2. Supersede paragraphs 820-10-50-1 through 50-1B, add paragraphs 820-10-50-1C through 820-10-50-1E, and 820-10-50-2G, and amend paragraphs 820-10-50-2, 820-10-50-2C, 820-10-50-2F, 820-10-50-3, 820-10-50-6A, and 820-10-50-10, with a link to transition paragraph 820-10-65-12, as follows:

Fair Value Measurement—Overall

Disclosure

820-10-50-1 Paragraph superseded by Accounting Standards Update No. 2018-13. A reporting entity shall disclose information that helps users of its financial statements assess both of the following:

a. For assets and liabilities that are measured at fair value on a recurring or nonrecurring basis in the statement of financial position after initial recognition, the valuation techniques and inputs used to develop those measurements

b. For recurring fair value measurements using significant unobservable inputs (Level 3), the effect of the measurements on earnings (or changes in net assets) or other comprehensive income for the period

.

820-10-50-1A Paragraph superseded by Accounting Standards Update No. 2018-13.To meet the objectives in the preceding paragraph, a reporting entity shall consider all of the following:

a. The level of detail necessary to satisfy the disclosure requirements

b. How much emphasis to place on each of the various requirements

c. How much aggregation or disaggregation to undertake

d. Whether users of financial statements need additional information to evaluate the quantitative information disclosed.

If the disclosures provided in accordance with this Topic and other Topics are insufficient to meet the objectives in the preceding paragraph, a reporting entity shall disclose additional information necessary to meet those objectives.

[Content amended and moved to paragraph 820-10-50-1D] 820-10-50-1B Paragraph superseded by Accounting Standards Update No. 2018-13. Paragraphs 820-10-55-99 through 55-107 illustrate disclosures about fair value measurements.

[Content amended and moved to paragraph 820-10-50-1E]

820-10-50-1C The objective of the disclosure requirements in this Subtopic is to provide users of financial statements with information about assets and liabilities measured at fair value in the statement of financial position or disclosed in the notes to financial statements:

a. The valuation techniques and inputs that a reporting entity uses to arrive at its measures of fair value, including judgments and assumptions that the entity makes

b. The uncertainty in the fair value measurements as of the reporting date

c. How changes in fair value measurements affect an entity’s performance and cash flows.

820-10-50-1D To meet the objectives in the preceding paragraph

When complying with the disclosure requirements of this Subtopic, a reporting entity shall consider all the following:

a. The level of detail necessary to satisfy the disclosure requirements

b. How much emphasis to place on each of the various requirements

c. How much aggregation or disaggregation to undertake

d. Whether users of financial statements need additional information to evaluate the quantitative information disclosed.

If the disclosures provided in accordance with this topic and other Topics are

insufficient to meet the objectives in the preceding

paragraph, a reporting entity shall disclose additional information necessary to meet those objectives.

[Content amended as shown and moved from paragraph 820-10-50-1A] 820-10-50-1E Paragraphs 820-10-55-99 through 55-107 illustrate disclosures about fair value measurements. [Content moved from paragraph 820-10-50-1B]

820-10-50-2 To meet the objectives in paragraph 820-10-50-1, a

A reporting entity shall disclose,

at a minimum,

the following information for each class of assets and liabilities (see paragraph 820-10-50-2B for information on determining appropriate classes of assets and liabilities) measured at fair value (including measurements based on fair value within the scope of this Topic) in the statement of financial position after initial recognition:

a. For recurring fair value measurements, the fair value measurement at the end of the reporting period, and for nonrecurring fair value measurements, the fair value measurement at the relevant measurement date and the reasons for the measurement. Recurring fair value measurements of assets or liabilities are those that other Topics require or permit in the statement of financial position at the end of each reporting period. Nonrecurring fair value measurements of assets or liabilities are those that other Topics require or permit in the statement of financial position in particular circumstances (for example, when a reporting entity measures a long-lived asset or disposal group classified as held for sale at fair value less costs to sell in accordance with Topic 360 because the asset’s fair value less costs to sell is lower than its carrying amount). For nonrecurring measurements estimated at a date during the reporting period other than the end of the reporting period, a reporting entity shall clearly indicate that the fair value information presented is not as of the period’s end as well as the date or period that the measurement was taken.

b. For recurring and nonrecurring fair value measurements, the level of the fair value hierarchy within which the fair value measurements are categorized in their entirety (Level 1, 2, or 3).

1. Subparagraph superseded by Accounting Standards Update No. 2011-04

2. Subparagraph superseded by Accounting Standards Update No. 2011-04

3. Subparagraph superseded by Accounting Standards Update No. 2011-04

bb.

Subparagraph superseded by Accounting Standards Update No. 2018-13.For assets and liabilities held at the end of the reporting period that are measured at fair value on a recurring basis, the amounts of any transfers between Level 1 and Level 2 of the fair value hierarchy, the reasons for those transfers, and the reporting entity’s policy for determining when transfers between levels are deemed to have occurred (see paragraph 820-10-50-2C). Transfers into each level shall be disclosed and discussed separately from transfers out of each level.

1. Subparagraph superseded by Accounting Standards Update No. 2011-04

2. Subparagraph superseded by Accounting Standards Update No. 2011-04

3. Subparagraph superseded by Accounting Standards Update No. 2011-04

bbb. The information shall include:

1. For recurring and nonrecurring fair value measurements categorized within Level 2 and Level 3 of the fair value hierarchy, a description of the valuation technique(s) and the inputs used in the fair value measurement. If there has been a change in either or both a valuation approach and a valuation technique (for example, changing from matrix pricing to the binomial model or the use of an additional valuation technique), the reporting entity shall disclose that change and the reason(s) for making it.

2. For recurring and nonrecurring fair value measurements categorized within Level 3 of the fair value hierarchy, a reporting entity shall provide quantitative information about the significant {add glossary link}unobservable inputs{add glossary link} used in the fair value measurement. A reporting entity is not required to create quantitative information to comply with this disclosure requirement if quantitative unobservable inputs are not developed by the reporting entity when measuring fair value (for example, when a reporting entity uses prices from prior transactions or third-party pricing information without adjustment). However, when providing this disclosure, a reporting entity cannot ignore quantitative unobservable inputs that are significant to the fair value measurement and are reasonably available to the reporting entity. Employee benefit plans, other than those plans that are subject to the U.S. Securities and Exchange Commission’s (SEC) filing requirements, are not required to provide this disclosure for investments held by an employee benefit plan in their plan sponsor’s own nonpublic equity securities, including equity securities of their plan sponsor’s nonpublic affiliated entities.

i. In complying with (bbb)(2), a reporting entity shall provide the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements. A reporting entity shall disclose how it calculated the weighted average (for example, weighted by relative fair value). For certain unobservable inputs, a reporting entity may disclose other quantitative information, such as the median or arithmetic average, in lieu of the weighted average, if such information would be a more reasonable and rational method to reflect the distribution of unobservable inputs used to develop the Level 3 fair value measurement. An entity does not need to disclose its reason for omitting the weighted average in these cases.

ii. A nonpublic entity is not required to provide the information described in (bbb)(2)(i), but is required to provide quantitative information about the significant unobservable inputs used in the fair value measurement in accordance with (bbb)(2).

c. For recurring fair value measurements categorized within Level 3 of the fair value hierarchy, a reconciliation from the opening balances to the closing balances, disclosing separately changes during the period attributable to the following:

1. Total gains or losses for the period recognized in earnings (or changes in net assets), and the line item(s) in the statement of income (or activities) in which those gains or losses are recognized

1a. Total gains or losses for the period recognized in other comprehensive income, and the line item(s) in other comprehensive income in which those gains or losses are recognized

2. Purchases, sales, issues, and settlements (each of those types of changes disclosed separately)

3. The amounts of any transfers into or out of Level 3 of the fair value

hierarchy,

hierarchy and the reasons for those transfers,

and the reporting entity’s policy for determining when transfers between levels are deemed to have occurred (see paragraph 820-10-50-2C).

Transfers into Level 3 shall be disclosed and discussed separately from transfers out of Level 3.

See paragraph 820-10-50-2C for additional guidance.i. Subparagraph superseded by Accounting Standards Update No. 2011-04

ii. Subparagraph superseded by Accounting Standards Update No. 2011-04

iii. Subparagraph superseded by Accounting Standards Update No. 2011-04

d. For recurring fair value measurements categorized within Level 3 of the fair value hierarchy, the amount of the total gains or losses for the period in (c)(1) included in earnings (or changes in net assets)

and in (c)(1a) included in other comprehensive income that is attributable to the change in unrealized gains or losses relating to those assets and liabilities held at the end of the reporting period, and the line item(s) in the

statement

statement(s) of

comprehensive income (or activities) in which those unrealized gains or losses are recognized.

e. Subparagraph superseded by Accounting Standards Update No. 2011-04

f.

Subparagraph superseded by Accounting Standards Update No. 2018-13.For recurring and nonrecurring fair value measurements categorized within Level 3 of the fair value hierarchy, a description of the valuation processes used by the reporting entity (including, for example, how an entity decides its valuation policies and procedures and analyzes changes in fair value measurements from period to period). See paragraph 820-10-55-105 for further guidance.

g. For recurring fair value measurements categorized within Level 3 of the fair value hierarchy, a narrative description of the

uncertainty sensitivity

of the fair value measurement

to changes in unobservable inputs if

from the use of significant unobservable inputs if those inputs reasonably could have been different at the reporting date. For example, how a change in those

significant unobservable inputs to a different amount might result in a significantly higher or lower fair value measurement

at the reporting date. If there are interrelationships between those inputs and other unobservable inputs used in the fair value measurement, a reporting entity shall also provide a description of those interrelationships and of how they might magnify or mitigate the effect of changes in the unobservable inputs on the fair value measurement. To comply with that disclosure requirement, the narrative description of the

sensitivity to changes in

uncertainty of the fair value measurement that would result from using unobservable inputs shall

include include, at a minimum

, the unobservable inputs disclosed when complying with paragraph 820-10-50-2(bbb).

h. For recurring and nonrecurring fair value measurements, if the highest and best use of a nonfinancial asset differs from its current use, a reporting entity shall disclose that fact and why the nonfinancial asset is being used in a manner that differs from its highest and best use.

820-10-50-2C A reporting entity shall

disclose and

consistently follow its policy for determining when transfers between levels of the fair value hierarchy are deemed to have occurred

in accordance with paragraph 820-10-50-2(bb) and (c)(3)

. The policy about the timing of recognizing transfers shall be the same for transfers into the levels as for transfers out of the levels. Examples of policies for determining the timing of transfers include the following:

a. The date of the event or change in circumstances that caused the transfer

b. The beginning of the reporting period

c. The end of the reporting period.

820-10-50-2E For each class of assets and liabilities not measured at fair value in the statement of financial position but for which the fair value is disclosed, a reporting entity shall disclose the information required by paragraph 820-10-50-2(b), (bbb)(1), and (h). However, a reporting entity is not required to provide the quantitative disclosures about significant unobservable inputs used in fair value measurements categorized within Level 3 of the fair value hierarchy required by paragraph 820-10-50-2(bbb)(2). For such assets and liabilities, a reporting entity does not need to provide the other disclosures required by this Topic.

820-10-50-2F A

nonpublic entity is not required to disclose the information required by

paragraph 820-10-50-2(bb) and (g)

paragraph 820-10-50-2(bbb)(2)(i), (d), and (g) and paragraph 820-10-50-2E unless required by another Topic.

820-10-50-2G In lieu of paragraph 820-10-50-2(c), a nonpublic entity shall disclose separately changes during the period attributable to the following:

a. Purchases and issues (each of those types of changes disclosed separately)

b. The amounts of any transfers into or out of Level 3 of the fair value hierarchy and the reasons for those transfers. Transfers into Level 3 shall be disclosed and discussed separately from transfers out of Level 3. See paragraph 820-10-50-2C for additional guidance.

820-10-50-3 For derivative assets and liabilities, the reporting entity shall present both of the following:

a. The fair value disclosures required by paragraph 820-10-50-2(a) through

(b) (bb)

on a gross basis (which is consistent with the requirement of paragraph 815-10-50-4B(a))

b. The reconciliation disclosure required by paragraph 820-10-50-2(c) through (d) on either a gross or a net basis.

> Fair Value Measurements of Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent)

820-10-50-6A For investments that are within the scope of paragraphs 820-10-15-4 through 15-5 and that are measured using the practical expedient in paragraph 820-10-35-59 on a recurring or nonrecurring basis during the period, a reporting entity shall disclose information that helps users of its financial statements to understand the nature and risks of the investments and whether the investments, if sold, are probable of being sold at amounts different from

net asset value per share (or its equivalent, such as member units or an ownership interest in partners’ capital to which a proportionate share of net assets is attributed).

To meet that objective, to the extent applicable, a

A reporting entity shall disclose,

at a minimum,

the following information for each class of investment:

a. The fair value measurement (as determined by applying paragraphs 820-10-35-59 through 35-62) of the investments in the class at the reporting date and a description of the significant investment strategies of the investee(s) in the class.

b. For each class of investment that includes investments that can never be redeemed with the investees, but the reporting entity receives distributions through the liquidation of the underlying assets of the investees,

the reporting entity’s estimate of

the period of time over which the underlying assets are expected to be liquidated by the investees

if the investee has communicated the timing to the reporting entity or announced the timing publicly. If the timing is unknown, the reporting entity shall disclose that fact.c. The amount of the reporting entity’s unfunded commitments related to investments in the class.

d. A general description of the terms and conditions upon which the investor may redeem investments in the class (for example, quarterly redemption with 60 days’ notice).

e. The circumstances in which an otherwise redeemable investment in the class (or a portion thereof) might not be redeemable (for example, investments subject to a lockup or gate). Also, for those otherwise redeemable investments that are restricted from redemption as of the reporting entity’s measurement date, the reporting entity shall disclose

its estimate of

when the restriction from redemption might lapse

if the investee has communicated that timing to the reporting entity or announced the timing publicly. If

the timing is unknown an estimate cannot be made

, the reporting entity shall disclose that fact and how long the restriction has been in effect.

f. Any other significant restriction on the ability to sell investments in the class at the measurement date.

g. Subparagraph superseded by Accounting Standards Update No. 2015-07.

h. If a group of investments would otherwise meet the criteria in paragraph 820-10-35-62 but the individual investments to be sold have not been identified (for example, if a reporting entity decides to sell 20 percent of its investments in private equity funds but the individual investments to be sold have not been identified), so the investments continue to qualify for the practical expedient in paragraph 820-10-35-59, the reporting entity shall disclose its plans to sell and any remaining actions required to complete the sale(s).

> Tabular Format Required

820-10-50-10 Plan assets of a defined benefit pension or other postretirement plan that are accounted for in accordance with Topic 715 are not subject to the disclosure requirements in paragraphs

820-10-50-1C through 50-8 820-10-50-1 through 50-9.

Instead, the disclosures required in paragraphs 715-20-50-1(d)(iv) and 715-20-50-5(c)(iv) shall apply for fair value measurements of plan assets of a defined benefit pension or other postretirement plan.

3. Amend paragraphs 820-10-55-99, 820-10-55-101, 820-10-55-103 through 55-104, 820-10-55-106 through 55-107 and the related heading and supersede paragraph 820-10-55-105 and its related heading, with a link to transition paragraph 820-10-65-12, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Example 9: Fair Value Disclosures

820-10-55-99 The disclosures required by paragraphs

820-10-50-1D, 820-10-50-2(a) through (b), (bbb) through (d), and (g) 820-10-50-1A, 820-10-50-2(a) through (b) and (bbb) through (g

), 820-10-50-6A, and 820-10-50-8 are illustrated by the following Cases:

a. Assets measured at fair value (Case A)

b. Reconciliation of fair value measurements categorized within Level 3 of the fair value hierarchy (Case B)

c. Information about fair value measurements categorized within Level 3 of the fair value hierarchy (Case C)

d. Fair value measurements of investments

in certain entities that calculate

that are measured at net asset value per share (or its equivalent)

as a practical expedient (Case D).

> > > Case B: Disclosure—Reconciliation of Fair Value Measurements Categorized within Level 3 of the Fair Value Hierarchy

820-10-55-101 For recurring fair value measurements categorized within Level 3 of the fair value hierarchy, this Topic requires a reconciliation from the opening balances to the closing balances for each class of assets and liabilities, except for derivative assets and liabilities, which may be presented net. A reporting entity might disclose the following for assets to comply with paragraph 820-10-50-2(c) through (d).

> > > Case C: Disclosure—Information about Fair Value Measurements Categorized within Level 3 of the Fair Value Hierarchy

> > > > Valuation Techniques and Inputs

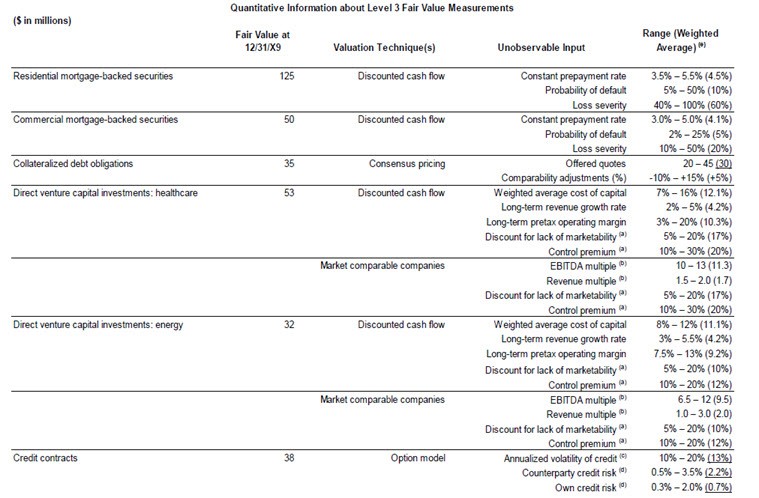

820-10-55-103 For fair value measurements categorized within Level 2 and Level 3 of the fair value hierarchy, this Topic requires a reporting entity to disclose a description of the valuation technique(s) and the inputs used in the fair value measurement. For fair value measurements categorized within Level 3 of the fair value hierarchy, information about the significant unobservable inputs used must be quantitative. A reporting entity might disclose the following for assets to comply with the requirement to disclose the significant unobservable inputs used in the fair value measurement in accordance with paragraph 820-10-50-2(bbb).

(a) Represents amounts used when the reporting entity has determined that market participants would take into account these premiums and discounts when pricing the investments.

(b) Represents amounts used when the reporting entity has determined that market participants would use such multiples when pricing the investments.

(c) Represents the range of the volatility curves used in the valuation analysis that the reporting entity has determined market participants would use when pricing the contracts.

(d) Represents the range of the credit default swap spread curves used in the valuation analysis that the reporting entity has determined market participants would use when pricing the contracts.

(e) Unobservable inputs were weighted by the relative fair value of the instruments. For credit contracts, the average represents the arithmetic average of the inputs and is not weighted by the relative fair value or notional amount.

(Note: For liabilities, a similar table should be presented.)

820-10-55-104 In addition, a reporting entity should provide additional information that will help users of its financial statements to evaluate the quantitative information disclosed. A reporting entity might disclose some or all of the following to comply with paragraph

820-10-50-1D 820-10-50-1A

:

a. The nature of the item being measured at fair value, including the characteristics of the item being measured that are taken into account in the determination of relevant inputs. For example, for residential mortgage-backed securities, a reporting entity might disclose the following:

1. The types of underlying loans (for example, prime loans or subprime loans)

2. Collateral

3. Guarantees or other credit enhancements

4. Seniority level of the tranches of securities

5. The year of issue

6. The weighted-average coupon rate of the underlying loans and the securities

7. The weighted-average maturity of the underlying loans and the securities

8. The geographical concentration of the underlying loans

9. Information about the credit ratings of the securities.

b. How third-party information such as broker quotes, pricing services, net asset values, and relevant market data was taken into account when measuring fair value.

> > > > Valuation Processes

820-10-55-105 Paragraph superseded by Accounting Standards Update No. 2018-13.For fair value measurements categorized within Level 3 of the fair value hierarchy, this Topic requires a reporting entity to disclose a description of the valuation processes used by the reporting entity. A reporting entity might disclose the following to comply with paragraph 820-10-50-2(f):

a. For the group within the reporting entity that decides the reporting entity’s valuation policies and procedures:

2. To whom that group reports

3. The internal reporting procedures in place (for example, whether and, if so, how pricing, risk management, or audit committees discuss and assess the fair value measurements).

b. The frequency and methods for calibration, back testing, and other testing procedures of pricing models.

c. The process for analyzing changes in fair value measurements from period to period.

d. How the reporting entity determined that third-party information, such as broker quotes or pricing services, used in the fair value measurement was developed in accordance with this Topic.

e. The methods used to develop and substantiate the unobservable inputs used in a fair value measurement.

> > > > Information about Uncertainty of Fair Value Measurements Sensitivity to Changes in Significant Unobservable Inputs

820-10-55-106 For recurring fair value measurements categorized within Level 3 of the fair value hierarchy, this Topic requires a reporting entity to provide a narrative description of the

uncertainty sensitivity

of the fair value measurement

to changes in

at the reporting date from the use of significant unobservable

inputs

inputs, if those inputs reasonably could have been different at the reporting date, and a description of any interrelationships

between those

among the unobservable inputs

used in the fair value measurement, which might magnify or mitigate the effect of changes in the unobservable inputs on the fair value measurement. A reporting entity might disclose the following about its residential mortgage-backed securities to comply with paragraph 820-10-50-2(g).

The significant unobservable inputs used in the fair value measurement of the reporting entity’s residential mortgage-backed securities are prepayment rates, probability of default, and loss severity in the event of default. Significant increases (decreases) in any of those inputs in isolation would

result

have resulted in a significantly lower (higher) fair value measurement. Generally, a change in the assumption used for the probability of default

is

would have been accompanied by a directionally similar change in the assumption used for the loss severity and a directionally opposite change in the assumption used for prepayment rates.

> > > Case D: Disclosure—Fair Value Measurements of Investments That Are Measured at Net Asset Value per Share (or Its Equivalent) as a Practical Expedient

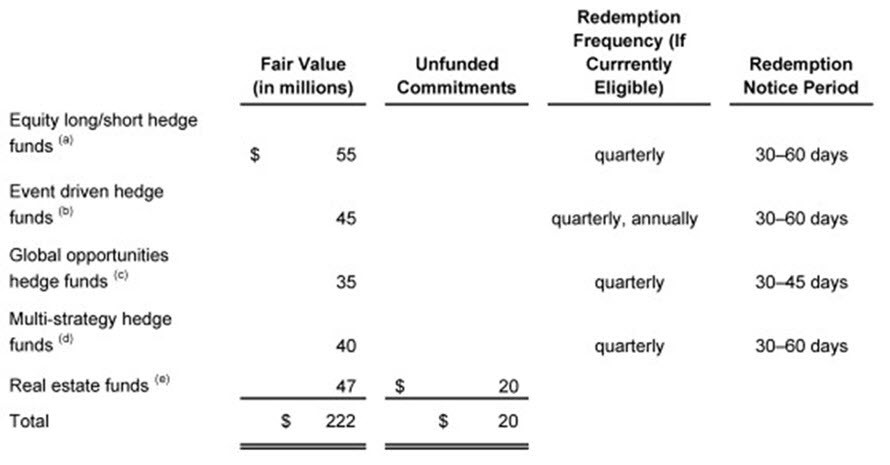

820-10-55-107 For investments that are within the scope of paragraphs 820-10-15-4 through 15-5 and that are measured at fair value using net asset value per share as a practical expedient, this Topic requires a reporting entity to disclose information that helps users to understand the nature, characteristics, and risks of the investments by class and whether the investments, if sold, are probable of being sold at amounts different from net asset value per share (or its equivalent, such as member units or an ownership interest in partners’ capital to which a proportionate share of net assets is attributed) (see paragraph 820-10-50-6A).

That information may be presented as follows. (The classes presented below are provided as examples only and are not intended to be treated as a template. The classes disclosed should be tailored to the nature, characteristics, and risks of the reporting entity’s investments.)

a. This class includes investments in hedge funds that invest both long and short primarily in U.S. common stocks. Management of the hedge funds has the ability to shift investments from value to growth strategies, from small to large capitalization stocks, and from a net long position to a net short position. The fair values of the investments in this class have been estimated using the net asset value per share of the investments. Investments representing approximately 22 percent of the value of the investments in this class cannot be redeemed because the investments include restrictions that do not allow for redemption in the first 12 to 18 months after acquisition. The remaining restriction period for these investments ranged from three to seven months at December 31, 20X3.

b. This class includes investments in hedge funds that invest in approximately 60 percent equities and 40 percent bonds to profit from economic, political, and government driven events. A majority of the investments are targeted at economic policy decisions. The fair values of the investments in this class have been estimated using the net asset value per share of the investments.

c. This class includes investments in hedge funds that hold approximately 80 percent of the funds’ investments in non-U.S. common stocks in the healthcare, energy, information technology, utilities, and telecommunications sectors and approximately 20 percent of the funds’ investments in diversified currencies. The fair values of the investments in this class have been estimated using the net asset value per share of the investments. For one investment, valued at $8.75 million, a gate has been imposed by the hedge fund manager and no redemptions are currently permitted. This redemption restriction has been in place for six months and the time at which the redemption restriction might lapse

is unknown cannot be estimated.

d. This class invests in hedge funds that pursue multiple strategies to diversify risks and reduce volatility. The hedge funds’ composite portfolio for this class includes investments in approximately 50 percent U.S. common stocks, 30 percent global real estate projects, and 20 percent arbitrage investments. The fair values of the investments in this class have been estimated using the net asset value per share of the investments. Investments representing approximately 15 percent of the value of the investments in this class cannot be redeemed because the investments include restrictions that do not allow for redemption in the first year after acquisition. The remaining restriction period for these investments ranged from four to six months at December 31, 20X3.

e. This class includes several real estate funds that invest primarily in U.S. commercial real estate. The fair values of the investments in this class have been estimated using the net asset value of the Company’s ownership interest in partners’ capital. These investments can never be redeemed with the funds. Distributions from each fund will be received as the underlying investments of the funds are liquidated.

It is estimated that the underlying assets of the fund will be liquidated over the next 7 to 10 years.

Twenty percent of the total investment in this class is planned to be sold

within the next three years. However, the individual investments that will be sold have not yet been determined. Because it is not probable that any individual investment will be sold, the fair value of each individual investment has been estimated using the net asset value of the Company’s ownership interest in partners’ capital. Once it has been determined which investments will be sold and whether those investments will be sold individually or in a group, the investments will be sold in an auction process. The investee fund’s management must approve of the buyer before the sale of the investments can be completed.

f. Footnote superseded by Accounting Standards Update No. 2015-07.

4. Add paragraph 820-10-65-12 and its related heading as follows:

Transition and Open Effective Date Information

> Transition Related to Accounting Standards Update No. 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement

820-10-65-12 The following represents the transition and effective date information related to Accounting Standards Update No. 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement:

a. The pending content that links to this paragraph shall be effective for all entities for fiscal years, and interim periods within those years, beginning after December 15, 2019.

b. An entity shall apply the pending content that links to this paragraph retrospectively to all periods presented, except for the changes in unrealized gains and losses required by paragraph 820-10-50-2(d), the range and weighted-average disclosure required by paragraph 820-10-50-2(bbb)(2)(i), and the narrative description of measurement uncertainty in accordance with paragraph 820-10-50-2(g) that are required to be applied prospectively for only the most recent interim or annual period presented in the initial fiscal year of adoption.

c. Early adoption of the pending content that links to this paragraph is permitted (an entity is permitted to early adopt the removed or modified disclosures in paragraph 820-10-50-2(bb), (c)(3), (f), and (g), paragraph 820-10-50-2G, and paragraph 820-10-50-6A(b) and (e) and adopt the additional disclosures in paragraph 820-10-50-2(bbb)(2)(i) and (d) upon their effective date), including adoption in any interim period for:

1. Public business entities for periods in which financial statements have not yet been issued

2. All other entities for periods in which financial statements have not yet been made available for issuance.