7. Add

Subtopic 958-805. All paragraphs in this new Subtopic are linked to transition paragraph 958-805-65-1.

Not-for-Profit Entities—Business Combinations

Overview and Background

General

958-805-05-1 This Subtopic provides guidance on a transaction or other event [FAS 164, paragraph 2, sequence 2.1] in which a not-for-profit entity (NFP) that is the reporting entity combines with one or more other NFPs, businesses, or nonprofit activities [FAS 164, paragraph 1, sequence 1.1] in a transaction that meets the definition of a merger of not-for-profit entities [FAS 164, paragraph 2, sequence 2.1.1] or an acquisition by a not-for-profit entity. [FAS 164, paragraph 2, sequence 2.1.2] The guidance is presented in the following three Subsections:

- General

- Merger of Not-for-Profit Entities

- Acquisition by a Not-for-Profit Entity.

958-805-05-2 The General Subsections provide overall guidance on the recognition of combinations involving NFPs, and they provide implementation guidance for determining whether a combination between an NFP and one or more businesses, nonprofit activities, or another NFP is a merger or an acquisition.

958-805-05-3 Paragraphs presented in bold type in this Subtopic state the main principles. All paragraphs have equal authority. [FAS 164, paragraph 1, sequence 1.3]

Merger of Not-for-Profit Entities

958-805-05-4 The Merger of Not-for-Profit Entities Subsections establish standards of financial accounting and reporting for transactions or other events that meet the definition of a merger of not-for-profit entities. Specifically, these Subsections establish principles and requirements for how a not-for-profit entity (NFP) does both of the following:

- Applies the carryover method in accounting for a merger [FAS 164, paragraph 1(b), sequence 1.1.2]

- Determines what information to disclose to enable users of financial statements to evaluate the nature and financial effects of a merger. [FAS 164, paragraph 1(d), sequence 1.1.4]

Acquisition by a Not-for-Profit Entity

958-805-05-5 The Acquisition by a Not-for-Profit Entity Subsections establish standards of financial accounting and reporting for transactions or other events that meet the definition of an acquisition by a not-for-profit entity. Those standards are incremental to the guidance in Subtopics 805-10, 805-20, and 805-40. Specifically, these Subsections establish principles and requirements for how a not-for-profit entity does both of the following:

a. Applies the acquisition method in accounting for an acquisition, including determining which of the combining entities is the acquirer [FAS 164, paragraph 1(c), sequence 1.1.3]

b. Determines what information to disclose to enable users of financial statements to evaluate the nature and financial effects of an acquisition. [FAS 164, paragraph 1(d), sequence 1.1.4]

Objectives

General

958-805-10-1 The objective of this Subtopic is to improve the relevance, representational faithfulness, and comparability of the information that a not-for-profit entity (NFP) that is a reporting entity provides in its financial reports about a combination with one or more other NFPs, businesses, or nonprofit activities. [FAS 164, paragraph 1, sequence 1.1]

Scope and Scope Exceptions

General

> Overall Guidance

958-805-15-1 This Subtopic follows the same scope and scope exceptions as the Overall Subtopic, see

Section 958-10-15.

958-805-15-2 The General Subsection of this Section establishes the pervasive scope for this Subtopic.

> Transactions

958-805-15-3 The guidance in this Subtopic applies to a transaction or other event that meets the definition of either of the following: [FAS 164, paragraph 2, sequence 2.1]

a. A merger of not-for-profit entities [FAS 164, paragraph 2, sequence 2.1.1]

b. An acquisition by a not-for-profit entity. [FAS 164, paragraph 2, sequence 2.1.2]

958-805-15-4 This Subtopic does not apply to all of the following: [FAS 164, paragraph 2, sequence 2.1.3]

- The formation of a joint venture [FAS 164, paragraph 2, sequence 2.1.3.1]

- The acquisition of an asset or a group of assets that does not constitute either a business or a nonprofit activity. (Subtopic 805-50 addresses the typical accounting for an asset acquisition.) [FAS 164, paragraph 2, sequence 2.1.3.2]

- A combination between not-for-profit entities (NFPs), businesses, or nonprofit activities under common control. (Subtopic 805-50 addresses the typical accounting for a transfer of assets or an exchange of shares between entities under common control.) [FAS 164, paragraph 2, sequence 2.1.3.3]

- A transaction or other event in which an NFP obtains control of another not-for-profit entity but does not consolidate that entity, as permitted or required by Section 958-810-25. Similarly, this Subtopic does not apply if an NFP that obtained control in a transaction or other event in which consolidation was permitted but not required decides in a subsequent annual reporting period to begin consolidating a controlled entity that it initially chose not to consolidate. [FAS 164, paragraph 2, sequence 2.1.3.4]

Merger of Not-for-Profit Entities

> Overall Guidance

958-805-15-5 The Merger of Not-for-Profit Entities Subsections follow the same Scope and Scope Exceptions as the General Subsections of this Subtopic, see

Section 958-805-15, with specific exceptions noted below.

> Transactions

958-805-15-6 The guidance in the Merger of Not-for-Profit Entities Subsections applies only to transactions or other events that meet the definition of a [FAS 164, paragraph 2, sequence 2.1] merger of not-for-profit entities. [FAS 164, paragraph 2, sequence 2.1.1]

Acquisition by a Not-for-Profit Entity

> Overall Guidance

958-805-15-7 The Acquisition by a Not-for-Profit Entity Subsections follow the same Scope and Scope Exceptions as the General Subsections of this Subtopic, see

Section 958-805-15, with specific exceptions noted below.

> Transactions

958-805-15-8 The guidance in the Acquisition by a Not-for-Profit Entity Subsections applies only to transactions or other events that meet the definition of an [FAS 164, paragraph 2, sequence 2.1.1] acquisition by a not-for-profit entity. [FAS 164, paragraph 2, sequence 2.1.2]

Recognition

General

958-805-25-1 A {Glossary link} not-for-profit entity {Glossary link} (NFP) shall determine whether a transaction or other event is a {Glossary link} merger of not-for-profit entities {Glossary link} or an {Glossary link} acquisition by a not-for-profit entity {Glossary link} by applying the definitions. [FAS 164, paragraph 4, sequence 4]

958-805-25-2 Paragraphs 958-805-55-1 through 55-31 provide guidance on distinguishing between a merger and an acquisition. [FAS 164, paragraph 5, sequence 5]

Merger of Not-for-Profit Entities

958-805-25-3 The {Glossary link} not-for-profit entity {Glossary link} (NFP) resulting from a merger (the new entity) shall account for the merger by applying the carryover method described in the Merger of Not-for-Profit Entities Subsections of this Subtopic. [FAS 164, paragraph 6, sequence 6]

958-805-25-4 Applying the carryover method requires combining the assets and liabilities recognized in the separate financial statements of the merging entities as of the merger date (or that would be recognized if the entities issued financial statements as of that date), adjusted as necessary in accordance with paragraph 958-805-25-7 and paragraphs 958-805-30-2 through 30-4. [FAS 164, paragraph 7, sequence 7.1]

958-805-25-5 The remainder of the discussion of the carryover method refers to financial statements of the merging entities, rather than a more precise, but longer, phrase such as assets and liabilities that would be recognized in the financial statements of the merging entities if statements are prepared. Use of the shorter phrase is not intended to exclude, for example, an NFP that has not prepared or issued financial statements. In that situation, the phrase refers to the items in the entity’s financial records that would be the basis for preparing financial statements. [FAS 164, paragraph 7 FN2, Sequence 7.1.1]

958-805-25-6 The new NFP shall recognize in its financial statements the assets and liabilities reported in the separate financial statements of the merging entities as of the merger date in accordance with generally accepted accounting principles (GAAP). [FAS 164, paragraph 8, sequence 8]

958-805-25-7 The new NFP does not recognize additional assets or liabilities, such as internally developed intangible assets, that GAAP did not require or permit the merging entities to recognize. However, if a merging entity’s separate financial statements are not prepared in accordance with GAAP, those statements shall be adjusted to GAAP before the new entity recognizes the assets and liabilities. [FAS 164, paragraph 9, sequence 9]

> Classifying or Designating Assets and Liabilities in a Merger

958-805-25-8 The new NFP shall carry forward at the merger date the merging entities’ classifications and designations of their assets and liabilities unless one of the exceptions in the following paragraph applies. [FAS 164, paragraph 10, sequence 10]

958-805-25-9 In some situations, GAAP provides for different accounting depending on how an entity classifies or designates a particular asset or liability. Paragraphs 805-20-25-7 through 25-8 provide examples of such classifications and designations. The new NFP shall carry forward into the opening balances in its financial statements (see paragraph 958-805-45-2(a)) the merging entities’ classifications and designations unless either of the following situations applies:

[FAS 164, paragraph 11, sequence 11.1]

- The merger results in a modification of a contract in a manner that would change those previous classifications or designations [FAS 164, paragraph 11, sequence 11.1.1]; for example, if the provisions of a lease are modified in a way that would require the revised agreement to be considered a new agreement under paragraph 840-10-35-4 [FIN 21, paragraph 13, sequence 34]

- Reclassifications are necessary to conform accounting policies in accordance with paragraph 958-805-30-2. [FAS 164, paragraph 11, sequence 11.1.2]

958-805-25-10 In situation (a) in the preceding paragraph, the new NFP shall classify or designate the asset or liability on the basis of the contractual terms, economic conditions, its operating or accounting policies, and other pertinent conditions as they exist at the date of that modification. In situation (b) in the preceding paragraph, the new NFP shall classify or designate the asset or liability on the basis of the conformed accounting policies at the merger date. [FAS 164, paragraph 11, sequence 11.2]

958-805-25-11 At the merger date, the new NFP may contemplate renegotiating and modifying leases of the business or nonprofit activity acquired. Modifications made after the merger date, including those that were planned at the time of the combination, are postcombination events that should be accounted for separately by the new NFP in accordance with

Topic 840.

[FIN 21, paragraph 15, sequence 136.1.1.2]

Acquisition by a Not-for-Profit Entity

958-805-25-12 A {Glossary link} not-for-profit entity {Glossary link} (NFP) shall account for each acquisition of a {Glossary link} business {Glossary link} or {Glossary link} nonprofit activity {Glossary link} by applying the acquisition method described in the Acquisition by a Not-for-Profit Entity Subsections of this Subtopic. [FAS 164, paragraph 20, sequence 20]

958-805-25-13 The acquisition method in the Acquisition by a Not-for-Profit Entity Subsections is the same as the acquisition method described in

Topic 805. However, these Subsections include guidance on aspects of the following items that are unique or especially significant to an NFP:

[FAS 164, paragraph 22, sequence 22.1]

a. Identifying the acquirer [FAS 164, paragraph 22, sequence 22.1.1]

b. Identifying the acquisition date [FAS 164, paragraph 22, sequence 22.1.2]

c. Recognizing the identifiable assets acquired, the liabilities assumed, and any noncontrolling interest in the acquiree [FAS 164, paragraph 22, sequence 22.1.3]

d. Recognizing goodwill acquired or a contribution received, including consideration transferred [FAS 164, paragraph 22, sequence 22.1.4]

e. Determining what is part of the acquisition transaction.

958-805-25-14 Differences in the application of the acquisition method by a NFP acquirer from the application of the acquisition method by a business entity include all of the following:

- The identification of the acquirer in accordance with paragraphs 958-805-25-15 through 25-16, instead of the guidance in paragraph 805-10-25-5

- The recognition and measurement of goodwill (or the immediate charge to the statement of activities) in accordance with paragraphs 958-805-25-27 through 25-30, instead of the guidance in paragraph 805-30-25-1 and paragraphs 805-30-30-1 through 30-3

- The recognition and measurement of an inherent contribution received in accordance with paragraph 958-805-25-31 and paragraphs 958-805-30-8 through 30-9, instead of the guidance for a gain from a bargain purchase in paragraphs 805-30-25-2 through 25-4 and paragraphs 805-30-30-4 through 30-6.

> Identifying the Acquirer

958-805-25-15 Paragraph 805-10-25-4 requires that one of the combining entities be identified as the acquirer. Instead of applying the guidance in paragraph 805-10-25-5, the following guidance on control and consolidation of NFPs shall be used to identify the acquirer: [FAS 164, paragraph 24, sequence 24.1]

- For an NFP acquirer other than a health care entity within the scope of Topic 954, the guidance in Subtopic 958-810, including the guidance referenced in paragraph 958-810-15-4. [FAS 164, paragraph 24, sequence 24.1.1]

- For a not-for-profit health care acquirer within the scope of Topic 954 (see Section 954-10-15), the guidance referenced in paragraph 954-810-15-3. [FAS 164, paragraph 24, sequence 24.1.2]

- Control of a for-profit business has the meaning of controlling financial interest in paragraph 810-10-15-8. [FAS 164, paragraph 3(j), sequence 3.2.1]

- Control of a not-for-profit entity has the meaning of control {Use definition of control from Subtopics 954-810 and 958-810} used in Subtopic 954-810 and Subtopic 958-810. [FAS 164, paragraph 3(k), sequence 3.2.2]

958-805-25-16 If an acquisition by a not-for-profit entity has occurred but applying the guidance in the previous paragraph does not clearly indicate which of the combining entities is the acquirer, the factors in paragraphs 958-805-55-42 through 55-46 shall be considered in making that determination. [FAS 164, paragraph 24, sequence 24.2]

> Identifying the Acquisition Date

958-805-25-17 Paragraphs 805-10-25-6 through 25-7 require identifying the acquisition date and provide guidance for doing so. In addition to that guidance, the date on which an NFP acquirer obtains control of an NFP with sole corporate membership generally also is the date on which the acquirer becomes the sole corporate member of that entity. [FAS 164, paragraph 26, sequence 26.2]

> Recognizing the Identifiable Assets Acquired, the Liabilities Assumed, and Any Noncontrolling Interest in the Acquiree

958-805-25-18 This Subsection includes the following guidance that is incremental to

Subtopic 805-20 for the recognition of identifiable assets acquired, liabilities assumed, and any noncontrolling interest in the acquiree

:

- Recognition conditions

- Classifying or designating identifiable assets acquired and liabilities assumed

- Additional exceptions to the recognition principle.

> > Recognition Conditions

958-805-25-19 When considering whether an identifiable asset or liability assumed qualifies for recognition as part of applying the acquisition method as described in paragraph 805-20-25-3, an identifiable asset or liability also qualifies if it is part of what was contributed in an acquisition that includes an inherent contribution (see paragraph 958-805-25-31). [FAS 164, paragraph 29, sequence 29]

> > Classifying or Designating Identifiable Assets Acquired and Liabilities Assumed

958-805-25-20 An NFP acquirer is not required to classify investments as described in paragraph 805-20-25-7(a). However, an NFP acquirer that is a health care entity (see

Section 954-10-15) shall classify particular investments as described in paragraph 954-805-25-1.

[FAS 164, paragraph 33(a), sequence 33.1.1]

> > Additional Exceptions to the Recognition Principle

958-805-25-21 This Subsection provides the following limited exceptions to the recognition principle in paragraph 805-20-25-1, which are incremental to the exceptions provided by paragraphs 805-20-25-16 through 25-28:

- Donor relationships

- Collections

- Conditional promises to give.

> > > Donor Relationships

958-805-25-22 An NFP acquirer shall not recognize an acquired donor relationship as an identifiable intangible asset separate from goodwill. [FAS 164, paragraph 38, sequence 38] Unlike acquired customer relationships (see paragraphs 805-20-55-23 through 55-25), acquired donor relationships are not recognized separately; they are instead subsumed into goodwill. [FAS 164, paragraph A72, sequence 173.3]

> > > Collections

958-805-25-23 An NFP acquirer that has an organizational policy of not capitalizing collections in accordance with paragraph 958-360-25-3 shall not recognize as an asset those items (works of art, historical treasures, or similar assets) that it acquires as part of an acquisition and adds to its collection. Rather, the acquirer shall do both of the following: [FAS 164, paragraph 39, sequence 39.1]

a. Recognize the cost of the collection items purchased (either by the transfer of consideration or the assumption of liabilities in excess of assets acquired) as a decrease in the appropriate class of net assets in the statement of activities and as a cash outflow for investing activities [FAS 164, paragraph 39, sequence 39.1.1]

b. Not recognize the fair value of collection items contributed—either as an asset or as contribution revenue. [FAS 164, paragraph 39, sequence 39.1.2]

958-805-25-24 An acquired item that is not added to the acquirer’s collection shall be recognized as an asset in accordance with paragraph 805-20-25-1. [FAS 164, paragraph 39, sequence 39.2]

958-805-25-25 Example 1 (see paragraphs 958-805-55-49 through 55-50) and Example 2 (see paragraphs 958-805-55-51 through 55-54) provide guidance on determining whether an acquired collection item is purchased or contributed and, if purchased, the appropriate amount of cost to attribute to it. [FAS 164, paragraph 39, sequence 39.2]

> > > Conditional Promises to Give

958-805-25-26 An NFP acquirer shall apply the guidance in paragraphs 958-605-25-11 through 25-15 to account for conditional promises to give. That guidance requires the acquirer to do either of the following: [FAS 164, paragraph 40, sequence 40.1]

- Recognize a conditional promise only if the conditions on which it depends are substantially met as of the acquisition date [FAS 164, paragraph 40, sequence 40.1.1]

- Recognize a transfer of assets with a conditional promise to contribute them as a refundable advance unless the conditions have been substantially met as of the acquisition date. [FAS 164, paragraph 40, sequence 40.1.2]

> Recognizing Goodwill Acquired or a Contribution Received, Including Consideration Transferred

958-805-25-27 An NFP acquirer applies the guidance in this Subsection instead of

Subtopic 805-30 for the recognition of the following items:

- Goodwill acquired, whether recognized as an asset or as an immediate charge to the statement of activities

- A contribution received in an acquisition

- Consideration transferred, including contingent consideration.

> > Goodwill Acquired, Whether Recognized as an Asset or as an Immediate Charge to the Statement of Activities

958-805-25-28 Unless the operations of the acquiree are expected to be predominantly supported by contributions and returns on investments (see paragraphs 958-805-25-29 through 25-30), an NFP acquirer shall recognize goodwill as of the acquisition date, measured in accordance with paragraph 958-805-30-6. [FAS 164, paragraph 50, sequence 50.1]

958-805-25-29 If the operations of the acquiree as part of the combined entity are expected to be predominantly supported by contributions and returns on investments, an NFP acquirer shall recognize a separate charge in its statement of activities as of the acquisition date, measured in accordance with paragraph 958-805-30-6, rather than goodwill. Predominantly supported by means that contributions and returns on investments are expected to be significantly more than the total of all other sources of revenues. [FAS 164, paragraph 51, sequence 51]

958-805-25-30 An NFP acquirer shall consider all relevant qualitative and quantitative factors in determining the expected nature of the predominant source of support for an acquiree’s operations as part of the combined entity. For example, an NFP acquirer shall consider qualitative and quantitative information about all forms of contributed support, including contributions that are precluded from being recognized or are not required to be recognized in the financial statements (such as certain contributed services and collection items and conditional promises to give). [FAS 164, paragraph 52, sequence 52]

> > A Contribution Received in an Acquisition

958-805-25-31 An NFP acquirer shall recognize an inherent contribution received, measured in accordance with paragraph 958-805-30-8, as a separate credit in its statement of activities as of the acquisition date. [FAS 164, paragraph 54, sequence 54] Example 1 (see paragraphs 958-805-55-49 through 55-50) and Example 6 (see paragraphs 958-805-55-62 through 55-67) illustrate acquisitions with inherent contributions.

> > Consideration Transferred, including Contingent Consideration

958-805-25-32 An NFP acquirer might transfer consideration to the former owner of the acquiree or to a designee of the former owner. The NFP acquirer also might receive assistance from an unrelated third party, which shall be taken into account in measuring the consideration transferred. Examples of potential forms of consideration include any of the following: [FAS 164, paragraph 56, sequence 56.2]

a. Cash [FAS 164, paragraph 56, sequence 56.2.1]

b. Other assets [FAS 164, paragraph 56, sequence 56.2.2]

c. A business or a nonprofit activity of the acquirer [FAS 164, paragraph 56, sequence 56.2.3]

d. Contingent consideration. [FAS 164, paragraph 56, sequence 56.2.4]

958-805-25-33 An asset transferred by an NFP acquirer to an unrelated third party as a required condition of an acquisition shall be accounted for as consideration transferred for the acquiree unless the NFP acquirer retains control over the transferred assets. [FAS 164, paragraph 57, sequence 57.1] Example 4 (see paragraphs 958-805-55-57 through 55-58) illustrates assistance received from a third party.

958-805-25-34 The consideration transferred may include assets or liabilities of the NFP acquirer that have carrying amounts that differ from their fair values at the acquisition date (for example, nonmonetary assets or a business of the acquirer). If so, the NFP acquirer shall recognize the resulting gains or losses, if any, in the statement of activities. However, sometimes the transferred assets or liabilities remain within the combined entity after the acquisition, and the acquirer therefore retains control of them. [FAS 141(R), paragraph 40, sequence 107] An NFP acquirer that retains control over the transferred assets shall not recognize a gain or loss in the statement of activities on assets or liabilities it controls both before and after the acquisition. [FAS 164, paragraph 57, sequence 57.1.2]

958-805-25-35 Examples of asset transfers in which control over the future economic benefits of the transferred assets is retained by the acquirer include all of the following: [FAS 164, paragraph 57, sequence 57.1.3]

a. The assets are transferred to the acquiree rather than to its former owners or are otherwise transferred to a recipient that is controlled by the acquirer. By virtue of its control over the recipient, the acquiring entity has the ability to revoke the transfer or to direct the use of the assets to itself or an affiliate. [FAS 164, paragraph 57, sequence 57.1.3.1]

b. The asset transfer is otherwise revocable, repayable, or refundable. [FAS 164, paragraph 57, sequence 57.1.3.2]

c. The assets are transferred with the stipulation that they be used on behalf of, or for the benefit of, the acquiree, the acquirer, the consolidated entity, or their affiliates. Example 3 (see paragraphs 958-805-55-55 through 55-56) illustrates an asset transfer in which the NFP acquirer retains control over the future economic benefits after the acquisition. [FAS 164, paragraph 57, sequence 57.1.3.3]

> > > Contingent Consideration

958-805-25-36 The consideration an NFP acquirer transfers in exchange for the acquiree includes any asset or liability resulting from a contingent consideration arrangement. The NFP acquirer shall recognize the contingent consideration as part of the consideration transferred in exchange for the acquiree. [FAS 164, paragraph 58, sequence 58]

> Determining What Is Part of the Acquisition Transaction

958-805-25-37 In addition to the examples in paragraph 805-10-25-21, a payment by a former owner of an acquired business that is unrelated to the acquiree, such as a contribution to fund activities of the acquirer or its affiliates that are unrelated to those of the acquiree, is an example of a separate transaction that is not to be included in applying the acquisition method. Those contributions made shall be accounted for in accordance with the guidance in

Subtopic 720-25.

[FAS 164, paragraph 68(d), sequence 68.1.4]

Initial Measurement

Merger of Not-for-Profit Entities

958-805-30-1 The new {Glossary link} not-for-profit entity {Glossary link} (NFP) shall measure the assets and liabilities in its financial statements as of the {Glossary link} merger date {Glossary link} at the amounts reported in the financial statements of the merging entities as of that date prepared in accordance with GAAP, adjusted as necessary in accordance with paragraphs 958-805-30-2 through 30-3. [FAS 164, paragraph 12, sequence 12]

958-805-30-2 The merging entities may have measured assets and liabilities using different methods of accounting in their separate financial statements. The new NFP shall adjust the amounts of those assets and liabilities as necessary to reflect a consistent method of accounting. [FAS 164, paragraph 13, sequence 13.1]

958-805-30-3 However, because the carryover method does not reflect a freshstart measurement, a merger is not an event that permits the election of accounting options that are restricted to the entity’s initial acquisition or recognition of an item (or the reversal of a previous election). Thus, for example, one merging entity’s election to apply the Fair Value Option Subsections of

Subtopic 825-10 for a particular financial asset or liability permits neither the new NFP’s election of the fair value option for other financial assets or liabilities at the merger date nor the reversal of the previous selection of the fair value option.

[FAS 164, paragraph 13, sequence 13.2]

958-805-30-4 The new NFP shall eliminate the effects of any intra-entity transactions on its assets, liabilities, and net assets as of the merger date. [FAS 164, paragraph 14, sequence 14]

Acquisition by a Not-for-Profit Entity

958-805-30-5 A

not-for-profit entity (NFP) that is an

acquirer applies the guidance in this Subsection instead of

Subtopic 805-30 for the measurement of the following items:

- Goodwill acquired, whether recognized as an asset or an immediate charge to the statement of activities

- A contribution received in an acquisition

- Consideration transferred, including contingent consideration.

> Goodwill Acquired, Whether Recognized as an Asset or an Immediate Charge to the Statement of Activities

958-805-30-6 An NFP acquirer shall measure goodwill acquired, including goodwill recognized as an immediate charge to the statement of activities, as of the {Glossary link} acquisition date {Glossary link} as the excess of (a) over (b): [FAS 164, paragraph 50, sequence 50.1]

a. The aggregate of the following: [FAS 164, paragraph 50, sequence 50.1.1]

1. The consideration transferred measured at its acquisition-date fair value (see paragraphs 958-805-30-10 through 30-13) [FAS 164, paragraph 50, sequence 50.1.1.1]

2. The fair value of any {Glossary link} noncontrolling interest {Glossary link} in the {Glossary link} acquiree {Glossary link} [FAS 164, paragraph 50, sequence 50.1.1.2]

3. In an {Glossary link} acquisition by a not-for-profit entity {Glossary link} achieved in stages, the acquisition-date fair value of the acquirer’s previously held {Glossary link} equity interest {Glossary link} in the acquiree. [FAS 164, paragraph 50, sequence 50.1.1.3]

b. The net of the acquisition-date amounts of the {Glossary link} identifiable {Glossary link} assets acquired and the liabilities assumed measured in accordance with Subtopic 805-20 and this Subtopic. [FAS 164, paragraph 50, sequence 50.1.2]

958-805-30-7 The result of the equation in the preceding paragraph will be to measure goodwill or the separate charge to the statement of activities as the excess of liabilities assumed over assets acquired if the acquisition by the NFP meets all of the following criteria: [FAS 164, paragraph 53, sequence 53.4]

a. No consideration is transferred. [FAS 164, paragraph 53, sequence 53.1]

b. There is no noncontrolling interest in an acquiree. [FAS 164, paragraph 53, sequence 53.2]

c. The acquisition was not achieved in stages. [FAS 164, paragraph 53, sequence 53.3]

> A Contribution Received in an Acquisition

958-805-30-8 An {Glossary link} inherent contribution {Glossary link} recognized in accordance with paragraph 958-805-25-31 shall be measured as the excess of the amount in paragraph 958-805-30-6b over the amount in paragraph 958-805-30-6(a). [FAS 164, paragraph 54, sequence 54.1]

958-805-30-9 The inherent contribution received will be measured as the excess of assets acquired over liabilities assumed if the acquisition meets all of the following criteria: [FAS 164, paragraph 55, sequence 55.1.4]

a. That acquisition is effected without the transfer of consideration. [FAS 164, paragraph 55, sequence 55.1.1]

b. There is no noncontrolling interest in an acquiree. [FAS 164, paragraph 55, sequence 55.1.2]

c. The acquisition was not achieved in stages. [FAS 164, paragraph 55, sequence 55.1.3]

Example 6 (see paragraphs 958-805-55-62 through 55-67) illustrates an inherent contribution.

> Consideration Transferred, Including Contingent Consideration

958-805-30-10 The consideration transferred in an acquisition by an NFP shall be measured at fair value, which shall be calculated as the sum of the acquisition-date fair values of the assets transferred by the acquirer and the liabilities incurred by the acquirer. [FAS 164, paragraph 56, sequence 56.1]

958-805-30-11 If the consideration transferred includes assets or liabilities of the NFP acquirer that have carrying amounts that differ from their fair values at the acquisition date, as discussed in paragraph 958-805-25-34, the NFP acquirer shall remeasure the transferred assets or liabilities to their fair values as of the acquisition date. [FAS 141(R), paragraph 40, sequence 107]

958-805-30-12 An NFP acquirer that retains control over the transferred assets as described in paragraphs 958-805-25-33 through 25-34 shall measure those assets and liabilities at their carrying amounts immediately before the acquisition date. [FAS 164, paragraph 57, sequence 57.1.2]

> > Contingent Consideration

958-805-30-13 Contingent consideration shall be measured initially at acquisition-date fair value. [FAS 164, paragraph 58, sequence 58.1]

Subsequent Measurement

Acquisition by a Not-for-Profit Entity

958-805-35-1 The guidance in this Section together with the guidance in paragraph 805-10-35-1 and

Section 805-20-35 applies to a

not-for-profit entity (NFP) that is an

acquirer. This Section provides the following incremental guidance for assets acquired and liabilities assumed or incurred in an

acquisition by a not-for-profit entity:

- Contingent consideration, including contingent consideration arrangements assumed by an acquirer

- Goodwill acquired.

> Contingent Consideration, Including Contingent Consideration Arrangements Assumed by an Acquirer

958-805-35-2 Some changes in the fair value of contingent consideration and contingent consideration arrangements assumed from an acquiree that the acquirer recognizes after the

acquisition date may be the result of additional information about facts and circumstances that existed at the acquisition date that the acquirer obtained after that date. Such changes are measurement period adjustments in accordance with paragraphs 805-10-25-13 through 25-18 and

Section 805-10-30.

[FAS 164, paragraph 80, sequence 80.1]

958-805-35-3 Changes resulting from events after the acquisition date, such as meeting an earnings or other performance target, reaching a specified share price, or reaching a milestone on a research and development project, are not measurement period adjustments. An NFP acquirer shall account for such changes by remeasuring the related asset or liability to fair value at each reporting date until the contingency is resolved and recognizing the changes in fair value in the statement of activities. [FAS 164, paragraph 80, sequence 80.2]

958-805-35-4 Contingent consideration arrangements of an acquiree assumed by the acquirer shall be measured subsequently in accordance with the guidance for contingent consideration arrangements in paragraphs 958-805-35-2 through 35-3. [FAS 164, paragraph 81, sequence 81]

> Goodwill Acquired

958-805-35-5 For guidance on subsequently measuring goodwill recognized in an acquisition of a business or a nonprofit activity, see

Subtopic 350-20.

[FAS 164, paragraph 82, sequence 82.1]

Other Presentation Matters

Merger of Not-for-Profit Entities

958-805-45-1 The {Glossary link} not-for-profit entity {Glossary link} (NFP) resulting from a {Glossary link} merger of not-for-profit entities {Glossary link} is a new reporting entity, with no activities before the {Glossary link} merger date {Glossary link}. Thus, the new NFP’s initial reporting period begins with the merger date, and the merger itself shall not be reported as activity of the new NFP’s initial reporting period. Rather, the combined assets, liabilities, and net assets of the merging entities are included in the statement of position as of the beginning of that initial reporting period, if presented. [FAS 164, paragraph 15, sequence 15]

958-805-45-2 The new NFP’s statement of activities and statement of cash flows for its initial reporting period shall do both of the following: [FAS 164, paragraph 16, sequence 16.1]

- Include in the reported amounts as of the beginning of the period (the opening amounts), such as cash and cash equivalents at the beginning of the period, the combined amounts of the merging entities’ assets, liabilities, and net assets (in total and by classes of net assets) as of the merger date. The following changes shall be reflected in the opening amounts: [FAS 164, paragraph 16, sequence 16.1.1]

- Accounting changes necessary to adjust a merging entity’s financial statements to generally accepted accounting principles (GAAP) in accordance with paragraph 958-805-25-7 [FAS 164, paragraph 16, sequence 16.1.1.1]

- Accounting changes to conform the individual accounting policies of the merging entities in accordance with paragraph 958-805-30-2 [FAS 164, paragraph 16, sequence 16.1.1.2]

- Changes to eliminate intra-entity balances in accordance with paragraph 958-805-30-4. [FAS 164, paragraph 16, sequence 16.1.1.3]

- Report activity from the merger date through the end of the reporting period. [FAS 164, paragraph 16, sequence 16.1.2]

Acquisition by a Not-for-Profit Entity

958-805-45-3 The financial statements of an {Glossary link} acquirer {Glossary link} (the combined entity) shall report an {Glossary link} acquisition by a not-for-profit entity {Glossary link} as activity of the period in which it occurs. [FAS 164, paragraph 70, sequence 70]

> Statement of Activities

958-805-45-4 A not-for-profit entity (NFP) acquirer shall report the excess amount recognized in accordance with the guidance in paragraph 958-805-25-29 as a separate line item on the face of its statement of activities. The separate line item shall be appropriately described, for example, as excess of consideration paid over net assets acquired in acquisition of Entity AB (or as excess of liabilities assumed over assets acquired in acquisition of Entity AB). [FAS 164, paragraph 71, sequence 71.1] Example 5 (see paragraphs 958-805-55-59 through 55-61) illustrates one way an acquirer might present that amount in its statement of activities. [FAS 164, paragraph 71, sequence 71.2]

958-805-45-5 An NFP acquirer shall report the inherent contribution recognized in accordance with paragraph 958-805-25-31 as a separate line item on the face of the statement of activities. The separate line item shall be appropriately described, for example, as excess of assets acquired over liabilities assumed in donation of Entity XY or as contribution received in donation of Entity XY. In another situation, that excess might be described as excess of fair value of net assets acquired over consideration paid in acquisition of Entity XY. [FAS 164, paragraph 72, sequence 72.1]

958-805-45-6 An NFP acquirer shall classify the inherent contribution received presented in accordance with the preceding paragraph on the basis of the type of restrictions imposed on the related net assets. In classifying those net assets, an acquirer shall do both of the following: [FAS 164, paragraph 73, sequence 73.1]

a. Include restrictions imposed on the net assets of the

acquiree by a donor before the acquisition and those imposed by the donor of the

business or

nonprofit activity acquired, if any, in accordance with

Section 958-605-45.

[FAS 164, paragraph 73, sequence 73.1.1] b. Report donor-restricted contributions as restricted support even if the restrictions are met in the same reporting period in which the acquisition occurs. That is, the acquirer shall not apply the reporting exception in paragraph 958-605-45-4 to restricted net assets acquired in an acquisition. [FAS 164, paragraph 73, sequence 73.1.2]

958-805-45-7 Thus, the inherent contribution received may increase permanently restricted net assets, temporarily restricted net assets, unrestricted net assets, or some combination of those items. Example 6 (see paragraphs 958-805-55-62 through 55-67) illustrates the application of the preceding paragraph’s guidance on reporting donor-imposed restrictions on an inherent contribution received. [FAS 164, paragraph 73, sequence 73.2]

958-805-45-8 An NFP acquirer that transfers assets as consideration for an acquired nonprofit activity or business shall assess whether that transaction satisfies a donor-imposed restriction (see the following paragraph) or otherwise results in a change in its net asset classifications (see paragraph 958-805-45-10). [FAS 164, paragraph 74, sequence 74.1]

958-805-45-9 For example, transferring consideration in an acquisition might satisfy a donor-imposed restriction on the acquirer’s net assets that were restricted for acquisition of land, buildings, works of art, or other long-lived assets if the acquiree has the qualifying assets. If so, the acquirer may either report the expiration of those restrictions separately or aggregate and report them together with other similar expirations of donor-imposed restrictions during the period in which the acquisition occurs. [FAS 164, paragraph 74, sequence 74.1.1.]

958-805-45-10 If transferring consideration results in changes in net asset classifications other than those described in the preceding paragraph, an NFP acquirer shall report those changes separately from both any other reclassifications and any expiration of those restrictions during the period in which the acquisition occurs. For example, an acquirer that transfers as consideration its unrestricted assets and acquires assets from the acquiree that have permanent or temporary donor restrictions shall recognize a reclassification in its statement of activities. [FAS 164, paragraph 74, sequence 74.1.2]

> Statement of Cash Flows

958-805-45-11 An NFP acquirer shall report the entire amount of any net cash flow related to an acquisition (cash paid as consideration, if any, less acquired cash of the acquiree) in the statement of cash flows as an investing activity. [FAS 164, paragraph 75, sequence 75.1] Example 7 (see paragraphs 958-805-55-68 through 55-70) illustrates this requirement. [FAS 164, paragraph 75, sequence 75.2]

Disclosure

Merger of Not-for-Profit Entities

958-805-50-1 The new {Glossary link} not-for-profit entity {Glossary link} (NFP) shall disclose information that enables users of its financial statements to evaluate the nature and financial effect of the {Glossary link} merger of not-for-profit entities {Glossary link} that resulted in its formation. [FAS 164, paragraph 17, sequence 17]

958-805-50-2 To meet the objective in the preceding paragraph, the new NFP shall disclose the following information for the merger that resulted in its formation: [FAS 164, paragraph 18, sequence 18.1]

a. The name and a description of each merging entity [FAS 164, paragraph 18, sequence 18.1.1]

b. The merger date [FAS 164, paragraph 18, sequence 18.1.2]

c. The primary reasons for the merger [FAS 164, paragraph 18, sequence 18.1.3]

d. Both of the following for each merging entity: [FAS 164, paragraph 18, sequence 18.1.4]

1. The amounts recognized as of the merger date for each major class of assets and liabilities and each class of net assets [FAS 164, paragraph 18, sequence 18.1.4.1]

2. The nature and amounts, if applicable, of any significant assets (for example, conditional promises receivable or collections) or liabilities (for example, conditional promises payable) not otherwise required to be recognized under generally accepted accounting principles (GAAP). [FAS 164, paragraph 18, sequence 18.1.4.2]

e. The nature and amount of any significant adjustments made to conform the individual accounting policies of the merging entities or to eliminate intra-entity balances. [FAS 164, paragraph 18, sequence 18.1.5]

958-805-50-3 If the new NFP is a public entity and the merger occurs at other than the beginning of an annual reporting period (that is, if its initial financial statements thus cover less than an annual reporting period), the new NFP shall disclose all of the following supplemental pro forma information: [FAS 164, paragraph 18(f), sequence 18.1.6]

- Revenue [FAS 164, paragraph 18(f), sequence 18.1.6.1.1] for the current reporting period as though the merger date had been the beginning of the annual reporting period [FAS 164, paragraph 18(f), sequence 18.1.6.1]

- Changes in unrestricted net assets, changes in temporarily restricted net assets, and changes in permanently restricted net assets for the current reporting period as though the merger date had been the beginning of the annual reporting period. [FAS 164, paragraph 18(f), sequence 18.1.6.1.3]

958-805-50-4 If the new NFP is a public entity and it presents comparative financial information in the annual reporting period following the year in which the merger occurs, it shall disclose the supplemental pro forma information in the preceding paragraph for the comparable prior reporting period as though the merger date had been the beginning of that prior annual reporting period. [FAS 164, paragraph 18(f), sequence 18.1.6.2]

958-805-50-5 If disclosure of any of the information required by paragraphs 958-805-50-2 through 50-3 is impracticable, the new NFP shall disclose that fact and explain why the disclosure is impracticable. The term impracticable has the same meaning as impracticability in paragraph 250-10-45-9. [FAS 164, paragraph 18(f), sequence 18.1.6.3]

958-805-50-6 If the specific disclosures required by this Subsection do not meet the objective in paragraph 958-805-50-1, the new NFP shall disclose whatever additional information is necessary to meet that objective. [FAS 164, paragraph 19, sequence 19]

Acquisition by a Not-for-Profit Entity

958-805-50-7 To meet the objective in the paragraph 805-10-50-1, an NFP acquirer shall disclose the information required by paragraph 805-10-50-2(a) through (g). [FAS 164, paragraph 86, sequence 86.1]

958-805-50-8 Instead of disclosing the information in paragraph 805-10-50-2(h), an NFP acquirer that is a public entity shall disclose all of the following information for each acquisition that occurs during the reporting period: [FAS 164, paragraph 86(t), sequence 86.1.3.2]

- Revenues [FAS 164, paragraph 86(t), sequence 86.1.3.2.1.1] attributable to the acquiree since the acquisition date that are included in the statement of activities for the reporting period [FAS 164, paragraph 86(t), sequence 86.1.3.2.1]

- Changes in unrestricted net assets, changes in temporarily restricted net assets, and changes in permanently restricted net assets attributable to the acquiree since the acquisition date that are included in the statement of activities for the reporting period [FAS 164, paragraph 86(t), sequence 86.1.3.2.1.3]

- The revenues of the combined entity [FAS 164, paragraph 86(t), sequence 86.1.3.2.2.1] as though the acquisition date for all acquisitions that occurred during the current year had been at the beginning of the annual reporting period (supplemental pro forma information) [FAS 164, paragraph 86(t), sequence 86.1.3.2.2]]

- Changes in unrestricted net assets, changes in temporarily restricted net assets, and changes in permanently restricted net assets as though the acquisition date for all acquisitions that occurred during the current year had been at the beginning of the annual reporting period (supplemental pro forma information). [FAS 164, paragraph 86(t), sequence 86.1.3.2.2.3]

958-805-50-9 If it presents comparative financial information, an NFP acquirer that is a public entity shall disclose the supplemental pro forma information required by the preceding paragraph for the comparable prior reporting period as though the acquisition date for all acquisitions that occurred during the current year had been the beginning of the comparable annual reporting period. [FAS 164, paragraph 86(t), sequence 86.1.3.2.3]

958-805-50-10 If the disclosure of any of the information required by paragraphs 958-805-50-8 through 50-9 is impracticable, the NFP acquirer shall disclose that fact and explain why the disclosure is impracticable. The term impracticable has the same meaning as impracticability in paragraph 250-10-45-9. [FAS 164, paragraph 86(t), sequence 86.1.3.2.4]

958-805-50-11 Instead of the information required by

Section 805-30-50, an NFP acquirer shall disclose the following information for each acquisition that occurs during the reporting period:

[FAS 164, paragraph 86, sequence 86.1]

a. A qualitative description of the factors, such as expected synergies from combining operations of the acquiree and the acquirer, intangible assets that do not qualify for separate recognition, or other factors, such as the nonrecognition of collections, that make up either of the following: [FAS 164, paragraph 86(e), sequence 86.1.1.5]

1. The goodwill recognized [FAS 164, paragraph 86(e), sequence 86.1.1.5.1]

2. The separate charge recognized in the statement of activities in accordance with paragraph 958-805-25-29. [FAS 164, paragraph 86(e), sequence 86.1.1.5.2]

b. The acquisition-date fair value of the total consideration transferred (or if no consideration was transferred, that fact) and the acquisition-date fair value of each major class of consideration, such as: [FAS 164, paragraph 86(f), sequence 86.1.1.6]

1. Cash [FAS 164, paragraph 86(f), sequence 86.1.1.6.1]

2. Other tangible or intangible assets, including a business or subsidiary of the acquirer [FAS 164, paragraph 86(f), sequence 86.1.1.6.2]

3. Liabilities incurred, for example, a liability for contingent consideration. [FAS 164, paragraph 86(f), sequence 86.1.1.6.3]

c. For contingent consideration arrangements, all of the following: [FAS 164, paragraph 86(g), sequence 86.1.1.7]

1. The amount recognized as of the acquisition date [FAS 164, paragraph 86(g), sequence 86.1.1.7.1]

2. A description of the arrangement and the basis for determining the amount of the payment [FAS 164, paragraph 86(g), sequence 86.1.1.7.2]

3. An estimate of the range of outcomes (undiscounted) or, if a range cannot be estimated, that fact and the reasons why a range cannot be estimated. If the maximum amount of the payment is unlimited, the acquirer shall disclose that fact. [FAS 164, paragraph 86(g), sequence 86.1.1.7.3]

d. The total amount of goodwill that is expected to be deductible for tax purposes. [FAS 164, paragraph 86(l), sequence 86.1.2.3]

e. If the acquisition results in an inherent contribution received, a description of the reasons why the transaction resulted in a contribution received (see paragraph 958-805-25-31). [FAS 164, paragraph 86(q), sequence 86.1.2.8]

958-805-50-12 Additionally, an NFP acquirer shall disclose the following information for each acquisition that occurs during the reporting period: [FAS 164, paragraph 86, sequence 86.1]

a. The amount of collection items acquired that are recognized in the statement of activities as a decrease in the acquirer’s net assets in accordance with paragraph 958-805-25-23. [FAS 164, paragraph 86(m), sequence 86.1.2.4]

b. The undiscounted amount of conditional promises to give acquired or assumed and a description and the amount of each group of promises with similar characteristics, such as amounts of promises conditioned on establishing new programs, completing a new building, or raising matching gifts by a specified date. [FAS 164, paragraph 86(n), sequence 86.1.2.5]

958-805-50-13 For individually immaterial acquisitions occurring during the reporting period that are material collectively, the NFP acquirer shall disclose the information required by paragraphs 958-805-50-8 through 50-12 and paragraph 805-10-50-2(e) through (g) in the aggregate. [FAS 164, paragraph 87, sequence 87]

958-805-50-14 If the date of an acquisition is after the reporting date but before the financial statements are issued or available for issue, the NFP acquirer shall disclose the information required by paragraphs 958-805-50-7 through 50-12 unless the initial accounting for the acquisition is incomplete at the time the financial statements are issued or available for issue. In that situation, the acquirer shall describe which disclosures could not be made and the reason why they could not be made. [FAS 164, paragraph 88, sequence 88]

958-805-50-15 An NFP acquirer shall disclose any noncash contributions received and any other noncash amounts received or transferred in relation to an acquisition as noncash activities in accordance with paragraph 230-10-50-3. Example 7 (see paragraphs 958-805-55-68 through 55-70) illustrates the disclosure of noncash activities. [FAS 164, paragraph 75(b), sequence 75.1.2]

958-805-50-16 To meet the objective in paragraph 805-10-50-5, an NFP acquirer shall disclose the information in this paragraph and paragraph 805-10-50-6 for each material acquisition or in the aggregate for individually immaterial business combinations that are material collectively. [FAS 164, paragraph 90, sequence 90.1] For each reporting period after the acquisition date until the NFP acquirer collects, sells, or otherwise loses the right to a contingent consideration asset, or until the NFP acquirer settles a contingent consideration liability or the liability is cancelled or expires, the NFP acquirer shall disclose all of the following: [FAS 164, paragraph 90(b), sequence 90.1.2]

- Any changes in the recognized amounts, including any differences arising upon settlement [FAS 164, paragraph 90(b), sequence 90.1.2.1]

- Any changes in the range of outcomes (undiscounted) and the reasons for those changes [FAS 164, paragraph 90(b), sequence 90.1.2.2]

- The disclosures required by paragraphs 820-10-50-1 through 50-3. [FAS 164, paragraph 90(b), sequence 90.1.2.3]

958-805-50-17 An NFP acquirer shall provide a reconciliation of the carrying amount of goodwill at the beginning and end of the reporting period as required by paragraph 350-20-50-1 for each material acquisition or in the aggregate for individually immaterial acquisitions that are material collectively. [FAS 164, paragraph 90(c), sequence 90.1.3]

Implementation Guidance and Illustrations

General

> Implementation Guidance

> > Distinguishing between a Merger and an Acquisition

958-805-55-1 This implementation guidance addresses the application of the definitions merger of not-for-profit entities and acquisition by a not-for-profit entity in making the determination required by paragraph 958-805-25-1 as to whether a transaction is a merger or an acquisition. Ceding control to a new NFP is the sole definitive criterion for identifying a merger, and one entity obtaining control over the other is the sole definitive criterion for an acquisition. [FAS 164, paragraph A4, sequence 105.1] If the participating entities in a combination retain shared control of the new not-for-profit entity (NFP), they have not ceded control. To qualify as a new NFP, the combined entity must have a newly formed governing body; a new NFP often is, but need not be, a new legal entity. The formation of a new NFP is not a pertinent factor in assessing whether one entity has obtained control over another. [FAS 164, paragraph A2, sequence 103.2]

958-805-55-2 Other transaction-specific characteristics can help in determining whether a particular combination is a merger, an acquisition, or another form of combination, such as the formation of a joint venture. The other characteristics, discussed in paragraphs 958-805-55-3 through 55-8, are indicators that often may help in identifying a merger. The participating entities should consider all of those characteristics and any other pertinent factors. Based on the preponderance of the evidence, the parties must make a professional judgment about whether each of the governing bodies has ceded control of those entities to create a new NFP, whether one entity has acquired the other, or whether another form of combination, such as the formation of a joint venture, has occurred. [FAS 164, paragraph A4, sequence 105.2]

958-805-55-3 Determining whether each of the governing bodies of the entities participating in a combination cede control of those entities to a new NFP requires assessing the characteristics of all of the following: [FAS 164, paragraph A5, sequence 106.1]

a. The process leading to the combination [FAS 164, paragraph A5, sequence 106.1.1]

b. The participants to the combination [FAS 164, paragraph A5, sequence 106.1.2]

c. The combined entity. [FAS 164, paragraph A5, sequence 106.1.3]

958-805-55-4 In a merger, generally no one party dominates or is capable of dominating the negotiations and process leading to the formation of the combined entity. In an acquisition, on the other hand, one party—the acquirer— often dominates that process, and sometimes may in effect dictate the terms of the transaction, including the date the combination occurs. [FAS 164, paragraph A6, sequence 107]

958-805-55-5 The characteristics of the entities participating in a combination and of the resulting combined entity that can help to distinguish between a merger and an acquisition fit into the following two groups: [FAS 164, paragraph A7, sequence 108.1]

a. Governance and related control powers [FAS 164, paragraph A7, sequence 108.1.1]

b. Financial capacity. [FAS 164, paragraph A7, sequence 108.1.2]

958-805-55-6 For example, one entity appointing significantly more of the governing board of the newly formed entity, retaining significantly more of its key senior officers, or retaining its bylaws, operating policies, and practices substantially unchanged is more likely to be a feature of an acquisition than of a merger. Similarly, the relative financial strength and relative size of the participants in the combination may help to determine whether one participant is able to dominate the process leading to the combination. For example, if one entity is financially strong and the other is experiencing financial difficulty, the stronger entity may be able to dominate the transaction, which would indicate that the transaction is an acquisition rather than a merger. Similarly, a participant that is substantially larger than each of the others in terms of revenues, assets, and net assets may be able to dominate the transaction. However, relative size, like relative financial strength and the other indicators discussed, is only one characteristic that may help to distinguish between a merger and an acquisition in particular situations—none of the indicators, by itself, is determinative. As discussed in paragraph 958-805-55-1, ceding of control is the sole definitive criterion for a merger. [FAS 164, paragraph A7, sequence 108.2]

958-805-55-7 Unlike an acquisition by a not-for-profit entity, a merger generally is accomplished by combining all of the assets and liabilities of the merging entities into a newly formed entity that assumes all of the assets and liabilities of the participating entities without a transfer of cash or other assets to those entities or any of their owners, members, sponsors, or other designated beneficiaries. Also, unlike the formation of a joint venture in which the venturers continue to exist and usually hold a financial interest, the creators of the merged entity cease to exist as autonomous entities and no one holds financial interests in the merged entity. Moreover, the merged entity generally has a perpetual life rather than a life that is limited by the period of the venture or that allows for one or more of the participating entities to opt out of the venture or other arrangement. [FAS 164, paragraph A8, sequence 109]

958-805-55-8 A particular combination of business entities may seem similar in some aspects to a merger of not-for-profit entities. For example, a new entity may be formed to effect a business combination, and no consideration is exchanged in some business combinations. Nevertheless, the guidance in this Subtopic on mergers does not apply in a business combination, and it shall not be applied by analogy. [FAS 164, paragraph A9, sequence 110]

> Illustrations

> > Example 1: Assessing Whether a Combination Is a Merger or Is neither a Merger nor an Acquisition

958-805-55-9 This Example has two Cases, which share the assumptions in paragraphs 958-805-55-10 through 55-14. The Cases illustrate the application of paragraph 958-805-25-1, which requires an NFP to determine whether a transaction or other event is a merger or acquisition, and the related implementation guidance in paragraphs 958-805-55-1 through 55-8. The Cases are:

- A combination that is a merger (Case A)

- A combination that is neither a merger nor an acquisition (Case B).

958-805-55-10 A community foundation that is a major grantor to social service entities in its metropolitan area begins a program to encourage its grantees to consider opportunities to improve their services through collaborative arrangements, including mergers, acquisitions, and joint ventures. In January 20X9, the community foundation convenes a meeting of the chief officers and chairpersons of several charities that provide complementary and, to some extent, overlapping services within its metropolitan area. Following that meeting, representatives of Charity A and Charity B see fruitful opportunities for collaborative efforts based on their geographic proximity and service areas; similar missions, programs, and operating practices; and complementary financial strengths with one having a much larger base of current contributors and unpaid volunteers and the other having a larger endowment and base of investment income. Charity A is 30 to 40 percent larger than Charity B in terms of most individual financial measures, including revenues and the fair value of assets and net assets. [FAS 164, paragraph A11, sequence 112]

958-805-55-11 In February 20X9, the governing boards of Charity A and Charity B authorize the formation of an exploratory committee to recommend whether the two charities should combine and, if so, to develop a plan for implementing a combination. The committee consists of three members from Charity A and the executive director and one additional member from Charity B, with administrative support from the legal counsel of each entity. Each of the five committee members has one vote, and a recommendation of the committee requires at least four votes of the members. Its recommendation is to be accompanied by the reasons underlying both the recommendation of the committee and any dissenting votes. [FAS 164, paragraph A12, sequence 113]

958-805-55-12 In July 20X9, after completing its discussions, the committee recommends, with the full support of all five of its members, that Charity A and Charity B combine under an agreement with the following key provisions: [FAS 164, paragraph A13, sequence 114.1]

a. A new NFP named Charity AB is to be formed. [FAS 164, paragraph A13(a), sequence 114.1.1]

b. The chief executive officer of Charity B will be offered the position of chief executive officer of Charity AB for a term of at least two years. [FAS 164, paragraph A13(c), sequence 114.1.3]

c. The initial Board of Charity AB will consist of 15 members. [FAS 164, paragraph A13(d), sequence 114.1.4] Charity A will appoint 9 of the initial members, preferably from the members of its existing 25-member board and its current chief executive officer. [FAS 164, paragraph A13(d), sequence 114.1.4.1] Charity B will appoint 6 of the initial members, preferably from its existing 50-member board. [FAS 164, paragraph A13(d), sequence 114.1.4.2]

d. The charter of Charity AB will provide for a maximum of 25 board members. The committee recommended that a search be undertaken to add 6 new members within a year, with each new member requiring approval by a minimum of 10 of the 15 initial members. [FAS 164, paragraph A13(d), sequence 114.1.4.3]

e. The headquarters of Charity A and its underlying lease (which has eight remaining years) will be retained. [FAS 164, paragraph A13(e), sequence 114.1.5]

f. A transition committee consisting of two members each from the current boards of Charity A and Charity B, under the authority of the chief executive officer of Charity AB, will be appointed to perform the following duties: [FAS 164, paragraph A13(f), sequence 114.1.6]

1. Submit a formal plan of merger to each of the governing boards and, if approved, seek approval from the appropriate state authorities. [FAS 164, paragraph A13(f), sequence 114.1.6.1]

2. Seek opportunities to sublease the headquarters space of Charity B for the remaining two-year lease term or to utilize that space for program activities. [FAS 164, paragraph A13(f), sequence 114.1.6.2]

3. Interview existing staff and other candidates for senior management positions. [FAS 164, paragraph A13(f), sequence 114.1.6.3]

4. Make recommendations about each of the following: [FAS 164, paragraph A13(f), sequence 114.1.6.4]

i. Eliminating program and operating redundancies, including severance packages for any terminated staff. [FAS 164, paragraph A13(f), sequence 114.1.6.4.1]

ii. Improving the current operating policies and practices of Charity A and Charity B. [FAS 164, paragraph A13(f), sequence 114.1.6.4.2]

iii. Revising employee benefit plans with the objective of adopting unified plans for Charity AB’s employees without diminishing the overall benefits being offered to existing employees. [FAS 164, paragraph A13(f), sequence 114.1.6.4.3]

958-805-55-13 In discussing revisions of employee benefit plans, the exploratory committee’s report notes that the committee interviewed the current chief executive officers of Charity A and Charity B and found both well qualified to serve as the chief executive officer of Charity AB. However, although both chief executive officers are in their early 60s and are eager to assist Charity AB through the initial transition period, the chief executive officer of Charity A had been contemplating retiring within the next year. The committee saw no need to open the chief executive officer search to other candidates. [FAS 164, paragraph A14, sequence 115]

958-805-55-14 During August 20X9, each of the governing boards of Charity A and Charity B tentatively approves the committee recommendations [FAS 164, paragraph A15, sequence 116.1] and appoints its members to the recommended transition committee. The boards also asked their respective nominating committees to make recommendations to each of their boards about the initial members to be appointed to the board of Charity AB. During October, each board approved the plan for their combination, and it was submitted to the state for approval. During November, the plan received the required state approval, and the combination became effective on January 1, 20X0, as proposed. [FAS 164, paragraph A15, sequence 116.2]

> > > Case A: A Combination That Is a Merger

958-805-55-15 In this Case, the executive committee recommends [FAS 164, paragraph A13(a), sequence 114.1] (and each of the governing boards of Charity A and B approves) [FAS 164, paragraph A15, sequence 116.1] that to minimize costs the corporate charter of Charity A is to be retained as the charter of Charity AB. The assets and liabilities of Charity B are to be transferred to Charity AB and Charity B will cease to exist. [FAS 164, paragraph A13(a), sequence 114.1.1.1] On the date the merger becomes effective (as approved by the appropriate state official), the corporate charter will be amended to reflect the new NFP’s name and its expanded mission, which is to encompass Charity B’s research and advocacy functions as well as the charitable functions of both entities. [FAS 164, paragraph A13(b), sequence 114.1.2] Thus, in effect, both Charity A and Charity B will cease to exist in their precombination forms. [FAS 164, paragraph A13(a), sequence 114.1.1.2]

958-805-55-16 Paragraph 958-805-55-4 describes the assessments required when determining whether each of the governing bodies of the participating entities in a combination cedes control of those entities to a new NFP. On the basis of the evidence, both Charity A and Charity B participated in the process leading to the combination. Moreover, the evidence indicates that neither charity was experiencing financial difficulties or other circumstances that might allow the other entity to dominate the negotiations leading to and through the approval of the transaction by both charities. Neither charity appointed significantly more of Charity AB’s initial governing board. Although the chief executive officer of Charity B is the only key senior officer for which a retention decision has been made, neither charity dominated the selection process of the governing board and senior management, collectively. Lastly, although the corporate charter and bylaws of Charity A were retained, the stated mission of Charity AB includes the operating objectives of Charity B. In addition, the bylaws and operating policies and practices of Charities A and B were similar. Thus, on the basis of the preponderance of the evidence, it is determined that the combination is a merger—that the governing boards of Charity A and Charity B each ceded control to the new NFP, Charity AB, which has a newly formed governing body. [FAS 164, paragraph A16, sequence 117]

> > > Case B: A Combination That Is neither a Merger nor an Acquisition

958-805-55-17 In this Case, Charity AB is established as a new legal entity with its own charter. [FAS 164, paragraph A17, sequence 118] Charity A and Charity B will each continue to exist with its current governing body but cease to operate its existing programs. [FAS 164, paragraph A17(a), sequence 118.1.1] Each has the power to veto nominations for future members of Charity AB’s governing body for two years. [FAS 164, paragraph A17(b), sequence 118.1.2] Each will retain $200,000 in operating cash and all of the investment assets of its donor-restricted endowment funds. [FAS 164, paragraph A17(c), sequence 118.1.3.1]

958-805-55-18 Charity A and Charity B each have the right to dissolve Charity AB. If the right is exercised, it will result in a reversion of assets, liabilities, and staff. Upon reversion, all staff will be retained by their respective legacy entity. In addition, the assets and liabilities of Charity AB will be transferred to each legacy entity in a distribution ratio equivalent to the fair value of the net assets contributed by each (which was determined to be about 65:35 at the combination date). [FAS 164, paragraph A17(d), sequence 118.1.4] Two years following the combination date, Charity A and Charity B will dissolve and transfer their remaining assets to Charity AB unless either exercises its right of withdrawal. [FAS 164, paragraph A17(c), sequence 118.1.3.2]

958-805-55-19 In this Case, it appears that Charity A and Charity B may intend to combine after the passage of a two-year period. But neither of their governing boards has ceded control, as defined, and neither entity has obtained control of the other. Therefore, the combination is neither a merger nor an acquisition; rather, on the basis of the preponderance of the evidence, it appears that Charity AB is a joint venture of Charity A and Charity B. [FAS 164, paragraph A18, sequence 119]

> > Example 2: A Combination That Is an Acquisition

958-805-55-20 Charity C provides health and human services to residents of City and two adjoining counties, referred to as Metro Area, a substantial portion of which is provided through its support to grantee agencies in its area. Charity D provides health and human services to residents of County, which adjoins the northern part of Metro Area. The charities share a common mission and operate under the same national brand name; that is, the charities operate as Brand Name of Metro Area and Brand Name of County. Each charity receives contributions from the residents of its service area. [FAS 164, paragraph A19, sequence 120]

958-805-55-21 In 20X1, the regions served by both charities were experiencing sharp economic declines, and contributions to both charities were declining as a result. To create efficiencies, the charities entered into two joint operating agreements. Under the first agreement, they conduct joint annual fundraising campaigns. Under the second, Charity C provides all information technology and marketing services to Charity D for a nominal fee. [FAS 164, paragraph A20, sequence 121]

958-805-55-22 By January 20X4, Charity D has successfully implemented three innovative program services, but it has not been able to improve its declining contribution revenues. Despite some staff layoffs, it continues to experience significant operating deficits. In March 20X4, the chief executive officers of the two charities encouraged their respective executive committees to explore opportunities to combine and restructure their operations and governance. In July 20X4, the executive committees of both charities formed a joint strategy committee to investigate opportunities to create the best charity for the combined service area and to develop recommendations for accomplishing that objective. [FAS 164, paragraph A21, sequence 122.1]

958-805-55-23 The strategy committee members include the chief executive officers and 6 directors from each charity and 10 community leaders from the area. It is chaired by the chief executive officer of a major corporation in the area who also is a director of Charity C. In January 20X5, although the strategy committee’s work was ongoing, the executive committees of both charities unanimously approved and advanced to the full governing board of each charity the committee’s recommendations for the governance model for a new charity to be formed by consolidating and dissolving both of the existing charities and its recommendations for the new charity’s name, mission, vision, and business model. That business model is the same as the model Charity D had adopted in 20X2, under which it successfully implemented three new programs. Charity C wanted to leverage the experiences of Charity D. [FAS 164, paragraph A21, sequence 122.2]

958-805-55-24 On November 1, 20X5, the governing boards of both charities approved the strategy committee’s plan of consolidation. The chief executive officers of both charities executed a joint memorandum of understanding, which includes the following statements: [FAS 164, paragraph A22, sequence 123.1]

- The charities will create a new NFP named Charity E upon completing the due diligence process and obtaining approvals of the state authorities and Internal Revenue Service (IRS) qualification as a tax exempt public charity, which will be concluded no later than December 31, 20X5. Charity E incorporates Charity C’s name into its own. [FAS 164, paragraph A22, sequence 123.1.1]

- The bylaws of Charity E will establish a board of directors of up to 30 members. [FAS 164, paragraph A22, sequence 123.1.2]

- The board of directors of Charity C will nominate 15 of the initial members of the board of Charity E. (All 15 nominees selected were current members of the board of directors of which 13 were also members of the executive committee.) The board of directors of Charity D will nominate five of the initial members. [FAS 164, paragraph A22, sequence 123.1.3]

- Charity E will have four local community committees representing four geographic areas, one of which is County. Each committee will provide advice to the board of directors for local decision-making consistent with Charity E’s mission and vision. At each election after the installation of the initial board, each local community committee may nominate up to four candidates for a one-year renewable term on the board of Charity E. The board will select a minimum of two members from each local community committee, for a total of eight additional members. [FAS 164, paragraph A22, sequence 123.1.4]

- Amendments to the articles of incorporation or bylaws, significant transactions (a merger, reorganization, termination, or sale of substantially all assets), and reductions in the authority and responsibilities of local community committees will require an affirmative vote of at least 60 percent of the board of directors. [FAS 164, paragraph A22, sequence 123.1.5]

- Each charity’s board of directors will appoint five members to a joint transition committee, with the charge of and authority to implement the plan of consolidation. [FAS 164, paragraph A22, sequence 123.1.6]

- Until the consolidation is complete, each charity’s board of directors agrees to do the following: [FAS 164, paragraph A22, sequence 123.1.7]

- Use reasonable efforts to conduct their activities consistent with their current mission allowing for changes consistent with moving to the business model, mission, and vision of Charity E. [FAS 164, paragraph A22, sequence 123.1.7.1]

- Preserve their tax-exempt status and relationships with contributors and grantee agencies. [FAS 164, paragraph A22, sequence 123.1.7.2]

- ot materially amend or modify their articles of incorporation or bylaws. [FAS 164, paragraph A22, sequence 123.1.7.3]

- During the first three years after the combination, Charity E will do the following: [FAS 164, paragraph A22, sequence 123.1.8]

- Use the business model (direct-services based) to increase its capacity for making sustained change to address key social needs. [FAS 164, paragraph A22, sequence 123.1.8.1]

- Fund and maintain no less than four geographic sites, with one in County, to allow for community involvement in campaign, community impact programs, marketing, and public policy. [FAS 164, paragraph A22, sequence 123.1.8.2]

- Fund and maintain the financial and program commitments of both of the consolidating charities to their respective grantee agencies, subject to available funding. [FAS 164, paragraph A22, sequence 123.1.8.3]

- Strive to expand Brand Name program of Charity D and its strategies throughout Charity E’s service area. Given the success of that program, its current staff will be given full opportunity and consideration to lead the Brand Name program for Charity E. [FAS 164, paragraph A22, sequence 123.1.8.4]

- Not reduce significantly the current staff of the charities. It is understood that reassignments or realignments are probable. Any reductions of the staff of Charity D will be made in consultation with its former chief executive officer, who will become the vice president for program services and strategic development of Charity E. [FAS 164, paragraph A22, sequence 123.1.8.5]

- The obligations of Charity D, which are outlined in the memorandum of understanding, are subject to approval by its board of directors. The obligations of Charity C, which also are outlined in the memorandum of understanding, are subject to approval by its executive committee. [FAS 164, paragraph A22, sequence 123.1.9]

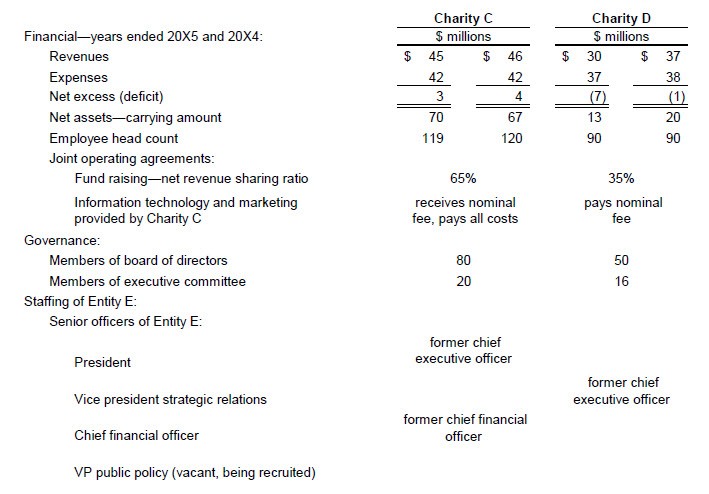

958-805-55-25 The following table summarizes certain facts for each of the combining charities and the initial staffing of the combined Charity E. [FAS 164, paragraph A23, sequence 124.1]

[FAS 164, paragraph A23, sequence 124.2]