9. Amend paragraph 946-10-05-1, with a link to transition paragraph 946-10-65-2, as follows:

Financial Services—Investment Companies—Overall

Overview and Background

946-10-05-1 The Financial Services—Investment Companies Topic includes the following Subtopics:

a. Overall

b. Investment Company Activities

c. Presentation of Financial Statements

d. Balance Sheet

e. Income Statement

f. Statement of Cash Flows

g. Notes to Financial Statements

h. Cash and Cash Equivalents

i. Receivables

j. Investments—Debt and Equity Securities

k. Investments—Equity Method and Joint Ventures

kk. Investments—Other

l. Liabilities

m. Equity

n. Revenue Recognition

o. Income Taxes

p. Consolidation

q. Foreign Currency Matters.

10. Supersede paragraphs 946-10-05-2 through 05-6, with a link to transition paragraph 946-10-65-2, as follows:

946-10-05-2 Paragraph superseded by Accounting Standards Update 2013-08. An investment company, as used in this Topic, generally is an entity that pools shareholders' funds to provide the shareholders with professional investment management. Typically, an investment company sells its shares to the public, invests the proceeds, mostly in securities, to achieve its investment objectives, and distributes to its shareholders the net income earned on its investments and net gains realized on the sale of its investments. In this Topic, the term investment company refers to an entity with the attributes described in paragraph 946-10-15-2. This term is not used to conform with the legal definition of an investment company in the federal securities laws.

[Content amended and moved to paragraph 946-20-05-1A]

946-10-05-3 Paragraph superseded by

Accounting Standards Update 2013-08.

Several kinds of investment companies exist: management investment companies, unit investment trusts, common (collective) trust funds, investment partnerships, certain separate accounts of life insurance companies, and offshore funds. Management investment companies may be open-end funds, usually known as mutual funds, closed-end funds, special purpose funds, venture capital investment companies, small business investment companies, and business development companies. Investment companies are organized as corporations (in the case of mutual funds, under the laws of certain states that authorize the issuance of common shares redeemable on demand of individual shareholders), common law trusts (sometimes called business trusts), limited partnerships, limited liability investment partnerships and companies, and other more specialized entities, such as separate accounts of insurance companies that are not in themselves entities at all except in the technical definition of the Investment Company Act of 1940

.

[Content amended and moved to paragraph 946-20-05-1B]

946-10-05-4 Paragraph superseded by Accounting Standards Update 2013-08.

Once an investment company has been organized to do business, it usually engages immediately in its planned principal operations, that is, the sale of capital stock and investment of funds. Employee training, development of markets for the sale of capital stock, and similar activities are usually performed by the investment adviser or other agent, and the costs of these activities are not borne directly by the investment company. However, an investment company, particularly one not engaging an agent to manage its portfolio and to perform other essential functions, may engage in such activities and may bear those costs directly during its development stage.

[Content moved to paragraph 946-20-05-1C]

946-10-05-5 Paragraph superseded by Accounting Standards Update 2013-08.

Multiple-class funds issue more than one class of shares. Each class of shares typically has a different kind of sales charge, such as a front-end load, contingent-deferred sales load, 12b-1 fee (referring to Rule 12b-1 in Chapter 17 of the Code of Federal Regulations, which implements the Investment Company Act of 1940), or combinations thereof. Multiple-class funds may charge different classes of shares for specific or incremental expenses, such as transferagent, registration, and printing expenses related to each class.

[Content moved to paragraph 946-20-05-1D]

946-10-05-6 Paragraph superseded by Accounting Standards Update 2013-08. Venture capital investment companies, including most small business investment companies, and business development companies differ in operating method from other types of investment companies. The usual open-end or closed-end company is a passive investor, whereas the venture capital investment company is more actively involved with its investees. In addition to providing funds, whether in the form of loans or equity, the venture capital investment company often provides technical and management assistance to its investees as needed and requested. The portfolio of a venture capital investment company may be illiquid by the very nature of the investments, which are usually securities with no public market. Often, gains on those investments are realized over a relatively long holding period. The nature of the investments therefore requires valuation procedures that differ markedly from those used by the typical investment company primarily addressed by this Subtopic. Venture capital investment companies may incur liabilities not generally found in other investment companies.

[Content amended and moved to paragraph 946-20-05-1E]

11. Amend paragraphs 946-10-15-1 through 15-3, with a link to transition paragraph 946-10-65-2, as follows:

Scope and Scope Exceptions

> Overall Guidance

946-10-15-1 The Financial Services—Investment Companies Topic only provides incremental industry-specific guidance for the entities

defined

that meet the assessment of investment company status described in this Scope Section,

or as further defined in the Scope Sections of the individual Financial Services— Investment Companies Subtopics

with the exception of Subtopic 946-605, which has its own discrete scope. Entities within the scope of this Topic also shall also comply with the applicable guidance not included in this Topic. The Scope Section of the Overall Subtopic establishes the pervasive scope for all Subtopics of the Financial Services—Investment Companies Topic. Unless explicitly addressed within specific Subtopics, the following scope guidance applies to all Subtopics of the Financial Services—Investment Companies Topic, with the exception of Subtopic 946-605,

which has its own discrete scope

.

> Entities

946-10-15-2 The accounting principles discussed in this the Financial Services—

Investment Companies Topic apply to all investment companies. Investment companies An investment company as discussed in this Topic

is an entity that meets the assessment described in paragraphs 946-10-15-4 through 15-9. are required to report their investment assets at

fair valueand have the following attributes:

- Subparagraph superseded by Accounting Standards Update 2013-08.Investment activity. The investment company's primary business activity involves investing its assets, usually in the securities of other entities not under common management, for current income, appreciation, or both.

- Subparagraph superseded by Accounting Standards Update 2013-08.Unit ownership. Ownership in the investment company is represented by units of investments, such as shares of stock or partnership interests, to which a proportionate shares of net assets can be attributed.

- Subparagraph superseded by Accounting Standards Update 2013-08.Pooling of funds. The funds of the investment company's owners are pooled to avail owners of professional investment management.

- Subparagraph superseded by Accounting Standards Update 2013-08.Reporting entity. The investment company is the primary reporting entity.

Further, an investment company (other than a separate account of an insurance company as defined in the Investment Company Act of 1940) must be a separate legal entity to be within the scope of the Financial Services—Investment Companies Topic. That is, the guidance in this Topic should be applied only if the investment is held by an investment company that is a separate legal entity. Though many aspects of venture capital investment companies, including small business investment companies and business development companies, differ from aspects of other types of investment companies, the provisions of this Topic generally apply.

946-10-15-3 The guidance in this Topic does not apply to real estate investment trusts

, which have some of the attributes of investment companies but are covered by other generally accepted accounting principles (GAAP)

.

12. Amend paragraphs 946-10-15-4 through 15-6 by adding the following new text and their related heading, with a link to transition paragraph 946-10-65-2, as follows:

> > Assessment of Investment Company Status

946-10-15-4 An entity regulated under the Investment Company Act of 1940 is an investment company under this Topic.

946-10-15-5 An entity that is not regulated under the Investment Company Act of 1940 shall assess all the characteristics of an investment company in paragraphs 946-10-15-6 through 15-7 to determine whether it is an investment company. The entity shall consider its purpose and design when making that assessment.

946-10-15-6 An investment company has the following fundamental characteristics:

a. It is an entity that does both of the following:

1. Obtains funds from one or more investors and provides the investor(s) with investment management services

2. Commits to its investor(s) that its business purpose and only substantive activities are investing the funds solely for returns from capital appreciation, investment income, or both.

b. The entity or its affiliates do not obtain or have the objective of obtaining returns or benefits from an investee or its affiliates that are not normally attributable to ownership interests or that are other than capital appreciation or investment income.

13. Add paragraphs 946-10-15-7 through 15-9, with a link to transition paragraph 946-10-65-2, as follows:

946-10-15-7 An investment company also has the following typical characteristics:

a. It has more than one investment.

b. It has more than one investor.

c. It has investors that are not related parties of the parent (if there is a parent) or the investment manager.

d. It has ownership interests in the form of equity or partnership interests.

e. It manages substantially all of its investments on a {add glossary link to second definition}fair value{add glossary link to second definition} basis.

946-10-15-8 To be an investment company, an entity shall possess the fundamental characteristics in paragraph 946-10-15-6. Typically, an investment company also has all of the characteristics in the preceding paragraph. However, the absence of one or more of those typical characteristics does not necessarily preclude an entity from being an investment company. If an entity does not possess one or more of the typical characteristics, it shall apply judgment and determine, considering all facts and circumstances, how its activities continue to be consistent (or are not consistent) with those of an investment company.

946-10-15-9 The implementation guidance in Section 946-10-55 is an integral part of assessing investment company status and provides additional guidance for that assessment.

14. Add paragraphs 946-10-25-1 through 25-3 and their related heading, with a link to transition paragraph 946-10-65-2, as follows:

Recognition

> Reassessment of Investment Company Status

946-10-25-1 The initial determination of whether an entity is an investment company within the scope of this Topic shall be made upon formation of the entity. An entity shall reassess whether it meets (or does not meet) the assessment of investment company status in paragraphs 946-10-15-4 through 15-9 only if there is a subsequent change in the purpose and design of the entity or if the entity is no longer regulated under the Investment Company Act of 1940.

946-10-25-2 An entity that is no longer an investment company under this Topic as a result of the reassessment of status shall discontinue applying the guidance in this Topic and shall account for the change in its status prospectively by accounting for its investments in accordance with other Topics as of the date of the change in status. The {add glossary link to second definition}fair value{add glossary link to second definition} of an investment at the date of the change in status shall be the investment's initial carrying amount.

946-10-25-3 An entity that subsequently is an investment company under this Topic as result of the reassessment of status shall account for the effect of the change in status from the date of the change in status. The effect of applying this Topic shall be recognized as a cumulative-effect adjustment to net assets at the date of the change in status. The cumulative-effect adjustment shall be included in the net asset value at the beginning of the period in the per-share information included in the financial highlights. The adjustment to net assets represents both of the following:

a. The difference between the fair value and the carrying amount of the entity's investees (or parent's portion of the assets minus liabilities for consolidated investments) at the date of the change in status

b. Any amounts previously recognized in accumulated other comprehensive income.

15. Amend paragraphs 946-10-50-1 through 50-2 by adding the following new text and their related headings, with a link to transition paragraph 946-10-65-2, as follows:

Disclosure

> Investment Company Status

946-10-50-1 An investment company under this Topic shall disclose that it is an investment company following accounting and reporting guidance in this Topic.

> > Change in Status

946-10-50-2 An entity with a change in status (as described in paragraphs 946-10-25-1 through 25-3) shall disclose that a change in status occurred and the reasons for that change.

16. Add paragraph 946-10-50-3, with a link to transition paragraph 946-10-65-2, as follows:

946-10-50-3 An entity that previously was not an investment company under this Topic and becomes an investment company under this Topic shall disclose the effect of the change in status on the reported amounts of investments as of the date of the change in status.

17. Amend paragraphs 946-10-55-1 through 55-45 by adding the following new text and their related headings, with a link to transition paragraph 946-10-65-2, as follows:

Implementation Guidance and Illustrations

> Implementation Guidance

946-10-55-1 This Section provides additional guidance for the assessment in paragraphs 946-10-15-5 through 15-9 to determine whether an entity that is not regulated under the Investment Company Act of 1940 is an investment company under this Topic.

946-10-55-2 This Section is organized as follows:

a. Fundamental characteristics of an investment company

b. Typical characteristics of an investment company

c. Illustrative examples.

> > Fundamental Characteristics of an Investment Company

946-10-55-3 To be an investment company, an entity shall possess the fundamental characteristics in paragraph 946-10-15-6. Paragraphs 946-10-55-4 through 55-10 provide additional guidance for determining whether an entity has the fundamental characteristics of an investment company.

> > > Business Purpose and Substantive Activities

946-10-55-4 An investment company should have no substantive activities other than its investing activities and should not have significant assets or liabilities other than those relating to its investing activities, subject to the exception in the following paragraph.

946-10-55-5 An investment company may provide investing-related services (for example, investment advisory or transfer agent services) to other entities, directly or indirectly through an investment in an entity that provides those services, as long as those services are not substantive. However, an investment company may provide substantive investing-related services, directly or indirectly through an investment in an entity that provides those services, if the substantive services are provided to the investment company only.

> > > > Evidence of an Entity's Business Purpose and Substantive Activities

946-10-55-6 Evidence of the entity's business purpose and substantive activities may be included in the entity's offering memorandum, publications distributed by the entity, and other corporate or partnership documents that indicate the investment objectives of the entity. Evidence of the entity's business purpose and substantive activities also may include the manner in which the entity presents itself to other parties (such as potential investors or potential investees). For example, an entity that presents its business to its investors as having the objective of investing for capital appreciation has characteristics that are consistent with the business purpose and substantive activities of an investment company. Alternatively, an entity that presents itself as an investor whose objective is jointly developing, producing, or marketing products with its investees has characteristics that are inconsistent with the business purpose and substantive activities of an investment company.

946-10-55-7 An entity's investment plans also provide evidence of its business purpose and substantive activities. Accordingly, an investment company whose business purpose and substantive activities include realizing capital appreciation should have an exit strategy for how it plans to realize the capital appreciation of its investments. Although the entity may not yet have determined the specific method or timing of disposing of an investment, the fact that it has identified potential exit strategies through which it can realize capital appreciation provides evidence that its business purpose and substantive activities are consistent with those of an investment company. The entity need not document specific exit strategies for each individual investment held for the purpose of realizing capital appreciation but should identify potential exit strategies for different types or portfolios of investments held with the purpose of realizing capital appreciation. Disposal of investments only during liquidation or to satisfy investor redemptions are not exit strategies. Therefore, an entity should have a plan to dispose of its investments before liquidation when its business purpose and substantive activities include realizing capital appreciation. An investment company whose business purpose and substantive activities are to invest for returns only from investment income does not require an exit strategy for its investments.

> > > Returns or Benefits from Investments

946-10-55-8 An entity would not be an investment company if the entity or its affiliates obtain or have the objective of obtaining returns or benefits from an investee or its affiliates that are not normally attributable to ownership interests or that are other than capital appreciation or investment income. Examples of relationships and activities that would be inconsistent with the characteristics of an investment company include any of the following:

a. The entity or its affiliates acquire, use, exchange, or exploit the processes, assets, or technology of an investee or its affiliates. This includes the entity or its affiliates having disproportionate or exclusive rights to acquire assets, technology, products, or services of an investee or its affiliates (for example, by holding an option to purchase an asset from an investee if the asset's development is deemed successful).

b. There are other arrangements between the entity or its affiliates and an investee or its affiliates to jointly develop, produce, market, or provide products or services.

c. An investee or its affiliates provide financing guarantees or assets to serve as collateral for borrowing arrangements of the entity or its affiliates to provide returns or with the objective of providing returns other than capital appreciation or investment income. The guidance in this paragraph does not prohibit an investment company from using its investments in its investees as collateral for any of its borrowings.

d. An affiliate of the entity holds an option to purchase from the entity ownership interests in an investee at an amount other than {add glossary link to second definition}fair value{add glossary link to second definition}.

e. There are transactions between the entity or its affiliates and an investee or its affiliates that meet any of the following:

1. They are on terms that are unavailable to entities that are not affiliates of the investee.

2. They are not at fair value or are not conducted at arm's length.

3. They represent a substantive portion of the investee's or the entity's business activities, including business activities of affiliates of the entity or affiliates of the investee.

946-10-55-9 An investment company may have a strategy to invest in more than one investee in the same industry, market, or geographical area to benefit from synergies that increase the returns from capital appreciation and investment income from those investments. Transactions between an entity's investees should not affect the entity's assessment of whether it is an investment company unless those transactions result in the entity obtaining returns or benefits other than capital appreciation or investment income.

946-10-55-10 An investment company may provide both of the following services to an investee, either directly or through an investment in an entity that provides those services, only if those services are provided for the purpose of maximizing returns from capital appreciation, investment income, or both (rather than other benefits) and do not represent a separate substantial business activity or separate substantial source of income for the investment company:

a. Assistance with day-to-day management of the operations of an investee

b. Financial support, such as a loan, capital commitment, or guarantee.

> > Typical Characteristics of an Investment Company

946-10-55-11 As required by paragraph 946-10-15-5, an entity shall assess all the typical characteristics in paragraph 946-10-15-7 to determine whether it is an investment company. If an entity does not possess one or more of the typical characteristics, it should apply judgment and determine, considering all facts and circumstances, how its activities continue to be consistent (or are not consistent) with those of an investment company. Paragraphs 946-10-55-12 through 55-29 provide additional guidance for determining whether an entity has a certain typical characteristic of an investment company.

> > > More Than One Investment

946-10-55-12 An investment company typically holds multiple investments at the same time to diversify its risk and maximize its returns from capital appreciation, investment income, or both. Investments typically consist of securities of other entities, but also may include commodities, securities based on indexes, securities sold short, derivative instruments, real estate properties, and other forms of investments.

946-10-55-13 An investment company may hold investments directly or indirectly through another investment company. For example, in a master-feeder structure, a feeder fund holds multiple investments indirectly through its investment in a master fund that holds multiple investments or, in a fund-of-funds structure, an investment company holds multiple investments indirectly through its investment in an underlying fund that holds multiple investments.

946-10-55-14 Holding a single investment does not necessarily preclude an entity from being an investment company. There may be times when an investment company holds a single investment, such as in any of the following examples:

a. It is in its start-up period and has not yet identified suitable investments and, therefore, has not yet executed its investment plan to acquire multiple investments.

b. It has not yet made other investments to replace those it has disposed of.

c. It is in the process of liquidation.

d. It is established to pool investors' funds to invest in a single investment when that investment is unobtainable by individual investors (for example, when the required minimum investment is too high for an individual investor).

946-10-55-15 An investment company with a single investment also may be formed (for legal, regulatory, tax, or other business reasons) in conjunction with another investment company that holds multiple investments (for example, a master-feeder structure or blocker fund). Investment companies formed in conjunction with each other are not required to be formed at the same time. Holding a single investment for that reason does not necessarily preclude an entity from being an investment company.

> > > More Than One Investor

946-10-55-16 An investment company typically pools funds from multiple investors and provides them with investment management services, including access to investment opportunities unobtainable by individual investors. Having multiple investors makes it less likely that the entity or its affiliates obtain or have the objective of obtaining returns or benefits from an investee or its affiliates that are not normally attributable to ownership interests or that are other than capital appreciation or investment income.

946-10-55-17 Having a single investor does not necessarily preclude an entity from being an investment company. There may be times when an investment company has a single investor, such as in any of the following examples:

a. It is in its initial offering period, which has not expired, and it is actively identifying suitable investors.

b. It is actively identifying investors but has not yet identified suitable investors to replace those that have redeemed their ownership interests.

c. It is in the process of liquidation.

946-10-55-18 An investment company may be formed by, or for, a single investor that represents or supports the interests of a wider group of investors (for example, a pension fund, government investment fund, or endowment fund). An investment company with a single investor also may be formed (for legal, regulatory, tax, or other business reasons) in conjunction with another investment company that has multiple investors (for example, a master-feeder structure or a blocker fund). Investment companies formed in conjunction with each other are not required to be formed at the same time. Having a single investor for those reasons does not necessarily preclude an entity from being an investment company.

> > > Investors That Are Not Related Parties of the Parent or Investment Manager

946-10-55-19 An investment company typically has investors that are not related parties of the parent (if there is a parent) or the investment manager. Those unrelated investors, in aggregate, hold a significant interest in the investment company. Having investors that are not related parties of the parent or the investment manager makes it less likely that the entity or its affiliates obtain or have the objective of obtaining returns or benefits from an investee or its affiliates that are not normally attributable to ownership interests or that are other than capital appreciation or investment income.

946-10-55-20 Investors that are related parties of the parent or investment manager should be combined and treated as a single investor, along with the parent or investment manager, for the purposes of evaluating the more-than-one investor characteristic of an investment company in paragraph 946-10-15-7.

946-10-55-21 Having investors that are related parties of the parent or the investment manager does not necessarily preclude an entity from being an investment company. For example, an investment manager may form an investment company for its employees in conjunction with another investment company. Although the employees may be related parties of the investment manager, the investment company formed for its employees mirrors the business purpose and activities of the main investment company.

946-10-55-22 If the parent or its related parties have an implicit or explicit arrangement that would require them to acquire another investor's ownership interest in the investment company at an amount other than fair value, those interests should be combined and treated as if they were owned by the parent for the purposes of evaluating the typical characteristics of an investment company. Examples of when interests would be combined and treated as if they were owned by the parent include any of the following:

a. The parent or its related parties have a written option to acquire another investor's ownership interests in the entity at an amount other than fair value.

b. The parent finances another investor's ownership interests, and the ownership interests are collateral for the debt.

> > > Ownership Interests

946-10-55-23 Ownership interests in an investment company are typically in the form of equity or partnership interests. Each ownership interest represents a specifically identifiable portion of the net assets of the investment company. An investor in an investment company contributes funds to acquire ownership interests, and the value of those interests is dependent on the changes in the fair value of the underlying investments of the investment company.

946-10-55-24 Having multiple classes of equity instruments, such as shares with distinct rights or rights that do not represent a proportionate interest in all of the underlying investments of the investment company, does not preclude an entity from meeting this characteristic of an investment company.

946-10-55-25 An investment company can be but is not required to be a separate legal entity. For example, separate accounts of life insurance companies may not be separate legal entities. However, investors in the separate accounts base their investment decisions on the changes in the fair value of the underlying investments held in those separate accounts.

946-10-55-26 In addition, having significant ownership interests that are not considered equity interests in accordance with other Topics (for example, ownership interests in the form of debt) does not necessarily preclude an entity from being an investment company provided that the holders are exposed to variable returns from changes in the fair value of the underlying investments of the entity. The economic substance of the entity, rather than its legal form, should be evaluated to determine whether the entity has that characteristic of an investment company.

> > > Managing on a Fair Value Basis

946-10-55-27 An investment company typically manages substantially all of its investments on a fair value basis. Determining whether an entity manages its investments on a fair value basis does not depend on the nature of its investments but, rather, includes an evaluation of whether fair value is a key component of any of the following:

a. How the entity evaluates the performance of its investments

b. How the entity transacts with its investors

c. How asset-based fees are calculated.

An investment company's activities typically demonstrate that fair value is the primary measurement attribute used to evaluate the financial performance of and to make investment decisions for substantially all of its investments. Also, an investment company typically transacts with investors on the basis of net asset value per share and incurs asset-based fees, both of which are based on the fair value of its investments.

946-10-55-28 Assets held by an investment company that are used to service the investment company's own investments are not required to be managed on a fair value basis (see paragraph 946-10-55-5).

946-10-55-29 Managing investments on another basis, such as a yield basis or an income basis, does not necessarily preclude an entity from being an investment company. For example, although a short-term investment fund may evaluate the performance of its investments on a yield (amortized cost) basis, fair value is the primary measurement attribute used to evaluate the financial performance of investments and to make investment decisions because the fund monitors the fair value of its investments to minimize the differences between the carrying value and the fair value.

> Illustrations

946-10-55-30 The following Examples illustrate the assessment to determine whether an entity that is not regulated under the Investment Company Act of 1940 is an investment company under this Topic:

a. Example 1: Limited partnership

b. Example 2: Technology fund

c. Example 3: Master-feeder structure.

> > Example 1: Limited Partnership

946-10-55-31 Entity A, a limited partnership, is formed in 20X1 with a 10-yearlife. The offering memorandum provides that Entity A's purpose is to invest in operating entities with rapid growth potential, with the only objective of realizing capital appreciation from investments in those entities over the life of Entity A. One percent of Entity A's capital was contributed by the general partner (the investment manager), who has the responsibility of identifying suitable investments for Entity A. The remaining 99 percent of Entity A's capital was contributed by 75 limited partners, who are not related parties of the general partner.

946-10-55-32 Entity A begins its investment activities in 20X1. However, no suitable investments are identified during that year. In 20X2, Entity A acquires a controlling financial interest in Entity B, a corporation. Entity A is unable to identify suitable investments and complete any other investment purchases until 20X3, at which time it acquires equity interests in five additional operating companies. Other than acquiring those equity interests, Entity A conducts no other activities. Entity A manages and evaluates the performance of its investments on a fair value basis. Information about Entity A's financial results, including changes in the fair value of its investments, are provided by the general partner to the limited partners periodically.

946-10-55-33 Entity A has plans to dispose of its interests in each of its investees during the 10-year stated life of the partnership to realize returns from the capital appreciation of its investees. Those disposals include the sale of the interests for cash or the distribution of marketable equity securities to investors following a successful public offering of an investee's securities.

946-10-55-34 From formation in 20X1 to December 31, 20X3, Entity A has the fundamental characteristics of an investment company because all of the following conditions exist:

a. Entity A obtained funds from investors (the general partner and the limited partners) and is providing those investors with investment management services.

b. Entity A's business purpose and only substantive activity is acquiring interests in operating companies with the objective of realizing returns over its life from the capital appreciation of the investments. Entity A has identified exit strategies for its investments to realize the capital appreciation.

c. Entity A does not have an objective of obtaining returns or benefits other than capital appreciation from its investments.

946-10-55-35 Entity A also has all of the following typical characteristics of an investment company:

a. Entity A is funded by multiple investors.

b. The limited partners of Entity A hold a significant interest in the partnership and are not related to the investment manager (the general partner).

c. Ownership in Entity A is represented by partnership interests acquired through capital contributions.

d. Investments are managed, and their performance is evaluated on a fair value basis.

946-10-55-36 Entity A does not hold more than one investment until 20X3. However, that is because during each of the years 20X1, 20X2, and part of 20X3, it is in its start-up period and has not yet fully executed its investment plan to acquire multiple investments because it could not identify suitable investment opportunities.

946-10-55-37 Entity A is an investment company from formation in 20X1 to December 31, 20X3. It has all the fundamental characteristics of an investment company. In addition, although Entity A does not possess all of the typical characteristics of an investment company, its activities are consistent with those of an investment company.

> > Example 2: Technology Fund

946-10-55-38 Entity C, an investment fund, is formed in 20X1 by six corporations in the technology industry to invest in multiple technology start-up companies for capital appreciation. Entity D, one of the corporations, holds a 70 percent controlling financial interest in Entity C. The remaining 30 percent of the fund is owned by the other 5 corporations, which are not related to each other or Entity D. Entity D holds options at amounts other than fair value to acquire controlling financial interests in the investees of the technology fund and options to purchase assets produced by the investees, if the technology developed by the investee is successful and would benefit the operations of Entity D. No plans for exiting the investments have been identified by Entity C. Entity C is managed by an investment manager that is not related to the investors. The investors in Entity C also provide significant advice to the investment manager about potential investments.

946-10-55-39 Even though Entity C's business purpose and substantive activities include investing for returns from capital appreciation and it has many of the typical characteristics of an investment company, Entity C is not an investment company because of both of the following conditions:

a.Entity D, the parent of Entity C, holds options at amounts other than fair value to acquire investees of the fund and assets of the investees if the technology developed by the investee is successful and would benefit Entity D's operations. That provides Entity D with a benefit that is other than returns from capital appreciation or investment income.

b. The investment plans of Entity C do not include exit strategies for its investments to realize returns from the capital appreciation of investees.

> > Example 3: Master-Feeder Structure

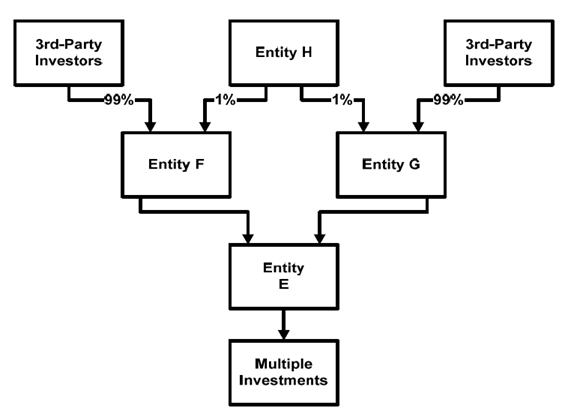

946-10-55-40 Entity E, a master fund, is formed in 20X1 with a 10-year life. The equity of Entity E is held by Entity F and Entity G, two affiliated feeder funds. Entity F and Entity G are established in conjunction with Entity E to meet legal, regulatory, tax, or other requirements. Entity F, the domestic feeder partnership, is capitalized with a 1 percent investment from the general partner and 99 percent from unaffiliated investors (with no party holding a controlling financial interest). Entity G, the offshore feeder fund, is capitalized with a 1 percent equity investment from the sponsor and 99 percent equity investments from unaffiliated investors (with no party holding a controlling financial interest). Entity H is the investment manager for the master-feeder structure and is the general partner of Entity F and the sponsor of Entity G.

946-10-55-41 This figure illustrates the master-feeder structure.

[Note: For ease of readability, the figure is not underlined as new text.]

946-10-55-42 The purpose of Entity E is to invest in multiple investments to generate returns solely from capital appreciation and investment income. Entity F and Entity G have communicated to investors that the sole purpose of the master-feeder structure is to provide investment opportunities for investors in separate market niches to invest in a large pool of assets. Entity E has identified exit strategies for the investments that it holds for returns from capital appreciation. In addition, Entity E manages, and evaluates the performance of, its investments on a fair value basis. Entity F and Entity G provide their investors with periodic information about the financial results of the master-feeder structure.

946-10-55-43 Entity E, Entity F, and Entity G each possess the fundamental characteristics of an investment company because all of the following conditions exist:

a. Entity E, Entity F, and Entity G obtained funds from investors and are providing those investors with investment management services.

b. The master-feeder structure's business purpose and only substantive activities, which were communicated to investors of Entity F and Entity G, are investing solely for returns from capital appreciation and investment income.

c. Entity E has identified exit strategies for the investments it holds for returns from capital appreciation. Although Entity F and Entity G do not have an exit strategy for their interests in Entity E, they are considered to have an exit strategy for their investments because Entity E was formed in conjunction with Entity F and Entity G and holds investments on behalf of them.

d. Entity E, Entity F, and Entity G do not have an objective of obtaining returns or benefits other than capital appreciation and investment income from their investments.

946-10-55-44 Entity E, Entity F, and Entity G each also possess all of the following typical characteristics of an investment company:

a. Entity E holds more than one investment. Both Entity F and Entity G also are considered to hold more than one investment because they were formed in conjunction with Entity E.

b. Both Entity F and Entity G are funded by multiple investors. Entity E also is considered to be funded by multiple investors because it was formed in conjunction with Entity F and Entity G.

c. Both Entity F and Entity G have investors that hold a significant interest in the partnership and are not related to the investment manager (Entity H). Although Entity F and Entity G are related to Entity E, Entity E is considered to have unrelated investors because it was formed in conjunction with Entity F and Entity G, which have unrelated investors.

d. Ownership in Entity E and Entity G are represented by equity interests acquired through capital contributions. Ownership in Entity F is represented by partnership interests acquired through capital contributions.

e. Entity E manages and evaluates the performance of investments on a fair value basis. Additionally, investors of Entity F and Entity G are provided with periodic financial information about the investing activities of Entity E, which includes information about the change in fair value of investments held.

946-10-55-45 Entity E, Entity F, and Entity G are investment companies. They possess all the fundamental characteristics of an investment company and all the typical characteristics of an investment company, either directly or indirectly as a result of the master-feeder structure.

18. Amend paragraph 946-10-65-1 and add paragraph 946-10-65-2 and its related heading as follows:

> Transition and Effective Date of Certain Scope, Equity Method, and Consolidation Guidance

946-10-65-1 The effective date of the pending content that links to this paragraph is delayed indefinitely.

An entity that early adopted

that

the pending content

that links to this paragraph before December 15, 2007, is permitted but not required to continue to apply the provisions of that pending

content.

content until the effective date of the amendments in Accounting Standards Update No. 2013-08, Financial Services—Investment Companies (Topic 946): Amendments to the Scope, Measurement, and Disclosure Requirements, as specified in paragraph 946-10-65-2(a). After the effective date of the amendments in Accounting Standards Update 2013-08, the pending content that links to this paragraph is superseded and may no longer be applied. No other entity may adopt the provisions of the pending content that links to this paragraph, with the following exception. If a

{add glossary link}parent

{add glossary link} entity

that early adopted the pending content that links to this paragraph chooses not to rescind its early adoption, an entity consolidated by that parent entity that is formed or acquired after that

parent's parent entity's

adoption of that pending content must apply the provisions of that pending content in its standalone financial statements. If an entity that early adopted the provisions of the pending content that links to this paragraph voluntarily rescinds its early adoption as permitted by this paragraph, that entity shall account for that change according to the provisions of Subtopic 250-10.

> Transition Related to Accounting Standards Update No. 2013-08, Financial Services—Investment Companies (Topic 946): Amendments to the Scope, Measurement, and Disclosure Requirements

946-10-65-2 The following represents the transition and effective date information related to Accounting Standards Update No. 2013-08, Financial Services—Investment Companies (Topic 946): Amendments to the Scope, Measurement, and Disclosure Requirements:

a. The pending content that links to this paragraph shall be effective for an entity's interim and annual reporting periods in fiscal years that begin after December 15, 2013. Earlier application is prohibited.

Entities that are no longer investment companies

b. An entity shall no longer apply the guidance in Topic 946 if it is no longer an investment company because it does not meet the assessment of investment company status in paragraphs 946-10-15-4 through 15-9.

c. At the date of adoption, for those entities that are no longer investment companies, the difference between the net assets required to be recognized and the amount previously recognized shall be recognized as a cumulative-effect adjustment to retained earnings as of the beginning of the period of adoption. An entity shall describe the transition method(s) applied and shall disclose the amount and classification of the consolidated assets or liabilities in its statement of financial position by the transition method(s) applied.

Initial measurement

d. If an entity is required to consolidate a subsidiary because the entity is no longer an investment company, the initial measurement of the assets, liabilities, and noncontrolling interests of the subsidiary depends on whether the determination of their carrying amounts is practicable. In that context, carrying amounts refers to the amounts at which the assets, liabilities, and noncontrolling interests would have been carried in the consolidated financial statements if the requirements of the pending content that links to this paragraph had been effective when the entity acquired its controlling financial interest in the subsidiary.

e. Similarly, for those investments that are required to be accounted for using the equity method as a result of the entity no longer being an investment company, the initial measurement of the investments depends on whether the determination of the investment's carrying amount is practicable. In that context, carrying amount refers to the amount at which the equity method investee would have been carried in the consolidated financial statements if the requirements of the pending content that links to this paragraph had been effective when the entity acquired its equity method investment.

f. If determining the carrying amounts is not practicable, the entity shall use the {add glossary link to second definition}fair value{add glossary link to second definition} of an investment at the date that the pending content that links to this paragraph becomes effective in applying Topic 805 on business combinations or Topic 323 on equity method and joint ventures at that date.

g. For all other investments that are required to be accounted for under other Topics as a result of the entity no longer being an investment company, the initial measurement of those investments shall be the fair value at the date of adoption.

Fair value option

h. An entity that is required to consolidate a subsidiary as a result of the initial application of the pending content that links to this paragraph may elect the fair value option provided by the Fair Value Option Subsections of Subtopic 825-10 only if the entity elects the option for all financial assets and financial liabilities of that subsidiary that are eligible for that option under those Fair Value Option Subsections. That election shall be made upon the adoption of the pending content that links to this paragraph on a subsidiary-by-subsidiary basis.

i. In addition, an entity may elect the fair value option provided by the Fair Value Option Subsections of Subtopic 825-10 for its financial instruments that are required to be accounted for under other Topics, including the equity method of accounting in Topic 323, as a result of the initial application of the pending content that links to this paragraph.

Entities that become investment companies or continue to be investment companies

j. An entity that is an investment company because it meets the assessment of investment company status in paragraphs 946-10-15-4 through 15-9 shall report the effect of applying the pending content that links to this paragraph as of the date that the content is first effective. The effect, if any, of applying the pending content that links to this paragraph shall be recorded as an adjustment to opening net assets (or a similar account). The adjustment to opening net assets (or a similar account) shall be included in the net asset value at the beginning of the period in the per-share information included in the financial highlights.

k. The adjustment to net assets (or a similar account) shall represent both of the following:

1. The difference between the fair value and the carrying amount of the entity's investees (or parent's portion of the assets minus liabilities for consolidated investments) at the date of adoption

2. Any amounts previously recognized in accumulated other comprehensive income.