4. Amend paragraph 610-20-05-1 and add paragraph 610-20-05-2, with a link to transition paragraph 606-10-65-1, as follows:

Other Income—Gains and Losses from the Derecognition of Nonfinancial Assets

Overview and Background

610-20-05-1 This Subtopic provides guidance on the recognition of gains and losses on transfers of nonfinancial assets and in substance nonfinancial assets to counterparties that are not customers. Although the guidance in this Subtopic applies to contracts with noncustomers, it refers to revenue recognition principles in Topic 606 on revenue from contracts with customersa gain or loss recognized upon the derecognition of a nonfinancial asset within the scope of Topic 350 on intangibles and Topic 360 on property, plant, and equipment (including in substance nonfinancial assets) if those assets are not in a contract with a customer within the scope of Topic 606 on revenue from contracts with customers.

610-20-05-2 The term transfer in this Subtopic is used broadly and includes sales and situations in which a parent transfers ownership interests (or variable interests) in a consolidated subsidiary or other changes in facts and circumstances that result in the derecognition of nonfinancial assets or in substance nonfinancial assets that do not constitute a business. For example, an entity may lose control of nonfinancial assets or in substance nonfinancial assets because of the expiration or termination of an existing contractual arrangement, a dilution event, a government action, or upon default of a subsidiary's nonrecourse debt. An entity also may lose control of nonfinancial assets or in substance nonfinancial assets by contributing those assets to a joint venture or other noncontrolled investee.

5. Amend paragraphs 610-20-15-2 through 15-3 and supersede the heading preceding paragraph 610-20-15-3 and add paragraphs 610-20-15-4 through 15-10 and their related headings, with a link to transition paragraph 606-10-65-1, as follows:

Scope and Scope Exceptions

> Entities

610-20-15-1 The guidance in this Subtopic applies to all entities.

> Transactions

610-20-15-2 Except as described in paragraph 610-20-15-4, the guidance in this Subtopic applies to gains or losses recognized upon the derecognition of nonfinancial assets and in substance nonfinancial assets. Nonfinancial assets within the scope of this Subtopic include intangible assets, land, buildings, or materials and supplies and may have a zero carrying value. In substance nonfinancial assets are described in paragraphs 610-20-15-5 through 15-8.The guidance in this Subtopic applies to the following events and transactions:

a.

Subparagraph superseded by Accounting Standards Update No. 2017-05.The gain or loss recognized upon the derecognition of a nonfinancial asset within the scope of Topic 350 on intangibles or Topic 360 on property, plant, and equipment, unless the entity sells or transfers the nonfinancial asset in a contract with a customer

b.

Subparagraph superseded by Accounting Standards Update No. 2017-05.The gain or loss recognized upon the transfer of financial assets that are in substance nonfinancial assets within the scope of Topic 350 or Topic 360 (for example, the sale of a subsidiary that only consists of an asset [for example, a machine or piece of equipment]).

610-20-15-3 The guidance in this Subtopic applies to a transfer of an ownership interest (or a variable interest) in a consolidated subsidiary (that is not a business or nonprofit activity) only if all of the assets in the subsidiary are nonfinancial assets and/or in substance nonfinancial assets.The guidance in this Subtopic does not apply to the following:

a.

Subparagraph superseded by Accounting Standards Update No. 2017-05.The derecognition of a nonfinancial asset, including an in substance nonfinancial asset, in a contract with a customer, see Topic 606 on revenue from contracts with customers

b.

Subparagraph superseded by Accounting Standards Update No. 2017-05.The derecognition of a subsidiary or group of assets that constitutes a business or nonprofit activity (excluding an in substance nonfinancial asset), see Section 810-10-40 on consolidation

c.

Subparagraph superseded by Accounting Standards Update No. 2017-05.Real estate sale-leaseback transactions, see Subtopics 360-20 and 840-40 on leases

d.

Subparagraph superseded by Accounting Standards Update No. 2017-05.A conveyance of oil and gas mineral rights, see Subtopic 932-360 on extractive activities

e.

Subparagraph superseded by Accounting Standards Update No. 2017-05.A transfer of a nonfinancial asset to another entity in exchange for a noncontrolling ownership interest in that entity, see the guidance on exchanges of a nonfinancial asset for a noncontrolling ownership interest in Section 845-10-30.

[Content amended and moved to paragraph 610-20-15-4] In addition, delete the following pending content for paragraph 610-20-15-3, with no additional link to transition:

Transition Date:

(P) December 16, 2018; (N) December 16, 2019

| Transition

Guidance:

842-10-65-1

610-20-15-3

The guidance in this Subtopic does not apply to the following:

a.

The derecognition of a nonfinancial asset, including an in substance nonfinancial asset, in a contract with a customer, see Topic 606 on revenue from contracts with customers

b.

The derecognition of a subsidiary or group of assets that constitutes a business or nonprofit activity (excluding an in substance nonfinancial asset), see Section 810-10-40 on consolidation

c.

Sale and leaseback transactions, see Subtopic 842-40 on leases

d.

A conveyance of oil and gas mineral rights, see Subtopic 932-360 on extractive activities

e.

A transfer of a nonfinancial asset to another entity in exchange for a noncontrolling ownership interest in that entity, see the guidance on exchanges of a nonfinancial asset for a noncontrolling ownership interest in Section 845-10-30.

610-20-15-4 The guidance in this Subtopic does not apply to the following:

a.

A transfer of a nonfinancial asset or an in substance nonfinancial asset The derecognition of a nonfinancial asset, including an in substance nonfinancial asset,

in a

contract with a

customer, see Topic 606 on

revenue from contracts with customers

b.

The derecognition

A transfer of a subsidiary or group of assets that constitutes a

business or

nonprofit activity (excluding an in substance nonfinancial asset

), see Section 810-10-40 on consolidation

c.

A real estate sale-leaseback transaction or a non-real-estate saleleaseback transaction within the scope of Subtopic 360-20 on property, plant, and equipment—real estate sales or within the scope of Subtopic 840-40 on leases—sale-leaseback transactionsReal estate saleleaseback transactions, see Subtopics 360-20 and 840-40 on leases

d. A conveyance of oil and gas mineral rights

, see

within the scope of Subtopic 932-360 on extractive activities

—oil and gas e.

A transaction that is entirely accounted for in accordance with Topic 860 on transfers and servicing (for example, a transfer of investments accounted for under Topic 320 on investments—debt and equity securities, Topic 323 on investments—equity method and joint ventures, Topic 325 on investments—other, Topic 815 on derivatives and hedging, and Topic 825 on financial instruments) A transfer of a nonfinancial asset to another entity in exchange for a noncontrolling ownership interest in that entity, see the guidance on exchanges of a nonfinancial asset for a noncontrolling ownership interest in Section 845-10-30.

[Content amended as shown and moved from paragraph 610-20-15-3]f. A transfer of nonfinancial assets that is part of the consideration in a business combination within the scope of Topic 805 on business combinations, see paragraph 805-30-30-8

g. A nonmonetary transaction within the scope of Topic 845 on nonmonetary transactions

h. A lease contract within the scope of Topic 840 on leases

i. An exchange of takeoff and landing slots within the scope of Subtopic 908-350 on airlines—intangibles

j. A contribution of cash and other assets, including a promise to give, within the scope of Subtopic 720-25 on other expenses—contributions made or within the scope of Subtopic 958-605 on not-for-profit entities— revenue recognition

k. A transfer of an investment in a venture that is accounted for by proportionately consolidating the assets, liabilities, revenues, and expenses of the venture as described in paragraph 810-10-45-14

l. A transfer of nonfinancial assets or in substance nonfinancial assets solely between entities or persons under common control, such as between a parent and its subsidiaries or between two subsidiaries of the same parent.

In addition, add the following pending content for paragraph 610-20-15-4, with a link to transition paragraph 825-10-65-2:

Pending Content:

Transition Date: (P) December 16, 2017; (N) December 16, 2018 | Transition Guidance: 825-10-65-2

610-20-15-4 The guidance in this Subtopic does not apply to the following:

a.

A transfer of a nonfinancial asset or an in substance nonfinancial asset The derecognition of a nonfinancial asset, including an in substance nonfinancial asset,

in a

contract with a

customer, see Topic 606 on

revenue from contracts with customers

b.

The derecognition

A transfer of a subsidiary or group of assets that constitutes a

business or

nonprofit activity (excluding an in substance nonfinancial asset),

see Section 810-10-40 on consolidation

c.

A real estate sale-leaseback transaction or a non-real-estate saleleaseback transaction within the scope of Subtopic 360-20 on property, plant, and equipment—real estate sales or Subtopic 840-40 on leases— sale-leaseback transactionsReal estate sale-leaseback transactions, see Subtopics 360-20 and 840-40 on leases

d. A conveyance of oil and gas mineral rights

, see

within the scope of Subtopic 932-360 on extractive activities

—oil and gase.

A transaction that is entirely accounted for in accordance with Topic 860 on transfers and servicing (for example, a transfer of investments accounted for under Topic 320 on investments—debt securities, Topic 321 on investments—equity securities, Topic 323 on investments—equity method and joint ventures, Topic 325 on investments—other, Topic 815 on derivatives and hedging, and Topic 825 on financial instruments) A transfer of a nonfinancial asset to another entity in exchange for a noncontrolling ownership interest in that entity, see the guidance on exchanges of a nonfinancial asset for a noncontrolling ownership interest in Section 845-10-30.

[Content amended as shown and moved from paragraph 610-20-15-3]f. A transfer of nonfinancial assets that is part of the consideration in a business combination within the scope of Topic 805 on business combinations, see paragraph 805-30-30-8

g. A nonmonetary transaction within the scope of Topic 845 on nonmonetary transactions

h. A lease contract within the scope of Topic 840 on leases

i. An exchange of takeoff and landing slots within the scope of Subtopic 908-350 on airlines—intangibles

j. A contribution of cash and other assets, including a promise to give, within the scope of Subtopic 720-25 on other expenses—contributions made or within the scope of Subtopic 958-605 on not-for-profit entities— revenue recognition

k. A transfer of an investment in a venture that is accounted for by proportionately consolidating the assets, liabilities, revenues, and expenses of the venture as described in paragraph 810-10-45-14

l. A transfer of nonfinancial assets or in substance nonfinancial assets solely between entities or persons under common control, such as between a parent and its subsidiaries or between two subsidiaries of the same parent.

In addition, add the following pending content for paragraph 610-20-15-4, with a link to transition paragraph 842-10-65-1:

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2019 | Transition Guidance: 842-10-65-1

610-20-15-4 The guidance in this Subtopic does not apply to the following:

The derecognition of a nonfinancial asset, including an in substance nonfinancial asset,

A transfer of a nonfinancial asset or an in substance nonfinancial asset in a contract with a customer, see Topic 606 on revenue from contracts with customers The derecognition

A transfer of a subsidiary or group of assets that constitutes a business or nonprofit activity (excluding an in substance nonfinancial asset),

see Section 810-10-40 on consolidation - Sale and leaseback transactions within the scope of,

see

Subtopic 842-40 on leases

- A conveyance of oil and gas mineral rights,

see

within the scope of Subtopic 932-360 on extractive activities—oil and gas

- A transaction that is entirely accounted for in accordance with Topic 860 on transfers and servicing (for example, a transfer of investments accounted for under Topic 320 on investments—debt securities, Topic 321 on investments—equity securities, Topic 323 on investments—equity method and joint ventures, Topic 325 on investments—other, Topic 815 on derivatives and hedging, and Topic 825 on financial instruments)

A transfer of a nonfinancial asset to another entity in exchange for a noncontrolling ownership interest in that entity, see the guidance on exchanges of a nonfinancial asset for a noncontrolling ownership interest in Section 845-10-30.

[Content amended as shown and moved from paragraph 610-20-15-3]

- A transfer of nonfinancial assets that is part of the consideration in a business combination within the scope of Topic 805 on business combinations, see paragraph 805-30-30-8

- A nonmonetary transaction within the scope of Topic 845 on nonmonetary transactions

- A lease contract within the scope of Topic 842 on leases

- An exchange of takeoff and landing slots within the scope of Subtopic 908-350 on airlines—intangibles

- A contribution of cash and other assets, including a promise to give, within the scope of Subtopic 720-25 on other expenses—contributions made or within the scope of Subtopic 958-605 on not-for-profit entities— revenue recognition

- An investment in a venture that is accounted by proportionately consolidating the assets, liabilities, revenues, and expenses of the venture as described in paragraph 810-10-45-14

- A transfer of nonfinancial assets or in substance nonfinancial assets solely between entities or persons under common control, such as between a parent and its subsidiaries or between two subsidiaries of the same parent.

> In Substance Nonfinancial Assets

610-20-15-5 An in substance nonfinancial asset is a financial asset (for example, a receivable) promised to a counterparty in a contract if substantially all of the fair value of the assets (recognized and unrecognized) that are promised to the counterparty in the contract is concentrated in nonfinancial assets. If substantially all of the fair value of the assets that are promised to a counterparty in a contract is concentrated in nonfinancial assets, then all of the financial assets promised to the counterparty in the contract are in substance nonfinancial assets. For purposes of this evaluation, when a contract includes the transfer of ownership interests in one or more consolidated subsidiaries that is not a business, an entity shall evaluate the underlying assets in those subsidiaries.

610-20-15-6When a contract includes the transfer of ownership interests in one or more consolidated subsidiaries that is not a business, and substantially all of the fair value of the assets promised to a counterparty in the contract is not concentrated in nonfinancial assets, an entity shall evaluate whether substantially all of the fair value of the assets promised to the counterparty in an individual subsidiary within the contract is concentrated in nonfinancial assets. If substantially all of the fair value of the assets in an individual subsidiary is concentrated in nonfinancial assets, then the financial assets in that subsidiary are in substance nonfinancial assets. (See Case C of Example 1 in paragraphs 610-20-55-9 through 55-10.)

610-20-15-7 When determining whether substantially all of the fair value of the assets promised to a counterparty in a contract (or an individual consolidated subsidiary within a contract) is concentrated in nonfinancial assets, cash or cash equivalents promised to the counterparty shall be excluded. Also, any liabilities assumed or relieved by the counterparty shall not affect the determination of whether substantially all of the fair value of the assets transferred is concentrated in nonfinancial assets.

610-20-15-8 If all of the assets promised to a counterparty in an individual consolidated subsidiary within a contract are not nonfinancial assets and/or in substance nonfinancial assets, an entity shall apply the guidance in paragraph 810-10-40-3A(c) or 810-10-45-21A(b)(2) to determine the guidance applicable to that subsidiary.

> Contracts Partially within the Scope of Other Topics

610-20-15-9 If the promises to a counterparty in a contract are not all nonfinancial assets or all nonfinancial assets and in substance nonfinancial assets, a contract may be partially within the scope of this Subtopic and partially within the scope of other Topics. For example, in addition to transferring nonfinancial assets and in substance nonfinancial assets that are within the scope of this Subtopic, an entity may issue a guarantee to the counterparty that is within the scope of Topic 460 on guarantees. An entity shall apply the guidance in paragraph 606-10-15-4 to determine how to separate and measure one or more parts of a contract that are within the scope of other Topics. (See also Case A of Example 1 in paragraphs 610-20-55-2 through 55-5 and Case C of Example 1 in paragraphs 610-20-55-9 through 55-10.)

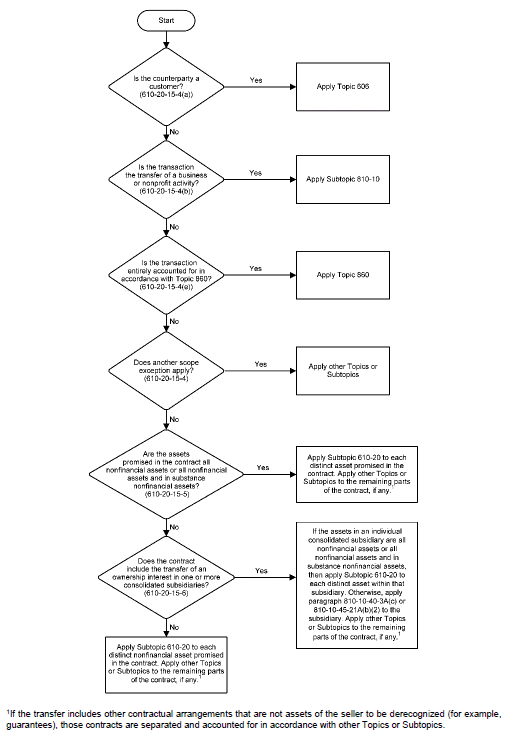

> Decision Tree

610-20-15-10 The following decision tree depicts the process for evaluating whether assets promised to a counterparty in a contract (or parts of a contract) shall be derecognized within the scope of this Subtopic. The decision tree is not intended as a substitute for the guidance in this Subtopic.

[For ease of readability, the new decision tree is not underlined.]

6. Amend paragraph 610-20-25-1 and add paragraphs 610-20-25-2 through 25-7, with a link to transition paragraph 606-10-65-1, as follows:

Recognition

610-20-25-1 To recognize a gain or loss from the transfer of nonfinancial assets or in substance nonfinancial assets within the scope of this Subtopic, an entity shall apply the guidance in Topic 810 on consolidation and in Topic 606 on revenue from contracts with customers as described in paragraphs 610-20-25-2 through 25-7.An entity shall recognize a gain or loss in accordance with the derecognition guidance in Section 610-20-40.

> Determining Whether an Entity Has a Controlling Financial Interest

610-20-25-2 An entity shall first evaluate whether it has (or continues to have) a controlling financial interest in the legal entity that holds the nonfinancial assets and/or in substance nonfinancial assets by applying the guidance in Topic 810 on consolidation. For example, if a parent transfers ownership interests in a consolidated subsidiary, the parent shall evaluate whether it continues to have a controlling financial interest in that subsidiary. Similarly, when an entity transfers assets directly to a counterparty (or a legal entity formed by the counterparty), the entity shall evaluate whether it has a controlling financial interest in the counterparty (or the legal entity formed by the counterparty).

610-20-25-3 If an entity determines it has (or continues to have) a controlling financial interest in the legal entity that holds the nonfinancial assets or in substance nonfinancial assets, it shall not derecognize those assets and shall apply the guidance in paragraphs 810-10-45-21A through 45-24.

610-20-25-4 Any nonfinancial assets or in substance nonfinancial assets transferred that are held in a legal entity in which the entity does not have (or ceases to have) a controlling financial interest shall be further evaluated in accordance with the guidance in paragraphs 610-20-25-5 through 25-7.

> Applying Revenue Recognition Guidance

610-20-25-5 After applying the guidance in paragraphs 610-20-25-2 through 25-4, an entity shall next evaluate a contract in accordance with the guidance in paragraphs 606-10-25-1 through 25-8. If a contract does not meet all of the criteria in paragraph 606-10-25-1, an entity shall not derecognize the nonfinancial assets or in substance nonfinancial assets transferred, and it shall apply the guidance in paragraph 350-10-40-3 to any intangible assets and the guidance in paragraph 360-10-40-3C to any property, plant, and equipment. An entity shall follow the guidance in paragraphs 606-10-25-6 through 25-8 to determine if and when a contract subsequently meets all of the criteria in paragraph 606-10-25-1.

610-20-25-6 Once a contract meets all of the criteria in paragraph 606-10-25-1, an entity shall identify each distinct nonfinancial asset and distinct in substance nonfinancial asset promised to a counterparty in accordance with the guidance in paragraphs 606-10-25-19 through 25-22. An entity shall derecognize each distinct asset when it transfers control of the asset in accordance with paragraph 606-10-25-30. In some cases, control of each asset may transfer at the same time such that an entity may not need to separate and allocate consideration to each distinct nonfinancial asset and in substance nonfinancial asset. That may be the case, for example, when a parent transfers ownership interests in a consolidated subsidiary that holds nonfinancial assets (or nonfinancial assets and in substance nonfinancial assets) and ceases to have a controlling financial interest in the subsidiary in accordance with Topic 810. However, control of each asset may not transfer at the same time if the parent has control of some of the assets in accordance with paragraph 606-10-25-30 (for example, through repurchase agreements).

610-20-25-7 For purposes of evaluating the indicators of the transfer of control in paragraph 606-10-25-30, if an entity has (or continues to have) a noncontrolling interest in the legal entity that holds the nonfinancial assets or in substance nonfinancial assets as a result of the transaction, the entity shall evaluate the point in time at which the legal entity holding the assets obtains (or has) control (for example, by evaluating whether the legal entity can direct the use of, and obtain substantially all of the benefits from, each distinct nonfinancial asset or in substance nonfinancial asset within it). (See Case A of Example 2 in paragraphs 610-20-55-11 through 55-14.) If the entity does not have a noncontrolling interest in the legal entity that holds the nonfinancial assets or in substance nonfinancial assets as a result of the transaction, it shall evaluate the point in time at which a counterparty (or counterparties, collectively) obtains control of the assets in the legal entity (for example, by evaluating whether a counterparty [or counterparties, collectively] can direct the use of, and obtain substantially all of the benefits from, each distinct nonfinancial asset or in substance nonfinancial asset within the legal entity).

7. Supersede paragraph 610-20-32-1 and add paragraphs 610-20-32-2 through 32-6, with a link to transition paragraph 606-10-65-1, as follows:

Measurement

610-20-32-1 Paragraph superseded by Accounting Standards Update No. 2017-05.To determine the amount of consideration to be included in the calculation of a gain or loss recognized upon the derecognition of a nonfinancial asset, an entity shall apply the following paragraphs in Topic 606 on revenue from contracts with customers:

a.

Paragraphs 606-10-32-2 through 32-27 on determining the transaction price, including all of the following:

1.

Estimating variable consideration

2.

Constraining estimates of variable consideration

3.

The existence of a significant financing component

5.

Consideration payable to a customer.

b.

Paragraphs 606-10-32-42 through 32-45 on accounting for changes in the transaction price.

[Content amended and moved to paragraph 610-20-32-3] 610-20-32-2 When an entity meets the criteria to derecognize a distinct nonfinancial asset or a distinct in substance nonfinancial asset, it shall recognize a gain or loss for the difference between the amount of consideration measured and allocated to that distinct asset in accordance with paragraphs 610-20-32-3 through 32-6 and the carrying amount of the distinct asset. The amount of consideration promised in a contract that is included in the calculation of a gain or loss includes both the transaction price and the carrying amount of liabilities assumed or relieved by a counterparty.

610-20-32-3 To determine the

transaction priceamount of consideration to be included in the calculation of a gain or loss recognized upon the derecognition of a nonfinancial asset

, an entity shall apply the following paragraphs in Topic 606 on

revenue from

{remove glossary link}contracts{remove glossary link} with

customers:

a. Paragraphs 606-10-32-2 through 32-27 on determining the {remove glossary link}transaction price{remove glossary link}, including all of the following:

1. Estimating variable consideration

2. Constraining estimates of variable consideration

3. The existence of a significant financing component

4. Noncash consideration

5. Consideration payable to a customer.

b. Paragraphs 606-10-32-42 through 32-45 on accounting for changes in the transaction price. [Content amended as shown and moved from paragraph 610-20-32-1]

610-20-32-4 If an entity transfers control of a distinct nonfinancial asset or distinct in substance nonfinancial asset in exchange for a noncontrolling interest, the entity shall consider the noncontrolling interest received from the counterparty as noncash consideration and shall measure it in accordance with the guidance in paragraphs 606-10-32-21 through 32-24. Similarly, if a parent transfers control of a distinct nonfinancial asset or in substance nonfinancial asset by transferring ownership interests in a consolidated subsidiary but retains a noncontrolling interest in its former subsidiary, the entity shall consider the noncontrolling interest retained as noncash consideration and shall measure it in accordance with the guidance in paragraphs 606-10-32-21 through 32-24. (See Case A of Example 2 in paragraphs 610-20-55-11 through 55-14.)

610-20-32-5 If a counterparty promises to assume or relieve a liability of an entity in exchange for a transfer of nonfinancial assets or in substance nonfinancial assets within the scope of this Subtopic, the transferring entity shall include the carrying amount of the liability in the consideration used to calculate the gain or loss. Although a liability assumed or relieved by a counterparty shall be included in the consideration used to calculate a gain or loss, an entity shall not derecognize the liability until it has been extinguished in accordance with the guidance in paragraph 405-20-40-1 (see paragraph 610-20-45-3 on how to present the liability if it is extinguished before or after the entity transfers control of the nonfinancial assets or in substance nonfinancial assets). If an entity transfers control of the nonfinancial assets or in substance nonfinancial assets before a liability is extinguished, it shall apply the guidance on constraining estimates of variable consideration in paragraph 606-10-32-11 to determine the carrying amount of the liability to be included in the gain or loss calculation.

610-20-32-6 An entity shall allocate the consideration calculated in accordance with the guidance in paragraphs 610-20-32-2 through 32-5 to each distinct nonfinancial asset or in substance nonfinancial asset by applying the guidance in paragraphs 606-10-32-28 through 32-41.

8. Supersede paragraphs 610-20-40-1 through 40-2, with a link to transition paragraph 606-10-65-1, as follows:

Derecognition

610-20-40-1 Paragraph superseded by Accounting Standards Update No. 2017-05. To determine when a nonfinancial asset shall be derecognized, an entity shall apply the following paragraphs in Topic 606 on revenue from contracts with customers:

a.

Paragraphs 606-10-25-1 through 25-8 on the existence of a contract

b.

Paragraph 606-10-25-30 on when an entity satisfies a performance obligation by transferring control of an asset.

610-20-40-2 Paragraph superseded by Accounting Standards Update No. 2017-05.When the guidance in paragraph 610-20-40-1 is met, an entity shall derecognize the nonfinancial asset and recognize as a gain or loss the difference between the amount of consideration measured in accordance with paragraph 610-20-32-1 and the carrying amount of the nonfinancial asset. When the guidance in paragraph 610-20-40-1 is not met, an entity shall apply the guidance in paragraphs 350-10-40-3 to intangible assets and 360-10-40-3C to property, plant, and equipment.

9. Add paragraphs 610-20-45-2 through 45-3, with a link to transition paragraph 606-10-65-1, as follows:

Other Presentation Matters

610-20-45-1 See paragraph 360-10-45-5 for guidance on presentation of a gain or loss recognized on the sale of a long-lived asset (disposal group).

610-20-45-2 When either party to a contract has performed, an entity shall apply the guidance in paragraphs 606-10-45-1 through 45-5 to present the relationship between the entity's performance and the counterparty's payment.

610-20-45-3 If an entity meets the criteria in paragraph 405-20-40-1 to derecognize a liability assumed (or relieved) by a counterparty before transferring control of a distinct nonfinancial asset, the liability shall be derecognized but no gain or loss shall be recognized. Instead, the entity shall record a contract liability, which represents consideration received before transferring control of the asset. If an entity transfers control of a distinct nonfinancial asset before meeting the criteria to derecognize a liability assumed by a counterparty, the entity shall recognize a contract asset to the extent the carrying amount of the liability is included in the calculation of the gain or loss.

10. Add Section 610-20-50, with a link to transition paragraph 606-10-65-1, as follows:

Disclosure

General

610-20-50-1 See paragraphs 360-10-50-3 through 50-3A for guidance on disclosure of a gain or loss recognized upon the derecognition of a long-lived asset (disposal group).

11. Amend paragraph 610-20-55-1 and supersede its related heading, amend paragraphs 610-20-55-2 through 55-4 and their related heading, and add paragraphs 610-20-55-5 through 55-19 and their related headings, with a link to transition paragraph 606-10-65-1, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Sale of a Nonfinancial Asset

610-20-55-1 The following

Examples illustrateExample illustrates

the guidance in this Subtopic.

> > > Example 1—Sale of a Nonfinancial Asset for Variable Consideration

> > Example 1—Scope

> > > Case A—Nonfinancial Assets, In Substance Nonfinancial Assets, and a Guarantee

610-20-55-2 Seller enters into a contract to transfer real estate, the related operating leases, and accounts receivable to Buyer. Seller guarantees Buyer that the cash flows of the property will be sufficient to meet all of the operating needs of the property for two years after the sale. In the event that the cash flows are not sufficient, Seller is required to make a payment in the amount of the shortfall. An entity sells the rights to in-process research and development that it recently acquired in a business combination and measured at fair value of $50 million in accordance with Topic 805 on business combinations. The buyer of the in-process research and development agrees to pay a nonrefundable amount of $5 million at inception plus 2 percent of sales of any products derived from the in-process research and development over the next 20 years. The entity concludes that the sale of in-process research and development is not a good or service that is an output of the entity's ordinary activities.

[Content amended and moved to paragraph 610-20-55-17]

610-20-55-3 Seller concludes that the assets promised in the contract are not a business within the scope of Topic 810 on consolidation and are not an output of Seller's ordinary activities within the scope of Topic 606 on revenue from contracts with customers. In addition, assume that Seller concludes that substantially all of the fair value of the assets promised in the contract is concentrated in nonfinancial assets (that is, substantially all of the fair value is concentrated in the real estate and in-place lease intangible assets). Therefore, the accounts receivable promised in the contract are in substance nonfinancial assets. In accordance with the guidance in this Subtopic, all of the assets in the contract, including the accounts receivable, are within the scope of this Subtopic.Topic 350 on goodwill and other intangibles requires the entity to apply the guidance on existence of a contract, control, and measurement in Topic 606 on revenue from contracts with customers to determine the amount and timing of income to be recognized as follows:

a.

The entity concludes that the criteria for identifying a contract in paragraph 606-10-25-1 are met.

b.

The entity also concludes that on the basis of the guidance in paragraph 606-10-25-30, it has transferred control of the in-process research and development asset to the buyer as of contract inception. This is because as of contract inception the buyer can use the in-process research and development's records, patents, and supporting documentation to develop potential products and the entity has relinquished all substantive rights to the in-process research and development asset.

c.

In estimating the consideration received, the entity applies the guidance in Topic 606 on determining the

transaction price

, including estimating and constraining variable consideration. The entity estimates that the amount of consideration that it will receive from the sales-based royalty is $100 million over the 20-year royalty period. However, the entity cannot assert that it is probable that recognizing all of the estimated variable consideration in other income would not result in a significant reversal of that consideration. The entity reaches this conclusion on the basis of its assessment of factors in paragraph 606-10-32-12. In particular, the entity is aware that the variable consideration is highly susceptible to the actions and judgments of third parties, because it is based on the buyer completing the in-process research and development asset, obtaining regulatory approval for the output of the in-process research and development asset, and marketing and selling the output. For the same reasons, the entity also concludes that it could not include any amount, even a minimum amount, in the estimate of the consideration. Consequently, the entity concludes that the estimate of the consideration to be used in the calculation of the gain or loss upon the derecognition of the in-process research and development asset is limited to the $5 million fixed upfront payment.

[Content amended and moved to paragraph 610-20-55-18]610-20-55-4 Seller concludes that the guarantee, which is a liability of Seller, is within the scope of Topic 460 on guarantees. Therefore, Seller would apply the guidance in paragraph 606-10-15-4 to separate and measure the guarantee as described in paragraph 610-20-15-9.At inception of the contract, the entity recognizes a net loss of $45 million ($5 million of consideration, less the in-process research and development asset of $50 million). The entity reassesses the transaction price at each reporting period to determine whether it is probable that a significant reversal would not occur from recognizing the estimate as other income and, if so, recognizes that amount as other income in accordance with paragraphs 606-10-32-14 and 606-10-32-42 through 32-45.

[Content moved to paragraph 610-20-55-19]

610-20-55-5 Seller's conclusions would be the same if it transferred the real estate, leases, and receivables by transferring ownership interests in a consolidated subsidiary. That is, Seller would still conclude that all of the assets in the subsidiary are nonfinancial assets and in substance nonfinancial assets within the scope of this Subtopic and that the guarantee is within the scope of Topic 460.

> > > Case B—Nonfinancial Assets and Financial Assets

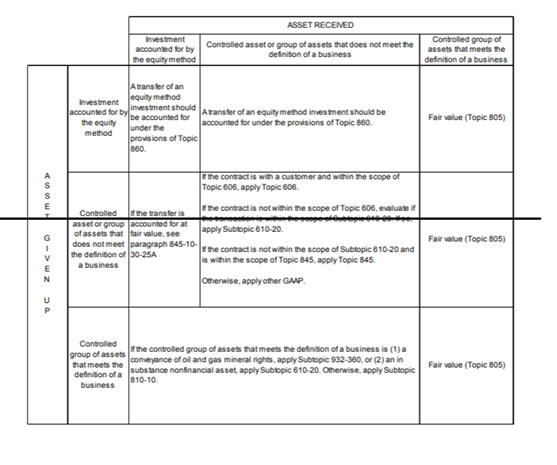

610-20-55-6 Entity X enters into a contract to transfer machinery and financial assets, both of which have significant fair value. Entity X concludes that the assets promised in the contract are not a business within the scope of Topic 810 and are not an output of the entity's ordinary activities within the scope of Topic 606. Entity X also concludes that substantially all of the fair value of the assets promised in the contract is not concentrated in nonfinancial assets. Therefore, the financial assets promised in the contract are not in substance nonfinancial assets.

610-20-55-7 In accordance with the guidance in paragraph 610-20-15-9, Entity X should derecognize only the machinery in accordance with this Subtopic. Entity X should apply the guidance in paragraph 606-10-15-4 to separate and measure the financial assets.

610-20-55-8 If Entity X transfers the machinery and financial assets by transferring ownership interests in a consolidated subsidiary, it would still conclude that the financial assets are not in substance nonfinancial assets. As described in paragraph 610-20-15-8, if all of the assets promised to the counterparty in an individual consolidated subsidiary within a contract are not nonfinancial assets and/or in substance nonfinancial assets, those assets should not be derecognized in accordance with this Subtopic. Instead, Entity X should apply the guidance in paragraph 810-10-40-3A(c) or 810-10-45-21A(b)(2) to determine the guidance applicable to that subsidiary.

> > > Case C—One Subsidiary That Holds Nonfinancial Assets and One Subsidiary That Holds Financial Assets

610-20-55-9 Entity A enters into a contract to transfer ownership interests in two consolidated subsidiaries to a single counterparty. Subsidiary 1 consists entirely of nonfinancial assets, and Subsidiary 2 consists entirely of financial assets. Assume that the assets in Subsidiary 1 and Subsidiary 2 have an equal amount of fair value. Entity A concludes that the transaction is not the transfer of a business within the scope of Topic 810 and that the subsidiaries are not outputs of the entity's ordinary activities within the scope of Topic 606.

610-20-55-10 Entity A first considers whether substantially all of the fair value of the assets promised to the counterparty in the contract is concentrated in nonfinancial assets. Because the contract includes the transfer of ownership interests in one or more consolidated subsidiaries, Entity A evaluates the underlying assets in those subsidiaries. Entity A concludes that because both the financial assets and nonfinancial assets have an equal amount of fair value, substantially all of the fair value of the assets promised to the counterparty in the contract is not concentrated in nonfinancial assets. Entity A next considers whether substantially all of the fair value of the assets within Subsidiary 1 or Subsidiary 2 is concentrated in nonfinancial assets. Because the assets transferred within Subsidiary 1 are entirely nonfinancial assets, Entity A concludes that those assets are within the scope of this Subtopic. Entity A also concludes that the financial assets in Subsidiary 2 are not in substance nonfinancial assets and, therefore, are not within the scope of this Subtopic. Entity A should apply the guidance in paragraph 606-10-15-4 to separate and measure the financial assets in Subsidiary 2 from the nonfinancial assets in Subsidiary 1 that are derecognized within the scope of this Subtopic.

> > Example 2—Transfer of Control

> > > Case A—Control Transfers under Topics 810 and 606

610-20-55-11 Entity A owns 100 percent of Entity B, a consolidated subsidiary. Entity B holds title to land with a carrying amount of $5 million. Entity A concludes that the land is not an output of its ordinary activities within the scope of Topic 606 and that Entity B does not meet the definition of a business within the scope of Topic 810.

610-20-55-12 Entity A enters into a contract to transfer 60 percent of Entity B to Entity X for $6 million cash due at contract inception. For ease of illustration, assume that at contract inception the fair value of the 40 percent interest retained by Entity A is $4 million. Because all of the assets (the land) promised to Entity X in the contract are nonfinancial assets, Entity A concludes that it should derecognize the land in accordance with this Subtopic.

610-20-55-13 As described in paragraphs 610-20-25-2 through 25-7, Entity A first considers the guidance in Topic 810 and concludes that it no longer has a controlling financial interest in Entity B or in Entity X (the buyer). Entity A then determines that the contract meets the criteria in paragraph 606-10-25-1 and that control of the land has been transferred in accordance with the guidance in paragraph 606-10-25-30. Because Entity A continues to have a noncontrolling interest in Entity B, it evaluates the point in time at which Entity B, its former subsidiary, has control of the distinct nonfinancial asset as described in paragraph 610-20-25-7. Entity A concludes that it has transferred control of the distinct nonfinancial asset because Entity B controls the distinct nonfinancial asset. When evaluating the indicators of control in paragraph 606-10-25-30, Entity A concludes the following:

a. It has the present right to payment.

b. Entity B has legal title to the land.

c. It does not have physical possession of the asset because it cannot restrict or prevent other entities from accessing the land.

d. Entity B has the significant risks and rewards of ownership.

e. There is no acceptance clause (assumption).

610-20-55-14 Entity A derecognizes the land and calculates the gain or loss as the difference between the amount of consideration measured in accordance with the guidance in paragraphs 610-20-32-2 and 610-20-32-6 and the carrying amount of the land. The amount of the consideration is $10 million, which includes $6 million in cash plus $4 million for the fair value of the noncontrolling interest in Entity B. Entity A recognizes a gain of $5 million ($10 million consideration ‒ $5 million carrying amount of the assets) and presents the gain in the income statement in accordance with the guidance in paragraph 360-10-45-5. In accordance with the guidance in paragraph 610-20-32-4, Entity A records the noncontrolling interest in Entity B at $4 million and subsequently accounts for that interest in accordance with other Topics.

> > > Case B—Control Transfers under Topic 810 but Not under Topic 606

610-20-55-15 Assume the same facts as in Case A, except that Entity A has the right but not the obligation to repurchase the 60 percent ownership interest in Entity B that it transferred to Entity X (that is, Entity A has a call option). The call option gives Entity A the right to repurchase the 60 percent ownership interest in 2 years for $7 million.

610-20-55-16 Entity A concludes that although the call option represents a variable interest in Entity B, it does not have a controlling financial interest in Entity B in accordance with the guidance in Topic 810. However, when evaluating whether control of the land has been transferred in accordance with the guidance in paragraph 606-10-25-30, Entity A considers the guidance on repurchase features in paragraphs 606-10-25-30(c) and 606-10-55-68 and concludes that it does not transfer control of the land. In addition, because the exercise price on the call option is an amount that is greater than the original selling price, the transaction is considered a financing agreement in accordance with the guidance in paragraph 606-10-55-68(b). Entity A does not derecognize the land and records a financial liability of $6 million in accordance with the guidance in paragraph 606-10-55-70. Entity A does not recognize an investment for its retained 40 percent ownership interest until it derecognizes the land.

> > > Example 1

> > Example 3—Sale of a Nonfinancial Asset for Variable Consideration 610-20-55-17 An entity sells (that is, does not out license) the rights to in-process research and development that it recently acquired in a business combination and measured at fair value of $50 million in accordance with Topic 805 on business combinations. The entity concludes that the transferred in-process research and development is not a business. The buyer of the in-process research and development agrees to pay a nonrefundable amount of $5 million at inception plus 2 percent of sales of any products derived from the in-process research and development over the next 20 years. The entity concludes that the sale of inprocess research and development is not a good or service that is an output of the entity's ordinary activities. [Content amended as shown and moved from paragraph 610-20-55-2]

610-20-55-18 Topic 350 on goodwill and other intangibles requires the entity to apply the guidance

in this Subtopicon existence of a

contract

, control, and measurement in Topic 606 on

revenue

from contracts with customers

to determine the amount and timing of income to be

recognized

recognized. Therefore, the entity applies the derecognition guidance in this Subtopic as follows:

a. The entity concludes that it does not have a controlling financial interest in the buyer.

a.

b. The entity concludes that the

criteria for identifying a

contract

meets the criteria in paragraph 606-10-25-1

are met

.

b.

c. The entity also concludes that on the basis of the guidance in paragraph 606-10-25-30, it has transferred control of the in-process research and development asset to the buyer

as of contract inception

. This is because

as of contract inception

the buyer can use the in-process research and development's records, patents, and supporting documentation to develop potential products and the entity has relinquished all substantive rights to the in-process research and development asset.

c.

d. In estimating the consideration received, the entity applies the guidance in Topic 606 on determining the

transaction price, including estimating and constraining variable consideration. The entity estimates that the amount of consideration that it will receive from the sales-based royalty is $100 million over the 20-year royalty period. However, the entity cannot assert that it is probable that recognizing all of the estimated variable consideration in other income would not result in a significant reversal of that consideration. The entity reaches this conclusion on the basis of its assessment of factors in paragraph 606-10-32-12. In particular, the entity is aware that the variable consideration is highly susceptible to the actions and judgments of third parties, because it is based on the buyer completing the in-process research and development asset, obtaining regulatory approval for the output of the in-process research and development asset, and marketing and selling the output. For the same reasons, the entity also concludes that it could not include any amount, even a minimum amount, in the estimate of the consideration. Consequently, the entity concludes that the estimate of the consideration to be used in the calculation of the gain or loss upon the derecognition of the in-process research and development asset is limited to the $5 million fixed upfront payment.

[Content amended as shown and moved from paragraph 610-20-55-3]610-20-55-19 At inception of the contract, the entity recognizes a net loss of $45 million ($5 million of consideration, less the in-process research and development asset of $50 million). The entity reassesses the transaction price at each reporting period to determine whether it is probable that a significant reversal would not occur from recognizing the estimate as other income and, if so, recognizes that amount as other income in accordance with paragraphs 606-10-32-14 and 610-10-32-42 through 32-45. [Content moved from paragraph 610-20-55-4]