4. Amend paragraphs 944-40-50-1 and 944-40-50-3 through 50-5, supersede paragraph 944-40-50-2, and add paragraphs 944-40-50-4A through 50-4I and related headings, with a link to transition paragraph 944-40-65-1, as follows:

Financial Services—Insurance—Claim Costs and Liabilities for Future Policy Benefits

Disclosure

General

944-40-50-1 Insurance entities

An insurance entity shall disclose in

their

its financial statements the basis for estimating the liabilities for unpaid

{add glossary link to 2nd definition}claims

{add glossary link to 2nd definition} and

claim adjustment expenses.

944-40-50-2 Paragraph superseded by Accounting Standards Update 2015-09.The requirements in paragraphs 944-40-50-3 through 50-4 apply to annual and complete sets of interim financial statements prepared in conformity with generally accepted accounting principles (GAAP).

944-40-50-3 For

annual and interim reporting periods each fiscal year for which an income statement is presented

, all of the following information about the

liability for unpaid claims and

{add glossary link}claim adjustment expenses

{add glossary link} shall be

disclosed

presented in a tabular rollforward:

a. The balance in the liability for unpaid

{add glossary link to 2nd definition}claims

{add glossary link to 2nd definition} and claim adjustment expenses at the beginning

and end

of each fiscal year presented

in the statement of income, and the related amount of

reinsurance recoverable

b.

Incurred

Year-to-date incurred claims and claim adjustment expenses with separate disclosure of the provision for insured events of the current fiscal year and of increases or decreases in the provision for insured events of prior fiscal years

c.

Payments

Year-to-date payments of claims and claim adjustment expenses with separate disclosure of payments of claims and

{remove glossary link}claim{remove glossary link} adjustment expenses attributable to insured events of the current fiscal year and to insured events of prior fiscal years

cc. The ending balance in the liability for unpaid claims and claim adjustment expenses and the related amount of reinsurance recoverable.

d.

Subparagraph superseded by Accounting Standards Update 2015-09. The reasons for the change in incurred claims and claim adjustment expenses recognized in the income statement attributable to insured events of prior fiscal years and should indicate whether additional premiums or return premiums have been accrued as a result of the prior-year effects.

[Content amended and moved below]In addition, an insurance entity shall disclose theThe

reasons for the change in incurred claims and claim adjustment expenses recognized in the income statement attributable to insured events of prior fiscal years and should indicate whether additional premiums or return premiums have been accrued as a result of the prior-year effects.

[Content amended as shown and moved from (d)]

944-40-50-4 For annual reporting periods, an insurance entityInsurance entities

shall disclose management's policies and methodologies for estimating the liability for unpaid claims and claim adjustment expenses for difficult-to-estimate liabilities, such as any of the following:

- Claims for toxic waste cleanup

- Asbestos-related illnesses

- Other environmental remediation exposures.

Short-Duration Contracts

> Information about the Liability for Unpaid Claims and Claim Adjustment Expenses

944-40-50-4A For health insurance claims, an insurance entity shall aggregate or disaggregate the information in paragraph 944-40-50-3 so that useful information is not obscured by either the inclusion of a large amount of insignificant detail or the aggregation of items that have significantly different characteristics (see paragraphs 944-40-55-9A through 55-9C).

944-40-50-4B For annual reporting periods, an insurance entity shall disclose in a tabular format, as of the date of the latest statement of financial position presented, undiscounted information about claims development by accident year, including separate information about both of the following on a net basis after risk mitigation through reinsurance:

a. Incurred claims and allocated claim adjustment expenses

b. Paid claims and allocated claim adjustment expenses.

The disclosure about claims development by accident year should present information for the number of years for which claims incurred typically remain outstanding, but need not exceed 10 years including the most recent reporting period presented. All periods presented in the disclosure about claims development that precede the most recent reporting period shall be considered supplementary information. For the most recent reporting period presented, the disclosure about claims development shall include the total net outstanding claims for accident years not separately presented as part of the claims development (see paragraph 944-40-55-9E).

944-40-50-4C For annual reporting periods, an insurance entity shall reconcile the disclosure about incurred and paid claims development information to the aggregate carrying amount of the liability for unpaid claims and claim adjustment expenses for the most recent reporting period presented, with separate disclosure of reinsurance recoverable on unpaid claims (see paragraph 944-40-55-9E).

944-40-50-4D For annual reporting periods, an insurance entity shall quantitatively disclose the following for each accident year presented in the disclosures about incurred claims development (see paragraph 944-40-55-9E) for the most recent reporting period presented:

a. The total of incurred-but-not-reported liabilities plus expected development on reported claims included in the liability for unpaid claims and claim adjustment expenses

b. Cumulative claim frequency information, unless it is impracticable to do so. If it is impracticable to disclose claim frequency information, where the term impracticable has the same meaning as impracticability in paragraph 250-10-45-9, an insurance entity shall disclose that fact and explain why the disclosure is impracticable.

944-40-50-4E For interim and annual reporting periods, for health insurance claims, an insurance entity shall disclose the total of incurred-but-not-reported liabilities plus expected development on reported claims included in the liability for unpaid claims and claim adjustment expenses.

944-40-50-4F An insurance entity shall describe both of the following:

a. Its methodologies for:

1. Determining the presented amounts of both incurred-but-not-reported liabilities and expected development on reported claims required by paragraphs 944-40-50-4D through 50-4E

2. Calculating cumulative claim frequency information required by paragraph 944-40-50-4D

b. Significant changes to those methodologies. When describing (2) above the insurance entity also shall include whether frequency is measured by claim event or individual claimant and how the insurance entity considers claims that do not result in a liability (see paragraph 944-40-55-9D).

944-40-50-4G For annual reporting periods, for all claims except health insurance claims, an insurance entity shall disclose as supplementary information the historical average annual percentage payout of incurred claims by age, net of reinsurance (that is, history of claims duration by age), as of the most recent reporting period. This information shall be disclosed for the same number of accident years presented in the disclosures required by paragraph 944-40-50-4B (see paragraphs 944-40-55-9F through 55-9G).

944-40-50-4H An insurance entity shall disclose the information required by paragraphs 944-40-50-4B through 50-4G and 944-40-50-5 in a manner that allows users to understand the amount, timing, and uncertainty of cash flows arising from the liabilities. An insurance entity shall aggregate or disaggregate the disclosures in paragraphs 944-40-50-4B through 50-4G and 944-40-50-5 so that useful information is not obscured by either the inclusion of a large amount of insignificant detail or the aggregation of items that have significantly different characteristics (see paragraphs 944-40-55-9A through 55-9C). An insurance entity need not provide disclosures about claims development for insignificant categories; however, balances for insignificant categories shall be included in the reconciliation required by paragraph 944-40-50-4C.

944-40-50-4I For annual reporting periods, an insurance entity shall disclose information about significant changes in methodologies and assumptions used in calculating the liability for unpaid claims and claim adjustment expenses, including reasons for the change and the effects on the financial statements for the most recent reporting period presented.

> > Information about Amounts Reported at Present Value

944-40-50-5 For liabilities for unpaid claims and claim adjustment expenses that are presented at present value in the financial statements, an insurance entityInsurance entities

shall disclose

both

all of the following in

itstheir

annual financial statements:

a.

For each period presented in the statement of financial position, theThe

carrying amount of liabilities for unpaid claims and claim adjustment expenses relating to short-duration contracts that are presented at present value

in the financial statements

b. The range of interest rates used to discount the liabilities disclosed in (a).

c. The aggregate amount of discount related to the time value of money deducted to derive the liabilities disclosed in (a)

d. For each period presented in the statement of income, the amount of interest accretion recognized

e. The line item(s) in the statement of income in which the interest accretion is classified.

5. Add paragraphs 944-40-55-9A through 55-9G and their related headings and the Subsection title, with a link to transition paragraph 944-40-65-1, as follows:

Implementation Guidance and Illustrations

Short-Duration Contracts

> Implementation Guidance

> > Information about the Liability for Unpaid Claims and Claim Adjustment Expenses

944-40-55-9A Paragraphs 944-40-50-4A and 944-40-50-4H require an insurance entity to aggregate or disaggregate certain disclosures so that useful information is not obscured by either the inclusion of a large amount of insignificant detail or the aggregation of items that have significantly different characteristics to allow users to understand the amount, timing, and uncertainty of cash flows arising from contracts issued by insurance entities. Consequently, the extent to which an insurance entity's information is aggregated or disaggregated for the purposes of those disclosures depends on the facts and circumstances that pertain to the characteristics of the liability for unpaid claims and claim adjustment expenses.

944-40-55-9B When selecting the type of category to use to aggregate or disaggregate disclosures, an insurance entity should consider how information about the insurance entity's liability for unpaid claims and claim adjustment expenses has been presented for other purposes, including all of the following:

a. Disclosures presented outside the financial statements (for example, in earnings releases, annual reports, statutory filings, or investor presentations)

b. Information regularly viewed by the chief operating decision maker for evaluating financial performance

c. Other information that is similar to the types of information identified in (a) and (b) and that is used by the insurance entity or users of the insurance entity's financial statements to evaluate the insurance entity's financial performance or make resource allocation decisions.

944-40-55-9C Examples of categories that might be appropriate include any of the following:

a. Type of coverage (for example, major product line)

b. Geography (for example, country or region)

c. Reportable segment as defined in Topic 280 on segment reporting

d. Market or type of customer (for example, personal or commercial lines of business)

e. Claim duration (for example, claims that have short settlement periods or claims that have long settlement periods).

When applying the guidance in paragraphs 944-40-50-4A and 944-40-50-4H, an insurance entity should not aggregate amounts from different reportable segments according to Topic 280.

944-40-55-9D Claim frequency information may be tracked and analyzed by an insurance entity in a variety of ways. For example, an insurance entity may track claim frequency by claim event (such as a car accident), while another entity may track claim frequency by individual claimant (such as the number of individual claimants in a car accident). Also, certain types of insurance coverage, such as excess-of-loss insurance or supplemental insurance, can experience claim activity that does not result in a liability to the insurance entity. This Subtopic does not require a particular methodology. Therefore, to allow users to understand the context of the information presented, an insurance entity should describe qualitatively the methodologies used to determine the quantitative claim frequency information presented. In certain circumstances, such as providing reinsurance on short-duration contracts or participating in residual market pools, an insurance entity may not have access to claim frequency information, in which case it may be impracticable to disclose this information. The insurance entity should disclose that fact and explain why the disclosure is impracticable.

> Illustrations

> > Example 1: Disclosure of Information about the Liability for Unpaid Claims and Claim Adjustment Expenses

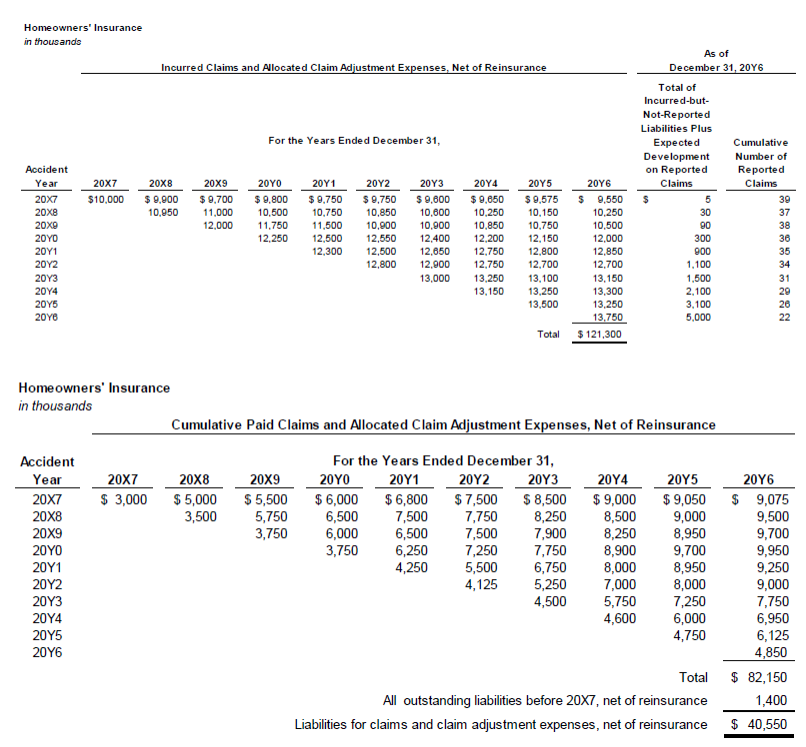

944-40-55-9E The following Example illustrates the information that an insurance entity with one major short-duration product line (homeowners' insurance) would disclose in its 20Y6 financial statements to meet the requirements of paragraphs 944-40-50-4B through 50-4D.

Note X: Liability for Unpaid Claims and Claim Adjustment Expenses

The following is information about incurred and paid claims development as of December 31, 20Y6, net of reinsurance, as well as cumulative claim frequency and the total of incurred-but-not-reported liabilities plus expected development on reported claims included within the net incurred claims amounts.

The information about incurred and paid claims development for the years ended December 31, 20X7, to 20Y5, is presented as supplementary information.

[For ease of readability, the illustration is not underlined as new text.]

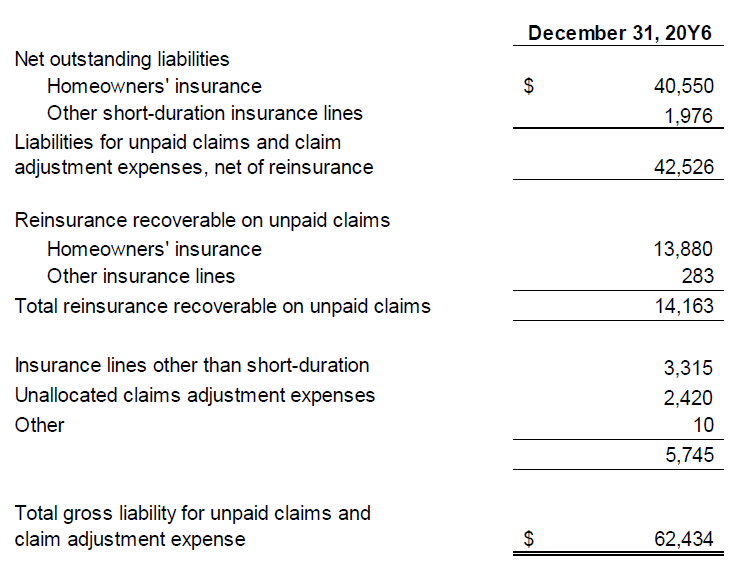

Reconciliation of the Disclosure of Incurred and Paid Claims Development to the Liability for Unpaid Claims and Claim Adjustment Expenses

The reconciliation of the net incurred and paid claims development tables to the liability for claims and claim adjustment expenses in the consolidated statement of financial position is as follows.

[For ease of readability, the calculation is not underlined as new text.]

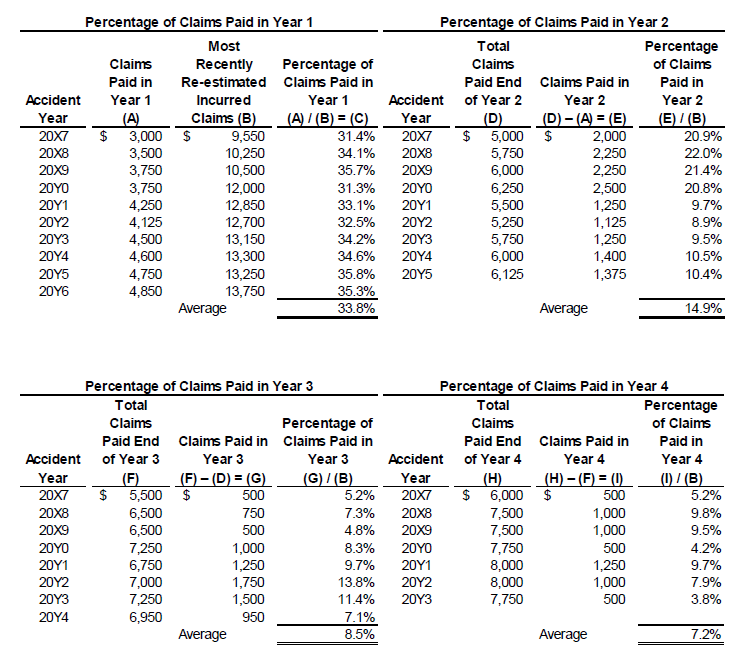

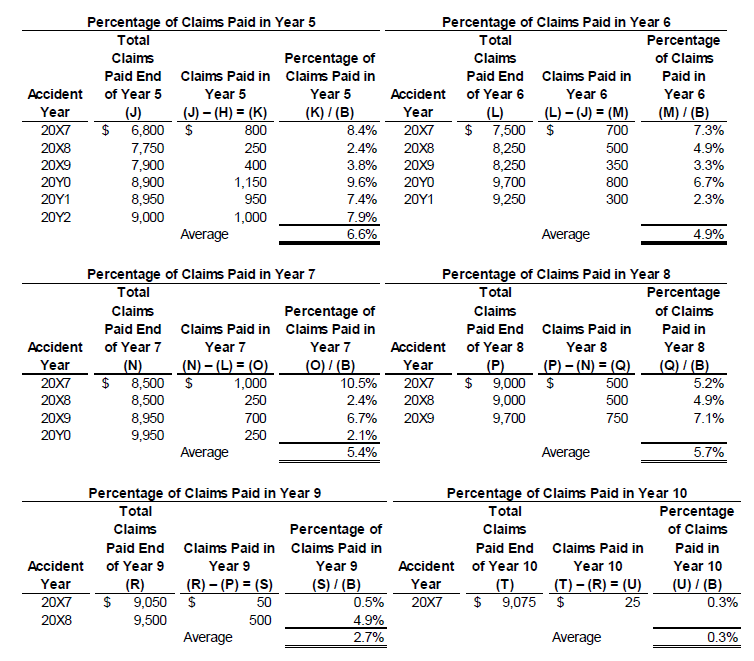

> > Example 2: Information about Historical Claims Duration

944-40-55-9F An illustrative Example of the supplementary information that an insurance entity would disclose to meet the requirements in paragraph 944-40-50-4G is as follows.

Note X: Liability for Unpaid Claims and Claim Adjustment Expenses

The following is supplementary information about average historical claims duration as of December 31, 20Y6.

[For ease of readability, the illustration is not underlined as new text.]

944-40-55-9G For this illustrative Example, the approach selected by the insurance entity to compute historical claims duration using the information about claims development included in paragraph 944-40-55-9F is as follows. These calculations are for illustrative purposes only and would not be included in the disclosure.

[For ease of readability, the illustration is not underlined as new text.]

6. Add paragraph 944-40-65-1 and its related headings as follows:

> Transition Related to Accounting Standards Update No. 2015-09, Financial Services—Insurance (Topic 944): Disclosures about Short Duration Contracts

944-40-65-1 The following represents the transition and effective date information related to Accounting Standards Update No. 2015-09, Financial Services—Insurance (Topic 944): Disclosures about Short-Duration Contracts:

a. A public business entity shall apply the pending content that links to this paragraph for annual periods beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016.

b. All other entities shall apply the pending content that links to this paragraph for annual periods beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017.

c. Early application of the pending content that links to this paragraph is permitted.

d. The pending content that links to this paragraph shall be applied retrospectively, except for those requirements that apply only to the current period.

e. In the year of initial application of the pending content that links to this paragraph, an insurance entity need not disclose information about claims development for a particular category that occurred earlier than five years before the end of the first period in which the pending content that links to this paragraph is first applied if it is impracticable to obtain the information required for disclosure. For each subsequent year following the year of initial application of the pending content that links to this paragraph, the minimum required number of years will increase by at least 1 year but need not exceed 10 years, including the most recent period presented in the statement of financial position.

7. Amend paragraph 270-10-00-1, by adding the following item to the table, as follows:

270-10-00-1 The following table identifies the changes made to this Subtopic.

Paragraph |

Action |

Accounting Standards Update |

Date |

270-10-50-7 |

Amended |

2015-09 |

05/21/2015 |

8. Amend paragraph 944-40-00-1, by adding the following items to the table, as follows:

944-40-00-1 The following table identifies the changes made to this Subtopic.

Paragraph |

Action |

Accounting Standards Update |

Date |

Accident Year |

Added |

2015-09 |

05/21/2015 |

Health Insurance Claims |

Added |

2015-09 |

05/21/2015 |

944-40-50-1 |

Amended |

2015-09 |

05/21/2015 |

944-40-50-2 |

Superseded |

2015-09 |

05/21/2015 |

944-40-50-3 through 50-5 |

Amended |

2015-09 |

05/21/2015 |

944-40-50-4A through 50-4I |

Added |

2015-09 |

05/21/2015 |

944-40-55-9A through 55-9G |

Added |

2015-09 |

05/21/2015 |

944-40-65-1 |

Added |

2015-09 |

05/21/2015 |

The amendments in this Update were adopted by the unanimous vote of the seven members of the Financial Accounting Standards Board:

Russell G. Golden, Chairman

James L. Kroeker, Vice Chairman

Daryl E. Buck

Thomas J. Linsmeier

R. Harold Schroeder

Marc A. Siegel

Lawrence W. Smith