2. Amend paragraph 715-20-50-1, with a link to transition paragraph 715-20-65-4, as follows: [Note: Only the portion of this paragraph that is relevant to the amendments is shown here.]

Compensation—Retirement Benefits—Defined Benefit Plans—General

Disclosure

> Disclosures by Public Entities

715-20-50-1 An employer that sponsors one or more defined benefit pension plans or one or more defined benefit other postretirement plans shall provide the following information, separately for pension plans and other postretirement benefit plans. Amounts related to the employer’s results of operations shall be disclosed for each period for which a statement of income is presented. Amounts related to the employer’s statement of financial position shall be disclosed as of the date of each statement of financial position presented. All of the following shall be disclosed:

k. On a weighted-average basis, all of the following assumptions used in the accounting for the plans, specifying in a tabular format, the assumptions used to determine the benefit obligation and the assumptions used to determine net benefit cost:

1.

Discount Assumed discount

rates (see paragraph 715-30-35-45 for a discussion of representationally faithful disclosure)

2. Rates of compensation increase (for pay-related plans)

3. Expected long-term rates of return on plan assets.

4. Interest crediting rates (for cash balance plans and other plans with promised interest crediting rates).

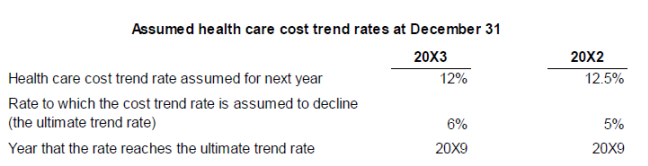

l. The assumed health care cost trend rate(s) for the next year used to measure the expected cost of benefits covered by the plan (gross eligible charges), and a general description of the direction and pattern of change in the assumed trend rates thereafter, together with the ultimate trend rate(s) and when that rate is expected to be achieved.

m.

Subparagraph superseded by Accounting Standards Update No. 2018-14.The effect of a one-percentage-point increase and the effect of a onepercentage-point decrease in the assumed health care cost trend rates on the aggregate of the service and interest cost components of net periodic postretirement health care benefit costs and the accumulated postretirement benefit obligation for health care benefits. Measuring the sensitivity of the accumulated postretirement benefit obligation and the combined service and interest cost components to a change in the assumed health care cost trend rates requires remeasuring the accumulated postretirement benefit obligation as of the beginning and end of the year. (For purposes of this disclosure, all other assumptions shall be held constant, and the effects shall be measured based on the substantive plan that is the basis for the accounting.)

n. If applicable, the amounts and types of securities of the employer and

related parties included in plan assets,

the approximate amount of future annual benefits of plan participants covered by insurance contracts, including annuity contracts issued by the employer or related parties, and any significant transactions between the employer or related parties and the plan during the period.

r. An explanation of

the following information:any significant change in the benefit obligation or plan assets not otherwise apparent in the other disclosures required by this Subtopic.

1. The reasons for significant gains and losses related to changes in the defined benefit obligation for the period

2. Any other significant change in the benefit obligation or plan assets not otherwise apparent in the other disclosures required by this Subtopic.

s.

Subparagraph superseded by Accounting Standards Update No. 2018-14.

The amounts in accumulated other comprehensive income expected to be recognized as components of net periodic benefit cost over the fiscal year that follows the most recent annual statement of financial position presented, showing separately the net gain or loss, net prior service cost or credit, and net transition asset or obligation.

t.

Subparagraph superseded by Accounting Standards Update No. 2018-14.The amount and timing of any plan assets expected to be returned to the employer during the 12-month period, or operating cycle if longer, that follows the most recent annual statement of financial position presented.

3. Amend paragraph 715-20-50-3, with a link to transition paragraph 715-20-65-4, as follows:

> Entities (Public and Nonpublic) with Two or More Plans

715-20-50-2 The disclosures required by this Subtopic shall be aggregated for all of an employer’s defined benefit pension plans and for all of an employer’s other defined benefit postretirement plans unless disaggregating in groups is considered to provide useful information or is otherwise required by the following paragraph and paragraph 715-20-50-4.

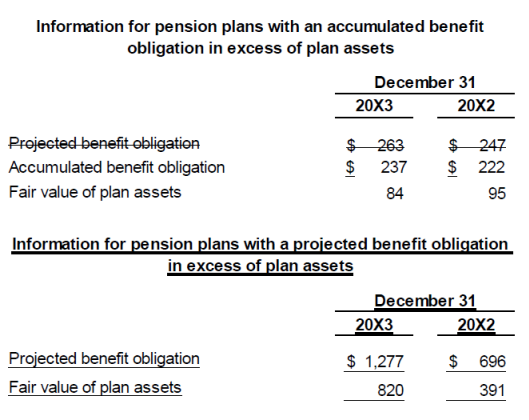

715-20-50-3 Disclosures about pension plans with assets in excess of the accumulated benefit obligation generally may be aggregated with disclosures about pension plans with accumulated benefit obligations in excess of assets. The same aggregation is permitted for other postretirement benefit plans.

If aggregate disclosures are presented, an employer shall disclose,

as of the date of each statement of financial position presented, both of the following:

a.

For pension plans, the projected benefit obligation and fair value of plan assets for plans with projected benefit obligations in excess of plan assets, and the accumulated benefit obligation and fair value of plan assets for plans with accumulated benefit obligations in excess of plan assets The aggregate benefit obligation and aggregate fair value of plan assets for plans with benefit obligations in excess of plan assets as of the measurement date of each statement of financial position presented

b.

For other postretirement benefit plans, the accumulated postretirement benefit obligation and fair value of plan assets for plans with accumulated postretirement benefit obligations in excess of plan assets The aggregate pension accumulated benefit obligation and aggregate fair value of plan assets for pension plans with accumulated benefit obligations in excess of plan assets.

715-20-50-4 A U.S. reporting entity may combine disclosures about pension plans or other postretirement benefit plans outside the United States with those for U.S. plans unless the benefit obligations of the plans outside the United States are significant relative to the total benefit obligation and those plans use significantly different assumptions. A foreign reporting entity that prepares financial statements in conformity with U.S. generally accepted accounting principles (GAAP) shall apply the preceding guidance to its domestic and foreign plans.

4. Amend paragraph 715-20-50-5, with a link to transition paragraph 715-20-65-4, as follows: [Note: Only the portion of this paragraph that is relevant to the amendments is shown here.]

> Disclosures by Nonpublic Entities

715-20-50-5 A

nonpublic entity is not required to disclose the information required by paragraph 715-20-50-1(a) through (c), 715-20-50-1(h),

715-20-50-1(m), and

715-20-50-1(o) through

(r)

(q), and 715-20-50-1(r)(2). A nonpublic entity that sponsors one or more defined benefit pension plans or one or more other defined benefit postretirement plans shall provide all of the following information, separately for pension plans and other postretirement benefit plans. Amounts related to the employer’s results of operations shall be disclosed for each period for which a statement of income is presented. Amounts related to the employer’s statement of financial position shall be disclosed as of the date of each statement of financial position presented.

c. The objectives of the disclosures about postretirement benefit plan assets are to provide users of financial statements with an understanding of:

1. How investment allocation decisions are made, including the factors that are pertinent to an understanding of investment policies and strategies

2. The classes of plan assets

3. The inputs and valuation techniques used to measure the fair value of plan assets

4. The effect of fair value measurements using significant unobservable inputs (Level 3) on changes in plan assets for the period

5. Significant concentrations of risk within plan assets.

An employer shall consider those overall objectives in providing the following information about plan assets:

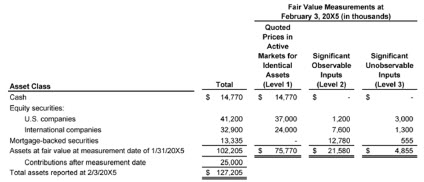

ii. The fair value of each class of plan assets as of each date for which a statement of financial position is presented. For additional guidance on determining appropriate classes of plan assets, see paragraph 820-10-50-2B. Examples of classes of assets could include, but are not limited to, the following: cash and cash equivalents; equity securities (segregated by industry type, company size, or investment objective); debt securities issued by national, state, and local governments; corporate debt securities; asset-backed securities; structured debt; derivatives on a gross basis (segregated by type of underlying risk in the contract, for example, interest rate contracts, foreign exchange contracts, equity contracts, commodity contracts, credit contracts, and other contracts); investment funds (segregated by type of fund); and real estate. Those examples are not meant to be all inclusive. An employer should consider the overall objectives in paragraph 715-20-50-5(c)(1) through (5) in determining whether additional classes of plan assets or further disaggregation of classes should be disclosed. If an employer determines the measurement date of plan assets in accordance with paragraph 715-30-35-63A or 715-60-35-123A and the employer contributes assets to the plan between the measurement date and its fiscal year-end, the employer shall not adjust the fair value of each class of plan assets for the effects of the contribution. Instead, the employer shall disclose the amount of the contribution to permit reconciliation of the total fair value of all the classes of plan assets to the ending balance of the fair value of plan assets. For example, the contribution could be disclosed as follows:

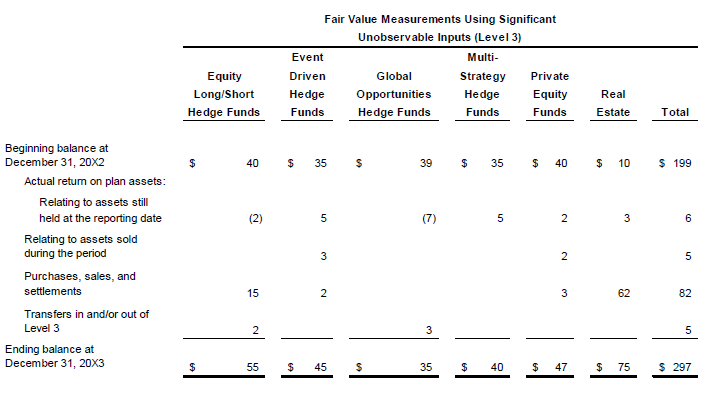

iv. Information that enables users of financial statements to assess the inputs and valuation techniques used to develop fair value measurements of plan assets at the reporting date. For fair value measurements using significant unobservable inputs, an employer shall disclose the effect of the measurements on changes in plan assets for the period. To meet those objectives, the employer shall disclose the following information for each class of plan assets disclosed pursuant to (ii) above for each annual period:

02. For fair value measurements of plan assets using significant unobservable inputs (Level 3),

the amounts of purchases and any transfers into or out of Level 3 (for example, transfers due to changes in the observability of significant inputs), disclosed separately.a reconciliation from the opening balances to the closing balances, disclosing separately changes during the period attributable to the following:

A.

Subparagraph superseded by Accounting Standards Update No. 2018-14. Actual Return on Plan Assets (Component of Net Periodic Postretirement Benefit Cost) or Actual Return on Plan Assets (Component of Net Periodic Pension Cost), separately identifying the amount related to assets still held at the reporting date and the amount related to assets sold during the period

B.

Subparagraph superseded by Accounting Standards Update No. 2018-14.Purchases, sales, and settlements, net

C.

Subparagraph superseded by Accounting Standards Update No. 2018-14.The amounts of any transfers into or out of Level 3 (for example, transfers due to changes in the observability of significant inputs).

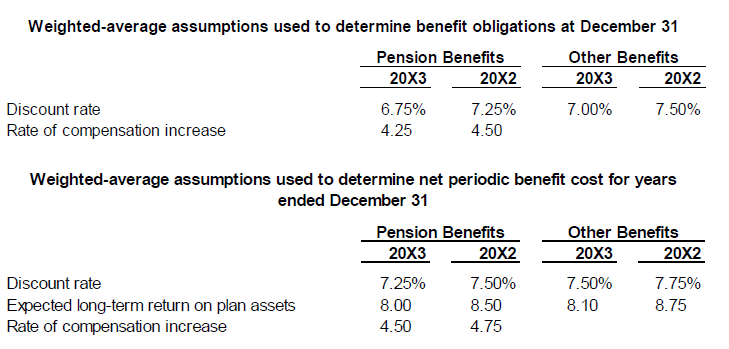

j. On a weighted-average basis, all of the following assumptions used in the accounting for the plans, specifying in a tabular format, the assumptions used to determine the benefit obligation and the assumptions used to determine net benefit cost:

1.

Discount Assumed discount

rates (see paragraph 715-30-35-45 for a discussion of representationally faithful disclosure)

2. Rates of compensation increase (for pay-related plans)

3. Expected long-term rates of return on plan assets.

4. Interest crediting rates (for cash balance plans and other plans with promised interest crediting rates).

l. If applicable, the amounts and types of securities of the employer and related parties included in plan assets,

the approximate amount of future annual benefits of plan participants covered by insurance contracts, including annuity contracts, issued by the employer or related parties, and any significant transactions between the employer or related parties and the plan during the period.

n.

Subparagraph superseded by Accounting Standards Update No. 2018-14. The amounts in accumulated other comprehensive income expected to be recognized as components of net periodic benefit cost over the fiscal year that follows the most recent annual statement of financial position presented, showing separately the net gain or loss, net prior service cost or credit, and net transition asset or obligation.

o.

Subparagraph superseded by Accounting Standards Update No. 2018-14. The amount and timing of any plan assets expected to be returned to the employer during the 12-month period, or operating cycle if longer, that follows the most recent annual statement of financial position presented.

r. An explanation of the reasons for significant gains and losses related to changes in the benefit obligation for the period.

5. Supersede paragraphs 715-20-50-9 through 50-10 and their related heading, with a link to transition paragraph 715-20-65-4, as follows:

> Disclosures Related to Japanese Governmental Settlement Transactions

715-20-50-9 Paragraph superseded by Accounting Standards Update No. 2018-14.See paragraphs 715-30-55-69 through 55-79 for guidance on the accounting for Japanese governmental settlement transactions.

715-20-50-10 Paragraph superseded by Accounting Standards Update No. 2018-14.The required disclosures for the separation of the substitutional portion of the benefit obligation from the corporate portion of the benefit obligation in a Japanese Employee Pension Fund arrangement and the transfer of the substitutional portion and related assets to the Japanese government pursuant to the June 2001 Japanese Welfare Pension Insurance Law amendment are as follows:

a. The difference between the obligation settled and the assets transferred to the government, determined pursuant to the government formula, shall be disclosed separately as a subsidy from the government pursuant to applicable GAAP.

b. The derecognition of previously accrued salary progression at the time of settlement, pursuant to this consensus, shall be disclosed separately from the government subsidy.

6. Amend paragraphs 715-20-55-15 through 55-17, with a link to transition paragraph 715-20-65-4, as follows:

Implementation Guidance and Illustrations

> Illustrations

715-20-55-15 The financial statements of a nonpublic entity would be similarly presented but would not be required to include the information contained in paragraph 715-20-50-1(a) through (c), 715-20-50-1(h),

715-20-50-1(m), and

715-20-50-1(o) through

(r)

(q), and 715-20-50-1(r)(2). The items presented in these Examples have been included for illustrative purposes. Certain assumptions have been made to simplify the computations and focus on the disclosure requirements.

> > Example 1: Disclosures about Defined Benefit Pension and Other Postretirement Benefit Plans in the Annual Financial Statements of a Publicly Traded Entity

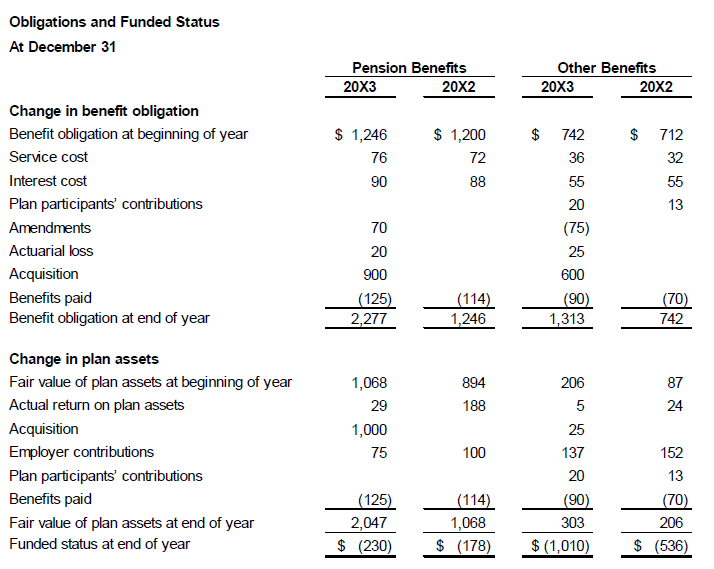

715-20-55-16 The following illustrates the fiscal 20X3 financial statement disclosures for an employer (Entity A) with multiple defined benefit pension plans and other postretirement benefit plans (dollar amounts in millions). This Example assumes that Entity A does not have cash balance plans or other plans with promised interest crediting rates. Narrative descriptions of the basis used to determine the overall expected long-term rate-of-return-on-assets assumption (see paragraph 715-20-50-1(d)(iii)) and disclosure of the valuation technique(s) and inputs used to measure the fair value of plan assets and a discussion of changes in valuation techniques and inputs (see paragraph 715-20-50-1(d)(iv)(03)), if any, are not included in this Example. The narrative description of the basis used to determine the overall expected long-term rate-of-return-onassets assumption is meant to be entity-specific. An explanation of the reasons for significant gains and losses related to changes in the benefit obligation for the period (see paragraph 715-20-50-1(r)(1)), if any, is not provided in this Example because the reasons may vary in different reporting periods or in different entities. For purposes of this Example, the disclosures required by paragraphs 715-20-50-1(d)(ii) and 715-20-50-1(d)(iv) are provided for only the fiscal year ending December 31, 20X3. However, those paragraphs indicate that the disclosures are required to be presented as of each date for which a statement of financial position is presented.

715-20-55-17 During 20X3, Entity A acquired FV Industries and amended its plans. Entity A would make the following disclosure.

Notes to Financial Statements

Pension and Other Postretirement Benefit Plans

[Note: Only the portion of this paragraph that is relevant to the amendments is shown here.]

Entity A has both funded and unfunded noncontributory defined benefit pension plans that together cover substantially all of its employees. The plans provide defined benefits based on years of service and final average salary.

Entity A also has both funded and unfunded other postretirement benefit plans covering substantially all of its employees. The health care plans are contributory with participants’ contributions adjusted annually; the life insurance plans are noncontributory. The accounting for the health care plans anticipates future cost-sharing changes to the written plans that are consistent with the entity’s expressed intent to increase retiree contributions each year by 50 percent of health care cost increases in excess of 6 percent. The postretirement health care plans include a limit on the entity’s share of costs for recent and future retirees.

Entity A acquired FV Industries on December 27, 20X3, including its pension plans and other postretirement benefit plans. Amendments made at the end of 20X3 to Entity A’s plans increased the pension benefit obligations by $70 and reduced the other postretirement benefit obligations by $75.

[Note: Nonpublic entities are not required to provide information in the preceding tables; they are required to disclose the employer’s contributions, participants’ contributions, benefit payments, and the funded status.]

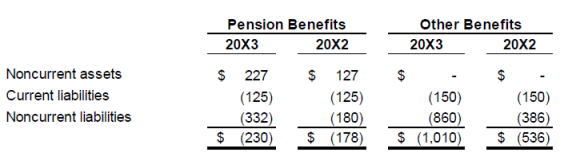

Amounts recognized in the statement of financial position consist of the following.

[Note: The sum of current liabilities and noncurrent liabilities consists of the amount of underfunded (including unfunded) pension benefits or other benefits.]

The accumulated benefit obligation for all defined benefit pension plans was $1,300 and $850 at December 31, 20X3, and 20X2, respectively.

[Note: The net amount of projected benefit obligation and plan assets for all underfunded (including unfunded) pension plans was $457 and $305 at December 31, 20X3, and 20X2, respectively, and was classified as liabilities on the statement of financial position.]

[Note: Information for other postretirement benefit plans with an accumulated postretirement benefit obligation in excess of plan assets has been disclosed in the note on “Obligations and Funded Status” because all the other postretirement benefit plans are unfunded or underfunded.]

The components of net periodic benefit cost other than the service cost component are included in the line item “other income/(expense)” in the income statement.

The estimated net loss and prior service cost for the defined benefit pension plans that will be amortized from accumulated other comprehensive income into net periodic benefit cost over the next fiscal year are $4 and $27, respectively. The estimated prior service credit for the other defined benefit postretirement plans that will be amortized from accumulated other comprehensive income into net periodic benefit cost over the next fiscal year is $10.

[Note: Nonpublic entities are not required to separately disclose components of net periodic benefit cost.]

[Entity-specific narrative description of the reasons for significant gains and losses related to changes in the defined benefit obligation for the period would be disclosed.]

Assumptions

[Entity-specific narrative description of the basis used to determine the overall expected long-term rate of return on assets, as described in paragraph 715-20-50-1(d)(iii), would be

disclosed included here.]

[An entity with cash balance plans or other plans with promised interest crediting rates would disclose the weighted-average interest crediting rates used to determine the benefit obligation and net periodic benefit cost.]

Assumed health care cost trend rates have a significant effect on the amounts reported for the health care plans. A one-percentage-point change in assumed health care cost trend rates would have the following effects.

[Note: Nonpublic entities are not required to provide the information about the impact of a one-percentage-point increase and one-percentage-point decrease in the assumed health care cost trend rates.]

Plan Assets

[Note: An entity shall disclose the following information regardless of its method for disclosing classes of plan assets.]

Note: Nonpublic entities are not required to provide a reconciliation from the opening balances to the closing balances of plan assets measured on a recurring basis in Level 3 of the fair value hierarchy. However, nonpublic entities are required to disclose separately the amounts of purchases of Level 3 plan assets and transfers into and out of Level 3 of the fair value hierarchy.]

7. Add paragraph 715-20-65-4 and its related heading as follows:

Transition and Open Effective Date Information

> Transition Related to Accounting Standards Update No. 2018-14, Compensation—Retirement Benefits—Defined Benefit Plans—General (Subtopic 715-20): Disclosure Framework—Changes to the Disclosure Requirements for Defined Benefit Plans

715-20-65-4 The following represents the transition and effective date information related to Accounting Standards Update No. 2018-14, Compensation—Retirement Benefits—Defined Benefit Plans—General (Subtopic 715-20): Disclosure Framework—Changes to the Disclosure Requirements for Defined Benefit Plans:

a. The pending content that links to this paragraph shall be effective as follows:

1. For public business entities, for financial statements issued for fiscal years ending after December 15, 2020

2. For all other entities, for financial statements issued for fiscal years ending after December 15, 2021.

b. An entity shall apply the pending content that links to this paragraph retrospectively to all periods presented.

c. Early adoption of the pending content that links to this paragraph is permitted.