |

2016-01 |

01/05/2016 |

Related Parties |

Added |

2016-01 |

01/05/2016 |

Security (2nd def.) |

Added |

2016-01 |

01/05/2016 |

321-10-05-1 |

Added |

2016-01 |

01/05/2016 |

321-10-05-2 |

Added |

2016-01 |

01/05/2016 |

321-10-15-1 through 15-6 |

Added |

2016-01 |

01/05/2016 |

321-10-30-1 |

Added |

2016-01 |

01/05/2016 |

321-10-35-1 through 35-6 |

Added |

2016-01 |

01/05/2016 |

321-10-40-1 |

Added |

2016-01 |

01/05/2016 |

321-10-45-1 |

Added |

2016-01 |

01/05/2016 |

321-10-45-2 |

Added |

2016-01 |

01/05/2016 |

321-10-50-1 through 50-4 |

Added |

2016-01 |

01/05/2016 |

321-10-55-1 through 55-9 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

323-10-05-1 |

Amended |

2016-01 |

01/05/2016 |

323-10-05-4 |

Amended |

2016-01 |

01/05/2016 |

323-10-35-24 through 35-26 |

Amended |

2016-01 |

01/05/2016 |

323-10-35-36 |

Amended |

2016-01 |

01/05/2016 |

323-10-35-37 |

Amended |

2016-01 |

01/05/2016 |

323-10-55-30 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

323-30-35-3 |

Amended |

2016-01 |

01/05/2016 |

323-30-35-4 |

Amended |

2016-01 |

01/05/2016 |

323-30-60-2 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

323-740-25-2A |

Added |

2016-01 |

01/05/2016 |

323-740-25-6 |

Amended |

2016-01 |

01/05/2016 |

323-740-30-2 |

Amended |

2016-01 |

01/05/2016 |

323-740-45-3 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

325-10-05-1 |

Amended |

2016-01 |

01/05/2016 |

325-10-05-2 |

Amended |

2016-01 |

01/05/2016 |

325-10-60-1 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Publicly Traded Company |

Superseded |

2016-01 |

01/05/2016 |

325-20-05-1 through 05-3 |

Superseded |

2016-01 |

01/05/2016 |

325-20-15-1 |

Superseded |

2016-01 |

01/05/2016 |

325-20-15-2 |

Superseded |

2016-01 |

01/05/2016 |

325-20-25-1 |

Superseded |

2016-01 |

01/05/2016 |

325-20-25-2 |

Superseded |

2016-01 |

01/05/2016 |

325-20-30-1 through 30-6 |

Superseded |

2016-01 |

01/05/2016 |

325-20-35-1 through 35-6 |

Superseded |

2016-01 |

01/05/2016 |

325-20-50-1 |

Superseded |

2016-01 |

01/05/2016 |

325-20-60-1 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

325-40-15-6 |

Amended |

2016-01 |

01/05/2016 |

325-40-25-2 |

Amended |

2016-01 |

01/05/2016 |

325-40-35-2 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

360-20-15-10 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

606-10-15-2 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

710-10-25-18 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Equity Security (2nd def.) |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

715-70-55-6 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

740-10-30-16 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

740-20-45-15 through 45-18 |

Added |

2016-01 |

01/05/2016 |

740-20-60-1 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

805-10-25-10 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-10-05-4 |

Amended |

2016-01 |

01/05/2016 |

815-10-15-138 |

Amended |

2016-01 |

01/05/2016 |

815-10-15-141 |

Amended |

2016-01 |

01/05/2016 |

815-10-15-142 |

Amended |

2016-01 |

01/05/2016 |

815-10-25-17 |

Amended |

2016-01 |

01/05/2016 |

815-10-25-18 |

Added |

2016-01 |

01/05/2016 |

815-10-30-5 |

Amended |

2016-01 |

01/05/2016 |

815-10-30-6 |

Added |

2016-01 |

01/05/2016 |

815-10-35-5 |

Amended |

2016-01 |

01/05/2016 |

815-10-35-6 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-15-15-6 |

Amended |

2016-01 |

01/05/2016 |

815-15-25-5 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-20-25-28 |

Amended |

2016-01 |

01/05/2016 |

815-20-25-37 |

Amended |

2016-01 |

01/05/2016 |

815-20-25-43 |

Amended |

2016-01 |

01/05/2016 |

815-20-25-71 |

Amended |

2016-01 |

01/05/2016 |

815-20-35-1 |

Amended |

2016-01 |

01/05/2016 |

815-20-55-117 |

Amended |

2016-01 |

01/05/2016 |

815-20-55-118 through 55-122 |

Superseded |

2016-01 |

01/05/2016 |

815-20-55-123 |

Amended |

2016-01 |

01/05/2016 |

815-20-55-187 through 55-192 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

815-25-35-6 |

Amended |

2016-01 |

01/05/2016 |

815-25-55-18 through 55-22 |

Superseded |

2016-01 |

01/05/2016 |

815-25-55-65 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

820-10-15-3 |

Amended |

2016-01 |

01/05/2016 |

820-10-55-100 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Conduit Debt Securities |

Superseded |

2016-01 |

01/05/2016 |

Nonpublic Entity (4th def.) |

Superseded |

2016-01 |

01/05/2016 |

Publicly Traded Company (1st def.) |

Superseded |

2016-01 |

01/05/2016 |

Public Business Entity (1st def.) |

Added |

2016-01 |

01/05/2016 |

825-10-05-3 |

Amended |

2016-01 |

01/05/2016 |

825-10-25-4 |

Amended |

2016-01 |

01/05/2016 |

825-10-35-4 |

Superseded |

2016-01 |

01/05/2016 |

825-10-45-1 |

Superseded |

2016-01 |

01/05/2016 |

825-10-45-1A |

Added |

2016-01 |

01/05/2016 |

825-10-45-1B |

Added |

2016-01 |

01/05/2016 |

825-10-45-4 through 45-7 |

Added |

2016-01 |

01/05/2016 |

825-10-50-2A |

Amended |

2016-01 |

01/05/2016 |

825-10-50-3 through 50-7 |

Superseded |

2016-01 |

01/05/2016 |

825-10-50-8 |

Amended |

2016-01 |

01/05/2016 |

825-10-50-10 |

Amended |

2016-01 |

01/05/2016 |

825-10-50-14 |

Superseded |

2016-01 |

01/05/2016 |

825-10-50-16 through 50-19 |

Superseded |

2016-01 |

01/05/2016 |

825-10-50-30 |

Amended |

2016-01 |

01/05/2016 |

825-10-50-31 |

Amended |

2016-01 |

01/05/2016 |

825-10-55-3 through 55-5 |

Superseded |

2016-01 |

01/05/2016 |

825-10-55-8 |

Amended |

2016-01 |

01/05/2016 |

825-10-55-10 |

Amended |

2016-01 |

01/05/2016 |

825-10-55-12 |

Amended |

2016-01 |

01/05/2016 |

825-10-65-2 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

835-10-60-5 |

Amended |

2016-01 |

01/05/2016 |

835-10-60-6A |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

845-10-30-26 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

860-10-55-77 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

940-340-35-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

942-320-50-2A |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

942-325-05-1 |

Amended |

2016-01 |

01/05/2016 |

942-325-05-2 |

Amended |

2016-01 |

01/05/2016 |

942-325-25-4 |

Added |

2016-01 |

01/05/2016 |

942-325-30-1 |

Added |

2016-01 |

01/05/2016 |

942-325-35-1 |

Amended |

2016-01 |

01/05/2016 |

942-325-35-5 |

Added |

2016-01 |

01/05/2016 |

942-325-45-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

942-470-50-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

942-825-50-2 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

944-10-05-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

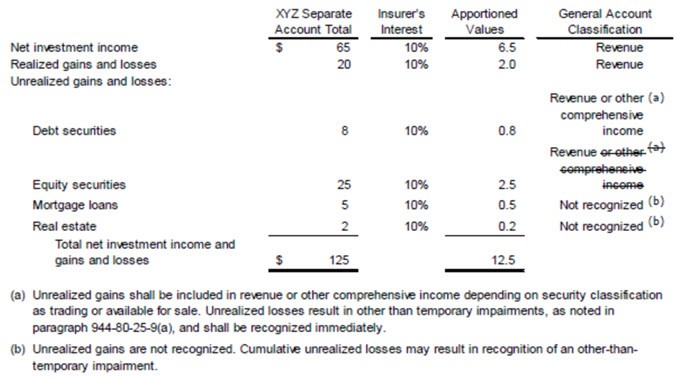

944-80-25-9 through 25-11 |

Amended |

2016-01 |

01/05/2016 |

944-80-55-8 |

Amended |

2016-01 |

01/05/2016 |

944-80-55-9 |

Amended |

2016-01 |

01/05/2016 |

944-80-55-11 |

Amended |

2016-01 |

01/05/2016 |

944-80-55-16 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Carrying Amount |

Superseded |

2016-01 |

01/05/2016 |

Separate Account |

Superseded |

2016-01 |

01/05/2016 |

944-320-05-1 |

Superseded |

2016-01 |

01/05/2016 |

944-320-15-1 |

Superseded |

2016-01 |

01/05/2016 |

944-320-15-2 |

Superseded |

2016-01 |

01/05/2016 |

944-320-25-1 |

Superseded |

2016-01 |

01/05/2016 |

944-320-50-1 |

Superseded |

2016-01 |

01/05/2016 |

944-320-50-2 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Fair Value (2nd def.) |

Superseded |

2016-01 |

01/05/2016 |

Market Participants |

Superseded |

2016-01 |

01/05/2016 |

Orderly Transaction |

Superseded |

2016-01 |

01/05/2016 |

Readily Determinable Fair Value |

Superseded |

2016-01 |

01/05/2016 |

Related Parties |

Superseded |

2016-01 |

01/05/2016 |

944-325-05-1 |

Superseded |

2016-01 |

01/05/2016 |

944-325-15-1 |

Superseded |

2016-01 |

01/05/2016 |

944-325-30-1 |

Superseded |

2016-01 |

01/05/2016 |

944-325-35-1 through 35-3 |

Superseded |

2016-01 |

01/05/2016 |

944-325-40-1 |

Superseded |

2016-01 |

01/05/2016 |

944-325-45-1 through 45-5 |

Superseded |

2016-01 |

01/05/2016 |

944-325-50-1 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

944-360-40-2 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

944-605-25-21 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

944-825-50-1 |

Superseded |

2016-01 |

01/05/2016 |

944-825-50-1A |

Added |

2016-01 |

01/05/2016 |

944-825-50-1B |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

954-10-05-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

954-225-45-7 |

Amended |

2016-01 |

01/05/2016 |

954-225-45-8 through 45-10 |

Added |

2016-01 |

01/05/2016 |

954-225-55-2 through 55-5 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Performance Indicator |

Superseded |

2016-01 |

01/05/2016 |

954-320-05-1 |

Superseded |

2016-01 |

01/05/2016 |

954-320-15-1 |

Superseded |

2016-01 |

01/05/2016 |

954-320-35-1 |

Superseded |

2016-01 |

01/05/2016 |

954-320-45-1 through 45-3 |

Superseded |

2016-01 |

01/05/2016 |

954-320-55-1 through 55-4 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

954-805-25-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

958-10-05-2 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

958-30-25-2 |

Amended |

2016-01 |

01/05/2016 |

958-30-25-4 |

Amended |

2016-01 |

01/05/2016 |

958-30-35-4 |

Amended |

2016-01 |

01/05/2016 |

958-30-35-11 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

958-210-45-12 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

958-225-48-8 |

Amended |

2016-01 |

01/05/2016 |

958-225-45-18 through 45-26 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Debt Security |

Added |

2016-01 |

01/05/2016 |

Equity Security (1st def.) |

Superseded |

2016-01 |

01/05/2016 |

Readily Determinable Fair Value |

Superseded |

2016-01 |

01/05/2016 |

958-320-05-1 |

Amended |

2016-01 |

01/05/2016 |

958-320-05-2 |

Amended |

2016-01 |

01/05/2016 |

958-320-15-1A through 15-4 |

Amended |

2016-01 |

01/05/2016 |

958-320-15-6 |

Amended |

2016-01 |

01/05/2016 |

958-320-15-7 |

Amended |

2016-01 |

01/05/2016 |

958-320-25-1 |

Amended |

2016-01 |

01/05/2016 |

958-320-25-2 |

Superseded |

2016-01 |

01/05/2016 |

958-320-30-1 |

Amended |

2016-01 |

01/05/2016 |

958-320-35-1 |

Amended |

2016-01 |

01/05/2016 |

958-320-35-2 |

Superseded |

2016-01 |

01/05/2016 |

958-320-45-1 through 45-10 |

Superseded |

2016-01 |

01/05/2016 |

958-320-55-3 |

Superseded |

2016-01 |

01/05/2016 |

958-320-60-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Equity Security (1st def.) |

Added |

2016-01 |

01/05/2016 |

Financially Interrelated Entities |

Added |

2016-01 |

01/05/2016 |

Net Assets |

Added |

2016-01 |

01/05/2016 |

Not-for-Profit Entity |

Added |

2016-01 |

01/05/2016 |

Permanently Restricted Net Assets |

Added |

2016-01 |

01/05/2016 |

Temporarily Restricted Net Assets |

Added |

2016-01 |

01/05/2016 |

Unrestricted Net Assets |

Added |

2016-01 |

01/05/2016 |

958-321-05-1 |

Added |

2016-01 |

01/05/2016 |

958-321-05-2 |

Added |

2016-01 |

01/05/2016 |

958-321-15-1 through 15-7 |

Added |

2016-01 |

01/05/2016 |

958-321-25-1 |

Added |

2016-01 |

01/05/2016 |

958-321-25-2 |

Added |

2016-01 |

01/05/2016 |

958-321-30-1 |

Added |

2016-01 |

01/05/2016 |

958-321-35-1 |

Added |

2016-01 |

01/05/2016 |

958-321-35-2 |

Added |

2016-01 |

01/05/2016 |

958-321-50-1 |

Added |

2016-01 |

01/05/2016 |

958-321-50-2 |

Added |

2016-01 |

01/05/2016 |

958-321-55-1 |

Added |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Readily Determinable Fair Value |

Superseded |

2016-01 |

01/05/2016 |

958-325-05-1 |

Amended |

2016-01 |

01/05/2016 |

958-325-05-2 |

Amended |

2016-01 |

01/05/2016 |

958-325-15-2 |

Amended |

2016-01 |

01/05/2016 |

958-325-15-3 |

Amended |

2016-01 |

01/05/2016 |

958-325-35-8 through 35-13 |

Superseded |

2016-01 |

01/05/2016 |

958-325-45-1 |

Amended |

2016-01 |

01/05/2016 |

958-325-50-2 |

Amended |

2016-01 |

01/05/2016 |

958-325-50-3 |

Superseded |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Equity Security (1st def.) |

Amended |

2016-01 |

01/05/2016 |

958-605-45-4 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

958-810-15-4 |

Amended |

2016-01 |

01/05/2016 |

958-810-55-4 |

Amended |

2016-01 |

01/05/2016 |

958-810-55-21 |

Amended |

2016-01 |

01/05/2016 |

958-810-55-24 |

Amended |

2016-01 |

01/05/2016 |

958-810-55-25 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

970-323-25-6 |

Amended |

2016-01 |

01/05/2016 |

970-323-25-7 |

Superseded |

2016-01 |

01/05/2016 |

970-323-25-8 |

Amended |

2016-01 |

01/05/2016 |

970-323-25-11 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

974-323-25-1 |

Amended |

2016-01 |

01/05/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

978-810-25-4 |

Amended |

2016-01 |

01/05/2016 |

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

Select a section below and enter your search term, or to search all click ASU 2016-01—Financial instruments—Overall (Subtopic 825-10)