Search within this section

Select a section below and enter your search term, or to search all click ASU 2016-09—Compensation—Stock compensation (Topic 718): Improvements to employee share-based payment accounting

Favorited Content

Copyright © 2016 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government.

|

Current GAAP |

Summary of Simplifications |

Accounting for Income Taxes: An entity must determine for each award whether the difference between the deduction for tax purposes and the compensation cost recognized for financial reporting purposes results in either an excess tax benefit or a tax deficiency. Excess tax benefits are recognized in additional paid-in capital; tax deficiencies are recognized either as an offset to accumulated excess tax benefits, if any, or in the income statement. Excess tax benefits are not recognized until the deduction reduces taxes payable. |

All excess tax benefits and tax deficiencies (including tax benefits of dividends on share-based payment awards) should be recognized as income tax expense or benefit in the income statement. The tax effects of exercised or vested awards should be treated as discrete items in the reporting period in which they occur.

An entity also should recognize excess tax benefits regardless of whether the benefit reduces taxes payable in the current period.

|

Classification of Excess Tax Benefits on the Statement of Cash Flows: Excess tax benefits must be separated from other income tax cash flows and classified as a financing activity. |

Excess tax benefits should be classified along with other income tax cash flows as an operating activity. |

Forfeitures: Accruals of compensation cost are based on the number of awards that are expected to vest. |

An entity can make an entity-wide accounting policy election to either estimate the number of awards that are expected to vest (current GAAP) or account for forfeitures when they occur. |

Minimum Statutory Tax Withholding Requirements: One of the requirements for an award to qualify for equity classification is that an entity cannot partially settle the award in cash in excess of the employer’s minimum statutory withholding requirements. |

The threshold to qualify for equity classification permits withholding up to the maximum statutory tax rates in the applicable jurisdictions. |

Classification of Employee Taxes Paid on the Statement of Cash Flows When an Employer Withholds Shares for Tax-Withholding Purposes: There is no guidance on classification of cash paid by an employer to the taxing authorities when directly withholding shares for tax-withholding purposes. |

Cash paid by an employer when directly withholding shares for tax-withholding purposes should be classified as a financing activity. |

Practical Expedient—Expected Term: Entities are required to estimate the period of time that an option will be outstanding. |

A nonpublic entity can make an accounting policy election to apply a practical expedient to estimate the expected term for all awards with performance or service conditions that meet certain conditions. |

Intrinsic Value: At initial adoption of Topic 718, Compensation—Stock Compensation, nonpublic entities were provided an option to measure all liability-classified awards at intrinsic value. Some nonpublic entities were not aware of that option. |

A nonpublic entity can make a one-time accounting policy election to switch from measuring all liability-classified awards at fair value to intrinsic value. |

Area for Simplification |

Paragraphs |

Issue 1: Accounting for Income Taxes |

3–21 |

Issue 2: Classification of Excess Tax Benefits on the Statement of Cash Flows |

22–25 |

Issue 3: Forfeitures |

26–39 |

Issue 4: Minimum Statutory Tax Withholding Requirements |

40–42 |

Issue 5: Classification of Employee Taxes Paid on the Statement of Cash Flows When an Employer Withholds Shares for Tax-Withholding Purposes |

43–46 |

Issue 6: Practical Expedient—Expected Term |

47–50 |

Issue 7: Intrinsic Value |

51–53 |

Issue 8: Eliminating the Indefinite Deferral in Topic 718 |

54–56 |

Share options granted Employees granted options

Expected forfeitures per year

Share price at the grant date

Exercise price

Contractual term of options

Risk-free interest rate over contractual term

Expected volatility over contractual term

Expected dividend yield over contractual term

Suboptimal exercise factor

|

900,000

3,000

3.0%

$ 30

$ 30

10 years

1.5 to 4.3%

40 to 60%

1.0%

2

|

Compensation cost |

$4,022,151 |

||

Additional paid-in capital |

$4,022,151 |

||

Deferred tax asset |

$1,407,753 |

||

Deferred tax benefit |

$1,407,753 |

||

Additional paid-in capital |

$723,531 |

||

Compensation cost |

$7 23,531 |

||

Deferred tax expense |

$253,236 |

||

Deferred tax asset |

$253,236 |

||

Compensation cost

Additional paid-in capital

|

$ 3,660,386

$ 3 ,660,386

|

Deferred tax asset

Deferred tax benefit

|

$ 1,281,135

$ 1 ,281,135

|

Cash (747,526 × $30) |

$22,425,780 |

||

Additional paid-in capital |

$10,981,157 |

||

Common stock |

$33,406,937 |

||

Deferred tax expense |

$3,843,405 |

||

Deferred tax asset |

$3 ,843,405 |

||

Current taxes payable

Current tax expense Current tax expense

Additional paid-in capital |

$ 7,849,023

$ 3,843,405 $ 7,849,023

$ 4,005,618 |

Compensation cost |

$23,333 |

||

Additional paid-in capital |

$23,333 |

||

Deferred tax asset |

$8,167 |

||

Deferred tax benefit |

$8,167 |

||

Deferred tax expense |

$24,500 |

||

Deferred tax asset |

$24,500 |

||

Current taxes payable

Current tax expense

Current tax expense

Additional paid-in capital |

$ 70,000

$ 24,500

$ 70,000

$ 45,500 |

Additional paid-in capital |

$1,916,614 |

||

Share-based compensation liability |

$1,916,614 |

||

Compensation cost |

$9,667,949 |

||

Additional paid-in capital |

$2,105,537 |

||

Share-based compensation liability |

$11,773,486 |

||

Deferred tax asset |

$3,383,782 |

||

Deferred tax benefit |

$3,383,782 |

||

Share-based compensation liability

Compensation cost

Additional paid-in capital

|

$5,476,040

$ 1,623,646

$ 3,852,394

|

Deferred tax expense

Deferred tax asset

|

$568,276

$568,276

|

Share-based compensation liability |

$8,214,060 |

||

Cash ($10 × 821,406) |

$8,214,060 |

||

Deferred tax expense |

$4,223,259 |

||

Deferred tax asset |

$4,223,259 |

||

Current taxes payable |

$2,874,921 |

||

Additional paid-in capital |

$1,348,338 |

||

Current tax expense |

$4,223,259 |

||

Current tax expense |

$2,874,921 |

||

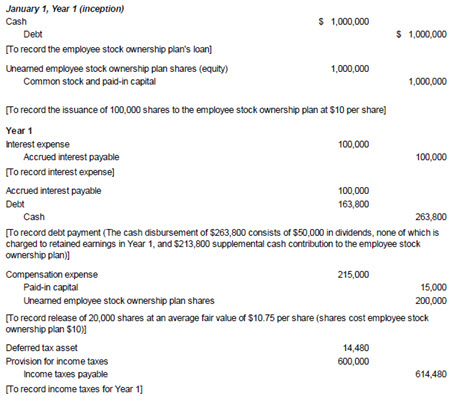

Debt |

$ 656,000 |

||

Additional paid-in capital |

60,000 |

||

Unearned employee stock ownership plan shares |

$ 600,000 |

||

Cash |

116,000 |

||

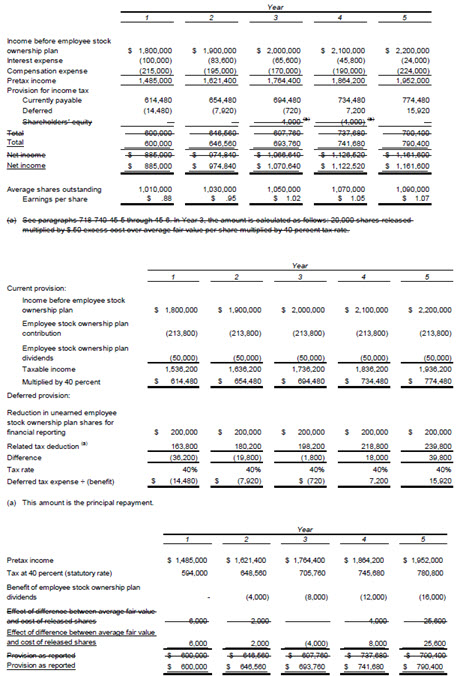

Cash outflow from operating activities: Excess tax benefits from share-based payment arrangements |

$ (4,005,618) |

Cash inflow from financing activities: Excess tax benefits from share-based payment arrangements |

$ 4,005,618 |

Share options granted

Employees granted options

Expected forfeitures per year

Share price at the grant date

Exercise price

Contractual term of options

Risk-free interest rate over contractual term

Expected volatility over contractual term

Expected dividend yield over contractual term

Suboptimal exercise factor

|

900,000

3,000

3.0%

$ 30

$ 30

10 years

1.5 to 4.3%

40 to 60%

1.0%

2

|

Compensation cost |

$4,022,151 |

||

Additional paid-in capital |

$4,022,151 |

||

Deferred tax asset |

$1,407,753 |

||

Deferred tax benefit |

$1,407,753 |

||

Additional paid-in capital |

$723,531 |

||

Compensation cost |

$723,531 |

||

Deferred tax expense |

$253,236 |

||

Deferred tax asset |

$253,236 |

||

Compensation cost |

$3,660,386 |

||

Additional paid-in capital |

$3,660,386 |

||

Deferred tax asset |

$1,281,135 |

||

Deferred tax benefit |

$1,281,135 |

||

Cash (747,526 × $30) |

$22,425,780 |

||

Additional paid-in capital |

$10,981,157 |

||

Common stock |

$33,406,937 |

||

Deferred tax expense |

$3,843,405 |

||

Deferred tax asset |

$3,843,405 |

||

Current taxes payable |

$7,849,023 |

||

Current tax expense |

$3,843,405 |

||

Additional paid-in capital |

$4,005,618 |

||

Compensation cost |

$4,407,000 |

||

Additional paid-in capital |

$4,407,000 |

||

Deferred tax asset |

$1,542,450 |

||

Deferred tax benefit |

$1,542,450 |

||

Additional paid-in capital |

$220,350 |

||

Compensation cost |

$220,350 |

||

Deferred tax benefit |

$77,123 |

||

Deferred tax asset |

$77,123 |

||

Compensation cost |

$4,186,650 |

||

Additional paid-in capital |

$4,186,650 |

||

Deferred tax asset |

$1,465,328 |

||

Deferred tax benefit |

$1,465,328 |

||

Additonal paid-capital |

$463,656 |

||

Compensation cost |

$463,656 |

||

Deferred tax benefit |

$162,280 |

||

Deferred tax asset |

$162,280 |

||

Paragraph |

Action |

Accounting Standards Update |

Date |

230-10-45-14 |

Amended |

2016-09 |

03/30/2016 |

230-10-45-15 |

Amended |

2016-09 |

03/30/2016 |

230-10-45-17 |

Amended |

2016-09 |

03/30/2016 |

230-10-45-25 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

260-10-45-29 |

Amended |

2016-09 |

03/30/2016 |

260-10-45-68B |

Amended |

2016-09 |

03/30/2016 |

260-10-55-69 |

Amended |

2016-09 |

03/30/2016 |

260-10-55-69A |

Added |

2016-09 |

03/30/2016 |

260-10-55-70 |

Amended |

2016-09 |

03/30/2016 |

260-10-55-76A |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

323-10-55-19 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Public Business Entity |

Added |

2016-09 |

03/30/2016 |

718-10-25-6 |

Amended |

2016-09 |

03/30/2016 |

718-10-25-18 |

Amended |

2016-09 |

03/30/2016 |

718-10-25-19 |

Superseded |

2016-09 |

03/30/2016 |

718-10-25-19A |

Added |

2016-09 |

03/30/2016 |

718-10-30-20A |

Added |

2016-09 |

03/30/2016 |

718-10-30-20B |

Added |

2016-09 |

03/30/2016 |

718-10-30-28 |

Amended |

2016-09 |

03/30/2016 |

718-10-35-3 |

Amended |

2016-09 |

03/30/2016 |

718-10-35-12 |

Amended |

2016-09 |

03/30/2016 |

718-10-35-13 |

Superseded |

2016-09 |

03/30/2016 |

718-10-45-1 |

Amended |

2016-09 |

03/30/2016 |

718-10-50-2 |

Amended |

2016-09 |

03/30/2016 |

718-10-50-2A |

Added |

2016-09 |

03/30/2016 |

718-10-55-2 |

Amended |

2016-09 |

03/30/2016 |

718-10-55-30 |

Amended |

2016-09 |

03/30/2016 |

718-10-55-34A |

Added |

2016-09 |

03/30/2016 |

718-10-55-45 |

Amended |

2016-09 |

03/30/2016 |

718-10-55-50A |

Added |

2016-09 |

03/30/2016 |

718-10-55-76 |

Amended |

2016-09 |

03/30/2016 |

718-10-55-137 |

Amended |

2016-09 |

03/30/2016 |

718-10-65-1 |

Superseded |

2016-09 |

03/30/2016 |

718-10-65-4 through 65-10 |

Added |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Excess Tax Benefits |

Superseded |

2016-09 |

03/30/2016 |

718-20-35-3A |

Added |

2016-09 |

03/30/2016 |

718-20-55-4 through 55-7 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-10 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-12 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-20 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-21 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-22 |

Superseded |

2016-09 |

03/30/2016 |

718-20-55-23 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-23A |

Added |

||

718-20-55-24 |

Superseded |

2016-09 |

03/30/2016 |

718-20-55-34A through 55-34G |

Added |

2016-09 |

03/30/2016 |

718-20-55-60 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-74 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-75 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-87 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-121 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-123 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-132 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-133 |

Amended |

2016-09 |

03/30/2016 |

718-20-55-144 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

718-30-30-2A |

Added |

2016-09 |

03/30/2016 |

718-30-55-2 |

Amended |

2016-09 |

03/30/2016 |

718-30-55-9 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

718-40-55-6 |

Amended |

2016-09 |

03/30/2016 |

718-40-55-8 |

Amended |

2016-09 |

03/30/2016 |

718-40-60-1 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Carryforward |

Superseded |

2016-09 |

03/30/2016 |

Excess Tax Benefits |

Superseded |

2016-09 |

03/30/2016 |

Measurement Date |

Superseded |

2016-09 |

03/30/2016 |

718-740-25-5 |

Amended |

2016-09 |

03/30/2016 |

718-740-25-6 |

Amended |

2016-09 |

03/30/2016 |

718-740-25-9 |

Superseded |

2016-09 |

03/30/2016 |

718-740-25-10 |

Superseded |

2016-09 |

03/30/2016 |

718-740-35-2 |

Amended |

2016-09 |

03/30/2016 |

718-740-35-3 |

Superseded |

2016-09 |

03/30/2016 |

718-740-35-5 through 35-9 |

Superseded |

2016-09 |

03/30/2016 |

718-740-45-1 through 45-4 |

Superseded |

2016-09 |

03/30/2016 |

718-740-45-5 |

Amended |

2016-09 |

03/30/2016 |

718-740-45-6 |

Superseded |

2016-09 |

03/30/2016 |

718-740-45-7 |

Amended |

2016-09 |

03/30/2016 |

718-740-45-8 |

Amended |

2016-09 |

03/30/2016 |

718-740-45-9 through 45-12 |

Superseded |

2016-09 |

03/30/2016 |

Paragraph Number |

Action |

Accounting Standards Update |

Date |

740-10-55-35 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

740-20-45-8 |

Amended |

2016-09 |

03/30/2016 |

740-20-45-11 |

Amended |

2016-09 |

03/30/2016 |

740-20-55-2 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

740-270-25-12 |

Amended |

2016-09 |

03/30/2016 |

740-270-30-4 |

Amended |

2016-09 |

03/30/2016 |

740-270-30-8 |

Amended |

2016-09 |

03/30/2016 |

740-270-30-12 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

805-30-55-11 |

Amended |

2016-09 |

03/30/2016 |

Paragraph |

Action |

Accounting Standards Update |

Date |

Excess Tax Benefits |

Superseded |

2016-09 |

03/30/2016 |

805-740-45-5 |

Amended |

2016-09 |

03/30/2016 |

805-740-45-6 |

Superseded |

2016-09 |

03/30/2016 |

Copyright #year# by Financial Accounting Foundation, Norwalk, Connecticut.

Select a section below and enter your search term, or to search all click ASU 2016-09—Compensation—Stock compensation (Topic 718): Improvements to employee share-based payment accounting