2. Add Subtopic 848-10 as follows:

[For ease of readability, the new Subtopic is not underlined.]

Reference Rate Reform—Overall

Overview and Background

General

848-10-05-1 The Reference Rate Reform Topic includes the following Subtopics:

- Overall

- Contract Modifications

- Hedging—General

- Fair Value Hedges

- Cash Flow Hedges.

848-10-05-2 Reference rates such as the London Interbank Offered Rate (LIBOR) are widely used in a broad range of financial instruments and other agreements. Regulators and market participants in various jurisdictions have undertaken efforts, generally referred to as reference rate reform, to eliminate certain reference rates and introduce new reference rates that are based on a larger and more liquid population of observable transactions. As a result of the reference rate reform initiative, certain widely used reference rates such as LIBOR are expected to be discontinued.

848-10-05-3 This Topic provides optional expedients for applying the guidance in certain Topics or Industry Subtopics for contract modifications or other situations affected by reference rate reform. The guidance in this Topic is temporary in accordance with the guidance in paragraph 848-10-65-1(a).

Scope and Scope Exceptions

General

> Overall Guidance

848-10-15-1 The Scope and Scope Exceptions Section of the Overall Subtopic establishes the pervasive scope for the Reference Rate Reform Topic. Unless explicitly addressed within the specific Subtopics, the following guidance applies to all Subtopics of the Reference Rate Reform Topic.

> Entities

848-10-15-2 The guidance in this Topic applies to all entities.

> Scope

848-10-15-3 The guidance in this Topic, if elected by an entity, shall apply to contracts or other transactions that reference the London Interbank Offered Rate (LIBOR) or a reference rate that is expected to be discontinued as a result of reference rate reform.

> > Identifying an Eligible Reference Rate

848-10-15-4 The guidance in this Topic applies to all maturities of LIBOR in all jurisdictions and currencies. For other reference rates, an expectation of the discontinuance of the rate may result from any of the following:

- A public statement or publication of information by or on behalf of the administrator of the relevant reference rate or by the regulatory supervisor for the administrator

- Initiatives by a significant number of market participants or by market participants representing a significant number of transactions to move away from the reference rate

- The production method for the calculation of the published reference rate that is either:

- Fundamentally restructured

- Reliant on another rate that is expected to discontinue.

Glossary

Financial Statements Are Available to Be Issued

Financial statements are considered available to be issued when they are complete in a form and format that complies with GAAP and all approvals necessary for issuance have been obtained, for example, from management, the board of directors, and/or significant shareholders. The process involved in creating and distributing the financial statements will vary depending on an entity’s management and corporate governance structure as well as statutory and regulatory requirements.

Subsequent Measurement

General

> Sale or Transfer from Held-to-Maturity Classification

848-10-35-1 An entity may make a one-time election to sell or transfer certain debt securities classified as held to maturity or to both sell and transfer certain debt securities classified as held to maturity to available for sale or trading. At the time of applying the one-time election, the entity may sell, transfer, or both sell and transfer debt securities classified as held to maturity that meet both of the following criteria:

- The debt securities reference a rate that meets the scope of paragraph 848-10-15-3.

- The debt securities were classified as held to maturity before January 1, 2020.

At the time of applying the one-time election, an entity is not required to transfer all its remaining debt securities classified as held to maturity that meet criteria (a) and (b). The one-time election to sell, transfer, or both sell and transfer debt securities classified as held to maturity may be made at any time, but no later than the date in paragraph 848-10-65-1(d).

848-10-35-2 An entity shall recognize the transfer of debt securities classified as held to maturity to available for sale or trading as of the date in the reporting period in which the entity makes its one-time election. The entity shall apply the measurement guidance for transfers of debt securities between categories in paragraphs 320-10-35-10 through 35-16. The sale or transfer, in and of itself, would not call into question the entity’s assertion at prior reporting dates that it had the intent and ability to hold to maturity those debt securities that continued to be classified as held to maturity in those prior periods.

Disclosure

General

848-10-50-1 An entity that has applied the one-time election to sell, transfer, or both sell and transfer debt securities classified as held to maturity in accordance with paragraphs 848-10-35-1 through 35-2 shall apply the disclosure requirements in paragraph 320-10-50-10 for the sale or transfer of debt securities classified as held to maturity.

Transition and Open Effective Date Information

General

> Transition Related to Accounting Standards Update No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting

848-10-65-1 The following represents the transition, end of application, and effective date information related to Accounting Standards Update No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting:

- The pending content that links to this paragraph shall be effective for all entities as of March 12, 2020 through December 31, 2022, as follows:

- An entity may elect to apply the pending content that links to this paragraph for contract modifications by Topic or Industry Subtopic as of any date from the beginning of an interim period that includes or is subsequent to March 12, 2020, or prospectively from a date within an interim period that includes or is subsequent to March 12, 2020, up to the date that the financial statements are available to be issued. Once elected for a Topic or an Industry Subtopic, the pending content that links to this paragraph shall be applied prospectively for all eligible contract modifications for that Topic or Industry Subtopic in accordance with paragraph 848-20-35-1.

- An entity may elect to apply the pending content that links to this paragraph to eligible hedging relationships existing as of the beginning of the interim period that includes March 12, 2020 and to new eligible hedging relationships entered into after the beginning of the interim period that includes March 12, 2020.

- If an entity elects to apply any of the pending content that links to this paragraph for an eligible hedging relationship existing as of the beginning of the interim period that includes March 12, 2020, any adjustments as a result of those elections shall be reflected as of the beginning of that interim period and recognized in accordance with Subtopics 848-30, 848-40, and 848-50 (as applicable). If an entity elects to apply any of the pending content that links to this paragraph for a new hedging relationship entered into between the beginning of the interim period that includes March 12, 2020 and March 12, 2020, any adjustments as a result of those elections shall be reflected as of the beginning of the hedging relationship and recognized in accordance with Subtopics 848-30, 848-40, and 848-50 (as applicable).

01. For private companies that are not financial institutions as described in paragraph 942-320-50-1 and not-for-profit entities (except for not-for-profit entities that have issued, or are a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market), an entity shall update its hedge documentation (as applicable) noting the changes made before the next interim (if applicable) or annual financial statements are available to be issued.

02. For all other entities, an entity shall update its hedge documentation (as applicable) noting the changes made no later than when the entity performs its first quarterly assessment of effectiveness after the election.

- The pending content that links to this paragraph shall not be applied to all the following:

- Contract modifications made after December 31, 2022.

- New hedging relationships entered into after December 31, 2022.

- Hedging relationships evaluated for periods after December 31, 2022, except for hedging relationships existing as of December 31, 2022, that apply the following optional expedients in Subtopics 848-30 and 848-40 that shall be retained through the end of the hedging relationship (including for periods evaluated after December 31, 2022):

01. An optional expedient to the systematic and rational method used to recognize in earnings the components excluded from the assessment of effectiveness in paragraph 848-30-25-12.

02. An optional expedient to the rate to discount cash flows associated with the hedged item and any adjustment to the cash flows for the designated term or the partial term of the designated hedged item in a fair value hedge in paragraph 848-40-25-6.

03. An optional expedient to not periodically evaluate the conditions in paragraph 815-20-25-104(d) and (g) when using the shortcut method for a fair value hedge in paragraph 848-40-25-8.

- An entity may elect the optional expedients in Subtopics 848-30, 848-40, and 848-50 if it has adopted the amendments in Accounting Standards Update No. 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities.

- An entity that has not adopted the amendments in Update 2017-12 may elect the following optional expedients in Subtopics 848-30, 848-40, and 848-50:

- An optional expedient allowing changes in critical terms of a hedging relationship in paragraphs 848-30-25-3 through 25-7.

- An optional expedient allowing a change to the method designated for use in assessing hedge effectiveness in a cash flow hedge in paragraph 848-30-25-8 if the optional expedient method being elected is the simplified hedge accounting approach for eligible private companies for initial hedge effectiveness in paragraph 848-50-25-8 or for subsequent hedge effectiveness in paragraph 848-50-35-7.

- An optional expedient allowing an entity to assume that the hedged forecasted transaction in a cash flow hedge is probable of occurring in paragraph 848-50-25-2.

- An optional expedient allowing an entity to assume that the reference rate will not be replaced for the remainder of the hedging relationships in paragraph 848-50-25-11(a) for initial hedge effectiveness and paragraph 848-50-35-17(a) for subsequent hedge effectiveness when the entity is using any of the methods for assessing and measuring hedge effectiveness in a cash flow hedge on a quantitative basis and if both the hedged forecasted transaction and the hedging instrument have a reference rate that meets the scope of paragraph 848-10-15-3.

- An optional expedient allowing an entity to disregard certain requirements of the simplified hedge accounting approach for eligible private companies for initial hedge effectiveness in paragraph 848-50-25-8 or for subsequent hedge effectiveness in paragraph 848-50-35-7 in a cash flow hedge.

- The one-time election to sell, transfer, or both sell and transfer debt securities classified as held to maturity in accordance with paragraphs 848-10-35-1 through 35-2 may be made at any time after March 12, 2020, but no later than December 31, 2022.

- An entity shall provide the following disclosures:

- The nature of and reason for electing to apply the pending content that links to this paragraph.

- The disclosures in (e)(1) in each interim and annual financial statement period in the fiscal year of application.

3. Add Subtopic 848-20 as follows:

[For ease of readability, the new Subtopic is not underlined.]

Reference Rate Reform—Contract Modifications

Overview and Background

General

848-20-05-1 This Subtopic provides optional expedients for contract modifications undertaken because of reference rate reform. It specifically addresses the accounting for modifications of contracts within the scope of Topics 310 on receivables, 470 on debt, and 840 and 842 on leases and Subtopic 815-15 on derivatives and hedging—embedded derivatives. This Subtopic also provides a principle to account for modifications of contracts within the scope of other Topics or Industry Subtopics not specifically addressed within this Subtopic.

Scope and Scope Exceptions

General

848-20-15-1 This Subtopic provides guidance on optional expedients for accounting for contract modifications when one or more terms are modified because of reference rate reform.

> Modifications of Terms

848-20-15-2 The guidance in this Subtopic, if elected, shall apply to contract modifications if the terms that are modified directly replace, or have the potential to replace, a reference rate within the scope of paragraph 848-10-15-3 with another interest rate index. If other terms are contemporaneously modified in a manner that changes, or has the potential to change, the amount or timing of contractual cash flows, the guidance in this Subtopic shall apply only if those modifications are related to the replacement of a reference rate. For example, the addition of contractual fallback terms or the amendment of existing contractual fallback terms related to the replacement of a reference rate that are contingent on one or more events occurring has the potential to change the amount or timing of contractual cash flows and the entity potentially would be eligible to apply the guidance in this Subtopic.

848-20-15-3 The guidance in this Subtopic shall not apply if a contract modification is made to a term that changes, or has the potential to change, the amount or timing of contractual cash flows and is unrelated to the replacement of a reference rate. That is, this Subtopic shall not apply if contract modifications are made contemporaneously to terms that are unrelated to the replacement of a reference rate.

848-20-15-4 Contemporaneous modifications of contract terms that do not change, or do not have the potential to change, the amount or timing of contractual cash flows shall not preclude application of the guidance in this Subtopic, regardless of whether those contemporaneous contract modifications are related or unrelated to the replacement of a reference rate.

> > Identifying Changes to Terms Related and Unrelated to the Replacement of the Reference Rate

848-20-15-5 Changes to terms that are related to the replacement of the reference rate are those that are made to effect the transition for reference rate reform and are not the result of a business decision that is separate from or in addition to changes to the terms of a contract to effect that transition. Examples of changes to terms that are related to the replacement of a reference rate in accordance with the guidance in paragraph 848-20-15-2 include the following:

- Changes to the referenced interest rate index (for example, a change from London Interbank Offered Rate [LIBOR] to another interest rate index)

- Addition of or changes to a spread adjustment (for example, adding or adjusting a spread to the interest rate index, amending the fixed rate for an interest rate swap, or paying or receiving a cash settlement for any difference intended to compensate for the difference in reference rates)

- Changes to the reset period, reset dates, day-count conventions, business-day conventions, payment dates, payment frequency, and repricing calculation (for example, a change from a forward-looking term rate to an overnight rate or a compounded overnight rate in arrears)

- Changes to the strike price of an existing interest rate option (including an embedded interest rate option)

- Addition of an interest rate floor or cap that is out of the money on the basis of the spot rate at the time of the amendment of the contract

- Addition of a prepayment option for which exercise is contingent upon the replacement reference interest rate index not being determinable in accordance with the terms of the agreement

- Addition of or changes to contractual fallback terms that are consistent with fallback terms developed by a regulator or by a private-sector working group convened by a regulator

- Changes to terms (including those in the examples in paragraph 848-20-15-6) that are necessary to comply with laws or regulations or to align with market conventions for the replacement rate.

848-20-15-6 Examples of changes to terms that are generally unrelated to the replacement of a reference rate in accordance with paragraph 848-20-15-3 include the following:

- Changes to the notional amount

- Changes to the maturity date

- Changes from a referenced interest rate index to a stated fixed rate

- Changes to the loan structure (for example, changing a term loan to a revolver loan)

- The addition of an underlying or variable unrelated to the referenced rate index (for example, addition of payments that are indexed to the price of gold)

- The addition of an interest rate floor or cap that is in the money on the basis of the spot rate at the time of the amendment of the contract

- A concession granted to a debtor experiencing financial difficulty

- The addition or removal of a prepayment or conversion option except for the addition of a prepayment option for which exercise is contingent upon the replacement reference interest rate index not being determinable in accordance with the terms of the agreement

- The addition or removal of a feature that is intended to provide leverage

- Changes to the counterparty except in accordance with paragraphs 815-20-55-56A, 815-25-40-1A, and 815-30-40-1A

- Changes to the priority or seniority of an obligation in the event of a default or a liquidation event

- The addition or termination of a right to use one or more underlying assets in a lease contract

- Changes to renewal, termination, or purchase option provisions in a lease contract.

> > > Changes to Contractual Fallback Terms

848-20-15-7 The addition of contractual fallback terms, or the amendment of existing contractual fallback terms, to be consistent with fallback terms developed by a regulator or by a private-sector working group convened by a regulator is presumed to be related to reference rate reform in accordance with paragraph 848-20-15-5(g). That includes a predefined method to replace the current reference rate upon the discontinuance (or an anticipated discontinuance) of the reference rate.

848-20-15-8 If an entity modifies a contract to add contractual fallback terms or to change contractual fallback terms in a manner that is not consistent with fallback terms developed by a regulator or by a private-sector working group convened by a regulator, the entity shall assess whether the fallback terms include, or have the potential to include, a term that is unrelated to reference rate reform in accordance with paragraph 848-20-15-6 (for example, whether it is possible that the replacement rate could be a stated fixed rate). However, the inclusion of fallback terms that include, or have the potential to include, a term that is unrelated to reference rate reform shall be disregarded by an entity if at the time that the contractual fallback terms are added or amended the entity determines that activation of the term unrelated to reference rate reform is not probable of occurring if the fallback terms are triggered.

> > > Changes from a Referenced Interest Rate Index to a Stated Fixed Rate

848-20-15-9 A contract modification that directly replaces a reference rate index with a stated fixed rate is unrelated to reference rate reform in accordance with paragraph 848-20-15-6(c). However, the selection of a rate that is the last published rate of an interest rate index that is discontinued is not considered a stated fixed rate for the purpose of paragraph 848-20-15-6(c) (for example, a reference to the last published LIBOR rate is not considered unrelated to reference rate reform).

848-20-15-10 If a contract has existing contractual fallback terms that replace the current reference rate with a stated fixed rate upon the discontinuation of that current reference rate, a modification to those contractual fallback terms to replace the stated fixed rate with a new interest rate index is a change that is related to the replacement of the reference rate in accordance with paragraph 848-20-15-5.

> Modifications before the Discontinuance of a Reference Rate

848-20-15-11 An entity may modify the terms of a contract in anticipation of the discontinuance of the reference rate (that is, before the actual discontinuance of the reference rate).

Subsequent Measurement

General

> Option to Apply Expedients

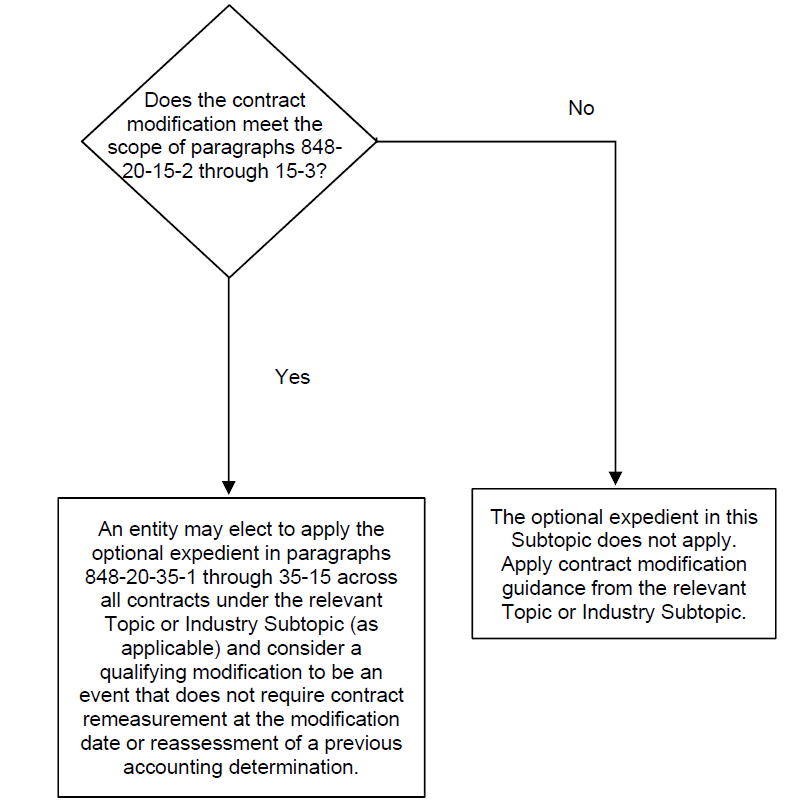

848-20-35-1 An entity may elect to apply the guidance in this Subtopic to account for contract modifications that meet the scope of paragraphs 848-20-15-2 through 15-3. If an entity elects to apply the guidance in this Subtopic, the entity shall apply it for all contract modifications that meet the scope of paragraphs 848-20-15-2 through 15-3 that otherwise would be accounted for in accordance with the same Topic or Industry Subtopic. For example:

- If an entity applies the guidance in this Subtopic to modifications of a lease for a lessee accounted for in accordance with Topic 842, it shall apply the guidance in this Subtopic to all modifications of leases accounted for in accordance with Topic 842 that meet the scope of paragraphs 848-20-15-2 through 15-3.

- If an insurance entity applies the guidance in this Subtopic to modifications of a contract accounted for in accordance with Topic 310 on receivables, it shall apply the guidance in this Subtopic to all modifications of contracts accounted for in accordance with Industry Subtopic 944-310 that meet the scope of paragraphs 848-20-15-2 through 15-3. The entity does not need to apply the guidance in this Subtopic to contracts within the scope of other Industry Subtopics of Topic 944 that meet the scope of paragraphs 848-20-15-2 through 15-3.

848-20-35-2 If a contract modification does not meet the guidance for applying the optional relief in this Subtopic and, therefore, an entity must apply the guidance in another Topic or Industry Subtopic to assess the contract modification, that result shall not preclude the entity from applying the optional expedients in this Subtopic if other contract modifications meet the guidance for applying this Subtopic.

> Optional Expedient: Contract Modifications Due to Reference Rate Reform

848-20-35-3 This Subtopic provides optional expedients for accounting for modifications of contracts accounted for in accordance with the following Topics that meet the scope of paragraphs 848-20-15-2 through 15-3:

- Topic 310 on receivables

- Topic 470 on debt

- Topic 840 or 842 on leases.

848-20-35-4 If a contract is not within the scope of the Topics referenced in paragraph 848-20-35-3, an entity shall have the option to account for and present a modification that meets the scope of paragraphs 848-20-15-2 through 15-3 as an event that does not require contract remeasurement at the modification date or reassessment of a previous accounting determination required under the relevant Topic or Industry Subtopic. Paragraph 848-20-55-2 includes examples that illustrate the application of that guidance.

848-20-35-5 If the optional expedient in paragraphs 848-20-35-3 through 35-4 is elected, it shall be applied to all contracts accounted for under the relevant Topic or Industry Subtopic as described in paragraph 848-20-35-1.

> > Contracts within the Scope of Topic 310

848-20-35-6 If an entity elects the optional expedient in this paragraph, the entity shall account for a modification of a contract within the scope of Topic 310 that meets the scope of paragraphs 848-20-15-2 through 15-3 as if the modification was only minor in accordance with paragraph 310-20-35-10.

848-20-35-7 If the optional expedient in paragraph 848-20-35-6 is elected, it shall be applied to all contracts subject to Topic 310 as described in paragraph 848-20-35-1.

> > Contracts within the Scope of Topic 470

848-20-35-8 If an entity elects the optional expedient in this paragraph, the entity shall account for a modification of a contract within the scope of Topic 470 that meets the scope of paragraphs 848-20-15-2 through 15-3 in accordance with paragraphs 470-50-40-14, 470-50-40-16, 470-50-40-17(b), and 470-50-40-18(b) as if the modification was not substantial. That is, the original contract and the new contract shall be accounted for as if they were not substantially different from one another, and the modification shall not be accounted for in the same manner as a debt extinguishment in accordance with paragraph 470-50-40-13.

848-20-35-9 If the optional expedient in paragraph 848-20-35-8 is elected, it shall be applied to all contracts under Topic 470 as described in paragraph 848-20-35-1.

> > > Debt Exchanges or Modifications within a Year of the Current Modification

848-20-35-10 If the optional expedient in paragraph 848-20-35-8 is elected, an entity that applies the 10 percent cash flow test described in paragraph 470-50-40-10 for any subsequent contract modification within a year shall consider only terms and provisions that were in effect immediately following the election of the optional expedient for the particular contract.

> > Contracts within the Scope of Topic 840 or 842

848-20-35-11 If an entity elects the optional expedient in this paragraph for a modification of a contract within the scope of Topic 840 or 842 that meets the scope of paragraphs 848-20-15-2 through 15-3, the entity shall not do any of the following:

- Reassess lease classification and the discount rate (for example, the incremental borrowing rate for a lessee)

- Remeasure lease payments

- Perform other reassessments or remeasurements that would otherwise be required under Topic 840 or 842 when a modification of a lease contract is not accounted for as a separate contract.

848-20-35-12 If the optional expedient in paragraph 848-20-35-11 is elected, it shall be applied to all contracts under Topic 840 or 842 as described in paragraph 848-20-35-1.

> > > Lessees

848-20-35-13 If the optional expedient in paragraph 848-20-35-11 is elected, the modification of the reference rate and other terms related to the replacement of the reference rate on which variable lease payments in the original contract depended shall not require an entity to remeasure the lease liability. The change in the reference rate shall be treated in the same manner as the variable lease payments that were dependent on the reference rate in the original lease. That change shall not be included in the calculation of the lease liability; that is, the change shall be recognized in profit or loss in the period in which the obligation for those payments is incurred.

> > Embedded Derivatives within the Scope of Subtopic 815-15

848-20-35-14 If the optional expedient in this paragraph is elected, modification of a contract that meets the scope of paragraphs 848-20-15-2 through 15-3 (including the addition of an interest rate floor or cap that is out of the money in paragraph 848-20-15-5(e)) shall not require an entity to reassess its original conclusion about whether that contract contains an embedded derivative that is clearly and closely related to the economic characteristics and risks of the host contract for the purposes of paragraph 815-15-25-1(a).

848-20-35-15 If the optional expedient in paragraph 848-20-35-14 is elected, it shall be applied to all contracts under Subtopic 815-15 as described in paragraph 848-20-35-1.

Implementation Guidance and Illustrations

General

> Implementation Guidance

848-20-55-1 The following flowchart summarizes the guidance in this Subtopic.

848-20-55-2 The following table illustrates the potential outcomes of applying the guidance in paragraph 848-20-35-4 to contract modifications that meet the scope of paragraphs 848-20-15-2 through 15-3 but are not within the scope of the Topics listed in paragraph 848-20-35-3. This table is not intended to be all-inclusive of the potential application of paragraph 848-20-35-4.

Contract or Instrument Modified as a Result of Reference Rate Reform | Potential Outcome of Applying Paragraph 848-20-35-4 |

An instrument accounted for as a derivative instrument in accordance with Subtopic 815-10

|

An entity should not reassess the modified instrument to determine whether it is a hybrid instrument and whether it includes a financing element in accordance with paragraphs 815-10-45-11 through 45-15. The modified instrument should be accounted for and presented in the same manner as the instrument existing before the modification.

|

A contract issued by an insurance entity and accounted for in accordance with Topic 944

|

An entity should not reassess the modified contract to determine whether it is substantially unchanged in accordance with Subtopic 944-30. The modified contract should be accounted for and presented as a continuation of the contract existing before the modification.

|

A contract accounted for in accordance with Topic 606 on revenue from contracts with customers

|

An entity should not reassess the modified contract in accordance with the contract modification guidance in paragraphs 606-10-25-10 through 25-13. Cash flow changes resulting from variability in the replacement reference rate should be accounted for and presented in the same manner as the cash flow changes that resulted from variability in the replaced reference rate before the modification for reference rate reform.

|

A contract with a counterparty entity that is within the scope of the Variable Interest Entities (VIE) Subsections in accordance with Topic 810 on consolidation

|

An entity should not reconsider the determination of the counterparty entity’s VIE status in accordance with paragraph 810-10-35-4. The counterparty entity’s VIE status should remain unchanged from the VIE status determined before the modification.

|

4. Add Subtopic 848-30 as follows:

[For ease of readability, the new Subtopic is not underlined.]

Reference Rate Reform—Hedging—General

Overview and Background

General

848-30-05-1 This Subtopic provides guidance on optional expedients for allowing hedging relationships to continue when one or more of the critical terms of the hedging relationship change because of reference rate reform.

Scope and Scope Exceptions

General

848-30-15-1 The guidance in this Subtopic provides optional expedients for the requirements of Subtopic 815-20 related to changes in the critical terms of a hedging relationship that may be applied if the hedging instrument or the hedged item or the hedged forecasted transaction in the hedging relationship references a rate that meets the scope of paragraph 848-10-15-3.

Recognition

General

848-30-25-1 This Section sets forth the conditions that allow amendments to be made to the formal designation and documentation of hedging relationships upon a change due to reference rate reform.

> Option to Apply Expedients

848-30-25-2 An entity may elect to apply the guidance in this Subtopic for hedging relationships affected by reference rate reform on an individual hedging relationship basis. In addition, an entity may elect to apply the different optional expedients specified in paragraphs 848-30-25-3 through 25-13 on an individual hedging relationship basis. That is, each optional expedient may be elected for each individual hedging relationship and may not be elected for other similar hedging relationships. In addition, an entity may elect multiple optional expedients for the same individual hedging relationship and may elect those optional expedients in different reporting periods. For example, for a cash flow hedge, an entity may elect the optional expedient for the changes in the critical terms of the hedging instrument in accordance with paragraphs 848-30-25-5 through 25-7 when the fallback protocol of the hedging instrument is changed. In a different reporting period, the entity may elect to apply the optional expedient in paragraph 848-30-25-8 to change the method used in assessing hedge effectiveness and may elect to apply an optional expedient for subsequent assessments of effectiveness set forth in Subtopic 848-50.

> Optional Expedient: Change to the Formal Designation and Documentation for Change in Critical Terms

848-30-25-3 This paragraph provides an optional expedient for the guidance in paragraph 815-20-55-56. A change in the critical terms of the hedging relationship as documented at inception because of the election of an optional expedient in this Subtopic and Subtopics 848-40 and 848-50 shall not, in and of itself, be considered a dedesignation of the hedging relationship.

848-30-25-4 If an entity elects the optional expedient in paragraph 848-30-25-3, the entity shall update its hedge documentation (as applicable) noting the changes made no later than when the entity performs its first assessment of effectiveness after the change was identified in accordance with paragraphs 815-20-25-3(b)(2)(iv)(02) and 815-20-25-3A.

> > Optional Expedient: Changes in the Critical Terms of a Hedging Instrument, a Hedged Item, or a Forecasted Transaction Designated in a Fair Value Hedge, a Cash Flow Hedge, or a Net Investment Hedge

848-30-25-5 An entity may change the contractual terms of a hedging instrument, a hedged item, or a forecasted transaction designated in a fair value hedge, a cash flow hedge, or a net investment hedge that is affected or expected to be affected by reference rate reform and not be required to dedesignate the hedging relationship if the changes to the contractual terms meet the scope of paragraphs 848-20-15-2 through 15-3.

848-30-25-6 Some derivative instruments designated as hedging instruments may be modified through direct contract amendments to effectuate a change because of reference rate reform. Alternatively, a derivative designated as a hedging instrument may be modified to effectuate the changes because of reference rate reform by both:

- Entering into a fully offsetting derivative contract to effectively cancel the original derivative contract

- Contemporaneously entering into a new derivative contract with the revised contractual terms.

Both methods of effectuating changes to contractual terms as a result of reference rate reform qualify for the optional expedient in paragraph 848-30-25-5.

848-30-25-7 A change to the interest rate used for margining, discounting, or contract price alignment for a derivative that is a hedging instrument in a fair value hedge, a cash flow hedge, or a net investment hedge shall not be considered a change to the critical terms of the hedging relationship that requires dedesignating the hedging relationship because of that change.

> > Optional Expedient: Changes to the Method Designated for Use in Assessing Hedge Effectiveness in a Cash Flow Hedge

848-30-25-8 An entity may change the method designated for use in assessing hedge effectiveness and documented at hedge inception in accordance with paragraph 815-20-25-3(b)(iv)(02) if both of the following criteria are met:

- Either the hedging instrument or the hedged forecasted transaction references a rate that meets the scope of paragraph 848-10-15-3.

- The new method designated for use in assessing hedge effectiveness is an optional expedient specified in Subtopic 848-50.

That expedient may be elected for a hedging relationship at the date an entity elects to apply any optional expedient method in accordance with this Subtopic. An entity also may change the method designated for use in assessing hedge effectiveness in Subtopics 815-20 and 815-30 upon the required discontinuance of an optional expedient as discussed in paragraph 848-50-35-19. An entity shall not be required to assess whether the replacement method is an improved method for assessing effectiveness or a preferable method of applying an accounting principle in accordance with Topic 250 on accounting changes and error corrections.

> > Optional Expedient: Changes to the Proportion of a Hedged Item or a Hedging Instrument in a Fair Value Hedge and to the Hedging Instruments That Are Designated in a Fair Value Hedge or a Cash Flow Hedge

848-30-25-9 If the hedging instrument or the hedged forecasted transaction or the designated benchmark interest rate in a fair value hedge references a rate that meets the scope of paragraph 848-10-15-3 and the hedging relationship is anticipated to be affected by reference rate reform, an entity may change:

- The proportion of a designated hedged item or a derivative instrument that is designated as a hedging instrument in a fair value hedge relationship. An entity may elect to rebalance the hedging relationship through any of the following approaches, including any combination of these approaches:

- Increasing the designated notional amount of the hedging instrument

- Decreasing the designated notional amount of the hedging instrument

- Increasing the designated portion of the hedged item

- Decreasing the designated portion of the hedged item.

If an entity applies the optional expedient in (3) or (4), the cumulative effect of changing the designated proportion of the hedged item shall be recognized as an adjustment to the basis adjustment that shall be recognized in accordance with paragraph 848-40-25-7.

- The designated hedging instrument to combine two or more derivative instruments, or proportions of those instruments, to be jointly designated as the hedging instrument in a hedge relationship.

848-30-25-10 If an entity changes the designated hedging instrument in a fair value hedge to combine two or more derivative instruments, or proportions of those instruments, in accordance with paragraph 848-30-25-9(b), the entity shall assess the hedge effectiveness of the amended hedging relationship using a method in accordance with Subtopics 815-20 and 815-25. An entity also may select a new method in accordance with Subtopics 815-20 and 815-25 to assess the hedge effectiveness.

848-30-25-11 If an entity changes the designated hedging instrument in a cash flow hedge to combine two or more derivative instruments, or proportions of those instruments, in accordance with paragraph 848-30-25-9(b), the entity shall assess the hedge effectiveness of the amended hedging relationship using any of the following:

- A method in accordance with Subtopics 815-20 and 815-30

- An optional expedient for the subsequent assessment methods for assuming perfect effectiveness in accordance with paragraphs 848-50-35-4 through 35-9

- An optional expedient for the subsequent qualitative method after an initial assessment using a quantitative method in accordance with paragraphs 848-50-35-10 through 35-16

- An optional expedient for the subsequent quantitative methods in accordance with paragraphs 848-50-35-17 through 35-18.

> > Optional Expedient: Changes to the Systematic and Rational Method Used for Recognizing in Earnings the Excluded Components in a Fair Value Hedge, a Cash Flow Hedge, or a Net Investment Hedge

848-30-25-12 If the changes to a hedging instrument’s contractual terms meet the scope of paragraphs 848-20-15-2 through 15-3, an entity may elect to change its systematic and rational method used to recognize in earnings the components excluded from the assessment of effectiveness in accordance with paragraph 815-20-25-83A. An entity shall apply the amended systematic and rational method prospectively and shall retain the amended systematic and rational method for the remaining life of the hedging relationship, including for periods after the date in paragraph 848-10-65-1(a)(3)(iii). The amended systematic and rational method may be subsequently amended for subsequent changes to a hedging instrument’s contractual terms that meet the scope of paragraphs 848-20-15-2 through 15-3. If an entity does not apply this optional expedient, the entity’s systematic and rational method documented at hedge inception may require an adjustment at the end of the hedging relationship so that no excluded components remain in accumulated other comprehensive income at the end of the hedging relationship.

848-30-25-13 In addition, if the changes to a hedging instrument’s contractual terms meet the scope of paragraphs 848-20-15-2 through 15-3 and any change in those contractual terms causes a change in the fair value of the excluded component, an entity may elect to recognize the change in fair value of the excluded component in current earnings. An entity shall present the recognition of the adjustment in the same income statement line item that is used to present the earnings effect of the hedged item.

5. Add Subtopic 848-40 as follows:

[For ease of readability, the new Subtopic is not underlined.]

Reference Rate Reform—Fair Value Hedges

Overview and Background

General

848-40-05-1 This Subtopic provides guidance on optional expedients for the accounting for and financial reporting of fair value hedges under Topic 815 that are affected by reference rate reform.

Scope and Scope Exceptions

General

848-40-15-1 The guidance in this Subtopic provides optional expedients for certain requirements of Subtopics 815-20 and 815-25 related to fair value hedges. An entity shall continue to apply all other requirements applicable to fair value hedges in Subtopics 815-20 and 815-25.

Recognition

General

> Option to Apply Expedients

848-40-25-1 An entity may elect to apply the guidance in this Subtopic for fair value hedges affected by reference rate reform on an individual hedging relationship basis. In addition, an entity may elect to apply the different optional expedients specified in paragraphs 848-40-25-2 through 25-9 on an individual hedging relationship basis. For example, an entity may elect to apply the optional expedient in this Subtopic for the change in the designated benchmark interest rate and not elect to apply the optional expedient for the shortcut method for assessing hedge effectiveness. An entity may disregard the guidance in paragraph 815-20-25-81 when applying the guidance in this Subtopic and shall not be required to assess effectiveness for similar hedges in a similar manner.

> Optional Expedient: Change in the Designated Benchmark Interest Rate

848-40-25-2 If the hedged item is a financial asset or liability, a recognized loan servicing right, or a nonfinancial firm commitment with financial components, the designated risk being hedged may be the risk of changes in the hedged item’s fair value attributable to changes in the designated benchmark interest rate in accordance with paragraph 815-20-25-12(f)(2). In a hedge of the changes in fair value attributable to the benchmark interest rate, if the referenced interest rate index of the hedging instrument changes or an entity changes the designated hedging instrument to combine two or more derivative instruments to be jointly designated as the hedging instrument in accordance with paragraph 848-30-25-9(b) (for example, adding a new interest rate basis swap to an existing interest rate swap), an entity may change the designated benchmark interest rate and the component of cash flows and continue to apply hedge accounting without dedesignation if all of the following criteria are met:

- The designated benchmark interest rate being changed is a rate within the scope of paragraph 848-10-15-3.

- The replacement designated benchmark interest rate is an eligible benchmark interest rate in accordance with paragraph 815-20-25-6A.

- The hedging instrument is expected to be prospectively highly effective at achieving offsetting changes in fair value attributable to the revised hedged risk on the basis of the amended terms of the hedging relationship.

848-40-25-3 An entity shall update its hedge documentation in accordance with paragraph 848-30-25-4 upon a change in the designated benchmark interest rate in accordance with paragraph 848-40-25-2.

> > Change in Fair Value of Hedged Item Due to a Change in the Designated Benchmark Interest Rate

848-40-25-4 If an entity elects the optional expedient in paragraphs 848-40-25-2 through 25-3 to change the designated benchmark interest rate, it shall, at a minimum, revise the rate used to discount the cash flows associated with the hedged item reflecting the change in the designated benchmark interest rate in accordance with paragraph 848-40-25-2. An entity may include a spread adjustment to the revised benchmark interest rate used to discount the cash flows associated with the hedged item in accordance with an approach in paragraph 848-40-25-5. In addition, an entity may adjust the cash flows for the designated term of the designated hedged item.

848-40-25-5 At the time of the change to the designated benchmark interest rate, an entity may either:

- Apply an approach that adjusts the hedged item’s cumulative fair value hedge basis adjustment attributable to changing from the originally designated benchmark interest rate to the replacement designated benchmark interest rate

- Apply an approach that results in no adjustment to the hedged item’s cumulative basis adjustment (that is, maintain the hedged item’s cumulative basis adjustment immediately before the date of the change).

This Subtopic does not specify a single method for applying those approaches. The method an entity uses shall be reasonable, and an entity shall use a similar method for similar hedges and shall justify the use of different methods for similar hedges.

848-40-25-6 In calculating the subsequent changes in the hedged item’s fair value attributable to changes in the replacement benchmark interest rate, an entity shall use the revised benchmark interest rate to discount the cash flows associated with the hedged item and shall use the remaining revised cash flows for the designated term of the designated hedged item. The revised benchmark interest rate (including the spread adjustment to the revised benchmark interest rate if applicable) to discount the cash flows associated with the hedged item and the remaining revised cash flows for the designated term shall be retained for periods after the date in paragraph 848-10-65-1(a)(3)(iii).

848-40-25-7 If an entity adjusts the cumulative basis adjustment because of the change in the designated benchmark interest rate in accordance with paragraph 848-40-25-5(a), the entity shall recognize the adjustment currently in earnings. An entity shall present the adjustment in the same income statement line item that is used to present the earnings effect of the hedged item.

> Optional Expedient: Assessment of Hedge Effectiveness When Assuming Perfect Hedge Effectiveness in a Hedge with an Interest Rate Swap (Shortcut Method)

848-40-25-8 For fair value hedges for which the shortcut method is applied in accordance with paragraphs 815-20-25-102 through 25-109 and 815-20-25-111 through 25-117, the following conditions from paragraph 815-20-25-104 that apply to fair value hedges may be disregarded in determining whether the hedging relationship continues to qualify for the shortcut method upon a change in the contractual terms of the hedging instrument in accordance with paragraphs 848-30-25-5 through 25-7:

- The formula for computing net settlements under the interest rate swap is the same for each net settlement in accordance with paragraph 815-20-25-104(d).

- The terms are typical of those instruments, and the terms do not invalidate the assumption of perfect effectiveness in accordance with paragraph 815-20-25-104(g).

If an entity elects the practical expedient in this paragraph for a fair value hedge for which the shortcut method is applied, the entity is not required to periodically evaluate the conditions in paragraph 815-20-25-104(d) and (g) for the remaining life of the hedging relationship, including for periods after December 31, 2022 (see paragraph 848-10-65-1(a)(3)(iii)).

848-40-25-9 If an entity elects to apply the optional expedient for the shortcut method in paragraph 848-40-25-8, the entity shall update its hedge documentation in accordance with paragraph 848-30-25-4.

6. Add Subtopic 848-50 as follows:

[For ease of readability, the new Subtopic is not underlined.]

Reference Rate Reform—Cash Flow Hedges

Overview and Background

General

848-50-05-1 This Subtopic provides guidance related to optional expedients for the accounting for and financial reporting of cash flow hedges under Topic 815 on derivatives and hedging that are affected by reference rate reform.

Scope and Scope Exceptions

General

848-50-15-1 The guidance in this Subtopic provides optional expedients for certain requirements of Subtopics 815-20 and 815-30 related to the assessment of hedge effectiveness and the designation of cash flow hedges. An entity shall continue to apply all other cash flow hedge accounting requirements specified in Subtopics 815-20 and 815-30.

Recognition

General

> Option to Apply Expedients

848-50-25-1 An entity may elect to apply the optional expedients for the assessment of hedge effectiveness in this Subtopic to cash flow hedges affected by reference rate reform on an individual hedging relationship basis. In addition, an entity may elect to apply the different optional expedients for the assessment of hedge effectiveness in this Subtopic on an individual hedging relationship basis. An entity may disregard the guidance in paragraph 815-20-25-81 when applying the guidance in this Subtopic and shall not be required to assess effectiveness for similar hedges in a similar manner.

> Eligibility of Cash Flow Hedges Affected by Reference Rate Reform

> > Probability of the Hedged Forecasted Transaction

848-50-25-2 An entity shall continue to assess whether the underlying hedged forecasted transaction (for example, the future interest receipts of a financial asset or future interest payments of a financial liability or the forecasted issuance or purchase of a debt instrument) remains probable in accordance with paragraph 815-20-25-15(b). If the designated hedged interest rate risk in a cash flow hedge of a forecasted transaction is a reference rate that meets the scope of paragraph 848-10-15-3, an entity may assert that the hedged forecasted transaction (for example, the future interest receipts of a financial asset or future interest payments of a financial liability or the forecasted issuance or purchase of a debt instrument) remains probable in accordance with paragraph 815-20-25-15(b) regardless of the modification or expected modification of terms in accordance with paragraphs 848-20-15-2 through 15-3.

> > Change in the Designated Hedged Interest Rate Risk

848-50-25-3 Paragraph 815-30-35-37A specifies that the designated hedged risk for a cash flow hedge of a forecasted transaction may change during a hedging relationship and an entity may continue to apply hedge accounting if the hedge remains highly effective. For purposes of applying that guidance to a cash flow hedge affected by reference rate reform, a cash flow hedge may continue hedge accounting subject to either the hedging relationship remaining highly effective in accordance with Subtopics 815-20 and 815-30 or an entity electing an optional expedient method to subsequently assess hedge effectiveness in accordance with paragraphs 848-50-35-1 through 35-18. If an entity elects to change the designated hedged interest rate risk for a cash flow hedge, the entity shall update its hedge documentation in accordance with paragraph 848-30-25-4.

> Initial Assessment of Hedge Effectiveness

> > Optional Expedients for Initial Assessment of Hedge Effectiveness

848-50-25-4 An entity may perform its initial hedge effectiveness assessment in a manner that adjusts how it applies certain guidance in Subtopics 815-20 and 815-30 as specified in paragraph 848-50-25-5 for cash flow hedges for which either the hedged forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3. For subsequent hedge effectiveness assessments, an entity may use the eligible optional expedients for hedge effectiveness assessment in paragraphs 848-50-35-1 through 35-18.

848-50-25-5 In accordance with paragraph 815-20-25-3(b)(2)(iv)(01), an entity shall perform an initial prospective assessment of hedge effectiveness on a quantitative basis unless one of the methods listed in paragraph 815-20-25-3(b)(2)(iv)(01) applies. Paragraphs 848-50-25-6 through 25-12 describe certain modifications to the relevant methods for performing an initial assessment of hedge effectiveness for cash flow hedges within the scope of this Subtopic.

848-50-25-6 An entity may disregard the following conditions in determining whether it may apply the shortcut method for assuming perfect hedge effectiveness in a cash flow hedge with an interest rate swap in accordance with paragraphs 815-20-25-102 through 25-109 and 815-20-25-111 through 25-117:

- The formula for computing net settlements under the interest rate swap is the same for each net settlement in accordance with paragraph 815-20-25-104(d).

- The terms are typical of those derivative instruments and do not invalidate the assumption of perfect effectiveness in accordance with paragraph 815-20-25-104(g).

- The repricing dates of the variable-rate asset or variable-rate liability and the hedging instrument must occur on the same dates and be calculated the same way in accordance with paragraph 815-20-25-106(d).

- The index on which the variable leg of the interest rate swap is based matches the contractually specified interest rate designated as the interest rate being hedged for that hedging relationship in accordance with paragraph 815-20-25-106(g).

848-50-25-7 For cash flow hedges when an option’s terminal value is used to assess hedge effectiveness, an entity may disregard the following conditions in determining whether a cash flow hedge of the option’s terminal value may be considered perfectly effective in accordance with paragraphs 815-20-25-126 through 25-129A:

- The underlying of the hedging instrument needs to match the underlying of the hedged forecasted transaction in accordance with paragraph 815-20-25-129(a).

- The strike price (or prices) of the hedging option (or combination of options) matches the specified level (or levels) beyond (or within) which the entity’s exposure is being hedged in accordance with paragraph 815-20-25-129(b).

- The hedging instrument’s inflows (outflows) at its maturity date due to the underlying reference rate and strike price (or prices) of the hedging option (or combination of options) completely offset the change in the hedged transaction’s cash flows for the risk being hedged in accordance with paragraph 815-20-25-129(c).

If all other conditions in paragraph 815-20-25-129 are met, the hedging relationship may be considered perfectly effective.

848-50-25-8 An eligible private company in accordance with paragraph 815-2025-135 may disregard the following conditions in determining whether a cash flow hedge of a variable-rate borrowing with a receive-variable pay-fixed interest rate swap using the simplified hedge accounting approach may be considered perfectly effective in accordance with paragraphs 815-20-25-133 through 25-138:

- Both the variable rate on the swap and the borrowing are based on the same index and reset period in accordance with paragraph 815-20-25-137(a).

- The terms of the swap are typical in accordance with paragraph 815-20-25-137(b).

- The repricing and settlement dates for the swap and the borrowing match in accordance with paragraph 815-20-25-137(c).

If all other conditions of paragraph 815-20-25-137 are met, the hedging relationship may apply the simplified hedge accounting approach.

848-50-25-9 For the change-in-variable-cash-flows method in accordance with paragraphs 815-30-35-16 through 35-24, an entity may disregard the following conditions in assessing whether the method will result in a perfectly effective hedge in accordance with paragraph 815-30-35-22:

- The variable-rate leg of the interest rate swap and the hedged variable cash flows of the asset or liability are based on the same interest rate index in accordance with paragraph 815-30-35-22(a).

- The interest rate reset dates applicable to the variable-rate leg of the interest rate swap and to the hedged variable cash flows of the asset or liability are the same in accordance with paragraph 815-30-35-22(b).

In addition, an entity may disregard the condition in paragraph 815-30-35-22(c) if the basis differences are due to differences in a cap or floor between the variable-rate leg of the interest rate swap and the variable-rate asset or the variable-rate liability. If all other conditions in paragraph 815-30-35-22 are met, the hedging relationship may be considered perfectly effective. If all other conditions in paragraph 815-30-35-22 are not met, an entity shall not consider that the method will result in a perfectly effective hedge.

848-50-25-10 For the hypothetical derivative method in accordance with paragraphs 815-30-35-25 through 35-29, an entity may disregard the following critical terms in assessing whether the method will result in a perfectly effective hedge:

- The same repricing dates in accordance with paragraph 815-30-35-25(b)(2)

- The same index in accordance with paragraph 815-30-35-25(b)(3)

- Mirror image caps and floors (including a cap or floor that exists in a variable-rate asset or a variable-rate liability and does not exist in a hedging instrument or vice versa) in accordance with paragraph 815-30-35-25(b)(4).

If all other conditions in paragraph 815-30-35-25 are met, the hedging relationship may be considered perfectly effective. If all other conditions in paragraph 815-30-35-25 are not met, an entity shall not consider that the method will result in a perfectly effective hedge.

> > > Optional Expedient: Initial Assessment Performed Using a Quantitative Method

848-50-25-11 An entity may adjust any of the three methods of assessing hedge effectiveness in paragraphs 815-30-35-10 through 35-32 when hedge effectiveness is assessed on a quantitative basis (using either a dollar-offset test or a statistical method such as regression analysis) as follows:

- If both the hedged forecasted transaction and the hedging instrument have a reference rate that meets the scope of paragraph 848-10-15-3 (or in a cash flow hedge of a forecasted purchase, sale, or issuance of a fixed-rate instrument in which the designated hedged interest rate risk is the benchmark interest rate if only the hedging instrument has a reference rate that meets the scope of paragraph 848-10-15-3), an entity may assume that the reference rate will not be replaced for the remainder of the hedging relationship. That is, the entity does not need to consider the likelihood of whether or when the reference rate will be discontinued or changed because of reference rate reform.

- If either the hedged forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3, the terms of the hedged forecasted transaction may be altered to match the hedging instrument for the following:

- The referenced interest rate index

- The reset period, reset dates, day-count conventions, business-day conventions, and repricing calculation (for example, forward-looking calculation or in-arrears calculation)

- A spread adjustment for the difference between the existing reference rate and the replacement reference rate

- A cap or floor (including a cap or floor that exists in a variable-rate asset or a variable-rate liability and does not exist in a hedging instrument or vice versa).

> > > Optional Expedient: Initial Assessment Based on an Option’s Terminal Value

848-50-25-12 If an entity assesses hedge effectiveness on the basis of an option’s terminal value in accordance with paragraph 815-20-25-126 and if either the hedged forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3, an entity may adjust the critical terms of the perfectly effective hypothetical hedging instrument in accordance with paragraph 815-20-25-129 to match the hedging instrument for the following:

- The underlying reference rate

- The strike price (or prices) of the hedging option (or combination of options)

- The hedging instrument’s inflows (outflows) at its maturity date due to the underlying reference rate and strike price (or prices) of the hedging option (or combination of options).

> > Hedging a Group of Forecasted Transactions

848-50-25-13 This paragraph provides an optional expedient for assessing a group of individual forecasted transactions in a cash flow hedge affected by reference rate reform. An entity may elect this optional expedient if a forecasted transaction in the hedged group of forecasted transactions references a rate that meets the scope of paragraph 848-10-15-3.

848-50-25-14 An entity may disregard the guidance in paragraph 815-20-25-15(a)(2) that states that a group of individual transactions shall share the same risk exposure for which they are designated as being hedged. However, other limitations in paragraph 815-20-25-15(a)(2) shall continue such that a forecasted purchase (including debt issuance) and a forecasted sale shall not both be included in the same group of individual transactions that constitute the hedged transaction.

Subsequent Measurement

General

> Subsequent Assessment of Hedge Effectiveness

848-50-35-1 This guidance provides optional expedients that may be elected for cash flow hedges affected by reference rate reform for the purposes of determining whether an entity shall be allowed to continue applying hedge accounting for the hedging relationship. An entity may elect these optional expedient methods if either the forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3.

848-50-35-2 If an entity elects to apply an optional expedient method in this Subtopic for a cash flow hedging relationship, the entity need only apply the optional expedient method prospectively beginning on the date that the expedient method is first applied in determining whether the entity can continue to apply hedge accounting to that hedging relationship. After the date on which the optional expedient method is first applied (if the hedging relationship continues), the entity shall assess the hedging relationship using the optional expedient method both prospectively and retrospectively from the date on which the expedient method is first applied.

848-50-35-3 If an entity elects to change the method of assessing hedge effectiveness for a cash flow hedge to an optional expedient method in accordance with paragraphs 848-50-35-4 through 35-18, the entity shall update its hedge documentation in accordance with paragraph 848-30-25-4.

> > Optional Expedient: Subsequent Assessments Using a Method That Assumes Perfect Effectiveness

848-50-35-4 If an entity applies an initial assessment method in accordance with paragraph 815-20-25-3(b)(2)(iv)(01) or an initial assessment method in accordance with paragraphs 848-50-25-6 through 25-10 for the assessment of initial hedge effectiveness, paragraphs 848-50-35-5 through 35-9 describe certain modifications to the relevant methods for performing an ongoing assessment of hedge effectiveness for cash flow hedges.

848-50-35-5 An entity may disregard the following conditions from paragraphs 815-20-25-104 and 815-20-25-106 that apply to cash flow hedges in determining whether the hedging relationship continues to qualify for the shortcut method upon a change in the contractual terms of the hedging instrument in accordance with paragraphs 848-30-25-5 through 25-7:

- The formula for computing net settlements under the interest rate swap is the same for each net settlement in accordance with paragraph 815-20-25-104(d).

- The terms are typical of those derivative instruments and do not invalidate the assumption of perfect effectiveness in accordance with paragraph 815-20-25-104(g).

- The repricing dates of the variable-rate asset or variable-rate liability and the hedging instrument must occur on the same dates and be calculated the same way in accordance with paragraph 815-20-25-106(d).

- The index on which the variable leg of the interest rate swap is based matches the contractually specified interest rate designated as the interest rate being hedged for that hedging relationship in accordance with paragraph 815-20-25-106(g).

848-50-35-6 For cash flow hedges when an option’s terminal value is used in assessing hedge effectiveness, an entity may disregard the following conditions in determining whether a cash flow hedge of the option’s terminal value may continue to be considered perfectly effective in accordance with paragraphs 815-20-25-126 through 25-129A:

- The underlying of the hedging instrument needs to match the underlying of the hedged forecasted transaction in accordance with paragraph 815-20-25-129(a).

- The strike price (or prices) of the hedging option (or combination of options) matches the specified level (or levels) beyond (or within) which the entity’s exposure is being hedged in accordance with paragraph 815-20-25-129(b).

- The hedging instrument’s inflows (outflows) at its maturity date due to the underlying reference rate and strike price (or prices) of the hedging option (or combination of options) completely offset the change in the hedged transaction’s cash flows for the risk being hedged in accordance with paragraph 815-20-25-129(c).

If all other conditions of paragraph 815-20-25-129 are met, the hedging relationship may continue to be considered perfectly effective.

848-50-35-7 An eligible private company in accordance with paragraph 815-20-25-135 may disregard the following conditions in determining whether a cash flow hedge of a variable-rate borrowing with a receive-variable pay-fixed interest rate swap using the simplified hedge accounting approach may continue to be considered perfectly effective in accordance with paragraphs 815-20-25-133 through 25-138:

- Both the variable rate on the swap and the borrowing are based on the same index and reset period in accordance with paragraph 815-20-25-137(a).

- The terms of the swap are typical in accordance with paragraph 815-20-25-137(b).

- The repricing and settlement dates for the swap and the borrowing match in accordance with paragraph 815-20-25-137(c).

If all other conditions of paragraph 815-20-25-137 continue to be met, the hedging relationship may continue to apply the simplified hedge accounting approach.

848-50-35-8 For the change-in-variable-cash-flows method in accordance with paragraphs 815-30-35-16 through 35-23, an entity may disregard the following conditions in assessing whether the method will result in a perfectly effective hedge in accordance with paragraph 815-30-35-22:

- The variable-rate leg of the interest rate swap and the hedged variable cash flows of the asset or liability are based on the same interest rate index in accordance with paragraph 815-30-35-22(a).

- The interest rate reset dates applicable to the variable-rate leg of the interest rate swap and to the hedged variable cash flows of the asset or liability are the same in accordance with paragraph 815-30-35-22(b).

In addition, an entity may disregard the condition in paragraph 815-30-35-22(c) if the basis differences are due to differences in a cap or floor between the variable-rate leg of the interest rate swap and the variable-rate asset or the variable-rate liability. If all other conditions of paragraph 815-30-35-22 continue to be met, the hedging relationship may continue to be considered perfectly effective. If all other conditions of paragraph 815-30-35-22 are not met, an entity shall not consider that the method will result in a perfectly effective hedge.

848-50-35-9 For the hypothetical-derivative method in accordance with paragraphs 815-30-35-25 through 35-29, an entity may disregard the following critical terms in assessing whether the method will result in a perfectly effective hedge:

- The same repricing dates in accordance with paragraph 815-30-35-25(b)(2)

- The same index in accordance with paragraph 815-30-35-25(b)(3)

- Mirror image caps and floors (including a cap or floor that exists in a variable-rate asset or a variable-rate liability and does not exist in a hedging instrument or vice versa) in accordance with paragraph 815-30-35-25(b)(4).

If all other conditions of paragraph 815-30-35-25 continue to be met, the hedging relationship may continue to be considered perfectly effective. If all other conditions of paragraph 815-30-35-25 are not met, an entity shall not consider that the method will result in a perfectly effective hedge.

> > Optional Expedient: Subsequent Assessments Performed Using a Qualitative Method

848-50-35-10 An entity may qualitatively assess cash flow hedges on an ongoing basis in accordance with paragraphs 848-50-35-11 through 35-16 after the entity has performed an initial assessment of hedge effectiveness using any of the following:

- A method in accordance with Subtopics 815-20 and 815-30

- An optional expedient method in accordance with paragraphs 848-50-25-6 through 25-12.

An entity that elects this optional expedient may disregard the guidance in paragraphs 815-20-35-2A through 35-2F for performing hedge effectiveness assessments on a qualitative basis.

848-50-35-11 The following criteria shall be met so that an entity may continue to assert qualitatively that it may continue to apply hedge accounting for a hedging relationship under this Subtopic:

- The hedged forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3.

- There have been no changes to the terms of the hedging instrument or the forecasted transaction other than those specified in paragraphs 848-20-15-2 through 15-3.

- An entity shall consider the likelihood of the counterparty’s compliance with the contractual terms of the hedging derivative that require the counterparty to make payments to the entity.

848-50-35-12 An entity shall verify and document whenever financial statements or earnings are reported and at least every three months that the facts and circumstances evaluated in accordance with paragraph 848-50-35-11 have not changed; therefore, the entity can assert qualitatively that the hedging relationship did qualify and continues to qualify for this optional expedient method. No other facts and circumstances related to paragraphs 815-20-35-2A through 35-2F need to be assessed as part of this evaluation.

848-50-35-13 If the facts and circumstances change in accordance with paragraph 848-50-35-12 such that an entity no longer can assert qualitatively that the hedging relationship may continue to qualify for hedge accounting under this Subtopic, the entity shall assess hedge effectiveness on a quantitative basis using the guidance in Subtopics 815-20 and 815-30 or using a quantitative optional expedient method in this Subtopic to the extent that the quantitative optional expedient method is eligible to be used.

848-50-35-14 If there is no identifiable event that led to the change in the facts and circumstances of the hedging relationship, the entity may begin performing quantitative assessments of effectiveness from the beginning of the current period. An entity may change its method of assessing hedge effectiveness and update its hedging documentation to reflect that change in accordance with paragraph 848-30-25-4.

848-50-35-15 After assessing the hedge effectiveness using a quantitative optional expedient method for one or more reporting periods, an entity may revert to a qualitative optional expedient method of hedge effectiveness under this Subtopic to the extent that the qualitative optional expedient method is eligible to be used.

848-50-35-16 An entity may perform a quantitative assessment of hedge effectiveness in any reporting period, and the results of that quantitative assessment shall not preclude an entity from using the qualitative optional expedient method in paragraphs 848-50-35-11 through 35-12 in a subsequent reporting period.

> > Optional Expedient: Subsequent Assessments Performed Using a Quantitative Method

848-50-35-17 After initially assessing the hedge effectiveness using a method in accordance with Subtopics 815-20 and 815-30 or using an optional expedient method in accordance with paragraphs 848-50-25-6 through 25-12, an entity may adjust any of the three methods of assessing subsequent hedge effectiveness in paragraphs 815-30-35-10 through 35-32 when hedge effectiveness is assessed on a quantitative basis (using either a dollar-offset test or a statistical method such as regression analysis) as follows:

- If both the hedged forecasted transaction and the hedging instrument have a reference rate that meets the scope of paragraph 848-10-15-3 (or in a cash flow hedge of a forecasted purchase, sale, or issuance of a fixed-rate instrument in which the designated hedged interest rate risk is the benchmark interest rate if only the hedging instrument has a reference rate that meets the scope of paragraph 848-10-15-3), an entity may assume that the reference rate will not be replaced for the remainder of the hedging relationship. That is, the entity does not need to consider the likelihood of whether the reference rate will be discontinued or changed because of reference rate reform.

- If either the hedged forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3, the terms of the hedged forecasted transaction may be altered to match the hedging instrument for the following:

- The referenced interest rate index

- The reset period, reset dates, day-count conventions, business-day conventions, and repricing calculation (for example, forward-looking calculation or in-arrears calculation)

- A spread adjustment for the difference between the existing reference rate and the replacement reference rate

- A cap or floor (including a cap or floor that exists in a variable-rate asset or a variable-rate liability and does not exist in a hedging instrument or vice versa).

> > Optional Expedient: Subsequent Assessment Based on an Option’s Terminal Value

848-50-35-18 If an entity assesses subsequent hedge effectiveness on the basis of an option’s terminal value in accordance with paragraph 815-20-25-126 and if either the forecasted transaction or the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3, an entity may adjust the critical terms of the perfectly effective hypothetical hedging instrument in accordance with paragraph 815-20-25-129 to match the hedging instrument for the following:

- The underlying reference rate

- The strike price (or prices) of the hedging option (or combination of options)

- The hedging instrument’s inflows (outflows) at its maturity date due to the underlying reference rate and strike price (or prices) of the hedging option (or combination of options).

> Conditions That Require Discontinuance of Optional Expedient for Assessing Hedge Effectiveness and Reversion to Subtopics 815-20 and 815-30

848-50-35-19 An entity shall discontinue the use of the optional expedients for assessing cash flow hedge effectiveness in paragraphs 848-50-35-1 through 35-18 if any of the following occurs:

- Neither the hedged item nor the hedging instrument references a rate that meets the scope of paragraph 848-10-15-3.

- The guidance in this Topic is superseded (see paragraph 848-10-65-1(a)(3)).

- The entity elects to cease to apply the optional expedients.

848-50-35-20 If an entity applies an optional expedient method for assessing hedge effectiveness in accordance with paragraphs 848-50-35-1 through 35-18 and the hedging relationship continues after the entity discontinues applying the optional expedient method because of a condition in paragraph 848-50-35-19, the entity shall revert to applying the qualifying criteria and hedge assessment methods in Subtopics 815-20 and 815-30 to assess whether hedge accounting may continue for subsequent reporting periods. The entity may elect any hedge assessment method in accordance with Subtopics 815-20 and 815-30, and the entity is not required to use a hedge assessment method that was used before the election of the optional expedient method in paragraphs 848-50-35-1 through 35-18. For example, an entity that is using the shortcut method optional expedient for the initial assessment of a cash flow hedging relationship in accordance with paragraph 848-50-25-6 and the subsequent assessment in accordance with paragraph 848-50-35-5 shall revert to a hedge assessment method in accordance with Subtopics 815-20 and 815-30 in assessing whether the hedging relationship continues to qualify for hedge accounting from the date that the replacement assessment method is first applied.