3. Amend paragraph 606-10-55-3(i), with a link to transition paragraph 606-10-65-1, as follows:

Implementation Guidance and Illustrations

> Implementation Guidance

606-10-55-3 This implementation guidance is organized into the following categories:

i. Licensing (paragraphs

606-10-55-54 through 55-60 and 606-10-55-62 through 55-65B55-65

)

4. Amend paragraphs 606-10-55-54 through 55-55, 606-10-55-57 through 55-60, and 606-10-55-62 through 55-64, add paragraphs 606-10-55-58A through 55-58C, 606-10-55-63A, 606-10-55-64A, and 606-10-55-65A through 55-65B, and supersede paragraph 606-10-55-61, with a link to transition paragraph 606-10-65-1, as follows:

> > Licensing

606-10-55-54 A license establishes a customer's rights to the intellectual property of an entity. Licenses of intellectual property may include, but are not limited to, licenses of any of the following:

- Software (other than software subject to a hosting arrangement that does not meet the criteria in paragraph 985-20-15-5) and technology

- Motion pictures, music, and other forms of media and entertainment

- Franchises

- Patents, trademarks, and copyrights.

606-10-55-55 In addition to a promise to grant a license (or licenses) to a customer, an entity may also promise to transfer other goods or services to the customer. Those promises may be explicitly stated in the contract or implied by an entity's customary business practices, published policies, or specific statements (see paragraph 606-10-25-16). As with other types of contracts, when a contract with a customer includes a promise to grant a license (or licenses) in addition to other promised goods or services, an entity applies paragraphs 606-10-25-14 through 25-22 to identify each of the performance obligations in the contract.

606-10-55-56 If the promise to grant a license is not distinct from other promised goods or services in the contract in accordance with paragraphs 606-10-25-18 through 25-22, an entity should account for the promise to grant a license and those other promised goods or services together as a single performance obligation. Examples of licenses that are not distinct from other goods or services promised in the contract include the following:

- A license that forms a component of a tangible good and that is integral to the functionality of the good

- A license that the customer can benefit from only in conjunction with a related service (such as an online service provided by the entity that enables, by granting a license, the customer to access content).

606-10-55-57 When a single performance obligation includes a license (or licenses) of intellectual property and one or more other goods or services, the entity considers the nature of the combined good or service for which the customer has contracted (including whether the license that is part of the single performance obligation provides the customer with a right to use or a right to access intellectual property in accordance with paragraphs 606-10-55-59 through 55-60 and 606-10-55-62 through 55-64A) in determining whether that combined good or service is satisfied over time or at a point in time in accordance with paragraphs 606-10-25-23 through 25-30 and, if over time, in selecting an appropriate method for measuring progress in accordance with paragraphs 606-10-25-31 through 25-37. If the license is not distinct, an entity should apply paragraphs 606-10-25-23 through 25-30 to determine whether the performance obligation (which includes the promised license) is a performance obligation that is satisfied over time or satisfied at a point in time

.

606-10-55-58 In evaluating whether a license transfers to a customer at a point in time or over time If the promise to grant the license is distinct from the other promised goods or services in the contract and, therefore, the promise to grant the license is a separate performance obligation, an entity should determine whether the license transfers to a customer either at a point in time or over time. In making this determination

, an entity should consider whether the nature of the entity's promise in granting the license to a customer is to provide the customer with either:

- A right to access the entity's intellectual property

as it exists

throughout the license period (or its remaining economic life, if shorter)

- A right to use the entity's intellectual property as it exists at the point in time at which the license is granted.

606-10-55-58A An entity should account for a promise to provide a customer with a right to access the entity's intellectual property as a performance obligation satisfied over time because the customer will simultaneously receive and consume the benefit from the entity's performance of providing access to its intellectual property as the performance occurs (see paragraph 606-10-25-27(a)). An entity should apply paragraphs 606-10-25-31 through 25-37 to select an appropriate method to measure its progress toward complete satisfaction of that performance obligation to provide access to its intellectual property.

606-10-55-58B An entity's promise to provide a customer with the right to use its intellectual property is satisfied at a point in time. The entity should apply paragraph 606-10-25-30 to determine the point in time at which the license transfers to the customer.

606-10-55-58C Notwithstanding paragraphs 606-10-55-58A through 55-58B, revenue cannot be recognized from a license of intellectual property before both:

- An entity provides (or otherwise makes available) a copy of the intellectual property to the customer.

- The beginning of the period during which the customer is able to use and benefit from its right to access or its right to use the intellectual property. That is, an entity would not recognize revenue before the beginning of the license period even if the entity provides (or otherwise makes available) a copy of the intellectual property before the start of the license period or the customer has a copy of the intellectual property from another transaction. For example, an entity would recognize revenue from a license renewal no earlier than the beginning of the renewal period.

> > > Determining the Nature of the Entity's Promise

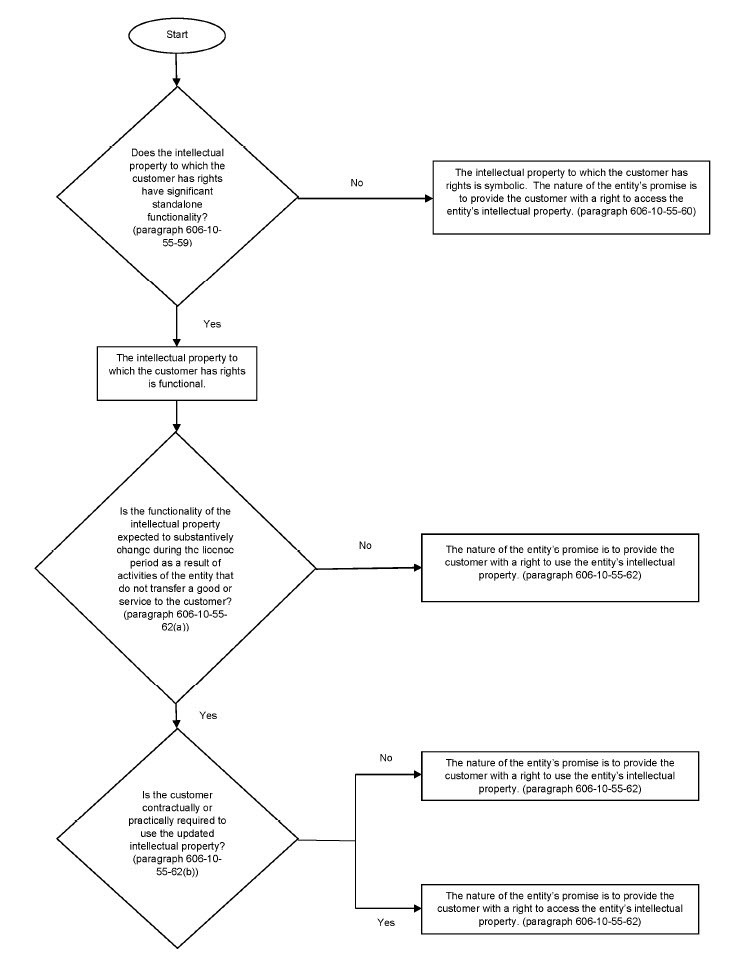

606-10-55-59 To determine whether an entity's promise to grant a license provides a customer with either a right to access an entity's intellectual property or a right to use an entity's intellectual property, an entity should consider whether a customer can direct the use of, and obtain substantially all of the remaining benefits from, a license at the point in time at which the license is granted. A customer cannot direct the use of, and obtain substantially all of the remaining benefits from, a license at the point in time at which the license is granted if the intellectual property to which the customer has rights changes throughout the license period. The intellectual property will change (and thus affect the entity's assessment of when the customer controls the license) when the entity continues to be involved with its intellectual property and the entity undertakes activities that significantly affect the intellectual property to which the customer has rights. In these cases, the license provides the customer with a right to access the entity's intellectual property (see paragraph 606-10-55-60). In contrast, a customer can direct the use of, and obtain substantially all of the remaining benefits from, the license at the point in time at which the license is granted if the intellectual property to which the customer has rights will not change (see paragraph 606-10-55-63). In those cases, any activities undertaken by the entity merely change its own asset (that is, the underlying intellectual property), which may affect the entity's ability to provide future licenses; however, those activities would not affect the determination of what the license provides or what the customer controls.

To determine whether the entity's promise to provide a right to access its intellectual property or a right to use its intellectual property, the entity should consider the nature of the intellectual property to which the customer will have rights. Intellectual property is either:

- Functional intellectual property. Intellectual property that has significant standalone functionality (for example, the ability to process a transaction, perform a function or task, or be played or aired). Functional intellectual property derives a substantial portion of its utility (that is, its ability to provide benefit or value) from its significant standalone functionality.

- Symbolic intellectual property. Intellectual property that is not functional intellectual property (that is, intellectual property that does not have significant standalone functionality). Because symbolic intellectual property does not have significant standalone functionality, substantially all of the utility of symbolic intellectual property is derived from its association with the entity's past or ongoing activities, including its ordinary business activities.

606-10-55-60 A customer's ability to derive benefit from a license to symbolic intellectual property depends on the entity continuing to support or maintain the intellectual property. Therefore, a license to symbolic intellectual property grants the customer a right to access the entity's intellectual property, which is satisfied over time (see paragraphs 606-10-55-58A and 606-10-55-58C) as the entity fulfills its promise to bothThe nature of an entity's promise in granting a license is a promise to provide a right to access the entity's intellectual property if all of the following criteria are met:

- Grant the customer rights to use and benefit from the entity's intellectual property

The contract requires, or the customer reasonably expects, that the entity will undertake activities that significantly affect the intellectual property to which the customer has rights (see paragraph 606-10-55-61).

- Support or maintain the intellectual property. An entity generally supports or maintains symbolic intellectual property by continuing to undertake those activities from which the utility of the intellectual property is derived and/or refraining from activities or other actions that would significantly degrade the utility of the intellectual property.

The rights granted by the license directly expose the customer to any positive or negative effects of the entity's activities identified in paragraph 606-10-55-60(a).

- Subparagraph superseded by Accounting Standards Update No. 2016-10.

Those activities do not result in the transfer of a good or a service to the customer as those activities occur (see paragraph 606-10-25-17).

606-10-55-61 Paragraph superseded by Accounting Standards Update No. 2016-10.Factors that may indicate that a customer could reasonably expect that an entity will undertake activities that significantly affect the intellectual property include the entity's customary business practices, published policies, or specific statements. Although not determinative, the existence of a shared economic interest (for example, a sales-based royalty) between the entity and the customer related to the intellectual property to which the customer has rights may also indicate that the customer could reasonably expect that the entity will undertake such activities.

606-10-55-62 If the criteria in paragraph 606-10-55-60 are met, an entity should account for the promise to grant a license as a performance obligation satisfied over time because the customer will simultaneously receive and consume the benefit from the entity's performance of providing access to its intellectual property as the performance occurs (see paragraph 606-10-25-27(a)). An entity should apply paragraphs 606-10-25-31 through 25-37 to select an appropriate method to measure its progress toward complete satisfaction of that performance obligation to provide access.

A license to functional intellectual property grants a right to use the entity's intellectual property as it exists at the point in time at which the license is granted unless both of the following criteria are met:

- The functionality of the intellectual property to which the customer has rights is expected to substantively change during the license period as a result of activities of the entity that do not transfer a promised good or service to the customer (see paragraphs 606-10-25-16 through 25-18). Additional promised goods or services (for example, intellectual property upgrade rights or rights to use or access additional intellectual property) are not considered in assessing this criterion.

- The customer is contractually or practically required to use the updated intellectual property resulting from the activities in criterion (a).

If both of those criteria are met, then the license grants a right to access the entity's intellectual property.

606-10-55-63 Because functional intellectual property has significant standalone functionality, an entity's activities that do not substantively change that functionality do not significantly affect the utility of the intellectual property to which the customer has rights. Therefore, the entity's promise to the customer in granting a license to functional intellectual property does not include supporting or maintaining the intellectual property. Consequently, if a license to functional intellectual property is a separate performance obligation (see paragraph 606-10-55-55) and does not meet the criteria in paragraph 606-10-55-62, it is satisfied at a point in time (see paragraphs 606-10-55-58B through 55-58C).If the criteria in paragraph 606-10-55-60 are not met, the nature of an entity's promise is to provide a right to use the entity's intellectual property as that intellectual property exists (in terms of form and functionality) at the point in time at which the license is granted to the customer. This means that the customer can direct the use of, and obtain substantially all of the remaining benefits from, the license at the point in time at which the license transfers. An entity should account for the promise to provide a right to use the entity's intellectual property as a performance obligation satisfied at a point in time. An entity should apply paragraph 606-10-25-30 to determine the point in time at which the license transfers to the customer. However, revenue cannot be recognized for a license that provides a right to use the entity's intellectual property before the beginning of the period during which the customer is able to use and benefit from the license. For example, if a software license period begins before an entity provides (or otherwise makes available) to the customer a code that enables the customer to immediately use the software, the entity would not recognize revenue before that code has been provided (or otherwise made available).

606-10-55-63A The following flowchart depicts the decision process for evaluating whether the nature of an entity's promise in granting a license is to provide the customer with a right to access the entity's intellectual property or a right to use the entity's intellectual property. The flowchart does not include all of the guidance on determining the nature of an entity's promise in granting a license of intellectual property in this Subtopic and is not intended as a substitute for the guidance in this Subtopic.

[For ease of readability, the new flowchart is not underlined.]

> > > Other Licensing Considerations

606-10-55-64 Contractual provisions that explicitly or implicitly require an entity to transfer control of additional goods or services to a customer (for example, by requiring the entity to transfer control of additional rights to use or rights to access intellectual property that the customer does not already control) should be distinguished from contractual provisions that explicitly or implicitly define the attributes of a single promised license (for example, restrictions of time, geographical region, or use). Attributes of a promised license define the scope of a customer's right to use or right to access the entity's intellectual property and, therefore, do not define whether the entity satisfies its performance obligation at a point in time or over time and do not create an obligation for the entity to transfer any additional rights to use or access its intellectual property. An entity should disregard the following factors when determining whether a license provides a right to access the entity's intellectual property or a right to use the entity's intellectual property:

- Subparagraph superseded by Accounting Standards Update No. 2016-10.

Restrictions of time, geographical region, or use Those restrictions define the attributes of the promised license, rather than define whether the entity satisfies its performance obligation at a point in time or over time

- Subparagraph superseded by Accounting Standards Update No. 2016-10.

Guarantees provided by the entity that it has a valid patent to intellectual property and that it will defend that patent from unauthorized use A promise to defend a patent right is not a performance obligation because the act of defending a patent protects the value of the entity's intellectual property assets and provides assurance to the customer that the license transferred meets the specifications of the license promised in the contract.

[Content amended and moved to paragraph 606-10-55-64A]

606-10-55-64A Guarantees provided by the entity that it has a valid patent to intellectual property and that it will defend that patent from unauthorized use—

do not affect whether a license provides a right to access the entity's intellectual property or a right to use the entity's intellectual property. Similarly, a A

promise to defend a patent right is not a

promised good or service performance obligation because the act of defending a patent protects the value of the entity's intellectual property assets

and

it provides assurance to the customer that the license transferred meets the specifications of the license promised in the contract.

[Content amended as shown and moved from paragraph 606-10-55-64(b)]

> > > Sales-Based or Usage-Based Royalties

606-10-55-65 Notwithstanding the guidance in paragraphs 606-10-32-11 through 32-14, an entity should recognize revenue for a sales-based or usage-based royalty promised in exchange for a license of intellectual property only when (or as) the later of the following events occurs:

- The subsequent sale or usage occurs.

- The performance obligation to which some or all of the sales-based or usage-based royalty has been allocated has been satisfied (or partially satisfied).

606-10-55-65A The guidance for a sales-based or usage-based royalty in paragraph 606-10-55-65 applies when the royalty relates only to a license of intellectual property or when a license of intellectual property is the predominant item to which the royalty relates (for example, the license of intellectual property may be the predominant item to which the royalty relates when the entity has a reasonable expectation that the customer would ascribe significantly more value to the license than to the other goods or services to which the royalty relates).

606-10-55-65B When the guidance in paragraph 606-10-55-65A is met, revenue from a sales-based or usage-based royalty should be recognized wholly in accordance with the guidance in paragraph 606-10-55-65. When the guidance in paragraph 606-10-55-65A is not met, the guidance on variable consideration in paragraphs 606-10-32-5 through 32-14 applies to the sales-based or usage-based royalty.

5. Amend paragraph 606-10-55-93(c) and (s), with a link to transition paragraph 606-10-65-1, as follows:

> Illustrations

606-10-55-93 The Examples are organized as follows:

c. Identifying Performance Obligations

Example 10—Goods and Services Are Not Distinct

Example 11—Determining Whether Goods or Services Are Distinct

Example 12—Explicit and Implicit Promises in a Contract

Example 12A—Series of Distinct Goods or Services

s. Licensing

Example 54—Right to Use Intellectual Property Example 55—License of Intellectual Property

Example 56—Identifying a Distinct License

Example 57—Franchise Rights Example

58—Access to Intellectual Property

Example 59—Right to Use Intellectual Property

Example 60—

Sales-Based Royalty Promised in Exchange for a License of Intellectual Property and Other Goods and Services Access to Intellectual Property

Example 61—Access to Intellectual Property

Example 61A—Right to Use Intellectual Property

Example 61B—Distinguishing Multiple Licenses from Attributes of a Single License6. Amend paragraphs 606-10-55-136 through 55-137, 606-10-55-139, 606-10-55-142 through 55-143, 606-10-55-145, 606-10-55-147 through 55-150, 606-10-55-153, 606-10-55-155, and the heading preceding paragraph 606-10-55-156 and add paragraphs 606-10-55-140A through 55-140F and their related headings, 606-10-55-150A through 55-150K and their related headings, paragraph 606-10-55-153A, and 606-10-55-157A through 55-157E and the related heading, with a link to transition paragraph 606-10-65-1, as follows:

> > Identifying Performance Obligations

606-10-55-136 Examples

10–12

10–12A illustrate the guidance in paragraphs 606-10-25-14 through 25-22 on identifying performance obligations.

> > > Example 10—Goods and Services Are Not Distinct

> > > > Case A—Significant Integration Service

606-10-55-137 An entity, a contractor, enters into a contract to build a hospital for a customer. The entity is responsible for the overall management of the project and identifies various

promised goods and services

to be provided

, including engineering, site clearance, foundation, procurement, construction of the structure, piping and wiring, installation of equipment, and finishing.

606-10-55-138 The promised goods and services are capable of being distinct in accordance with paragraph 606-10-25-19(a). That is, the customer can benefit from the goods and services either on their own or together with other readily available resources. This is evidenced by the fact that the entity, or competitors of the entity, regularly sells many of these goods and services separately to other customers. In addition, the customer could generate economic benefit from the individual goods and services by using, consuming, selling, or holding those goods or services.

606-10-55-139 However,

the promises to transfer the goods and services are not

separately identifiable distinct within the context of the contract

in accordance with paragraph 606-10-25-19(b) (on the basis of the factors in paragraph 606-10-25-21).

That is, the entity's promise to transfer individual goods and services in the contract are not separately identifiable from other promises in the contract.

This is evidenced by the fact that the entity provides a significant service of integrating the goods and services (the inputs) into the hospital (the combined output) for which the customer has contracted.

606-10-55-140 Because both criteria in paragraph 606-10-25-19 are not met, the goods and services are not distinct. The entity accounts for all of the goods and services in the contract as a single performance obligation.

> > > > Case B—Significant Integration Service

606-10-55-140A An entity enters into a contract with a customer that will result in the delivery of multiple units of a highly complex, specialized device. The terms of the contract require the entity to establish a manufacturing process in order to produce the contracted units. The specifications are unique to the customer based on a custom design that is owned by the customer and that were developed under the terms of a separate contract that is not part of the current negotiated exchange. The entity is responsible for the overall management of the contract, which requires the performance and integration of various activities including procurement of materials; identifying and managing subcontractors; and performing manufacturing, assembly, and testing.

606-10-55-140B The entity assesses the promises in the contract and determines that each of the promised devices is capable of being distinct in accordance with paragraph 606-10-25-19(a) because the customer can benefit from each device on its own. This is because each unit can function independently of the other units.

606-10-55-140C The entity observes that the nature of its promise is to establish and provide a service of producing the full complement of devices for which the customer has contracted in accordance with the customer's specifications. The entity considers that it is responsible for overall management of the contract and for providing a significant service of integrating various goods and services (the inputs) into its overall service and the resulting devices (the combined output) and, therefore, the devices and the various promised goods and services inherent in producing those devices are not separately identifiable in accordance with paragraphs 606-10-25-19(b) and 606-10-25-21. In this Case, the manufacturing process provided by the entity is specific to its contract with the customer. In addition, the nature of the entity's performance and, in particular, the significant integration service of the various activities mean that a change in one of the entity's activities to produce the devices has a significant effect on the other activities required to produce the highly complex specialized devices such that the entity's activities are highly interdependent and highly interrelated. Because the criterion in paragraph 606-10-25-19(b) is not met, the goods and services that will be provided by the entity are not separately identifiable, and, therefore, are not distinct. The entity accounts for all of the goods and services promised in the contract as a single performance obligation.

> > > > Case C—Combined Item

606-10-55-140D An entity grants a customer a three-year term license to anti-virus software and promises to provide the customer with when-and-if available updates to that software during the license period. The entity frequently provides updates that are critical to the continued utility of the software. Without the updates, the customer's ability to benefit from the software would decline significantly during the three-year arrangement.

606-10-55-140E The entity concludes that the software and the updates are each promised goods or services in the contract and are each capable of being distinct in accordance with paragraph 606-10-25-19(a). The software and the updates are capable of being distinct because the customer can derive economic benefit from the software on its own throughout the license period (that is, without the updates the software would still provide its original functionality to the customer), while the customer can benefit from the updates together with the software license transferred at the outset of the contract.

606-10-55-140F The entity concludes that its promises to transfer the software license and to provide the updates, when-and-if available, are not separately identifiable (in accordance with paragraph 606-10-25-19(b)) because the license and the updates are, in effect, inputs to a combined item (anti-virus protection) in the contract. The updates significantly modify the functionality of the software (that is, they permit the software to protect the customer from a significant number of additional viruses that the software did not protect against previously) and are integral to maintaining the utility of the software license to the customer. Consequently, the license and updates fulfill a single promise to the customer in the contract (a promise to provide protection from computer viruses for three years). Therefore, in this Example, the entity accounts for the software license and the when-and-if available updates as a single performance obligation. In accordance with paragraph 606-10-25-33, the entity concludes that the nature of the combined good or service it promised to transfer to the customer in this Example is computer virus protection for three years. The entity considers the nature of the combined good or service (that is, to provide anti-virus protection for three years) in determining whether the performance obligation is satisfied over time or at a point in time in accordance with paragraphs 606-10-25-23 through 25-30 and in determining the appropriate method for measuring progress toward complete satisfaction of the performance obligation in accordance with paragraphs 606-10-25-31 through 25-37.

> > > Example 11—Determining Whether Goods or Services Are Distinct

> > > > Case A—Distinct Goods or Services

606-10-55-141 An entity, a software developer, enters into a contract with a customer to transfer a software license, perform an installation service, and provide unspecified software updates and technical support (online and telephone) for a two-year period. The entity sells the license, installation service, and technical support separately. The installation service includes changing the web screen for each type of user (for example, marketing, inventory management, and information technology). The installation service is routinely performed by other entities and does not significantly modify the software. The software remains functional without the updates and the technical support.

606-10-55-142 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct in accordance with paragraph 606-10-25-19. The entity observes that the software is delivered before the other goods and services and remains functional without the updates and the technical support. The customer can benefit from the updates together with the software license transferred at the outset of the contract. Thus, the entity concludes that the customer can benefit from each of the goods and services either on their own or together with the other goods and services that are readily available and the criterion in paragraph 606-10-25-19(a) is met.

606-10-55-143 The entity also considers the

principle and the factors in paragraph 606-10-25-21 and determines that the promise to transfer each good and service to the customer is separately identifiable from each of the other promises (thus, the criterion in paragraph 606-10-25-19(b) is met).

In reaching this determination the entity considers that although it integrates the software into the customer's system, the installation services do not significantly affect the customer's ability to use and benefit from the software license because the installation services are routine and can be obtained from alternate providers. The software updates do not significantly affect the customer's ability to use and benefit from the software license because, in contrast with Example 10 (Case C), the software updates in this contract are not necessary to ensure that the software maintains a high level of utility to the customer during the license period. The entity further observes that none of the promised goods or services significantly modify or customize one another and the entity is not providing a significant service of integrating the software and the services into a combined output. Lastly, the entity concludes that the software and the services do not significantly affect each other and, therefore, are not highly interdependent or highly interrelated because the entity would be able to fulfill its promise to transfer the initial software license independent from its promise to subsequently provide the installation service, software updates, or technical support. In particular, the entity observes that the installation service does not significantly modify or customize the software itself, and, as such, the software and the installation service are separate outputs promised by the entity instead of inputs used to produce a combined output.

606-10-55-144 On the basis of this assessment, the entity identifies four performance obligations in the contract for the following goods or services:

- The software license

- An installation service

- Software updates

- Technical support.

606-10-55-145 The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether each of the performance obligations for the installation service, software updates, and technical support are satisfied at a point in time or over time. The entity also assesses the nature of the entity's promise to transfer the software license in accordance with

paragraph 606-10-55-60

paragraphs 606-10-55-59 through 55-60 and 606-10-55-62 through 55-64A (see Example 54 in paragraphs 606-10-55-362 through

55-363B 55-363).

> > > > Case B—Significant Customization

606-10-55-146 The promised goods and services are the same as in Case A, except that the contract specifies that, as part of the installation service, the software is to be substantially customized to add significant new functionality to enable the software to interface with other customized software applications used by the customer. The customized installation service can be provided by other entities.

606-10-55-147 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct in accordance with paragraph 606-10-25-19.

The entity first assesses whether the criterion in paragraph 606-10-25-19(a) has been met. For the same reasons as in Case A, the entity determines that the software license, installation, software updates, and technical support each meet that criterion. The entity next assesses whether the criterion in paragraph 606-10-25-19(b) has been met by evaluating the principle and the factors in paragraph 606-10-25-21. The entity observes that the terms of the contract result in a promise to provide a significant service of integrating the licensed software into the existing software system by performing a customized installation service as specified in the contract. In other words, the entity is using the license and the customized installation service as inputs to produce the combined output (that is, a functional and integrated software system) specified in the contract (see paragraph 606-10-25-21(a)).

In addition, the

The software is significantly modified and customized by the service (see paragraph 606-10-2521(b)).

Although the customized installation service can be provided by other entities

,

Consequently, the entity determines that

within the context of the contract

, the promise to transfer the license is not separately identifiable from the customized installation service and, therefore, the criterion in paragraph 606-10-25-19(b)

(on the basis of the factors in paragraph 606-10-25-21)

is not met. Thus, the software license and the customized installation service are not distinct.

606-10-55-148 As in Case A

,

On the basis of the same analysis as in Case A, the entity concludes that the software updates and technical support are distinct from the other promises in the contract.

This is because the customer can benefit from the updates and technical support either on their own or together with the other goods and services that are readily available and because the promise to transfer the software updates and the technical support to the customer are separately identifiable from each of the other promises.

606-10-55-149 On the basis of this assessment, the entity identifies three performance obligations in the contract for the following goods or services:

Customized

Software customization installation service (that which is comprised of the license to the software and the customized installation service includes the software license)

- Software updates

- Technical support.

606-10-55-150 The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether each performance obligation is satisfied at a point in time or over time and paragraphs 606-10-25-31 through 25-37 to measure progress toward complete satisfaction of those performance obligations determined to be satisfied over time. In applying those paragraphs to the software customization, the entity considers that the customized software to which the customer will have rights is functional intellectual property and that the functionality of that software will not change during the license period as a result of activities that do not transfer a good or service to the customer. Therefore, the entity is providing a right to use the customized software. Consequently, the software customization performance obligation is completely satisfied upon completion of the customized installation service. The entity considers the other specific facts and circumstances of the contract in the context of the guidance in paragraphs 606-10-25-23 through 25-30 in determining whether it should recognize revenue related to the single software customization performance obligation as it performs the customized installation service or at the point in time the customized software is transferred to the customer.

> > > > Case C—Promises Are Separately Identifiable (Installation)

606-10-55-150A An entity contracts with a customer to sell a piece of equipment and installation services. The equipment is operational without any customization or modification. The installation required is not complex and is capable of being performed by several alternative service providers.

606-10-55-150B The entity identifies two promised goods and services in the contract: (a) equipment and (b) installation. The entity assesses the criteria in paragraph 606-10-25-19 to determine whether each promised good or service is distinct. The entity determines that the equipment and the installation each meet the criterion in paragraph 606-10-25-19(a). The customer can benefit from the equipment on its own, by using it or reselling it for an amount greater than scrap value, or together with other readily available resources (for example, installation services available from alternative providers). The customer also can benefit from the installation services together with other resources that the customer will already have obtained from the entity (that is, the equipment).

606-10-55-150C The entity further determines that its promises to transfer the equipment and to provide the installation services are each separately identifiable (in accordance with paragraph 606-10-25-19(b)). The entity considers the principle and the factors in paragraph 606-10-25-21 in determining that the equipment and the installation services are not inputs to a combined item in this contract. In this Case, each of the factors in paragraph 606-10-25-21 contributes to, but is not individually determinative of, the conclusion that the equipment and the installation services are separately identifiable as follows:

- The entity is not providing a significant integration service. That is, the entity has promised to deliver the equipment and then install it; the entity would be able to fulfill its promise to transfer the equipment separately from its promise to subsequently install it. The entity has not promised to combine the equipment and the installation services in a way that would transform them into a combined output.

- The entity's installation services will not significantly customize or significantly modify the equipment.

- Although the customer can benefit from the installation services only after it has obtained control of the equipment, the installation services do not significantly affect the equipment because the entity would be able to fulfill its promise to transfer the equipment independently of its promise to provide the installation services. Because the equipment and the installation services do not each significantly affect the other, they are not highly interdependent or highly interrelated.

On the basis of this assessment, the entity identifies two performance obligations (the equipment and installation services) in the contract.

606-10-55-150D The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether each performance obligation is satisfied at a point in time or over time.

> > > > Case D—Promises Are Separately Identifiable (Contractual Restrictions)

606-10-55-150E Assume the same facts as in Case C, except that the customer is contractually required to use the entity's installation services.

606-10-55-150F The contractual requirement to use the entity's installation services does not change the evaluation of whether the promised goods and services are distinct in this Case. This is because the contractual requirement to use the entity's installation services does not change the characteristics of the goods or services themselves, nor does it change the entity's promises to the customer. Although the customer is required to use the entity's installation services, the equipment and the installation services are capable of being distinct (that is, they each meet the criterion in paragraph 606-10-25-19(a)), and the entity's promises to provide the equipment and to provide the installation services are each separately identifiable (that is, they each meet the criterion in paragraph 606-10-25-19(b)). The entity's analysis in this regard is consistent with Case C.

> > > > Case E—Promises Are Separately Identifiable (Consumables)

606-10-55-150G An entity enters into a contract with a customer to provide a piece of off-the-shelf equipment (that is, it is operational without any significant customization or modification) and to provide specialized consumables for use in the equipment at predetermined intervals over the next three years. The consumables are produced only by the entity, but are sold separately by the entity.

606-10-55-150H The entity determines that the customer can benefit from the equipment together with the readily available consumables. The consumables are readily available in accordance with paragraph 606-10-25-20 because they are regularly sold separately by the entity (that is, through refill orders to customers that previously purchased the equipment). The customer can benefit from the consumables that will be delivered under the contract together with the delivered equipment that is transferred to the customer initially under the contract. Therefore, the equipment and the consumables are each capable of being distinct in accordance with paragraph 606-10-25-19(a).

606-10-55-150I The entity determines that its promises to transfer the equipment and to provide consumables over a three-year period are each separately identifiable in accordance with paragraph 606-10-25-19(b). In determining that the equipment and the consumables are not inputs to a combined item in this contract, the entity considers that it is not providing a significant integration service that transforms the equipment and consumables into a combined output. Additionally, neither the equipment nor the consumables are significantly customized or modified by the other. Lastly, the entity concludes that the equipment and the consumables are not highly interdependent or highly interrelated because they do not significantly affect each other. Although the customer can benefit from the consumables in this contract only after it has obtained control of the equipment (that is, the consumables would have no use without the equipment) and the consumables are required for the equipment to function, the equipment and the consumables do not each significantly affect the other. This is because the entity would be able to fulfill each of its promises in the contract independently of the other. That is, the entity would be able to fulfill its promise to transfer the equipment even if the customer did not purchase any consumables and would be able to fulfill its promise to provide the consumables even if the customer acquired the equipment separately.

606-10-55-150J On the basis of this assessment, the entity identifies two performance obligations in the contract for the following goods or services:

- The equipment

- The consumables.

606-10-55-150K The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether each performance obligation is satisfied at a point in time or over time.

> > > Example 12—Explicit and Implicit Promises in a Contract

606-10-55-151 An entity, a manufacturer, sells a product to a distributor (that is, its customer), who will then resell it to an end customer.

> > > > Case A—Explicit Promise of Service

606-10-55-152 In the contract with the distributor, the entity promises to provide maintenance services for no additional consideration (that is, free) to any party (that is, the end customer) that purchases the product from the distributor. The entity outsources the performance of the maintenance services to the distributor and pays the distributor an agreed-upon amount for providing those services on the entity's behalf. If the end customer does not use the maintenance services, the entity is not obliged to pay the distributor.

606-10-55-153 The contract with the customer includes two promised goods or services—(a) the product and (b) the maintenance services (because Because

the promise of maintenance services is a promise to transfer goods or services in the future and is part of the negotiated exchange between the entity and the

distributor). distributor, the entity determines that the promise to provide maintenance services is a performance obligation (see paragraph 606-10-25-18(g)). The entity concludes that the promise would represent a performance obligation regardless of whether the entity, the distributor, or a third party provides the service. Consequently, the entity allocates a portion of the transaction price to the promise to provide maintenance services.

The entity assesses whether each good or service is distinct in accordance with paragraph 606-10-25-19. The entity determines that both the product and the maintenance services meet the criterion in paragraph 606-10-25-19(a). The entity regularly sells the product on a standalone basis, which indicates that the customer can benefit from the product on its own. The customer can benefit from the maintenance services together with a resource the customer already has obtained from the entity (that is, the product).

606-10-55-153A The entity further determines that its promises to transfer the product and to provide the maintenance services are separately identifiable (in accordance with paragraph 606-10-25-19(b)) on the basis of the principle and the factors in paragraph 606-10-25-21. The product and the maintenance services are not inputs to a combined item in this contract. The entity is not providing a significant integration service because the presence of the product and the services together in this contract do not result in any additional or combined functionality. In addition, neither the product nor the services modify or customize the other. Lastly, the product and the maintenance services are not highly interdependent or highly interrelated because the entity would be able to satisfy each of the promises in the contract independent of its efforts to satisfy the other (that is, the entity would be able to transfer the product even if the customer declined maintenance services and would be able to provide maintenance services in relation to products sold previously through other distributors). The entity also observes, in applying the principle in paragraph 606-10-25-21, that the entity's promise to provide maintenance is not necessary for the product to continue to provide significant benefit to the customer. Consequently, the entity allocates a portion of the transaction price to each of the two performance obligations (that is, the product and the maintenance services) in the contract.

> > > > Case B—Implicit Promise of Service

606-10-55-154 The entity has historically provided maintenance services for no additional consideration (that is, "free") to end customers that purchase the entity's product from the distributor. The entity does not explicitly promise maintenance services during negotiations with the distributor, and the final contract between the entity and the distributor does not specify terms or conditions for those services.

606-10-55-155 However, on the basis of its customary business practice, the entity determines at contract inception that it has made an implicit promise to provide maintenance services as part of the negotiated exchange with the distributor. That is, the entity's past practices of providing these services create

valid

reasonable expectations of the entity's customers (that is, the distributor and end customers) in accordance with paragraph 606-10-25-16. Consequently, the entity

identifies

assesses whether the promise of maintenance services as

is a performance obligation

. For the same reasons as in Case A, the entity determines that the product and maintenance services are separate performance obligations to which it allocates a portion of the transaction price.

> > > > Case C—Services Are Not a Promised Service Performance Obligation

606-10-55-156 In the contract with the distributor, the entity does not promise to provide any maintenance services. In addition, the entity typically does not provide maintenance services, and, therefore, the entity's customary business practices, published policies, and specific statements at the time of entering into the contract have not created an implicit promise to provide goods or services to its customers. The entity transfers control of the product to the distributor and, therefore, the contract is completed. However, before the sale to the end customer, the entity makes an offer to provide maintenance services to any party that purchases the product from the distributor for no additional promised consideration.

606-10-55-157 The promise of maintenance is not included in the contract between the entity and the distributor at contract inception. That is, in accordance with paragraph 606-10-25-16, the entity does not explicitly or implicitly promise to provide maintenance services to the distributor or the end customers. Consequently, the entity does not identify the promise to provide maintenance services as a performance obligation. Instead, the obligation to provide maintenance services is accounted for in accordance with Topic 450 on contingencies.

606-10-55-157A Although the maintenance services are not a promised service in the current contract, in future contracts with customers the entity would assess whether it has created a business practice resulting in an implied promise to provide maintenance services.

> > > Example 12A—Series of Distinct Goods or Services

606-10-55-157B An entity, a hotel manager, enters into a contract with a customer to manage a customer-owned property for 20 years. The entity receives consideration monthly that is equal to 1 percent of the revenue from the customer-owned property.

606-10-55-157C The entity evaluates the nature of its promise to the customer in this contract and determines that its promise is to provide a hotel management service. The service comprises various activities that may vary each day (for example, cleaning services, reservation services, and property maintenance). However, those tasks are activities to fulfill the hotel management service and are not separate promises in the contract. The entity determines that each increment of the promised service (for example, each day of the management service) is distinct in accordance with paragraph 606-10-25-19. This is because the customer can benefit from each increment of service on its own (that is, it is capable of being distinct) and each increment of service is separately identifiable because no day of service significantly modifies or customizes another and no day of service significantly affects either the entity's ability to fulfill another day of service or the benefit to the customer of another day of service.

606-10-55-157D The entity also evaluates whether it is providing a series of distinct goods or services in accordance with paragraphs 606-10-25-14 through 25-15. First, the entity determines that the services provided each day are substantially the same. This is because the nature of the entity's promise is the same each day and the entity is providing the same overall management service each day (although the underlying tasks or activities the entity performs to provide that service may vary from day to day). The entity then determines that the services have the same pattern of transfer to the customer because both criteria in paragraph 606-10-25-15 are met. The entity determines that the criterion in paragraph 606-10-25-15(a) is met because each distinct service meets the criteria in paragraph 606-10-25-27 to be a performance obligation satisfied over time. The customer simultaneously receives and consumes the benefits provided by the entity as it performs. The entity determines that the criterion in paragraph 606-10-25-15(b) also is met because the same measure of progress (in this case, a timebased output method) would be used to measure the entity's progress toward satisfying its promise to provide the hotel management service each day.

606-10-55-157E After determining that the entity is providing a series of distinct daily hotel management services over the 20-year management period, the entity next determines the transaction price. The entity determines that the entire amount of the consideration is variable consideration. The entity considers whether the variable consideration may be allocated to one or more, but not all, of the distinct days of service in the series in accordance with paragraph 606-10-32-39(b). The entity evaluates the criteria in paragraph 606-10-32-40 and determines that the terms of the variable consideration relate specifically to the entity's efforts to transfer each distinct daily service and that allocation of the variable consideration earned based on the activities performed by the entity each day to the distinct day in which those activities are performed is consistent with the overall allocation objective. Therefore, as each distinct daily service is completed, the variable consideration allocated to that period may be recognized, subject to the constraint on variable consideration.

7. Amend paragraphs 606-10-55-309 and 606-10-55-311 through 55-313, with a link to transition paragraph 606-10-65-1, as follows:

> > > Example 44—Warranties

606-10-55-309 An entity, a manufacturer, provides its customer with a warranty with the purchase of a product. The warranty provides assurance that the product complies with agreed-upon specifications and will operate as promised for one year from the date of purchase. The contract also provides the customer with the right to receive up to 20 hours of training services on how to operate the product at no additional cost. The training services will help the customer optimize its use of the product in a short time frame. Therefore, although the training services are only for 20 hours and are not essential to the customer's ability to use the product, the entity determines that the training services are material in the context of the contract on the basis of the facts and circumstances of the arrangement.

606-10-55-310 The entity assesses the goods and services in the contract to determine whether they are distinct and therefore give rise to separate performance obligations.

606-10-55-311 The product is distinct because it meets both criteria in paragraph 606-10-25-19.

The product

and training services are each is

capable of being distinct in accordance with paragraphs 606-10-25-19(a) and 606-10-25-20 because the customer can benefit from the product on its own without the training services

and can benefit from the training services together with the product that already has been transferred by the entity. The entity regularly sells the product separately without the training services.

In addition, the product is distinct within the context of the contract in accordance with paragraphs 606-10-25-19(b) and 606-10-25-21 because the entity's promise to transfer the product is separately identifiable from other promises in the contract.

606-10-55-312 In addition, the training services are distinct because they meet both criteria in paragraph 606-10-25-19. The training services are capable of being distinct in accordance with paragraphs 606-10-25-19(a) and 606-10-25-20 because the customer can benefit from the training services together with the product that has already been provided by the entity. In addition, the training services are distinct within the context of the contract in accordance with

The entity next assesses whether its promises to transfer the product and to provide the training services are separately identifiable in accordance with paragraphs 606-10-25-19(b) and 606-10-25-21

because the entity's promise to transfer the training services are separately identifiable from other promises in the contract

. The entity does not provide a significant service of integrating the training services with the product (see paragraph 606-10-25-21(a)). The training services

and product are not

do not significantly

modify or customize each other modified or customized by the product

(see paragraph 606-10-25-21(b)). The

product and the training services are not highly

interdependent dependent on,

or highly interrelated with, the product as described in paragraph 606-10-25-21(c).

The entity would be able to fulfill its promise to transfer the product independent of its efforts to subsequently provide the training services and would be able to provide training services to any customer that previously acquired its product. Consequently, the entity concludes that its promise to transfer the product and its promise to provide training services are not inputs to a combined item and, therefore, are each separately identifiable.

606-10-55-313 The product and training services are each distinct in accordance with paragraph 606-10-25-19 and therefore give rise to two separate performance obligations.

606-10-55-314 Finally, the entity assesses the promise to provide a warranty and observes that the warranty provides the customer with the assurance that the product will function as intended for one year. The entity concludes, in accordance with paragraphs 606-10-55-30 through 55-35, that the warranty does not provide the customer with a good or service in addition to that assurance and, therefore, the entity does not account for it as a performance obligation. The entity accounts for the assurance-type warranty in accordance with the requirements on product warranties in Subtopic 460-10.

606-10-55-315 As a result, the entity allocates the transaction price to the two performance obligations (the product and the training services) and recognizes revenue when (or as) those performance obligations are satisfied.

8. Amend paragraphs 606-10-55-361, 606-10-55-363 through 55-368, 606-10-55-370 through 55-383, 606-10-55-385 through 55-389, 606-10-55-391 through 55-394, and 606-10-55-396 through 55-399 and add paragraphs 606-10-55-363A through 55-363B, 606-10-55-365A, 606-10-55-372A, 606-10-55-392A though 55-392D and their related heading, and 606-10-55-399A through 55-399O and their related headings, with a link to transition paragraph 606-10-65-1, as follows:

> > Licensing

606-10-55-361 Examples 54–

61B 61

illustrate the guidance in paragraphs 606-10-25-14 through 25-22 on identifying performance obligations and paragraphs 606-10-55-54 through 55-

60 and 606-10-55-62 through 55-65B65

on licensing. These Examples also illustrate other guidance as follows:

- Paragraphs 606-10-25-31 through 25-37 on measuring progress toward complete satisfaction of a performance obligation

(Example

Examples 57 and 58)

- Paragraphs 606-10-32-39 through 32-41 on allocating variable consideration to performance obligations (Example 57)

Paragraph

Paragraphs 606-10-55-65 through 55-65B on consideration in the form of sales-based or usage-based royalties on licenses of intellectual property (Examples 57 and 61).

> > > Example 54—Right to Use Intellectual Property

606-10-55-362 Using the same facts as in Case A in Example 11 (see paragraphs 606-10-55-141 through 55-145), the entity identifies four performance obligations in a contract:

- The software license

- Installation services

- Software updates

- Technical support.

606-10-55-363 The entity assesses the nature of its promise to transfer the software license

. The entity first concludes that the software to which the customer obtains rights as a result of the license is functional intellectual property. This is because the software has significant standalone functionality from which the customer can derive substantial benefit regardless of the entity's ongoing business activities. in accordance with paragraph 606-10-55-60. The entity observes that the software is functional at the time that the license transfers to the customer, and the customer can direct the use of, and obtain substantially all of the remaining benefits from, the software when the license transfers to the customer. Furthermore, the entity concludes that because the software is functional when it transfers to the customer, the customer does not reasonably expect the entity to undertake activities that significantly affect the intellectual property to which the license relates. This is because at the point in time that the license is transferred to the customer, the intellectual property will not change throughout the license period. The entity does not consider in its assessment of the criteria in paragraph 606-10-55-60 the promise to provide software updates because they represent a separate performance obligation. Therefore, the entity concludes that none of the criteria in paragraph 606-10-55-60 are met and that the nature of the entity's promise in transferring the license is to provide a right to use the entity's intellectual property as it exists at a point in time—that is, the intellectual property to which the customer has rights is static. Consequently, the entity accounts for the license as a performance obligation satisfied at a point in time.

606-10-55-363A The entity further concludes that while the functionality of the underlying software is expected to change during the license period as a result of the entity's continued development efforts, the functionality of the software to which the customer has rights (that is, the customer's instance of the software) will change only as a result of the entity's promise to provide when-and-if available software updates. Because the entity's promise to provide software updates represents an additional promised service in the contract, the entity's activities to fulfill that promised service are not considered in evaluating the criteria in paragraph 606-10-55-62. The entity further notes that the customer has the right to install, or not install, software updates when they are provided such that the criterion in 606-10-55-62(b) would not be met even if the entity's activities to develop and provide software updates had met the criterion in paragraph 606-10-55-62(a).

606-10-55-363B Therefore, the entity concludes that it has provided the customer with a right to use its software as it exists at the point in time the license is granted and the entity accounts for the software license performance obligation as a performance obligation satisfied at a point in time. The entity recognizes revenue on the software license performance obligation in accordance with paragraphs 606-10-55-58B through 55-58C.

> > > Example 55—License of Intellectual Property

606-10-55-364 An entity enters into a contract with a customer to license (for a period of three years) intellectual property related to the design and production processes for a good. The contract also specifies that the customer will obtain any updates to that intellectual property for new designs or production processes that may be developed by the entity. The updates are

essential

integral to the customer's ability to

derive benefit from use

the license

during the license period because the

customer operates

intellectual property is used in an industry in which technologies change rapidly.

The entity does not sell the updates separately, and the customer does not have the option to purchase the license without the updates.

606-10-55-365 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct in accordance with paragraph 606-10-25-19.

The entity determines that the customer can benefit from (a) the license on its own without the updates and (b) the updates together with the initial license. Although the benefit the customer can derive from the license on its own (that is, without the updates) is limited because the updates are integral to the customer's ability to continue to use the intellectual property in an industry in which technologies change rapidly, the license can be used in a way that generates some economic benefits. Therefore, the criterion in paragraph 606-10-25-19(a) is met for the license and the updates. The entity determines that although the entity can conclude that the customer can obtain benefit from the license on its own without the updates (see paragraph 606-10-25-19(a)), that benefit would be limited because the updates are critical to the customer's ability to continue to make use of the license in the rapidly changing technological environment in which the customer operates. In assessing whether the criterion in paragraph 606-10-25-19(b) is met, the entity observes that the customer does not have the option to purchase the license without the updates and the customer obtains limited benefit from the license without the updates. Therefore, the entity concludes that the license and the updates are highly interrelated and the promise to grant the license is not distinct within the context of the contract because the license is not separately identifiable from the promise to provide the updates (in accordance with the criterion in paragraph 606-10-25-19(b) and the factors in paragraph 606-10-25-21).

606-10-55-365A The fact that the benefit the customer can derive from the license on its own (that is, without the updates) is limited (because the updates are integral to the customer's ability to continue to use the license in the rapidly changing technological environment) also is considered in assessing whether the criterion in paragraph 606-10-25-19(b) is met. Because the benefit that the customer could obtain from the license over the three-year term without the updates would be significantly limited, the entity's promises to grant the license and to provide the expected updates are, in effect, inputs that, together fulfill a single promise to deliver a combined item to the customer. That is, the nature of the entity's promise in the contract is to provide ongoing access to the entity's intellectual property related to the design and production processes for a good for the three-year term of the contract. The promises within that combined item (that is, to grant the license and to provide when-and-if available updates) are therefore not separately identifiable in accordance with the criterion in paragraph 606-10-25-19(b).

606-10-55-366 The

nature of the combined good or service that the entity promised to transfer to the customer is ongoing access to the entity's intellectual property related to the design and production processes for a good for the three-year term of the contract. Based on this conclusion, the entity applies paragraphs 606-10-25-23 through 25-30 to determine whether the

single performance obligation

(which includes the license and the updates)

is satisfied at a point in time or over time

and paragraphs 606-10-25-31 through 25-37 to determine the appropriate method for measuring progress toward complete satisfaction of the performance obligation. The entity concludes that because the customer simultaneously receives and consumes the benefits of the entity's performance as it occurs, the performance obligation is satisfied over time in accordance with paragraph 606-10-25-27(a)

and that a time-based input measure of progress is appropriate because the entity expects, on the basis of its relevant history with similar contracts, to expend efforts to develop and transfer updates to the customer on a generally even basis throughout the three-year term.

> > > Example 56—Identifying a Distinct License

606-10-55-367 An entity, a pharmaceutical company, licenses to a customer its patent rights to an approved drug compound for 10 years and also promises to manufacture the drug for the customer

for 5 years, while the customer develops its own manufacturing capability. The drug is a mature product; therefore,

there is no expectation that the entity will

not

undertake

any

activities to

change support

the drug

(for example, to alter its chemical composition),

which is consistent with its customary business practices.

There are no other promised goods or services in the contract.

> > > > Case A—License Is Not Distinct

606-10-55-368 In this case, no other entity can manufacture this drug

while the customer learns the manufacturing process and builds its own manufacturing capability because of the highly specialized nature of the manufacturing process. As a result, the license cannot be purchased separately from the manufacturing

service services.

606-10-55-369 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct in accordance with paragraph 606-10-25-19. The entity determines that the customer cannot benefit from the license without the manufacturing service; therefore, the criterion in paragraph 606-10-25-19(a) is not met. Consequently, the license and the manufacturing service are not distinct, and the entity accounts for the license and the manufacturing service as a single performance obligation.

606-10-55-370 The nature of the combined good or service for which the customer contracted is a sole sourced supply of the drug for the first five years; the customer benefits from the license only as a result of having access to a supply of the drug. After the first five years, the customer retains solely the right to use the entity's functional intellectual property (see Case B, paragraph 606-10-55-373), and no further performance is required of the entity during Years 6–10. The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether the

single performance obligation (that is, the bundle of the license and the manufacturing

service services

) is a performance obligation satisfied at a point in time or over time.

Regardless of the determination reached in accordance with paragraphs 606-10-25-23 through 25-30, the entity's performance under the contract will be complete at the end of Year 5.

> > > > Case B—License Is Distinct

606-10-55-371 In this case, the manufacturing process used to produce the drug is not unique or specialized, and several other entities also can also manufacture the drug for the customer.

606-10-55-372 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct

, and it concludes that the criteria in paragraph 606-10-25-19 are met for each of the license and the manufacturing service. The entity concludes that the criterion in paragraph 606-10-25-19(a) is met because the customer can benefit from the license together with readily available resources other than the entity's manufacturing service (that is, because there are other entities that can provide the manufacturing service) and can benefit from the manufacturing service together with the license transferred to the customer at the start of the contract.

in accordance with paragraph 606-10-25-19. Because the manufacturing process can be provided by other entities, the entity concludes that the customer can benefit from the license on its own (that is, without the manufacturing service) and that the license is separately identifiable from the manufacturing process (that is, the criteria in paragraph 606-10-25-19 are met). Consequently, the entity concludes that the license and the manufacturing service are distinct and the entity has two performance obligations:

License of patent rights

Manufacturing service.

606-10-55-372A The entity also concludes that its promises to grant the license and to provide the manufacturing service are separately identifiable (that is, the criterion in paragraph 606-10-25-19(b) is met). The entity concludes that the license and the manufacturing service are not inputs to a combined item in this contract on the basis of the principle and the factors in paragraph 606-10-25-21. In reaching this conclusion, the entity considers that the customer could separately purchase the license without significantly affecting its ability to benefit from the license. Neither the license nor the manufacturing service is significantly modified or customized by the other, and the entity is not providing a significant service of integrating those items into a combined output. The entity further considers that the license and the manufacturing service are not highly interdependent or highly interrelated because the entity would be able to fulfill its promise to transfer the license independent of fulfilling its promise to subsequently manufacture the drug for the customer. Similarly, the entity would be able to manufacture the drug for the customer even if the customer had previously obtained the license and initially utilized a different manufacturer. Thus, although the manufacturing service necessarily depends on the license in this contract (that is, the entity would not contract for the manufacturing service without the customer having obtained the license), the license and the manufacturing service do not significantly affect each other. Consequently, the entity concludes that its promises to grant the license and to provide the manufacturing service are distinct and that there are two performance obligations:

- License of patent rights

- Manufacturing service.

606-10-55-373 The entity assesses,

in accordance with paragraph 606-10-55-60,

the nature of

the entity's

its promise to grant the license.

The entity concludes that the patented drug formula is functional intellectual property (that is, it has significant standalone functionality in the form of its ability to treat a disease or condition). There is no expectation that the entity will undertake activities to change the functionality of the drug formula during the license period. Because the intellectual property has significant standalone functionality, any other activities the entity might undertake (for example, promotional activities like advertising or activities to develop other drug products) would not significantly affect the utility of the licensed intellectual property. Consequently, the nature of the entity's promise in transferring the license is to provide a right to use the entity's functional intellectual property, and it accounts for the license as a performance obligation satisfied at a point in time. The entity recognizes revenue for the license performance obligation in accordance with paragraphs 606-10-55-58B through 55-58C.The drug is a mature product (that is, it has been approved, is currently being manufactured, and has been sold commercially for the last several years). For these types of mature products, the entity's customary business practices are not to undertake any activities to support the drug. Consequently, the entity concludes that the criteria in paragraph 606-10-55-60 are not met because the contract does not require, and the customer does not reasonably expect, the entity to undertake activities that significantly affect the intellectual property to which the customer has rights. In its assessment of the criteria in paragraph 606-10-55-60, the entity does not take into consideration the separate performance obligation of promising to provide a manufacturing service. Consequently, the nature of the entity's promise in transferring the license is to provide a right to use the entity's intellectual property in the form and the functionality with which it exists at the point in time that it is granted to the customer. Consequently, the entity accounts for the license as a performance obligation satisfied at a point in time

606-10-55-374 In its assessment of the nature of the license, the entity does not consider the manufacturing service because it is an additional promised service in the contract. The entity applies paragraphs 606-10-25-23 through 25-30 to determine whether the manufacturing service is a performance obligation satisfied at a point in time or over time.

> > > Example 57—Franchise Rights

606-10-55-375 An entity enters into a contract with a customer and promises to grant a franchise license that provides the customer with the right to use the entity's trade name and sell the entity's products for 10 years. In addition to the license, the entity also promises to provide the equipment necessary to operate a franchise store. In exchange for granting the license, the entity receives a

fixed fee of $1 million, as well as a sales-based royalty of 5 percent of the customers

monthly

sales

for the term of the license. The fixed consideration for the equipment is $150,000 payable when the equipment is delivered.

> > > > Identifying Performance Obligations

606-10-55-376 The entity assesses the goods and services promised to the customer to determine which goods and services are distinct in accordance with paragraph 606-10-25-19. The entity observes that the entity, as a franchisor, has developed a customary business practice to undertake activities such as analyzing the

customers