13. Amend paragraph 740-270-25-5, with a link to transition paragraph 740-10-65-8, as follows:

Income Taxes—Interim Reporting

Recognition

> General Recognition Approach

740-270-25-5 The effects of new tax legislation shall not be recognized prior to enactment. The tax effect of a change in tax laws or rates on taxes currently payable or refundable for the current year shall be

recorded after the effective dates prescribed in the statutes and

reflected in the computation of the annual effective tax rate beginning

no earlier than

in the first interim period that includes the enactment date of the new legislation. The effect of a change in tax laws or rates on a

deferred tax liability or asset shall not be apportioned among interim periods through an adjustment of the annual effective tax rate.

14. Amend paragraphs 740-270-30-11, 740-270-30-28, and 740-270-30-34, with a link to transition paragraph 740-10-65-8, as follows:

Initial Measurement

> Exclusion of Items from Estimated Annual Effective Tax Rate

> > Items Always Excluded from Estimated Annual Effective Tax Rate

740-270-30-11 The effects of changes in judgment about beginning-of-year valuation allowances and effects of changes in tax laws or rates

on deferred tax assets or liabilities and taxes payable or refundable for prior years (in the case of a retroactive change) shall be excluded from the estimated annual effective tax rate calculation.

See paragraph 740-270-25-5 for requirements related to when the estimated annual effective tax rate shall be adjusted to reflect changes in tax laws and rates that affect current year taxes payable or refundable.

> Effect of Operating Losses

> > Year-to-Date Ordinary Loss; Anticipated Ordinary Loss for the Year

740-270-30-28 If an entity has an ordinary loss for the year to date at the end of an interim period and anticipates an ordinary loss for the fiscal year, the interim period tax benefit shall be computed in accordance with paragraph 740-270-30-5. The estimated tax benefit for the fiscal year, used to determine the estimated annual effective tax rate described in paragraphs 740-270-30-6 through 30-8, shall not exceed the tax benefit determined in accordance with paragraphs 740-270-30-30 through 30-33.

In addition to that limitation in the effective rate computation, if the year-to-date ordinary loss exceeds the anticipated ordinary loss for the fiscal year, the tax benefit recognized for the year to date shall not exceed the tax benefit determined, based on the year-to-date ordinary loss, in accordance with paragraphs 740-270-30-30 through 30-33.

> Determining Income Tax Benefit Limitations

740-270-30-34 See Example 2, Cases A1

and A2; B

, C1

;

and C1 and C2 (paragraphs 740-270-55-15

through 55-17; 740-270-55-17;

and 740-270-55-19 through 55-20) for illustrations of computations involving operating losses, and Example 1, Cases B2 and B3 (see paragraphs 740-270-55-7 through 55-8)

, and Example 2, Case A2 (see paragraph 740-270-55-16)

for illustrations of special year-to-date limitation computations.

15. Amend paragraphs 740-270-55-16, 740-270-55-44 through 55-45 and the related heading, and 740-270-55-49 and supersede paragraphs 740-270-55-50 through 55-51 and their related heading, with a link to transition paragraph 740-10-65-8, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Example 2: Accounting for Income Taxes Applicable to Ordinary Income (or Loss) at an Interim Date If an Ordinary Loss Is Anticipated for the Fiscal Year

> > > Case A: Realization of the Tax Benefit of the Loss Is More Likely Than Not

> > > > Case A2: Ordinary Income and Losses in Interim Periods

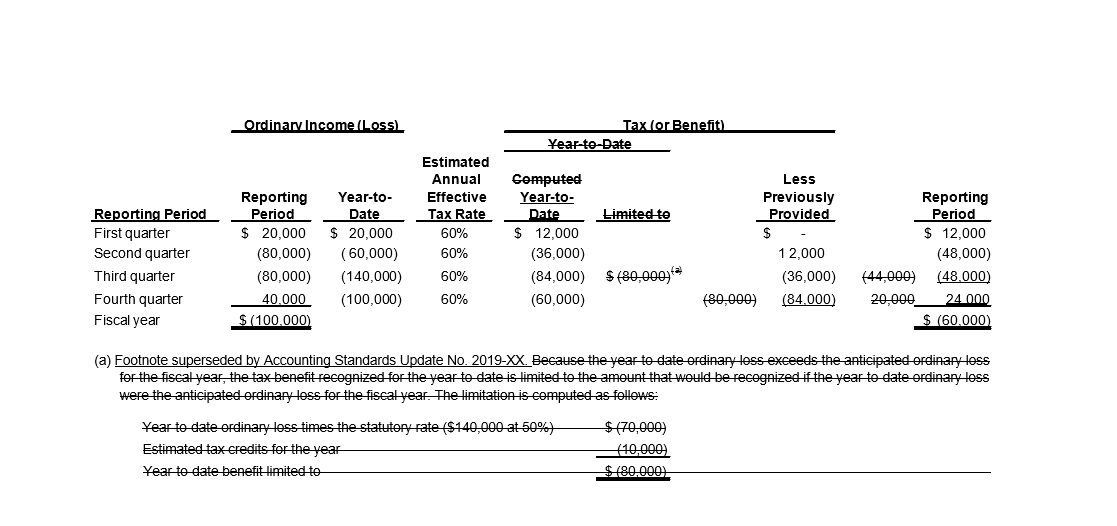

740-270-55-16 The entity has ordinary income and losses in interim periods and for the year to date. The full tax benefit of the anticipated ordinary loss and the anticipated tax credits will be realized by carryback. The full tax benefit of the maximum year-to-date ordinary loss can also be realized by carryback. Quarterly tax computations are as follows.

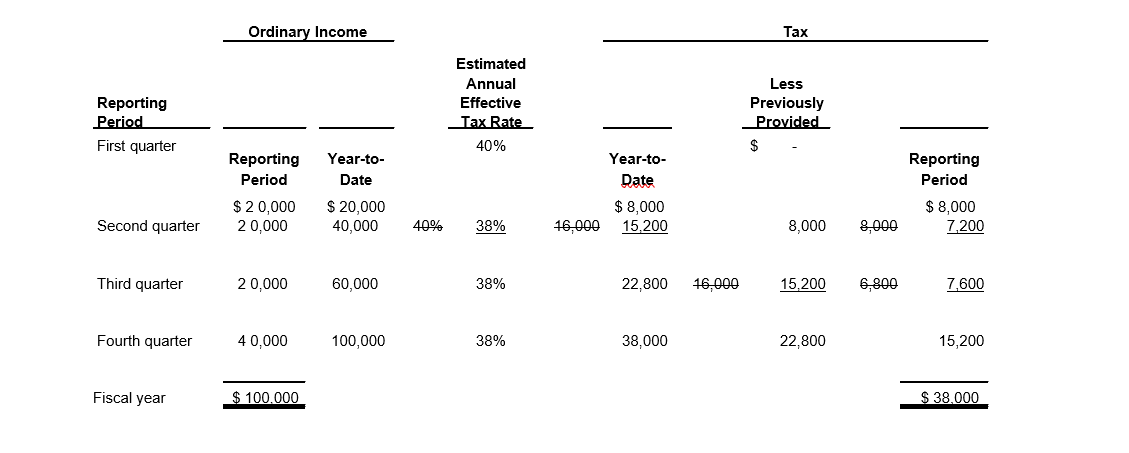

> > Example 6: Effect of New Tax Legislation

740-270-55-44 The following

Cases illustrate

Example illustrates the guidance in paragraphs 740-270-25-5 through 25-6 for accounting in interim periods for the effect of new tax legislation on income

taxes:

taxes when legislation is effective in a future interim period.

- Subparagraph superseded by Accounting Standards Update No. 2019- 12.

Legislation effective in a future interim period (Case A)

- Subparagraph superseded by Accounting Standards Update No. 2019- 12.

Effective date of new legislation (Case B).

> > > Case A:

Legislation Effective in a Future Interim Period 740-270-55-45 The assumed facts applicable to this

Case

Example follow.

740-270-55-46 For the full fiscal year, an entity anticipates ordinary income of $100,000. All income is taxable in one jurisdiction at a 50 percent rate. Anticipated tax credits for the fiscal year total $10,000. No events that do not have tax consequences are anticipated.

740-270-55-47 Computation of the estimated annual effective tax rate applicable to ordinary income is as follows.

Tax at statutory rate ($100,000 at 50%)

| |

Less anticipated tax credits

| |

|

Estimated annual effective tax rate ($40,000 ÷ $100,000)

| |

740-270-55-48 Further, assume that new legislation creating additional tax credits is enacted during the second quarter of the entity’s fiscal year. The new legislation is effective on the first day of the third quarter. As a result of the estimated effect of the new legislation, the entity revises its estimate of its annual effective tax rate to the following.

Tax at statutory rate ($100,000 at 50%)

| |

Less anticipated tax credits

| |

|

Estimated annual effective tax rate ($38,000 ÷ $100,000)

| |

740-270-55-49 The effect of the new legislation shall

not

be reflected

until it is effective or administratively effective

in the computation of the annual effective tax rate beginning in the first interim period that includes the enactment date of the new legislation. Accordingly, quarterly tax computations are as follows.

> > > Case B: Effective Date of New Legislation

740-270-55-50 Paragraph superseded by Accounting Standards Update No.2019-12.Legislation generally becomes effective on the date prescribed in the statutes. However, tax legislation may prescribe changes that become effective during an entity’s fiscal year that are administratively implemented by applying a portion of the change to the full fiscal year. For example, if the statutory tax rate applicable to calendar-year corporations were increased from 48 to 52 percent, effective January 1, the increased statutory rate might be administratively applied to a corporation with a fiscal year ending at June 30 in the year of the change by applying a 50 percent rate to its

taxable income

for the fiscal year, rather than 48 percent for the first 6 months and 52 percent for the last 6 months. In that case the legislation becomes effective for that entity at the beginning of the entity’s fiscal year.

740-270-55-51 Paragraph superseded by Accounting Standards Update No.2019-12.Applying this to specific legislation, an entity with a fiscal year other than a calendar year would account during interim periods for the reduction in the corporate tax rate resulting from the Revenue Act of 1978 through a revised annual effective tax rate calculation in the same way that the change will be applied to the entity’s taxable income for the year. The revised annual effective tax rate would then be applied to pretax income for the year to date at the end of the current interim period.