2. Amend paragraphs 350-20-35-1 through 35-3, 350-20-35-3B and 350-20-35-3D through 35-4 and the related heading, 350-20-35-6, 350-20-35-8, 350-20-35-25, 350-20-35-30, 350-20-35-57A, and 350-20-35-73, add paragraphs 350-20-35-8B and 350-20-35-39A, supersede paragraphs 350-20-35-8A through 35-11, and 350-20-35-14 through 35-21 and their related headings, with a link to transition paragraph 350-20-65-3, as follows:

Intangibles—Goodwill and Other—Goodwill

Subsequent Measurement

General

> Overall Accounting for Goodwill

350-20-35-1 Goodwill shall not be amortized. Instead, goodwill shall be tested at least annually for impairment at a level of reporting referred to as a reporting unit. (Paragraphs 350-20-35-33 through 35-46 provide guidance on determining reporting units.)

350-20-35-2 Impairment

of goodwill is the condition that exists when the carrying amount of

a reporting unit that includes goodwill exceeds its

implied

fair value.

A goodwill impairment loss is recognized for the amount that the carrying amount of a reporting unit, including goodwill, exceeds its fair value, limited to the total amount of goodwill allocated to that reporting unit. However, an entity shall consider the related income tax effect from any tax deductible goodwill, if applicable, in accordance with paragraph 350-20-35-8B when measuring the goodwill impairment loss.The fair value of goodwill can be measured only as a

residual and cannot be measured directly. Therefore, this Subtopic includes a

methodology to determine an amount that achieves a reasonable estimate of the

value of goodwill for purposes of measuring an impairment loss. That estimate is

referred to as the implied fair value of goodwill.

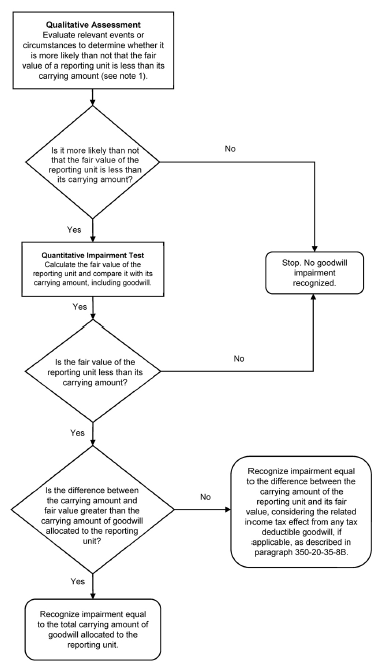

350-20-35-3 An entity may first assess qualitative factors, as described in paragraphs 350-20-35-3A through 35-3G, to determine whether it is necessary to perform the two-step

quantitative goodwill impairment test

discussed in paragraphs 350-20-35-4 through

35-13 35-19

. If determined to be necessary, the

two-step

quantitative impairment test shall be used to identify

potential

goodwill impairment and measure the amount of a goodwill impairment loss to be recognized (if any).

> Recognition and Measurement of an Impairment Loss

> > Qualitative Assessment

350-20-35-3A An entity may assess qualitative factors to determine whether it is more likely than not (that is, a likelihood of more than 50 percent) that the fair value of a reporting unit is less than its carrying amount, including goodwill.

350-20-35-3B An entity has an unconditional option to bypass the qualitative assessment described in the preceding paragraph for any reporting unit in any period and proceed directly to performing the first step of

the

quantitative goodwill impairment test. An entity may resume performing the qualitative assessment in any subsequent period.

350-20-35-3C In evaluating whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount, an entity shall assess relevant events and circumstances. Examples of such events and circumstances include the following:

a. Macroeconomic conditions such as a deterioration in general economic conditions, limitations on accessing capital, fluctuations in foreign exchange rates, or other developments in equity and credit markets

b. Industry and market considerations such as a deterioration in the environment in which an entity operates, an increased competitive environment, a decline in market-dependent multiples or metrics (consider in both absolute terms and relative to peers), a change in the market for an entity's products or services, or a regulatory or political development

c. Cost factors such as increases in raw materials, labor, or other costs that have a negative effect on earnings and cash flows

d. Overall financial performance such as negative or declining cash flows or a decline in actual or planned revenue or earnings compared with actual and projected results of relevant prior periods

e. Other relevant entity-specific events such as changes in management, key personnel, strategy, or customers; contemplation of bankruptcy; or litigation

f. Events affecting a reporting unit such as a change in the composition or carrying amount of its net assets, a more-likely-than-not expectation of selling or disposing of all, or a portion, of a reporting unit, the testing for recoverability of a significant asset group within a reporting unit, or recognition of a goodwill impairment loss in the financial statements of a subsidiary that is a component of a reporting unit

g. If applicable, a sustained decrease in share price (consider in both absolute terms and relative to peers).

350-20-35-3D If, after assessing the totality of events or circumstances such as those described in the preceding paragraph, an entity determines that it is not more likely than not that the fair value of a reporting unit is less than its carrying amount, then the quantitative first and second steps of the

goodwill impairment test is are

unnecessary.

350-20-35-3E If, after assessing the totality of events or circumstances such as those described in paragraph 350-20-35-3C(a) through (g), an entity determines that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, then the entity shall perform the quantitative first step of the twostep

goodwill impairment test.

350-20-35-3F The examples included in paragraph 350-20-35-3C(a) through (g) are not all-inclusive, and an entity shall consider other relevant events and circumstances that affect the fair value or carrying amount of a reporting unit in determining whether to perform the quantitative first step of the

goodwill impairment test. An entity shall consider the extent to which each of the adverse events and circumstances identified could affect the comparison of a reporting unit's fair value with its carrying amount. An entity should place more weight on the events and circumstances that most affect a reporting unit's fair value or the carrying amount of its net assets. An entity also should consider positive and mitigating events and circumstances that may affect its determination of whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If an entity has a recent fair value calculation for a reporting unit, it also should include as a factor in its consideration the difference between the fair value and the carrying amount in reaching its conclusion about whether to perform the quantitative first step of the

goodwill impairment test.

350-20-35-3G An entity shall evaluate, on the basis of the weight of evidence, the significance of all identified events and circumstances in the context of determining whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. None of the individual examples of events and circumstances included in paragraph 350-20-35-3C(a) through (g) are intended to represent standalone events or circumstances that necessarily require an entity to perform the quantitative first step of the

goodwill impairment test. Also, the existence of positive and mitigating events and circumstances is not intended to represent a rebuttable presumption that an entity should not perform the quantitative first step

of the

goodwill impairment test.

3. Amend paragraph 350-20-35-8A, with a link to transition paragraph 350-20- 65-1, as follows:

> > Quantitative Impairment Test Step 1

350-20-35-4 The

quantitative first step of the

goodwill impairment test, used to identify

both the existence of potential

impairment

and the amount of impairment loss, compares the fair value of a reporting unit with its carrying amount, including goodwill.

350-20-35-5 The guidance in paragraphs 350-20-35-22 through 35-24 shall be considered in determining the fair value of a reporting unit.

350-20-35-6 If the

fair value carrying amount of a reporting unit is greater than zero and its fair value exceeds its carrying amount, goodwill of the reporting unit is considered not impaired impaired; thus, the second step of the impairment test is unnecessary. If the carrying amount of the reporting unit is zero or negative, the guidance in paragraph 350-20-35-8A shall be followed .

350-20-35-7 In determining the carrying amount of a reporting unit, deferred income taxes shall be included in the carrying amount of the reporting unit, regardless of whether the fair value of the reporting unit will be determined assuming it would be bought or sold in a taxable or nontaxable transaction.

350-20-35-8 If the carrying amount of a reporting unit exceeds its fair value, an impairment loss shall be recognized in an amount equal to that excess, limited to the total amount of goodwill allocated to that reporting unit. Additionally, an entity shall consider the income tax effect from any tax deductible goodwill on the carrying amount of the reporting unit, if applicable, in accordance with paragraph 350-20-35-8B when measuring the goodwill impairment loss.

the second step of the goodwill impairment test shall be performed to measure the amount of impairment loss, if any.

350-20-35-8A Paragraph superseded by Accounting Standards Update No. 2017-04.If the carrying amount of a reporting unit is zero or negative, the second step of the impairment test shall be performed to measure the amount of impairment loss, if any, when it is more likely than not

(that is, a likelihood of more than 50 percent)

that a goodwill impairment exists.

In considering whether it is more likely than not that a goodwill impairment exists, an entity shall evaluate,

using the process described in paragraphs 350-20-35-3F through 35-3G, whether there are adverse qualitative factors, including the examples

of events and circumstances provided in paragraph 350-20-35-30(a) through (g). In evaluating whether it is more likely than not that the goodwill of a reporting unit with a zero or negative carrying amount is impaired, an entity also should take into consideration whether there are significant differences between the carrying amount and the estimated fair value of its assets and liabilities, and the existence of significant unrecognized intangible assets

> > Step 2

350-20-35-8B If a reporting unit has tax deductible goodwill, recognizing a goodwill impairment loss may cause a change in deferred taxes that results in the carrying amount of the reporting unit immediately exceeding its fair value upon recognition of the loss. In those circumstances, the entity shall calculate the impairment loss and associated deferred tax effect in a manner similar to that used in a business combination in accordance with the guidance in paragraphs 805-740-55-9 through 55-13. The total loss recognized shall not exceed the total amount of goodwill allocated to the reporting unit. See Example 2A in paragraphs 350-20-55-23A through 55-23C for an illustration of the calculation.

350-20-35-9 Paragraph superseded by Accounting Standards Update No. 2017-04.The second step of the goodwill impairment test, used to measure the amount

of impairment loss, compares the implied fair value of reporting unit goodwill with

the carrying amount of that goodwill.

350-20-35-10 Paragraph superseded by Accounting Standards Update No. 2017-04.The guidance in paragraphs 350-20-35-14 through 35-17 shall be used to

estimate the implied fair value of goodwill.

350-20-35-11 Paragraph superseded by Accounting Standards Update No. 2017-04.If the carrying amount of reporting unit goodwill exceeds the implied fair value

of that goodwill, an impairment loss shall be recognized in an amount equal to that

excess. The loss recognized cannot exceed the carrying amount of goodwill.

350-20-35-12 After a goodwill impairment loss is recognized, the adjusted carrying amount of goodwill shall be its new accounting basis.

350-20-35-13 Subsequent reversal of a previously recognized goodwill impairment loss is prohibited once the measurement of that loss is recognized.

> > Determining the Implied Fair Value of Goodwill

350-20-35-14 Paragraph superseded by Accounting Standards Update No. 2017-04.The implied fair value of goodwill shall be determined in the same manner as

the amount of goodwill recognized in a business combination or an acquisition

by a not-for-profit entity

was determined. That is, an entity shall assign the fair

value of a reporting unit to all of the assets and liabilities of that unit (including any

unrecognized intangible assets) as if the reporting unit had been acquired in a

business combination or an acquisition by a not-for-profit entity. Throughout this

Section, the term business combination includes an acquisition by a not-for-profit

entity

.

350-20-35-15 Paragraph superseded by Accounting Standards Update No. 2017-04.The relevant guidance in Subtopic 805-20 shall be used in determining how to

assign the fair value of a reporting unit to the assets and liabilities of that unit.

Included in that allocation would be research and development assets that meet

the criteria in paragraph 350-20-35-39.

350-20-35-16 Paragraph superseded by Accounting Standards Update No. 2017-04.The excess of the fair value of a reporting unit over the amounts assigned to its

assets and liabilities is the implied fair value of goodwill.

350-20-35-17 Paragraph superseded by Accounting Standards Update No. 2017-04.That assignment process discussed in paragraphs 350-20-35-14 through 3516 shall be performed only for purposes of testing goodwill for impairment; an entity

shall not write up or write down a recognized asset or liability, nor shall it recognize

a previously unrecognized intangible asset as a result of that allocation process.

350-20-35-18 Paragraph superseded by Accounting Standards Update No. 2017-04.If the second step of the goodwill impairment test is not complete before the

financial statements are issued or are available to be issued (as discussed in

Section 855-10-25) and a goodwill impairment loss is probable and can be

reasonably estimated, the best estimate of that loss shall be recognized in those

financial statements (see Subtopic 450-10).

350-20-35-19 Paragraph superseded by Accounting Standards Update No. 2017-04.Paragraph 350-20-50-2(c) requires disclosure of the fact that the measurement

of the impairment loss is an estimate. Any adjustment to that estimated loss based

on the completion of the measurement of the impairment loss shall be recognized

in the subsequent reporting period.

> > > Deferred Income Tax Considerations

350-20-35-20 Paragraph superseded by Accounting Standards Update No. 2017-04.For purposes of determining the implied fair value of goodwill, an entity shall

use the income tax bases of a reporting unit's assets and liabilities implicit in the

tax structure assumed in its estimation of fair value of the reporting unit in Step 1.

That is, an entity shall use its existing income tax bases if the assumed structure

used to estimate the fair value of the reporting unit was a nontaxable transaction,

and it shall use new income tax bases if the assumed structure was a taxable

transaction.

350-20-35-21 Paragraph superseded by Accounting Standards Update No. 2017-04.Paragraph 805-740-25-6 indicates that a deferred tax liability or asset shall be

recognized for differences between the assigned values and the income tax bases

of the recognized assets acquired and liabilities assumed in a business

combination in accordance with paragraph 805-740-25-3. To the extent present,

tax attributes that will be transferred in the assumed tax structure, such as

operating loss or tax credit carry forwards, shall be valued consistent with the

guidance contained in paragraph 805-740-30-3.

> Determining the Fair Value of a Reporting Unit

> > Deferred Income Tax Considerations

350-20-35-25 Before estimating the fair value of a reporting unit, an entity shall determine whether that estimation should be based on an assumption that the reporting unit could be bought or sold in a nontaxable transaction or a taxable transaction. Making that determination is a matter of judgment that depends on the relevant facts and circumstances and must be evaluated carefully on a case-bycase basis (see

Examples

Example 1

through 2

[paragraphs 350-20-55-10 through 55-23]).

350-20-35-26 In making that determination, an entity shall consider all of the following:

a. Whether the assumption is consistent with those that marketplace participants would incorporate into their estimates of fair value

b. The feasibility of the assumed structure

c. Whether the assumed structure results in the highest and best use and would provide maximum value to the seller for the reporting unit, including consideration of related tax implications.

350-20-35-27 In determining the feasibility of a nontaxable transaction, an entity shall consider, among other factors, both of the following:

a. Whether the reporting unit could be sold in a nontaxable transaction

b. Whether there are any income tax laws and regulations or other corporate governance requirements that could limit an entity's ability to treat a sale of the unit as a nontaxable transaction.

> When to Test Goodwill for Impairment

350-20-35-28 Goodwill of a reporting unit shall be tested for impairment on an annual basis and between annual tests in certain circumstances (see paragraph 350-20-35-30). The annual goodwill impairment test may be performed any time during the fiscal year provided the test is performed at the same time every year. Different reporting units may be tested for impairment at different times.

350-20-35-29 Paragraph superseded by Accounting Standards Update No. 2011-08.

350-20-35-30 Goodwill of a reporting unit shall be tested for impairment between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying amount.

Additionally, if the carrying amount of a reporting unit is zero or negative, goodwill of that reporting unit shall be tested for impairment on an annual or interim basis if an event occurs or circumstances exist that indicate that it is more likely than not that a goodwill impairment exists.

Paragraph 350-20-35-3C(a) through (g) includes examples of such events and circumstances

, and paragraph 350-20-35-8A includes additional factors to consider when the carrying amount of a reporting unit is zero or negative.

Paragraphs 350-20-35-3F through 35-3G describe the process for making these evaluations.

a. Subparagraph superseded by Accounting Standards Update No. 2011-08

b. Subparagraph superseded by Accounting Standards Update No. 2011-08

c. Subparagraph superseded by Accounting Standards Update No. 2011-08

d. Subparagraph superseded by Accounting Standards Update No. 2011-08

e. Subparagraph superseded by Accounting Standards Update No. 2011-08

f. Subparagraph superseded by Accounting Standards Update No. 2011-08

g. Subparagraph superseded by Accounting Standards Update No. 201108

350-20-35-31 If goodwill and another asset (or asset group) of a reporting unit are tested for impairment at the same time, the other asset (or asset group) shall be tested for impairment before goodwill. For example, if a significant asset group is to be tested for impairment under the Impairment or Disposal of Long-Lived Assets Subsections of Subtopic 360-10 (thus potentially requiring a goodwill impairment test), the impairment test for the significant asset group would be performed before the goodwill impairment test. If the asset group was impaired, the impairment loss would be recognized prior to goodwill being tested for impairment.

350-20-35-32 This requirement applies to all assets that are tested for impairment, not just those included in the scope of the Impairment or Disposal of Long-Lived Assets Subsections of Subtopic 360-10.

> Assigning Acquired Assets and Assumed Liabilities to a ReportingUnit

350-20-35-39 For the purpose of testing goodwill for impairment, acquired assets and assumed liabilities shall be assigned to a reporting unit as of the acquisition date if both of the following criteria are met:

a. The asset will be employed in or the liability relates to the operations of a reporting unit.

b. The asset or liability will be considered in determining the fair value of the reporting unit.

Assets or liabilities that an entity considers part of its corporate assets or liabilities shall also be assigned to a reporting unit if both of the preceding criteria are met. Examples of corporate items that may meet those criteria and therefore would be assigned to a reporting unit are environmental liabilities that relate to an existing operating facility of the reporting unit and a pension obligation that would be included in the determination of the fair value of the reporting unit. This provision applies to assets acquired and liabilities assumed in a business combination and to those acquired or assumed individually or with a group of other assets.

350-20-35-39A Foreign currency translation adjustments should not be allocated to a reporting unit from an entity's accumulated other comprehensive income. The reporting unit's carrying amount should include only the currently translated balances of the assets and liabilities assigned to the reporting unit.

350-20-35-40 Some assets or liabilities may be employed in or relate to the operations of multiple reporting units. The methodology used to determine the amount of those assets or liabilities to assign to a reporting unit shall be reasonable and supportable and shall be applied in a consistent manner. For example, assets and liabilities not directly related to a specific reporting unit, but from which the reporting unit benefits, could be assigned according to the benefit received by the different reporting units (or based on the relative fair values of the different reporting units). In the case of pension items, for example, a pro rata assignment based on payroll expense might be used. A reasonable allocation method may be very general. For use in making those assignments, the basis for and method of determining the fair value of the acquiree and other related factors (such as the underlying reasons for the acquisition and management's expectations related to dilution, synergies, and other financial measurements) shall be documented at the acquisition date.

> Reorganization of Reporting Structure

> > Disposal of All or a Portion of a Reporting Unit

> > > Goodwill Impairment Testing and Disposal of All or a Portion of a Reporting Unit When the Reporting Unit Is Less Than Wholly Owned

350-20-35-57A If a reporting unit is less than wholly owned, the fair value of the reporting unit

as a whole and the implied fair value of goodwill

shall be determined in

accordance with paragraphs 350-20-35-22 through 35-24, including any portion attributed to the noncontrolling interest the same manner as it would be determined

in a business combination accounted for in accordance with Topic 805 or an

acquisition accounted for in accordance with Subtopic 958-805

. Any impairment loss measured in

the second step of

the goodwill impairment test shall be attributed to the parent and the

noncontrolling interest on a rational basis. If the reporting unit includes only goodwill attributable to the parent, the goodwill impairment loss would be attributed entirely to the parent. However, if the reporting unit includes goodwill attributable to both the parent and the noncontrolling interest, the goodwill impairment loss shall be attributed to both the parent and the noncontrolling interest.

Accounting Alternative

> Recognition and Measurement of a Goodwill Impairment Loss

> > The Goodwill Impairment Test

350-20-35-73 A goodwill impairment loss, if any, shall be measured as the amount by which the carrying amount of an entity (or a reporting unit) including goodwill exceeds its fair value

, limited to the total amount of goodwill of the entity (or allocated to the reporting unit). Additionally, an entity shall consider the income tax effect from any tax deductible goodwill on the carrying amount of the entity (or the reporting unit), if applicable, in accordance with paragraph 350-20-35-8B when measuring the goodwill impairment loss. See Example 2A in paragraph 350-20-55-23A for an illustration.

A goodwill impairment loss shall not exceed the entity's

(or the reporting unit's) carrying amount of goodwill.

3. Amend paragraph 350-20-40-7, with a link to transition paragraph 350-20-65-3, as follows:

Derecognition

> Disposal of All or a Portion of a Reporting Unit

350-20-40-7 When only a portion of goodwill is allocated to a business to be disposed of, the goodwill remaining in the portion of the reporting unit to be retained shall be tested for impairment in accordance with paragraphs 350-20-35-3A through

35-13 35-19

using its adjusted carrying amount.

4. Add paragraph 350-20-50-1A and amend paragraph 350-20-50-2, with a link to transition paragraph 350-20-65-3, as follows:

Disclosure

> Information for Each Period for Which a Statement of Financial Position Is Presented

350-20-50-1 The changes in the carrying amount of goodwill during the period shall be disclosed, showing separately (see Example 3 [paragraph 350-20-55-24]):

a. The gross amount and accumulated impairment losses at the beginning of the period

b. Additional goodwill recognized during the period, except goodwill included in a disposal group that, on acquisition, meets the criteria to be classified as held for sale in accordance with paragraph 360-10-45-9

c. Adjustments resulting from the subsequent recognition of deferred tax assets during the period in accordance with paragraphs 805-740-25-2 through 25-4 and 805-740-45-2

d. Goodwill included in a disposal group classified as held for sale in accordance with paragraph 360-10-45-9 and goodwill derecognized during the period without having previously been reported in a disposal group classified as held for sale

e. Impairment losses recognized during the period in accordance with this Subtopic

f. Net exchange differences arising during the period in accordance with Topic 830

g. Any other changes in the carrying amounts during the period

h. The gross amount and accumulated impairment losses at the end of the period.

Entities that report segment information in accordance with Topic 280 shall provide the above information about goodwill in total and for each reportable segment and shall disclose any significant changes in the allocation of goodwill by reportable segment. If any portion of goodwill has not yet been allocated to a reporting unit at the date the financial statements are issued, that unallocated amount and the reasons for not allocating that amount shall be disclosed.

350-20-50-1A Entities that have one or more reporting units with zero or negative carrying amounts of net assets shall disclose those reporting units with allocated goodwill and the amount of goodwill allocated to each and in which reportable segment the reporting unit is included.

> Goodwill Impairment Loss

350-20-50-2 For each goodwill impairment loss recognized, all of the following information shall be disclosed in the notes to the financial statements that include the period in which the impairment loss is recognized:

a. A description of the facts and circumstances leading to the impairment

b. The amount of the impairment loss and the method of determining the fair value of the associated reporting unit (whether based on quoted market prices, prices of comparable businesses or nonprofit activities, a present value or other valuation technique, or a combination thereof)

c.

Subparagraph superseded by Accounting Standards Update No. 2017-04.If a recognized impairment loss is an estimate that has not yet been

finalized (see paragraphs 350-20-35-18 through 35-19), that fact and the

reasons therefore and, in subsequent periods, the nature and amount of

any significant adjustments made to the initial estimate of the impairment

loss.

5. Amend paragraphs 350-20-55-12 through 55-16, the heading preceding paragraph 350-20-55-17, and 350-20-55-19 through 55-26 and add the heading preceding paragraph 350-20-55-10 and paragraphs 350-20-55-23A through 55-23D and their related heading, with a link to transition paragraph 350-20-65-3, as follows:

Implementation Guidance and Illustrations

General

> Illustrations

> > Example 1: Impairment Test When either a Taxable or Nontaxable Transaction Is Feasible

> > > Case A—Effect of a Nontaxable Transaction on the Impairment Test of Goodwill

350-20-55-10 This Example illustrates the effect of a nontaxable transaction on the impairment test of goodwill. The Example may not necessarily be indicative of actual income tax liabilities that would arise in the sale of a reporting unit or the relationship of those liabilities in a taxable versus nontaxable structure.

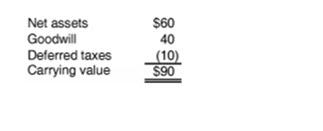

350-20-55-11 Entity A is performing a goodwill impairment test relative to Reporting Unit at December 31, 20X2. Reporting Unit has the following assets and liabilities:

a. Net assets (excluding goodwill and deferred income taxes) of $60 with a tax basis of $35

b. Goodwill of $40

c. Net deferred tax liabilities of $10.

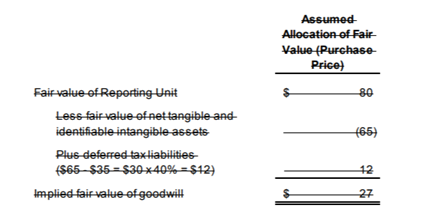

350-20-55-12 Entity A believes that it is feasible to sell Reporting Unit in either a nontaxable or a taxable transaction. Entity A could sell Reporting Unit for $80 in a nontaxable transaction or $90 in a taxable transaction. If Reporting Unit were sold in a nontaxable transaction, Entity A would have a current tax payable resulting from the sale of $10. Assuming a tax rate of 40 percent, if Reporting Unit were sold in a taxable transaction, Entity A would have a current tax payable resulting from the sale of $22 ([$90 - 35] × 40%).

The fair value of the net tangible and identifiable

intangible assets

in Reporting Unit is $65, before consideration of deferred

income taxes.

350-20-55-13 In

Step 1 of

the

quantitative impairment test in paragraphs 350-20-35-4 through 35-8, Entity A concludes that market participants would act in their economic best interest by selling Reporting Unit in a nontaxable transaction based on the following evaluation of its expected after-tax proceeds.

350-20-55-14 In

Step 1 of

the

quantitative impairment test, Entity A would determine the carrying

amount value

of Reporting Unit as follows.

350-20-55-15 The goodwill allocated to

Reporting Unit

fails Step 1 of the goodwill

impairment test as its

is determined to be impaired because Reporting Unit's carrying value ($90) exceeds its fair value ($80 assuming a nontaxable transaction).

Entity A must perform Step 2 of the goodwill impairment test in

paragraphs 350-20-35-9 through 35-13. Because Entity A assumed that Reporting

Unit would be sold in a nontaxable transaction, the analysis in Step 2 is as follows.

350-20-55-16 Reporting Unit must recognize

a

the full goodwill impairment

loss of

$10 $13

(determined as the

excess of the carrying

amount value

of

Reporting Unit goodwill

of

$90 $40

compared

with to

its

implied

fair value of

$27)

$80) because the $10 impairment loss does not exceed the $40 carrying amount of the goodwill allocated to Reporting Unit.

> > Example 2: Impairment Test When Either a Taxable or Nontaxable

Transaction Is Feasible

> > > Case B—Effect of a Taxable Transaction on the Impairment Test of Goodwill

350-20-55-17 This Example illustrates the effect of a taxable transaction on the impairment test of goodwill. The Example may not necessarily be indicative of actual income tax liabilities that would arise in the sale of a reporting unit or the relationship of those liabilities in a taxable versus nontaxable structure.

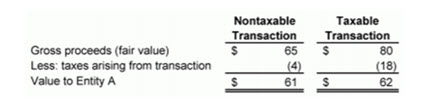

350-20-55-18 Entity A is performing a goodwill impairment test relative to Reporting Unit at December 31, 20X2. Reporting Unit has the following assets and liabilities:

a. Net assets (excluding goodwill and deferred income taxes) of $60 with a tax basis of $35

b. Goodwill of $40

c. Net deferred tax liabilities of $10.

350-20-55-19 Entity A believes that it is feasible to sell Reporting Unit in either a nontaxable or a taxable transaction. Entity A could sell Reporting Unit for $65 in a nontaxable transaction or $80 in a taxable transaction. If Reporting Unit were sold in a nontaxable transaction, Entity A would have a current tax payable resulting from the sale of $4. Assuming a tax rate of 40 percent, if Reporting Unit were sold in a taxable transaction, Entity A would have a current tax payable resulting from the sale of $18 ([$80 - 35] × 40%).

The fair value of the net tangible and identifiable intangible assets in Reporting Unit is $65, before consideration of deferred income taxes.

350-20-55-20 In

Step 1 of

the

quantitative impairment test in paragraphs 350-2035-4 through 35-8, Entity A concludes that market participants would act in their economic best interest by selling Reporting Unit in a taxable transaction. This conclusion was based on the following.

350-20-55-21 Deferred taxes related to the net assets of Reporting Unit should be included in the carrying value of Reporting Unit. Accordingly, in

Step 1 of

the

quantitative impairment test Entity A would determine the carrying

amount value

of Reporting Unit as follows.

350-20-55-22 The goodwill allocated to Reporting Unit

is determined to be impaired fails Step 1

because

its

Reporting Unit's carrying

amount value

($90) exceeds its fair value

($80). ($80); therefore, Entity A must perform Step 2 of the

goodwill impairment test (see paragraphs 350-20-35-9 through 35-13). Because

Entity A assumed that Reporting Unit would be sold in a taxable transaction, the

calculation of the implied fair value of goodwill in Step 2 of the impairment analysis

is as follows.

350-20-55-23 Reporting Unit must recognize

a

the full goodwill impairment

loss of

$10 $25

(determined as the

excess of the carrying

amount value

of

Reporting Unit goodwill

of

$90 $40

compared

with to

its

implied

fair value of

$15)

$80) because the $10 impairment loss does not exceed the $40 carrying amount of the goodwill allocated to Reporting Unit.

> > Example 2A: Impairment Test When Goodwill Is Tax Deductible

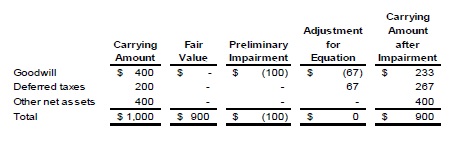

350-20-55-23A Goodwill is deductible for tax purposes for some business combinations in certain jurisdictions. In those jurisdictions, a deferred tax asset or deferred tax liability is recorded upon acquisition on the basis of the difference between the book basis and the tax basis of goodwill. When goodwill of a reporting unit is tax deductible, the impairment of goodwill creates a cycle of impairment because the decrease in the book value of goodwill increases the deferred tax asset (or decreases the deferred tax liability) such that the carrying amount of the reporting unit increases. However, there is no corresponding increase in the fair value of the reporting unit and this could trigger another impairment test.

350-20-55-23B This Example illustrates the use of a simultaneous equation when tax deductible goodwill is present to account for the increase in the carrying amount from the deferred tax benefit.

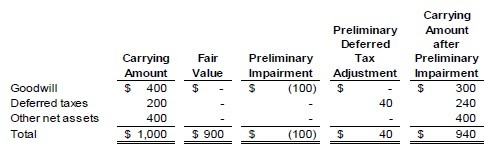

Beta Entity has goodwill from an acquisition in Reporting Unit X. All of the goodwill allocated to Reporting Unit X is tax deductible. On October 1, 20X6 (the date of the annual impairment test for the reporting unit), Reporting Unit X had a book value of goodwill of $400, which is all tax deductible, deferred tax assets of $200 relating to the tax-deductible goodwill, and book value of other net assets of $400. Reporting Unit X is subject to a 40 percent income tax rate. Beta Entity estimated the fair value of Reporting Unit X at $900.

[For ease of readability, the new table is not underlined.]

350-20-55-23C In the Example above, the carrying amount of Reporting Unit X immediately after the impairment charge exceeds its fair value by the amount of the increase in the deferred tax asset calculated as 40 percent of the impairment charge. To address the circular nature of the carrying amount exceeding the fair value, instead of continuing to calculate impairment on the excess of carrying amount over fair value until those amounts are equal, Beta Entity would apply the simultaneous equation demonstrated in paragraphs 805-740-55-9 through 55-13 to Reporting Unit X, as follows.

[For ease of readability, the new table is not underlined.]

Simultaneous equation: [tax rate/(1 – tax rate)] × (preliminary temporary difference) = deferred tax asset

Equation for this example: 40%/(1 – 40%) × 100 = 67

350-20-55-23D The company would report a $167 goodwill impairment charge partially offset by a $67 deferred tax benefit recognized in the income tax line. If the impairment charge calculated using the equation exceeds the total goodwill allocated to a reporting unit, the total impairment charge would be limited to the goodwill amount.

> > Example 3: Illustration of Disclosures

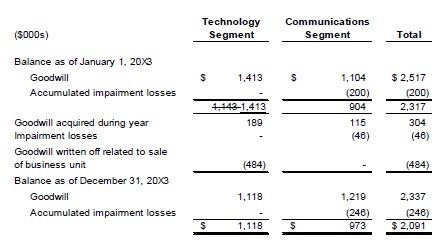

350-20-55-24 In accordance with paragraphs 350-20-50-1 through 50-2, the following disclosures would be made by Theta Entity in its December 31, 20X3 financial statements relating to goodwill.

Theta Entity has

two

three reporting units with goodwill—

Technology

Software, Electronics, and Communications—

which also are

and two reportable segments

—Technology and Communications. The Electronics reporting unit has a negative carrying amount.

Note C: Goodwill

The changes in the carrying amount of goodwill for the year ended December 31, 20X3, are as follows.

The Communications segment is tested for impairment in the third quarter, after the annual forecasting process. Due to an increase in competition in the Texas and Louisiana cable industry, operating profits and cash flows were lower than expected in the fourth quarter of 20X2 and the first and second quarters of 20X3. Based on that trend, the earnings forecast for the next five years was revised. In September 20X3, a goodwill impairment loss of $46 was recognized in the Communications reporting unit. The fair value of that reporting unit was estimated using the expected present value of future cash flows.

The Electronics reporting unit to which $498 of goodwill is allocated had a negative carrying amount on December 31, 20X3, and 20X2. This reporting unit is part of the Technology segment.

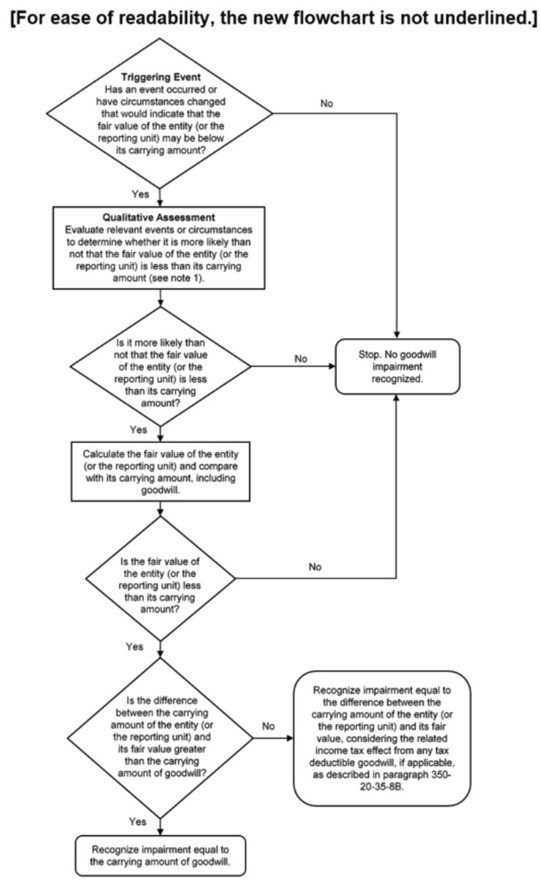

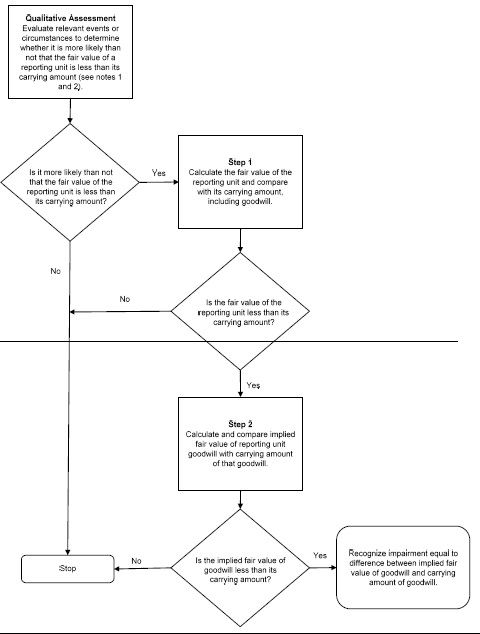

> > Example 4: Goodwill Impairment Test

350-20-55-25 The flowchart in this Example illustrates the optional qualitative assessment and the

quantitative two-step

goodwill impairment test described in paragraphs 350-20-35-3A through

35-13 35-19

.

[For ease of readability, the new flowchart is not underlined.]

1. An entity has the unconditional option to skip the qualitative assessment and proceed directly to

calculating the fair value of the reporting unit and comparing that value with its carrying amount, including goodwill performing Step 1, except in the circumstance where a reporting unit has a carrying amount that is zero or negative

.

2. An entity having a reporting unit with a carrying amount that is zero or negative would proceed directly to Step 2 if it determines, as a result of performing its required qualitative assessment, that it is more likely than not that a goodwill impairment exists. To perform Step 2, an entity must calculate the fair value of a reporting unit.

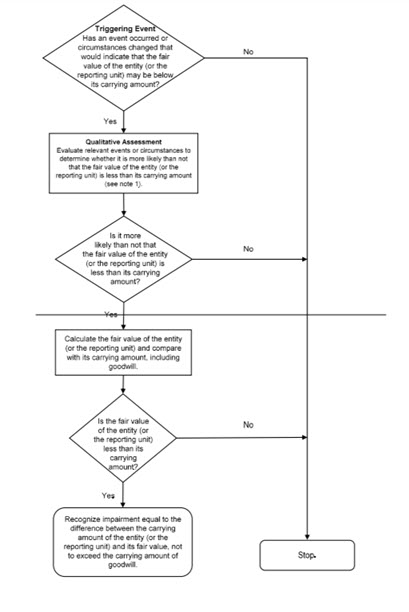

Accounting Alternative

> Implementation Guidance

350-20-55-26 The following flowchart provides an overview of the accounting alternative for entities within the scope of paragraph 350-20-15-4.

Note 1: An entity has the unconditional option to skip the qualitative assessment and proceed directly to calculating the fair value of the entity (or the reporting unit) and comparing that value with its carrying amount, including goodwill.

6. Add paragraph 350-20-65-3 and its related heading, as follows:

> Transition Related to Accounting Standards Update No. 2017-04, Intangibles—Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment

350-20-65-3 The following represents the transition and effective date information related to Accounting Standards Update No. 2017-04, Intangibles—Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment:

a. The pending content that links to this paragraph shall be effective for annual and any interim impairment tests performed for periods beginning after:

1. December 15, 2019, for public business entities that are U.S. Securities and Exchange Commission (SEC) filers

2. December 15, 2020, for public business entities that are not SEC filers

3. December 15, 2021, for all other entities, including not-for-profit entities.

b. Early adoption is permitted for interim and annual goodwill impairment tests with a measurement date after January 1, 2017.

c. An entity shall apply the pending content that links to this paragraph prospectively.

d. An entity shall disclose the nature of and reason for the change in accounting principle, including an explanation of why the newly adopted accounting principle is preferable, in the fiscal period in which the change in accounting principle is made. An entity that issues interim financial statements shall provide the required disclosures in the financial statements of both the interim period of the change and the annual period of the change.

e. Private companies that have adopted the private company accounting alternative for the subsequent measurement of goodwill but have not adopted the private company alternative for subsuming certain intangible assets into goodwill are allowed, but not required, to adopt this guidance prospectively on or before the effective date without having to justify preferability of the accounting change. Private companies that have adopted the private company alternative to subsume certain intangible assets into goodwill and, thus, also adopted the goodwill alternative are not permitted to adopt this guidance upon issuance without following the guidance in Topic 250 on accounting changes and error corrections, including justifying why it is preferable to change their accounting policies