3. Add paragraphs 810-10-15-17D, 810-10-30-10 through 30-16, 810-10-35-6 through 35-9, and 810-10-50-20 through 50-22 and their related headings, with a link to transition paragraph 810-10-65-6, as follows:

Consolidation—Overall

Scope and Scope Exceptions

Variable Interest Entities

> Collateralized Financing Entities

810-10-15-17D The guidance on collateralized financing entities in this Topic provides a measurement alternative to Topic 820 on fair value measurement and applies to a reporting entity that consolidates a collateralized financing entity when both of the following conditions exist:

a. All of the financial assets and the financial liabilities of the collateralized financing entity are measured at fair value in the consolidated financial statements under other applicable Topics, other than financial assets and financial liabilities that are incidental to the operations of the collateralized financing entity and have carrying values that approximate fair value (for example, cash, broker receivables, or broker payables).

b. The changes in the fair values of those financial assets and financial liabilities are reflected in earnings.

Initial Measurement

Variable Interest Entities

> Collateralized Financing Entities

810-10-30-10 When a reporting entity initially consolidates a variable interest entity that is a collateralized financing entity that meets the scope requirements in paragraph 810-10-15-17D, it may elect to measure the financial assets and the financial liabilities of the collateralized financing entity using a measurement alternative to Topic 820 on fair value measurement.

810-10-30-11 Under the measurement alternative, the reporting entity shall measure both the financial assets and the financial liabilities of the collateralized financing entity using the more observable of the fair value of the financial assets and the fair value of the financial liabilities. Any gain or loss that results from the initial application of this measurement alternative shall be reflected in earnings and attributed to the reporting entity in the consolidated statement of income (loss).

810-10-30-12 If the fair value of the financial assets of the collateralized financing entity is more observable, those financial assets shall be measured at fair value. The financial liabilities shall be measured in the initial consolidation as the difference between the following two amounts:

a. The sum of:

1. The fair value of the financial assets

2. The carrying value of any nonfinancial assets held temporarily

b. The sum of:

1. The fair value of any beneficial interests retained by the reporting entity (other than those that represent compensation for services)

2. The reporting entity's carrying value of any beneficial interests that represent compensation for services.

The fair value of the financial assets in (a)(1) should include the carrying values of any financial assets that are incidental to the operations of the collateralized financing entity because the financial assets' carrying values approximate their fair values.

810-10-30-13 If the fair value of the financial liabilities of the collateralized financing entity is more observable, those financial liabilities shall be measured at fair value. The financial assets shall be measured in the initial consolidation as the difference between the following two amounts:

a. The sum of:

1. The fair value of the financial liabilities (other than the beneficial interests retained by the reporting entity)

2. The fair value of any beneficial interests retained by the reporting entity (other than those that represent compensation for services)

3. The reporting entity's carrying value of any beneficial interests that represent compensation for services

b. The carrying value of any nonfinancial assets held temporarily.

The fair value of the financial liabilities in (a)(1) should include the carrying values of any financial liabilities that are incidental to the operations of the collateralized financing entity because the financial liabilities' carrying values approximate their fair values.

810-10-30-14 The amount resulting from paragraph 810-10-30-12 or paragraph 810-10-30-13 shall be allocated to the less observable of the financial assets and financial liabilities (other than the beneficial interests retained by the reporting entity), as applicable, using a reasonable and consistent methodology.

810-10-30-15 The carrying value of the beneficial interests that represent compensation for services (for example, rights to receive management fees or servicing fees) and the carrying value of any nonfinancial assets held temporarily by the collateralized financing entity shall be measured in accordance with other applicable Topics.

810-10-30-16 If a reporting entity does not elect to apply the measurement alternative to a collateralized financing entity that meets the scope requirements in paragraph 810-10-15-17D, the reporting entity shall measure the fair value of the financial assets and the fair value of the financial liabilities of the collateralized financing entity using the requirements of Topic 820 on fair value measurement. If Topic 820 is applied, any initial difference in the fair value of the financial assets and the fair value of the financial liabilities of the collateralized financing entity shall be reflected in earnings and attributed to the reporting entity in the consolidated statement of income (loss).

Subsequent Measurement

Variable Interest Entities

> Collateralized Financing Entities

810-10-35-6 A reporting entity that elects to apply the measurement alternative to Topic 820 on fair value measurement upon initial consolidation of a collateralized financing entity that meets the scope requirements in paragraph 810-10-15-17D shall consistently apply the measurement alternative for the subsequent measurement of the financial assets and the financial liabilities of that consolidated collateralized financing entity provided that it continues to meet the scope requirements in paragraph 810-10-15-17D. If a collateralized financing entity subsequently fails to meet the scope requirements, a reporting entity shall no longer apply the measurement alternative to that collateralized financing entity. Instead, it shall apply Topic 820 to measure those financial assets and financial liabilities that were previously measured using the measurement alternative.

810-10-35-7 Under the measurement alternative, a reporting entity shall measure both the financial assets and the financial liabilities of the collateralized financing entity using the more observable of the fair value of the financial assets and the fair value of the financial liabilities, as described in paragraphs 810-10-30-12 through 30-15.

810-10-35-8 A reporting entity that applies the measurement alternative shall recognize in its earnings all amounts that reflect its own economic interests in the consolidated collateralized financing entity, including both of the following:

a. The changes in the fair value of any beneficial interests retained by the reporting entity (other than those that represent compensation for services)

b. Beneficial interests that represent compensation for services (for example, management fees or servicing fees).

810-10-35-9 If a reporting entity does not apply the measurement alternative to a collateralized financing entity that meets the scope requirements in paragraph 810-10-15-17D, the reporting entity shall measure the fair value of the financial assets and the fair value of the financial liabilities of the collateralized financing entity using the requirements of Topic 820 on fair value measurement. If Topic 820 is applied, any subsequent changes in the fair value of the financial assets and the changes in the fair value of the financial liabilities of the collateralized financing entity shall be reflected in earnings and attributed to the reporting entity in the consolidated statement of income (loss).

Disclosure

Variable Interest Entities

> Collateralized Financing Entities

810-10-50-20 A reporting entity that consolidates a collateralized financing entity and measures the financial assets and the financial liabilities using the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8 shall disclose the information required by Topic 820 on fair value measurement and Topic 825 on financial instruments for the financial assets and the financial liabilities of the consolidated collateralized financing entity.

810-10-50-21 For the less observable of the fair value of the financial assets and the fair value of the financial liabilities of the collateralized financing entity that is measured in accordance with the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8, a reporting entity shall disclose that the amount was measured on the basis of the more observable of the fair value of the financial liabilities and the fair value of the financial assets.

810-10-50-22 The disclosures in paragraphs 810-10-50-20 through 50-21 do not apply to the financial assets and the financial liabilities that are incidental to the operations of the collateralized financing entity and have carrying values that approximate fair value.

4. Add paragraphs 810-10-55-205J through 55-205K and their related headings, with a link to transition paragraph 810-10-65-6, as follows: [Note: For ease of readability, the tables and footnotes are not underlined as new text.]

Implementation Guidance and Illustrations

Variable Interest Entities

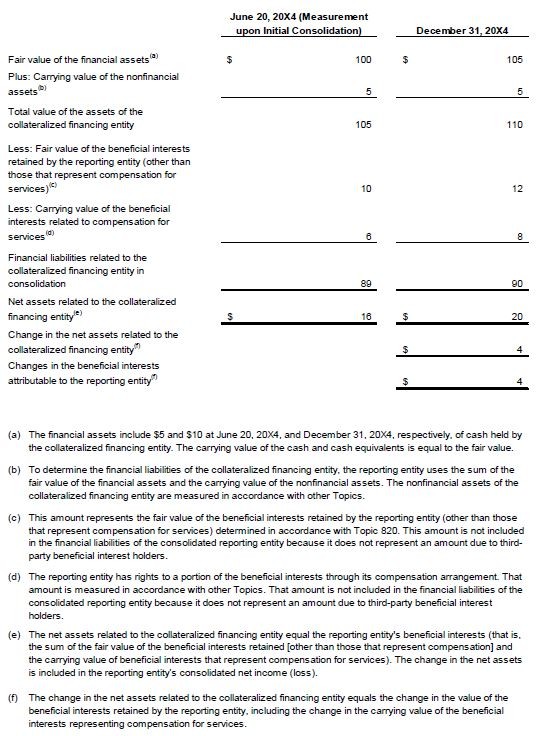

> > Example 9: Collateralized Financing Entities—Application of the Measurement Alternative to the Financial Liabilities When the Fair Value of the Financial Assets Is More Observable

810-10-55-205J A reporting entity has determined that it must consolidate a collateralized financing entity under this Topic and is eligible to and has elected to apply the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8. The reporting entity retains certain beneficial interests in the collateralized financing entity as compensation for its services and also retains other beneficial interests. Since initial consolidation, the collateralized financing entity has not settled any of the outstanding beneficial interests related to compensation for services. The collateralized financing entity's only assets are corporate debt obligations, and its only liabilities (the beneficial interests issued by the collateralized financing entity) are thinly traded. The reporting entity determines that the fair value of the collateralized financing entity's financial assets is more observable than the fair value of its financial liabilities. Because the fair value of the financial assets is more observable, the reporting entity determines the amount of the financial liabilities of the collateralized financing entity (other than those beneficial interests retained by the reporting entity) as follows.

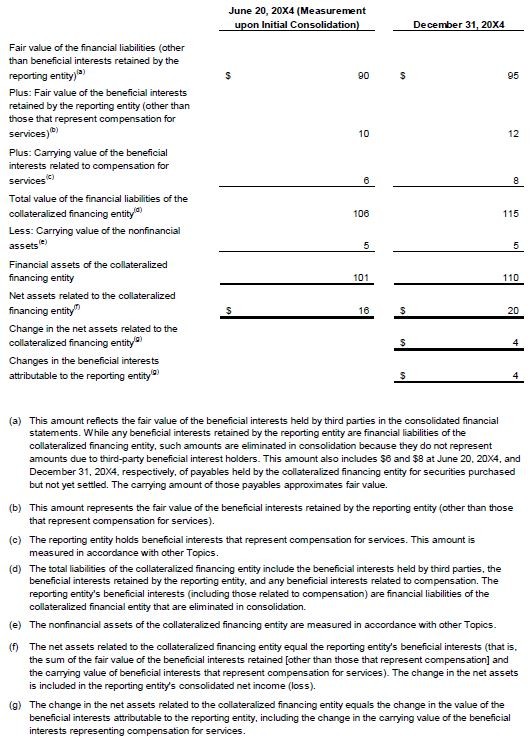

> > Example 10: Collateralized Financing Entities—Application of the Measurement Alternative to the Financial Assets When the Fair Value of the Financial Liabilities Is More Observable

810-10-55-205K A reporting entity has determined that it must consolidate a collateralized financing entity under this Topic and is eligible to and has elected to apply the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8. The reporting entity retains certain beneficial interests in the collateralized financing entity as compensation for its services and also retains other beneficial interests. Since initial consolidation, the collateralized financing entity has not settled any of the outstanding beneficial interests related to compensation for services. The collateralized financing entity's only assets are mortgages with primarily unobservable inputs, and its only liabilities are beneficial interests issued in those assets. The beneficial interests of the collateralized financing entity are frequently traded, although not in an active market. Because the fair value of the financial liabilities is more observable, the reporting entity determines the amount of the financial assets of the collateralized financing entity as follows.

5. Add paragraph 810-10-65-6 and its related heading as follows:

> Transition Related to Accounting Standards Update No. 2014-13, Consolidation (Topic 810): Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity

810-10-65-6 The following represents the transition and effective date information related to Accounting Standards Update No. 2014-13, Consolidation (Topic 810): Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity:

a. The pending content that links to this paragraph shall be effective as follows:

1. For public business entities, for annual periods, and interim periods within those annual periods, beginning after December 15, 2015

2. For all other entities, for annual periods ending after December 15, 2016, and interim periods beginning after December 15, 2016.

b. Upon adoption, a reporting entity may apply the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8 to any existing consolidated collateralized financing entity that meets the scope requirements of paragraph 810-10-15-17D using a modified retrospective approach by remeasuring the financial assets or the financial liabilities of the existing consolidated collateralized financing entity as of the beginning of the annual period of adoption and recording a cumulative-effect adjustment for the remeasurement to equity. Any reporting entity that does not elect to apply the measurement alternative shall reclassify any accumulated differences in the fair value of the financial assets and the fair value of the financial liabilities of its collateralized financing entity to retained earnings if those differences were previously presented in another caption within equity (for example, appropriated retained earnings).

c. A reporting entity also may elect to apply the pending content that links to this paragraph retrospectively to all relevant prior periods beginning with the annual period in which the amendments in Accounting Standards Update No. 2009-17, Consolidations (Topic 810): Improvements to Financial Reporting by Enterprises Involved with Variable Interest Entities, were initially adopted.

d. A reporting entity that consolidates a collateralized financing entity that does not meet the scope requirements in paragraph 810-10-15-17D because the fair value option in Topic 825 was not elected to measure the eligible financial assets, financial liabilities, or both of the collateralized financing entity when it was initially consolidated, may elect at the date of adoption to apply the measurement alternative in paragraphs 810-10-30-10 through 30-15 and 810-10-35-6 through 35-8 to those financial assets and financial liabilities or to continue using the guidance in other Topics to measure the financial assets and the financial liabilities of the consolidated collateralized financing entity. A reporting entity that does not elect to use the measurement alternative may not elect at the date of adoption to use the measurement requirements of Topic 820 on fair value measurement or to otherwise change its basis for measuring the financial assets or the financial liabilities of the collateralized financing entity.

e. Earlier application of the pending content that links to this paragraph is permitted as of the beginning of an annual period.

f. An entity shall provide the disclosures in paragraphs 250-10-50-1 through 50-3 in the period the entity adopts the pending content that links to this paragraph.