Accounting Standards Update No. 2020-06

August 2020

Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40)

Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity

An Amendment of the FASB Accounting Standards Codification®

The FASB Accounting Standards Codification® is the source of authoritative generally accepted accounting principles (GAAP) recognized by the FASB to be applied by nongovernmental entities. An Accounting Standards Update is not authoritative; rather, it is a document that communicates how the Accounting Standards Codification is being amended. It also provides other information to help a user of GAAP understand how and why GAAP is changing and when the changes will be effective.

For additional copies of this Accounting Standards Update and information on applicable prices and discount rates contact:

Order Department

Financial Accounting Standards Board

401 Merritt 7

PO Box 5116

Norwalk, CT 06856-5116

Please ask for our Product Code No. ASU2020-06.

FINANCIAL ACCOUNTING SERIES (ISSN 0885-9051) is published monthly with the exception of May, July, and October by the Financial Accounting Foundation, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116. Periodicals postage paid at Norwalk, CT and at additional mailing offices. The full subscription rate is $312 per year. POSTMASTER: Send address changes to Financial Accounting Series, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116. | No. 497

Copyright© 2020 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government.

|

Summary

Why Is the FASB Issuing This Accounting Standards Update (Update)?

The Board is issuing this Update to address issues identified as a result of the complexity associated with applying generally accepted accounting principles (GAAP) for certain financial instruments with characteristics of liabilities and equity. Complexity associated with the accounting is a significant contributing factor to numerous financial statement restatements and results in complexity for users attempting to understand the results of applying the current guidance. In addressing the complexity, the Board focused on amending the guidance on convertible instruments and the guidance on the derivatives scope exception for contracts in an entity’s own equity.

For convertible instruments, the Board decided to reduce the number of accounting models for convertible debt instruments and convertible preferred stock. Limiting the accounting models results in fewer embedded conversion features being separately recognized from the host contract as compared with current GAAP. Convertible instruments that continue to be subject to separation models are (1) those with embedded conversion features that are not clearly and closely related to the host contract, that meet the definition of a derivative, and that do not qualify for a scope exception from derivative accounting and (2) convertible debt instruments issued with substantial premiums for which the premiums are recorded as paid-in capital.

The Board concluded that eliminating certain accounting models simplifies the accounting for convertible instruments, reduces complexity for preparers and practitioners, and improves the decision usefulness and relevance of the information provided to financial statement users. In addition to eliminating certain accounting models, the Board also decided to enhance information transparency by making targeted improvements to the disclosures for convertible instruments and earnings-per-share (EPS) guidance on the basis of feedback from financial statement users.

The Board decided to amend the guidance for the derivatives scope exception for contracts in an entity’s own equity to reduce form-over-substance-based accounting conclusions. The Board observed that the application of the derivatives scope exception guidance results in accounting for some contracts as derivatives while accounting for economically similar contracts as equity. The Board also decided to improve and amend the related EPS guidance.

Who Is Affected by the Amendments in This Update?

The amendments in this Update affect entities that issue convertible instruments and/or contracts in an entity’s own equity.

For convertible instruments, the instruments primarily affected are those issued with beneficial conversion features or cash conversion features because the accounting models for those specific features are removed. However, all entities that issue convertible instruments are affected by the amendments to the disclosure requirements in this Update.

For contracts in an entity’s own equity, the contracts primarily affected are freestanding instruments and embedded features that are accounted for as derivatives under the current guidance because of failure to meet the settlement conditions of the derivatives scope exception related to certain requirements of the settlement assessment. The Board simplified the settlement assessment by removing the requirements (1) to consider whether the contract would be settled in registered shares, (2) to consider whether collateral is required to be posted, and (3) to assess shareholder rights. Those amendments also affect the assessment of whether an embedded conversion feature in a convertible instrument qualifies for the derivatives scope exception.

Additionally, the amendments in this Update affect the diluted EPS calculation for instruments that may be settled in cash or shares and for convertible instruments.

What Are the Main Provisions, How Do the Main Provisions Differ from Current Generally Accepted Accounting Principles (GAAP), and Why Are They an Improvement?

Convertible Instruments

Under current GAAP, there are five accounting models for convertible debt instruments. Except for the traditional convertible debt model that recognizes a convertible debt instrument as a single debt instrument, the other four models, with their different measurement guidance, require that a convertible debt instrument be separated (using different separation approaches) into a debt component and an equity or a derivative component. Convertible preferred stock also is required to be assessed under similar models.

Feedback from preparers and practitioners indicated that the current accounting guidance for convertible instruments is unnecessarily complex and difficult to navigate, resulting in applying or interpreting the guidance incorrectly or inconsistently. Consequently, accounting for convertible instruments has been the subject of a significant number of restatements.

Feedback from users of financial statements indicated that most users do not find the current separation models for convertible instruments useful and relevant because they generally view and analyze those instruments on a whole-instrument basis. Because a convertible debt instrument is going to be either repaid at maturity or converted at conversion date(s), users of financial statements asserted that separating the instrument into two components is confusing and creates a result in the financial statements that is inconsistent with their analyses. Many users also indicated that cash (coupon) interest expense is more relevant information for their analyses, rather than an imputed interest expense that results from the separation of conversion features required by GAAP. Overall, most users of financial statements stated that they would prefer a simple recognition, measurement, and presentation approach with sufficient disclosures for convertible instruments to have a simplified and consistent starting point across entities to perform their analyses.

In response to the feedback received, the Board decided to simplify the accounting for convertible instruments by removing certain separation models in Subtopic 470-20, Debt—Debt with Conversion and Other Options, for convertible instruments. Under the amendments in this Update, the embedded conversion features no longer are separated from the host contract for convertible instruments with conversion features that are not required to be accounted for as derivatives under Topic 815, Derivatives and Hedging, or that do not result in substantial premiums accounted for as paid-in capital. Consequently, a convertible debt instrument will be accounted for as a single liability measured at its amortized cost and a convertible preferred stock will be accounted for as a single equity instrument measured at its historical cost, as long as no other features require bifurcation and recognition as derivatives. By removing those separation models, the interest rate of convertible debt instruments typically will be closer to the coupon interest rate when applying the guidance in Topic 835, Interest.

The amendments in this Update provide financial statement users with a simpler and more consistent starting point to perform analyses across entities, consistent with feedback received from users. The amendments also improve the operability of the guidance and reduce, to a large extent, the complexities in the accounting for convertible instruments and the difficulties with the interpretation and application of the relevant guidance.

To further improve the decision usefulness and relevance of the information being provided to users of financial statements, the Board decided to increase information transparency by making the following disclosure amendments in this Update for convertible instruments:

- Add a disclosure objective

- Add information about events or conditions that occur during the reporting period that cause conversion contingencies to be met or conversion terms to be significantly changed

- Add information on which party controls the conversion rights

- Align disclosure requirements for contingently convertible instruments with disclosure requirements for other convertible instruments

- Require that existing fair value disclosures in Topic 825, Financial Instruments, be provided at the individual convertible instrument level rather than in the aggregate.

Additionally, for convertible debt instruments with substantial premiums accounted for as paid-in capital, the Board decided to add disclosures about (1) the fair value amount and the level of fair value hierarchy of the entire instrument for public business entities and (2) the premium amount recorded as paid-in capital.

Derivatives Scope Exception for Contracts in an Entity’s Own Equity

Under current guidance in Subtopic 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity, an entity must determine whether a contract qualifies for a scope exception from derivative accounting. This guidance must be applied to freestanding financial instruments and embedded features that have all the characteristics of a derivative instrument and freestanding financial instruments that potentially are settled in an entity’s own stock, regardless of whether the instrument has all the characteristics of a derivative instrument. The analysis to determine whether a contract meets this scope exception includes two criteria: (1) the contract is indexed to an entity’s own stock and (2) the contract is equity classified. If both of those criteria are not met, the contract must be recognized as an asset or a liability.

Under Section 815-40-25 on recognition, an entity must determine whether a contract meets specific conditions to be classified as equity (referred to as the settlement criterion). Analyzing whether a contract meets the settlement criterion involves evaluating the contract’s settlement optionality and conditions necessary for share settlement. The general concept behind the settlement criterion is that a contract that will settle in an entity’s own equity shares meets the criterion, whereas a contract that may (or will) require settlement in cash does not. The current guidance includes seven conditions for performing this assessment and explicitly precludes considering the likelihood that an event would trigger cash settlement.

The Board received feedback that stakeholders have difficulty applying the current guidance for this exception to derivative accounting because of its lack of organization, as well as that the current guidance is rules based, internally inconsistent, and often is asserted to result in form-over-substance-based accounting conclusions.

The amendments in this Update revise the guidance in Subtopic 815-40, as follows:

- Remove the following conditions from the settlement guidance:

- Settlement in unregistered shares

- Collateral

- Shareholder rights.

- Regarding the condition about failure to timely file in the settlement guidance, clarify that penalty payments do not preclude equity classification.

- Require instruments that are required to be classified as an asset or liability under paragraph 815-40-15-8A to be measured subsequently at fair value, with changes reported in earnings and disclosed in the financial statements, which is consistent with instruments that are required to be classified as an asset or a liability under Section 815-40-25 on recognition.

- Clarify that the scope of the disclosure requirements in Section 815-40-50 applies only to freestanding instruments. Embedded features are not subject to Section 815-40-50 requirements.

- Clarify that the scope of the reassessment guidance in Section 815-40-35 on subsequent measurement applies to both freestanding instruments and embedded features.

The amendments in this Update to the derivatives scope exception for contracts in an entity’s own equity change the population of contracts that are recognized as assets or liabilities. For a freestanding instrument, if the instrument qualifies for the derivatives scope exception under the amendments, an entity should record the instrument in equity. For an embedded feature, if the feature qualifies for the derivatives scope exception under the amendments, an entity should no longer bifurcate the feature and account for it separately.

EPS

In considering improvements to the EPS guidance, the Board focused on the areas included in the project’s overall scope of convertible instruments and of instruments that qualify for the derivatives scope exception for contracts in an entity’s own equity in Subtopic 815-40 and consequences of the amendments in this Update to classification, recognition, and measurement in those areas of the guidance. The amendments improve the consistency of EPS calculations by amending the guidance as follows:

- Align the diluted EPS calculation for convertible instruments by requiring that an entity use the if-converted method. The treasury stock method should no longer be used to calculate diluted EPS for convertible instruments.

- Require that the effect of potential share settlement be included in the diluted EPS calculation when an instrument may be settled in cash or shares. The amendments remove current guidance that allows an entity to rebut this presumption if it has a history or policy of cash settlement. This amendment affects any instrument that may be settled in cash or shares (other than certain liability-classified share-based payment arrangements) and, therefore, affects the diluted EPS calculation for both convertible instruments and contracts in an entity’s own equity.

- Include equity-classified convertible preferred stock that includes a down round feature within the scope of the recognition and measurement guidance for financial instruments that include down round features in Topic 260, Earnings Per Share, because the beneficial conversion features model is eliminated.

- Clarify that an average market price should be used to calculate the diluted EPS denominator in cases in which the exercise prices may change on the basis of an entity’s share price or changes in the entity’s share price may affect the number of shares that may be used to settle a financial instrument.

- Clarify that an entity should use the weighted-average share count from each quarter when calculating the year-to-date weighted-average share count.

When Will the Amendments Be Effective and What Are the Transition Requirements?

The amendments in this Update are effective for public business entities that meet the definition of a Securities and Exchange Commission (SEC) filer, excluding entities eligible to be smaller reporting companies as defined by the SEC, for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years. Early adoption is permitted, but no earlier than fiscal years beginning after December 15, 2020, including interim periods within those fiscal years. The Board specified that an entity should adopt the guidance as of the beginning of its annual fiscal year.

The Board decided to allow entities to adopt the guidance through either a modified retrospective method of transition or a fully retrospective method of transition. In applying the modified retrospective method, entities should apply the guidance to transactions outstanding as of the beginning of the fiscal year in which the amendments are adopted. Transactions that were settled (or expired) during prior reporting periods are unaffected. The cumulative effect of the change should be recognized as an adjustment to the opening balance of retained earnings at the date of adoption. If an entity elects the fully retrospective method of transition, the cumulative effect of the change should be recognized as an adjustment to the opening balance of retained earnings in the first comparative period presented.

An entity that has not yet adopted the amendments in Accounting Standards Update No. 2017-11, Earnings Per Share (Topic 260), Distinguishing Liabilities from Equity (Topic 480), Derivatives and Hedging (Topic 815): (Part I) Accounting for Certain Financial Instruments with Down Round Features, and (Part II) Replacement of the Indefinite Deferral for Mandatorily Redeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests with a Scope Exception, can early adopt the amendments in this Update for convertible instruments that include a down round feature. This early adoption is permitted for fiscal years beginning after December 15, 2019.

The Board also decided to allow all entities to irrevocably elect the fair value option in accordance with Subtopic 825-10, Financial Instruments—Overall, for any financial instrument that is a convertible security upon adoption of the amendments in this Update.

Amendments to the FASB Accounting Standards Codification ®

Summary of Amendments to the Accounting Standards Codification

1. The following table provides a summary of the amendments to the Accounting Standards Codification.

|

|

- Superseded the term beneficial conversion feature

- Added the term convertible security to Subtopics 505-10, 718-10, and 815-40

- Added the terms freestanding financial instrument and Securities and Exchange Commission (SEC) Filer to Subtopic 815-40

- Added the term contingently convertible instruments to Subtopics 470-20 and 505-10

- Added the term public business entity to Subtopics 470-20 and 815-40

|

Subtopic 260-10, Earnings Per Share—Overall

|

- Expanded the scope of the recognition and measurement guidance to include equity-classified convertible preferred stock

- Amended the method used to calculate diluted earnings per share for convertible instruments and for instruments that may be settled in cash or shares

- Amended the guidance to require the use of an average market price when calculating the diluted earnings-per-share denominator for contracts with variable prices or number of shares to be issued

- Amended the guidance about calculating year-to-date weighted average shares

|

Subtopic 470-10, Debt—Overall

|

- Includes consequential amendments

|

Subtopic 470-20, Debt—Debt with Conversion and Other Options

|

- Amended the guidance on convertible debt instruments by removing accounting models for the instruments with beneficial conversion features and cash conversion features

- Amended the disclosure guidance on convertible debt instruments

|

Subtopic 505-10, Equity—Overall

|

- Added the guidance on convertible preferred stock

|

Subtopic 718-10, Compensation—Stock Compensation—Overall

|

- Amended the guidance to require that convertible instruments within the scope of Topic 718 remain in that Topic when the instruments are fully vested

|

Subtopic 740-10, Income Taxes—Overall

|

- Removed the guidance on beneficial conversion features

|

Subtopic 815-10, Derivatives and Hedging—Overall

|

- Includes consequential amendments

|

Subtopic 815-15, Derivatives and Hedging—Embedded Derivatives

|

- Includes consequential amendments

|

Subtopic 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity

|

- Amended the guidance on the derivatives scope exception for contracts in an entity’s own equity, including related implementation and disclosure guidance

|

Subtopic 825-10, Financial Instruments—Overall

|

- Added guidance requiring fair value disclosures of convertible debt instruments at the individual instrument level

- Includes consequential amendments

|

Subtopic 835-30, Interest—Imputation of Interest

|

- Removed the reference to Subtopic 470-20 about specific accounting for interest expense of convertible debt instruments with beneficial conversion features or cash conversion features

|

2. The Accounting Standards Codification is amended as described in paragraphs 3–62. In some cases, to put the change in context, not only are the amended paragraphs shown but also the preceding and following paragraphs. Terms from the Master Glossary are in

bold type. Added text is

underlined, and deleted text is

struck out

.

Amendments to Master Glossary

3. Supersede the Master Glossary term Beneficial Conversion Feature, with a link to transition paragraph 815-40-65-1, as follows:

Beneficial Conversion Feature

A nondetachable conversion feature that is in the money at the commitment date.

4. Add the Master Glossary term Convertible Security to Subtopics 505-10, 718-10, and 815-40 as follows:

Convertible Security

A security that is convertible into another security based on a conversion rate. For example, convertible preferred stock that is convertible into common stock on a two-for-one basis (two shares of common for each share of preferred).

5. Add the Master Glossary terms Freestanding Financial Instrument and Securities and Exchange Commission (SEC) Filer to Subtopic 815-40 as follows:

Freestanding Financial Instrument

A financial instrument that meets either of the following conditions:

- It is entered into separately and apart from any of the entity’s other financial instruments or equity transactions.

- It is entered into in conjunction with some other transaction and is legally detachable and separately exercisable.

Securities and Exchange Commission (SEC) Filer

An entity that is required to file or furnish its financial statements with either of the following:

- The Securities and Exchange Commission (SEC)

- With respect to an entity subject to Section 12(i) of the Securities Exchange Act of 1934, as amended, the appropriate agency under that Section.

Financial statements for other entities that are not otherwise SEC filers whose financial statements are included in a submission by another SEC filer are not included within this definition.

6. Add the Master Glossary term Contingently Convertible Instruments to Subtopics 470-20 and 505-10 as follows:

Contingently Convertible Instruments

Contingently convertible instruments are instruments that have embedded conversion features that are contingently convertible or exercisable based on either of the following:

- A market price trigger

- Multiple contingencies if one of the contingencies is a market price trigger and the instrument can be converted or share settled based on meeting the specified market condition.

A market price trigger is a market condition that is based at least in part on the issuer’s own share price. Examples of contingently convertible instruments include contingently convertible debt, contingently convertible preferred stock, and the instrument described by paragraph 260-10-45-43, all with embedded market price triggers.

7. Add the Master Glossary term Public Business Entity to Subtopics 470-20 and 815-40 as follows:

Public Business Entity

A public business entity is a business entity meeting any one of the criteria below. Neither a not-for-profit entity nor an employee benefit plan is a business entity.

- It is required by the U.S. Securities and Exchange Commission (SEC) to file or furnish financial statements, or does file or furnish financial statements (including voluntary filers), with the SEC (including other entities whose financial statements or financial information are required to be or are included in a filing).

- It is required by the Securities Exchange Act of 1934 (the Act), as amended, or rules or regulations promulgated under the Act, to file or furnish financial statements with a regulatory agency other than the SEC.

- It is required to file or furnish financial statements with a foreign or domestic regulatory agency in preparation for the sale of or for purposes of issuing securities that are not subject to contractual restrictions on transfer.

- It has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market.

- It has one or more securities that are not subject to contractual restrictions on transfer, and it is required by law, contract, or regulation to prepare U.S. GAAP financial statements (including notes) and make them publicly available on a periodic basis (for example, interim or annual periods). An entity must meet both of these conditions to meet this criterion.

An entity may meet the definition of a public business entity solely because its financial statements or financial information is included in another entity’s filing with the SEC. In that case, the entity is only a public business entity for purposes of financial statements that are filed or furnished with the SEC.

Amendments to Subtopic 260-10

8. Amend paragraph 260-10-25-1 and add the related heading and amend paragraphs 260-10-30-1, 260-10-35-1, and 260-10-45-12B, with a link to transition paragraph 815-40-65-1, as follows:

Earnings Per Share—Overall

Recognition

> Financial Instruments That Include a Down Round Feature

260-10-25-1 An entity that presents

earnings per share (EPS) in accordance with this Topic shall recognize the value of the effect of a

down round feature in an equity-classified freestanding

financial instrument and an equity-classified convertible preferred stock (if the conversion feature has not been bifurcated in accordance with other guidance) (that is, instruments that are not convertible instruments)

when the down round feature is triggered. That effect shall be treated as a dividend and as a reduction of income available to common stockholders in

basic earnings per share, in accordance with the guidance in paragraph 260-10-45-12B. See paragraphs 260-10-55-95 through 55-97 for an illustration of this guidance.

Initial Measurement

260-10-30-1 As of the date that a down round feature is triggered (that is, upon the occurrence of the triggering event that results in a reduction of the strike price) in an equity-classified freestanding financial instrument and an equity-classified convertible preferred stock (if the conversion feature has not been bifurcated in accordance with other guidance), an entity shall measure the value of the effect of the feature as the difference between the following amounts determined immediately after the down round feature is triggered:

- The fair value of the financial instrument (without the down round feature) with a strike price corresponding to the currently stated strike price of the issued instrument (that is, before the strike price reduction)

- The fair value of the financial instrument (without the down round feature) with a strike price corresponding to the reduced strike price upon the down round feature being triggered.

Subsequent Measurement

260-10-35-1 An entity shall recognize the value of the effect of a down round feature in an equity-classified freestanding financial instrument and an equity-classified convertible preferred stock (if the conversion feature has not been bifurcated in accordance with other guidance) each time it is triggered but shall not otherwise subsequently remeasure the value of a down round feature that it has recognized and measured in accordance with paragraphs 260-10-25-1 and 260-10-30-1 through 30-2. An entity shall not subsequently amortize the amount in additional paid-in capital arising from recognizing the value of the effect of the down round feature.

Other Presentation Matters

> Basic EPS

> > Freestanding Equity-Classified Financial Instrument with a Down Round Feature

260-10-45-12B For a freestanding equity-classified financial instrument and an equity-classified convertible preferred stock (if the conversion feature has not been bifurcated in accordance with other guidance) with a down round feature, an entity shall deduct the value of the effect of a down round feature (as recognized in accordance with paragraph 260-10-25-1 and measured in accordance with paragraphs 260-10-30-1 through 30-2) in computing income available to common stockholders when that feature has been triggered (that is, upon the occurrence of the triggering event that results in a reduction of the strike price).

9. Amend paragraphs 260-10-45-16, 260-10-45-23, 260-10-45-40, and 260-10-45-44 through 45-46, add paragraphs 260-10-45-21A and its related heading and 260-10-45-45A, and supersede paragraph 260-10-45-64, with a link to transition paragraph 815-40-65-1, as follows:

> Diluted EPS and Related Topics

> > Computation of Diluted EPS

260-10-45-16 The computation of diluted EPS is similar to the computation of basic EPS except that the denominator is increased to include the number of additional common shares that would have been outstanding if the dilutive potential common shares had been issued. In

addition, in

computing the dilutive effect of convertible securities, the numerator is adjusted

in accordance with the guidance in paragraph 260-10-45-40. to add back any convertible preferred dividends and the after-tax amount of interest recognized in the period associated with any convertible debt. The numerator also is adjusted for any other changes in income or loss that would result from the assumed conversion of those potential common shares, such as profit-sharing expenses. Similar adjustments

Adjustments also may be necessary for certain contracts that provide the issuer or holder with a choice between settlement methods. See Example 1 (paragraph 260-10-55-38) for an illustration of this guidance.

> > Variable Denominator

260-10-45-21A Changes in an entity’s share price may affect the exercise price of a financial instrument or the number of shares that would be used to settle the financial instrument. For example, when the principal of a convertible debt instrument is required to be settled in cash but the conversion premium is required to (or may) be settled in shares, the number of shares to be included in the diluted EPS denominator is affected by the entity’s share price. In applying both the treasury stock method and the if-converted method of calculating diluted EPS, the average market price shall be used for purposes of calculating the denominator for diluted EPS when the number of shares that may be issued is variable, except for contingently issuable shares within the scope of the guidance in paragraphs 260-10-45-48 through 45-57. See paragraphs 260-10-55-4 through 55-5 for implementation guidance on determining an average market price.

> > Options, Warrants, and Their Equivalents and the Treasury Stock Method

260-10-45-22 The dilutive effect of outstanding call options and warrants (and their equivalents) issued by the reporting entity shall be reflected in diluted EPS by application of the treasury stock method unless the provisions of paragraphs 260-10-45-35 through 45-36 and 260-10-55-8 through 55-11 require that another method be applied. Equivalents of options and warrants include nonvested stock granted under a share-based payment arrangement, stock purchase contracts, and partially paid stock subscriptions (see paragraph 260-10-55-23). Antidilutive contracts, such as purchased put options and purchased call options, shall be excluded from diluted EPS.

260-10-45-23 Under the treasury stock method:

- Exercise of options and warrants shall be assumed at the beginning of the period (or at time of issuance, if later) and common shares shall be assumed to be issued.

- The proceeds from exercise shall be assumed to be used to purchase common stock at the average market price during the period. (See paragraphs 260-10-45-29 and 260-10-55-4 through 55-5.)

- The incremental shares (the difference between the number of shares assumed issued and the number of shares assumed purchased) shall be included in the denominator of the diluted EPS computation.

Example 15 (see paragraph 260-10-55-92) provides an illustration of this guidance. See paragraph 260-10-45-21A if the exercise price of a financial instrument or the number of shares that would be used to settle the financial instrument is variable.

> > Convertible Securities and the If-Converted Method

260-10-45-40 The dilutive effect of convertible securities shall be reflected in diluted EPS by application of the if-converted method. Under that method:

- If an entity has convertible preferred stock outstanding, the preferred dividends applicable to convertible preferred stock shall be added back to the numerator. The amount of preferred dividends added back will be the amount of preferred dividends for convertible preferred stock deducted from income from continuing operations (and from net income) in computing income available to common stockholders pursuant to paragraph 260-10-45-11.

- If an entity has convertible debt outstanding:

- Interest charges applicable to the convertible debt shall be added back to the numerator. For convertible debt for which the principal is required to be paid in cash, the interest charges shall not be added back to the numerator.

- To the extent nondiscretionary adjustments based on income made during the period would have been computed differently had the interest on convertible debt never been recognized, the numerator shall be appropriately adjusted. Nondiscretionary adjustments include any expenses or charges that are determined based on the income (loss) for the period, such as profit-sharing and royalty agreements.

- The numerator shall be adjusted for the income tax effect of (b)(1) and (b)(2).

- The convertible preferred stock or convertible debt shall be assumed to have been converted at the beginning of the period (or at time of issuance, if later), and the resulting common shares shall be included in the denominator. See paragraph 260-10-45-21A if the incremental shares are variable (such as when calculating a conversion premium).

> > > Contingently Convertible Instruments

260-10-45-44 Contingently convertible instruments shall be included in diluted EPS (if dilutive) regardless of whether the market price trigger has been met. There is no substantive economic difference between contingently convertible instruments and

conventional

convertible instruments with a market price conversion premium. The treatment for diluted EPS shall not differ because of a contingent market price trigger. The guidance provided in this paragraph also shall be applied to instruments that have multiple contingencies if one of the contingencies is a market price trigger and the instrument is convertible or settleable in shares based on meeting a market condition—that is, the conversion is not dependent (or no longer dependent) on a substantive non-market-based contingency. For example, this guidance applies if an instrument is convertible upon meeting a market price trigger or a substantive non-market-based contingency (for example, a change in control). Alternatively, if the instrument is convertible upon achieving both a market price trigger and a substantive non-market-based contingency, this guidance would not apply until the non-market-based contingency has been met. See Example 11 (paragraph 260-10-55-78) for an illustration of this guidance.

> > Contracts That May Be Settled in Stock or Cash

260-10-45-45 The effect of potential share settlement shall be included in the diluted EPS calculation (if the effect is more dilutive) for an otherwise cash-settleable instrument that contains a provision that requires or permits share settlement (regardless of whether the election is at the option of an entity or the holder, or the entity has a history or policy of cash settlement). An example of such a contract accounted for in accordance with this paragraph and paragraph 260-10-45-46 is a written call option that gives the holder a choice of settling in common stock or in cash. An election to share settle an instrument, for purposes of applying the guidance in this paragraph, does not include circumstances in which share settlement is contingent upon the occurrence of a specified event or circumstance (such as contingently issuable shares). In those circumstances (other than if the contingency is an entity’s own share price), the guidance on contingently issuable shares should first be applied, and, if the contingency would be considered met, then the guidance in this paragraph should be applied. If an entity issues a contract that may be settled in common stock or in cash at the election of either the entity or the holder, the determination of whether that contract shall be reflected in the computation of diluted EPS shall be made based on the facts available each period. It shall be presumed that the contract will be settled in common stock and the resulting potential common shares included in diluted EPS (in accordance with the relevant provisions of this Topic) if the effect is more dilutive.

Share-based payment arrangements that are payable in common stock or in cash at the election of either the entity or the grantee shall be accounted for pursuant to this paragraph and paragraph 260-10-45-46

, unless the share-based payment arrangement is classified as a liability because of the requirements in paragraph 718-10-25-15 (see paragraph 260-10-45-45A for guidance for those instruments).

If the payment of cash is required only upon the final liquidation of an entity, then the entity shall include the effect of potential share settlement in the diluted EPS calculation until the liquidation occurs. An example of such a contract is a written put option that gives the holder a choice of settling in common stock or in cash.

260-10-45-45A For a share-based payment arrangement that is classified as a liability because of the requirements in paragraph 718-10-25-15 and may be settled in common stock or in cash at the election of either the entity or the holder, determining whether that contract shall be reflected in the computation of diluted EPS shall be prepared on the basis of the facts available each period. It shall be presumed that the contract will be settled in common stock and the resulting potential common shares included in diluted EPS (in accordance with the relevant guidance of this Topic) if the effect is more dilutive. The presumption that the contract will be settled in common stock may be overcome if past experience or a stated policy provides a reasonable basis to conclude that the contract will be paid partially or wholly in cash.

260-10-45-46 A contract that is reported as an asset or liability for accounting purposes may require an adjustment to the numerator for any changes in income or loss that would result if the contract had been reported as an equity instrument for accounting purposes during the period. That adjustment is similar to the adjustments required for convertible debt in paragraph 260-10-45-40(b).

The presumption that the contract will be settled in common stock may be overcome if past experience or a stated policy provides a reasonable basis to believe that the contract will be paid partially or wholly in cash.

> Special Issues Affecting Basic and Diluted EPS

> > Participating Securities and the Two-Class Method

260-10-45-64 Paragraph superseded by Accounting Standards Update No. 2020-06.A dividend equivalent that is applied to reduce the conversion price or increase the conversion ratio of a convertible security may represent a contingent beneficial conversion feature. Guidance on whether such a dividend equivalent represents a contingent beneficial conversion feature is presented in Subtopic 470-20. That Subtopic also establishes the accounting required for contingent beneficial conversion features.

10. Amend the headings preceding paragraph 260-10-55-3, paragraphs 260-10-55-4 and 260-10-55-6 through 55-7 and the related headings, 260-10-55-32 through 55-34, 260-10-55-36A, 260-10-55-78 through 55-79 and their related heading, 260-10-55-82, and 260-10-55-84A through 55-84B, add paragraphs 260-10-55-84C through 55-84E and their related heading, and supersede paragraph 260-10-55-36, with a link to transition paragraph 815-40-65-1, as follows:

Implementation Guidance and Illustrations

> Implementation Guidance

> > Applying the Treasury Stock Method: Year-to-Date Computations

> > > Year-to-Date Computations

260-10-55-3 The number of incremental shares included in quarterly diluted EPS shall be computed using the average market prices during the three months included in the reporting period. For year-to-date diluted EPS, the number of incremental shares to be included in the denominator shall be determined by computing a year-to-date weighted average of the number of incremental shares included in each quarterly diluted EPS computation. Example 1 (see paragraph 260-10-55-38) provides an illustration of that provision.

260-10-55-3A Computation of year-to-date diluted EPS when an entity has a year-to-date loss from continuing operations including one or more quarters with income from continuing operations and when in-the-money options or warrants were not included in one or more quarterly diluted EPS computations because there was a loss from continuing operations in those quarters is as follows. In computing year-to-date diluted EPS, year-to-date income (or loss) from continuing operations shall be the basis for determining whether or not dilutive potential common shares not included in one or more quarterly computations of diluted EPS shall be included in the year-to-date computation.

260-10-55-3B Therefore:

- When there is a year-to-date loss, potential common shares should never be included in the computation of diluted EPS, because to do so would be antidilutive.

- When there is year-to-date income, if in-the-money options or warrants were excluded from one or more quarterly diluted EPS computations because the effect was antidilutive (there was a loss from continuing operations in those periods), then those options or warrants should be included in the diluted EPS denominator (on a weighted-average basis) in the year-to-date computation as long as the effect is not antidilutive. Similarly, contingent shares that were excluded from a quarterly computation solely because there was a loss from continuing operations should be included in the year-to-date computation unless the effect is antidilutive.

Example 12 (see paragraph 260-10-55-85) illustrates this guidance.

> > > > >

Average Market Price 260-10-55-4 In applying the

treasury stock method

, the

The average market price of

common stock shall represent a meaningful average. Theoretically, every market transaction for an entity’s common stock could be included in determining the average market price. As a practical matter, however, a simple average of weekly or monthly prices usually will be adequate.

260-10-55-5 Generally, closing market prices are adequate for use in computing the average market price. When prices fluctuate widely, however, an average of the high and low prices for the period that the price represents usually would produce a more representative price. The method used to compute the average market price shall be used consistently unless it is no longer representative because of changed conditions. For example, an entity that uses closing market prices to compute the average market price for several years of relatively stable market prices might need to change to an average of high and low prices if prices start fluctuating greatly and the closing market prices no longer produce a representative average market price.

> > > > >

Options and Warrants and Their Equivalents 260-10-55-6 Options or warrants to purchase convertible securities shall be assumed to be exercised to purchase the convertible security whenever the average prices of both the convertible security and the common stock obtainable upon conversion are above the exercise price of the options or warrants. However, exercise shall not be assumed unless conversion of similar outstanding convertible securities, if any, also is assumed. The {add glossary link}treasury stock method{add glossary link} shall be applied to determine the incremental number of convertible securities that are assumed to be issued and immediately converted into common stock. Interest or dividends shall not be imputed for the incremental convertible securities because any imputed amount would be reversed by the if-converted adjustments for assumed conversions.

260-10-55-7 Paragraphs 260-10-55-9 through 55-11 provide guidance on how certain

options and warrants options, warrants, and convertible securities

should be included in the computation of diluted EPS.

Conversion or exercise

Exercise of the potential common shares discussed in those paragraphs shall not be reflected in diluted EPS unless the effect is dilutive. Those potential common shares will have a dilutive effect if either of the following conditions is met:

- The average market price of the related common stock for the period exceeds the exercise price.

- The security to be tendered is selling at a price below that at which it may be tendered under the option or warrant agreement and the resulting discount is sufficient to establish an effective exercise price below the market price of the common stock obtainable upon exercise.

> > Contracts That May Be Settled in Stock or Cash

260-10-55-32 Adjustments shall be made to the numerator for contracts that are

asset or liability classified, in accordance with Section 815-40-25,

but for which the potential common shares are included in the denominator in accordance with the guidance in paragraph 260-10-45-45. as equity instruments but for which the entity has a stated policy or for which past experience provides a reasonable basis to believe that such contracts will be paid partially or wholly in cash (in which case there will be no potential common shares included in the denominator). That is, a contract that is reported as an equity instrument for accounting purposes may require an adjustment to the numerator for any changes in income or loss that would result if the contract had been reported as an asset or liability for accounting purposes during the period.

For purposes of computing diluted EPS, the adjustments to the numerator are only permitted for instruments for which the effect on net income (the numerator) is different depending on whether the instrument is accounted for as an equity instrument or as an asset or liability (for example, those that are within the scope of Subtopics 480-10 and 815-40).

260-10-55-33 The references in paragraphs 260-10-45-30 and 260-10-45-45 for share-based payment arrangements that are payable in common stock or in cash at the election of either the entity or the grantee refer to using the guidance in paragraph

260-10-45-45A 260-10-45-45

for purposes of determining whether shares issuable in accordance with such plans are included in the denominator for purposes of computing diluted EPS amounts. Accordingly, the numerator is not adjusted in those circumstances. Paragraph 260-10-55-36A illustrates these requirements.

260-10-55-34 Year-to-date diluted EPS calculations may require an adjustment to the numerator in certain circumstances. For example, for contracts

that are share settled for EPS purposes in which the counterparty controls the method of settlement and that would have a more dilutive effect if settled in shares

, the numerator adjustment is equal to the earnings effect of the change in the fair value of the asset or liability recorded pursuant to Section 815-40-35 during the year-to-date period. In that example, the number of incremental shares included in the denominator should be determined

in accordance with the guidance in paragraph 260-10-55-3 by calculating the number of shares that would be required to settle the contract using the average share price during the year-to-date period

.

260-10-55-36 Paragraph superseded by Accounting Standards Update No. 2020-06.For contracts in which the counterparty controls the means of settlement, past experience or a stated policy is not determinative. Accordingly, in those situations, the more dilutive of cash or share settlement shall be used.

260-10-55-36A The following table illustrates the guidance in paragraphs

260-10-45-45 through 45-46 and 260-10-55-32 through

55-34 55-36

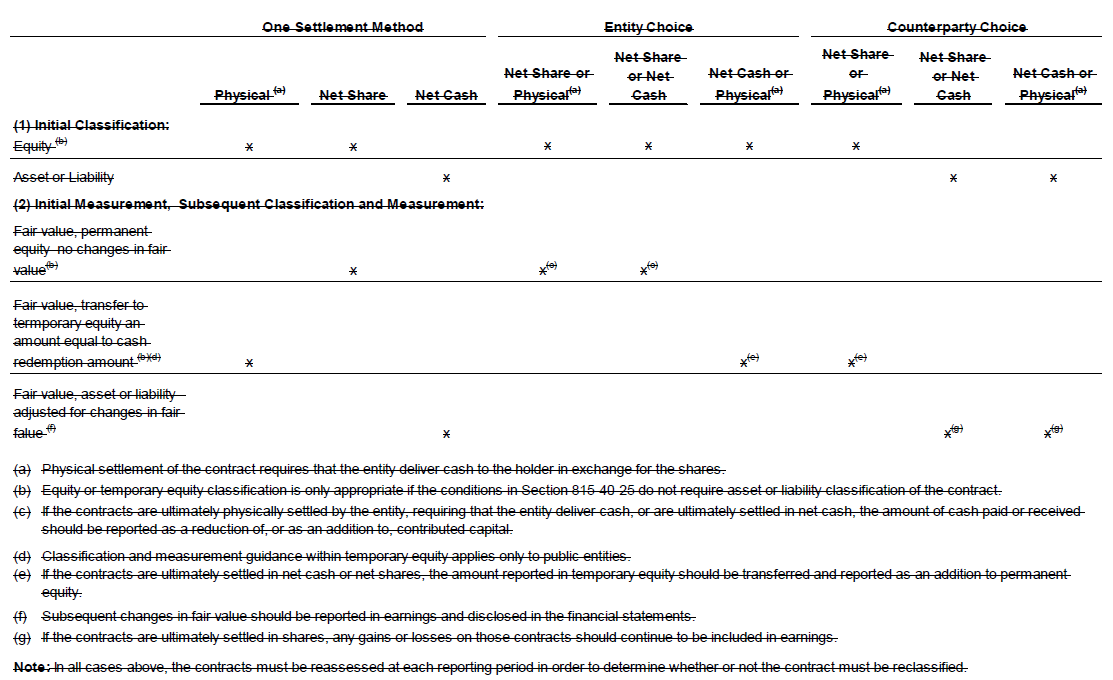

for the effects of contracts that may be settled in stock or cash on the computation of diluted EPS.

Assumed Settlement for EPS Purposes(a)

| |

Accounting for Book Purposes (per Topic 480 or 815)

| |

Adjustment Required to Book Earnings (Numerator) for Purposes of Computing Diluted Earnings per Share?(b)

| |

Adjustment Required to Number of Shares Included in Denominator? (b)

|

| |

Asset/Liability

Equity

Asset/Liability

| |

Yes (per paragraph 260-10-45-45)

No

No

| | |

(a) Note that for purposes of computing EPS, delivery of the full stated amount of cash in exchange for delivery of the full stated number of shares (physical settlement) should be considered share settlement.

(b) Except for forward purchase contracts that require physical settlement by repurchase of a fixed number of shares in exchange for cash. Topic 480 provides EPS guidance for those contracts.

> Illustrations

> > Example 11: Computation of Basic and Diluted EPS for Two

Three Examples of Contingently Convertible Instruments 260-10-55-78 The following Cases illustrate the guidance in paragraphs 260-10-45-43 through

45-44

45-46 related to diluted EPS computations for

two

three examples of contingently convertible instruments:

- Contingently convertible debt with a market price trigger (Case A)

- Contingently convertible debt with a market price trigger, issuer must settle the principal amount of the debt in cash, but may settle any conversion premium in either cash or stock (Case B).

- Convertible debt for which the principal and conversion premium can be settled in any combination of shares or cash (Case C).

260-10-55-79 Cases

A and B

A, B, and C share all of the following assumptions:

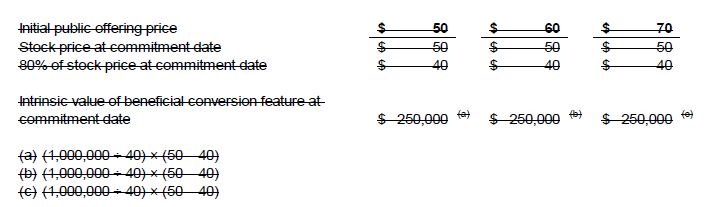

- Principal amount of the convertible debt: $1,000

- Conversion ratio: 20

- Conversion price per share of common stock: $50 Conversion price = (Convertible bond’s principal amount) ÷ (Conversion ratio) = $1,000 ÷ 20 = $50.

- Share price of common stock at issuance: $40

- Market price trigger: average share price for the year must exceed $65 (130% of conversion price)

- Interest rate: 4%

- Effective tax rate: 35%

- Shares of common stock outstanding: 2,000.

> > > Case A: Contingently Convertible Debt with a Market Price Trigger

260-10-55-81 The holder of the debt may convert the debt into shares of common stock when the share price exceeds the market price trigger; otherwise, the holder is only entitled to the par value of the debt.

260-10-55-82 The contingently convertible debt is issued on January 1, 200X, income available to common shareholders for the year ended December 31, 200X, is $10,000, and the average share price for the year is $55. The issuer of the contingently convertible debt should apply the

guidance in paragraphs 260-10-45-43 through 45-44 consensus in this Issue

, which requires the issuer to include the dilutive effect of the convertible debt in diluted EPS even though the market price trigger of $65 has not been met. In this Case, basic EPS is $5.00. (Basic EPS = [Income available to common shareholders (IACS)] ÷ [Shares outstanding (SO)] = $10,000 ÷ 2,000 shares = $5.00 per share) and applying the if-converted method to the debt instrument dilutes EPS to $4.96 (Diluted EPS computed using the if-converted method = [IACS + Interest (1-tax rate)] ÷ (SO + Potential common shares) = ($10,000 + $26) ÷ (2,000 + 20) shares = $4.96 per share.)

> > > Case B: Contingently Convertible Debt with a Market Price Trigger, Issuer Must Settle Principal in Cash, but May Settle Conversion Premium in either Cash or Stock

260-10-55-84 The issuer of the contingently convertible debt must settle the principal amount of the debt in cash upon conversion and it may settle any conversion premium in either cash or stock. The holder of the instrument is only entitled to the conversion premium if the share price exceeds the market price trigger. The contingently convertible instrument is issued on January 1, 200X, income available to common shareholders for the year ended December 31, 200X is $9,980, and the average share price for the year is $64.

260-10-55-84A The if-converted method should

not

be used to determine the earnings-per-share implications of convertible debt with the characteristics described in this Case. There would be no adjustment to the numerator in the diluted earnings-per-share computation for the cash-settled portion of the instrument

(the principal amount of the debt) because that portion will always be settled in cash

(see paragraph 260-10-45-40). The conversion premium should be included in diluted earnings per share based on the provisions of paragraphs 260-10-45-45 through 45-46 and 260-10-55-32 through

55-36A 55-36

. The convertible debt instrument in this Case is subject to other applicable guidance in Subtopic 260-10 as well, including the antidilution provisions of that Subtopic.

260-10-55-84B In this Example, basic EPS is $4.99, and diluted earnings per share is $4.98. Basic EPS = IACS ÷ SO = $9,980 ÷ 2,000 shares = $4.99 per share. Diluted EPS would be calculated using the if-converted method by determining the number of shares needed to settle the conversion premium and adding that amount to shares outstanding to calculate the diluted EPS denominator. The average market price is used to determine the dilution in accordance with paragraph 260-10-45-21A. The effect would be dilutive in this case because the average market price of the shares exceeds the conversion price. However, if the average market price of the shares was less than the conversion price, then the conversion premium would be zero and there would be no dilutive effect. Diluted EPS = IACS ÷ (SO + Potential common shares) = ($9,980) ÷ (2,000 + 4.38) shares = $4.98 per share. Potential common shares = (Conversion spread value) ÷ (Average share price) = $14 × 20 shares ÷ $64 = 4.38 shares.

> > > Case C: Convertible Debt That the Principal and Conversion Premium Can Be Settled in Any Combination of Shares or Cash

260-10-55-84C The issuer of the convertible debt can settle the principal and the conversion premium in any combination of cash or shares (the issuer has the option). Consistent with the facts in Case B, the convertible instrument is issued on January 1, 200X, income available to common shareholders for the year ended December 31, 200X, is $9,980, and the average share price for the year is $64.

260-10-55-84D The if-converted method should be used to determine the earnings-per-share implications of convertible debt. The effect of settling the principal and conversion premium in shares is included for purposes of calculating diluted earnings per share in accordance with the guidance in paragraph 260-10-45-45.

260-10-55-84E In this case, basic EPS is $4.99 (the same calculation in paragraph 260-10-55-84B), and diluted earnings per share is $4.95. Diluted EPS is calculated using the if-converted method = [IACS + Interest (1-tax rate)] ÷ (SO + Potential common shares) = (9,980 + 26) ÷ (2,000 + 20). See paragraph 260-10-55-82 for interest expense amount.

11. Amend paragraph 260-10-65-4, with no link to a transition paragraph, as follows:

Transition and Open Effective Date Information

> Transition Related to Accounting Standards Update No. 2017-11,Earnings Per Share (Topic 260) and Derivatives and Hedging (Topic 815): Part I, Accounting for Certain Financial Instruments with Down Round Features

260-10-65-4 The following represents the transition and effective date information related to Accounting Standards Update No. 2017-11, Earnings Per Share (Topic 260) and Derivatives and Hedging (Topic 815): Part I, Accounting for Certain Financial Instruments with Down Round Features:

- The pending content that links to this paragraph shall be effective as follows:

- For public business entities, for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years

- For all other entities, for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020.

- For all entities, early adoption of the pending content that links to this paragraph is permitted as of the beginning of an interim period for which financial statements (interim or annual) have not been issued or have not been made available for issuance.

- An entity shall apply the pending content that links to this paragraph using one of the following methods:

- Retrospectively to outstanding financial instruments with a down round feature by means of a cumulative-effect adjustment to the statement of financial position as of the beginning of the first fiscal year and interim period(s) in which the pending content that links to this paragraph is effective. The cumulative effect of the change shall be recognized as an adjustment of the opening balance of retained earnings in the fiscal year and interim period of adoption.

- Retrospectively to outstanding financial instruments with a down round feature for each prior reporting period presented in accordance with the guidance on accounting changes in paragraphs 250-10-45-5 through 45-10.

- An entity shall provide the following disclosures consistent with Section 250-10-50 in the period of adoption:

- The nature of the change in accounting principle

- The method of applying the change

- The cumulative effect of the change on retained earnings in the statement of financial position as of the beginning of the earliest period presented in which the pending content that links to this paragraph is effective.

- If the pending content that links to this paragraph is applied retrospectively in accordance with (c)(2), an entity shall provide both of the following disclosures:

- A description of the prior-period information that has been retrospectively adjusted, if any

- The effect of the change on income from continuing operations, net income (or other appropriate captions of changes in the applicable net assets or performance indicator), any other affected financial statement line item, and any affected per-share amounts for the current period and any prior periods retrospectively adjusted.

- An entity that issues interim financial statements shall provide the disclosures in (d) through (e) in the financial statements of both the interim period of the change and the fiscal year of the change.

- See paragraph 815-40-65-1(c) for additional information about the date of adoption and transition for convertible instruments that include a down round feature.

Amendments to Subtopic 470-10

12. Amend paragraph 470-10-50-1, with a link to transition paragraph 815-40-65-1, as follows:

Debt—Overall

Disclosure

> Disclosure of Long-Term Obligations

470-10-50-1 The combined aggregate amount of maturities and sinking fund requirements for all long-term borrowings shall be disclosed for each of the five years following the date of the latest balance sheet presented. (See

paragraph 505-10-50-11 for related disclosure guidance on redeemable securities Section 505-10-50 for disclosure guidance that applies to securities, including debt securities

.) See Example 3 (paragraph 470-10-55-10) for an illustration of this disclosure requirement.

13. Amend paragraphs 470-10-55-11 through 55-12, with a link to transition paragraph 815-40-65-1, as follows:

Implementation Guidance and Illustrations

> Illustrations

> > Example 3: Disclosure of Long-Term Obligations

470-10-55-10 This Example provides an illustration of the guidance in paragraph 470-10-50-1 for disclosures for long-term borrowings and preferred stock with mandatory redemption requirements. This Example has the following assumptions.

470-10-55-11 Entity D has outstanding two long-term

borrowings

loans, one convertible debt, and one issue of preferred stock with mandatory redemption requirements. The first

borrowing

loan is a $100 million sinking fund debenture with annual sinking fund payments of $10 million in 19X2, 19X3, and 19X4, $15 million in 19X5 and 19X6, and $20 million in 19X7 and 19X8. The second

borrowing

loan is a $50 million note due in 19X5.

The convertible debt has a principal amount of $70 million that is not convertible before maturity in 19X9. This convertible debt requires a 2 percent annual cumulative sinking fund payment of $1.4 million until settled. The $30 million issue of preferred stock requires a 5 percent annual cumulative sinking fund payment of $1.5 million until retired.

470-10-55-12 Entity D’s disclosure might be as follows.

Maturities and sinking fund requirements on long-term

debt

loans and convertible debt and sinking fund requirements on preferred stock subject to mandatory redemption are as follows (in thousands).

14. Supersede paragraph 470-10-60-2 and its related heading, with a link to transition paragraph 815-40-65-1, as follows:

Relationships

470-10-60-2 Paragraph superseded by Accounting Standards Update No. 2020-06.For guidance on contingently convertible securities, including those containing contingent conversion requirements that have not been met, see Subtopic 505-10.

Amendments to Subtopic 470-20

15. Supersede the Cash Conversion Subsections from Sections 05, 10, 15, 25, 30, 35, 40, 45, 50, and 55 of this Subtopic. [Paragraphs 470-20-15-6, 470-20-25-24, 470-20-25-26, 470-20-45-3, 470-20-50-5(d), and 470-20-55-70 are amended and moved to paragraphs 470-20-15-2D, 470-20-25-15, 470-20-45-1A, 470-20-45-1B, 470-20-50-1I, and 470-20-55-1A, respectively.]

16. Amend paragraphs 470-20-05-1 and 470-20-05-4 through 05-9 and the related heading, supersede paragraphs 470-20-05-1A and 470-20-05-12 and its related heading and the heading preceding paragraph 470-20-05-7, and add paragraphs 470-20-05-7A and 470-20-05-8A, with a link to transition paragraph 815-40-65-1, as follows:

Debt—Debt with Conversion and Other Options

Overview and Background

470-20-05-1 This Subtopic provides accounting and reporting guidance for debt (and certain preferred stock) with specific conversion features and other options as follows:

- Debt instruments with detachable warrants

- Convertible debt instruments

securities—general

- Subparagraph superseded by Accounting Standards Update No. 2020-06.

Beneficial conversion features

- Interest forfeiture

- Induced conversions

- Conversion upon issuer’s exercise of call option

- Subparagraph superseded by Accounting Standards Update No. 2020-06.

Convertible instruments issued to nonemployees for goods and services

- Own-share lending arrangements issued in contemplation of convertible debt issuance or other financing.

470-20-05-1A Paragraph superseded by Accounting Standards Update No. 2020-06.This Subtopic presents guidance in the following two Subsections:

General

Cash Conversion.

> Convertible Debt Instruments Securities—General

470-20-05-4 A convertible debt

instrument security

is a complex hybrid instrument bearing an option, the alternative choices of which cannot exist independently of one another. The holder ordinarily does not sell one right and retain the other. Furthermore the two choices are mutually exclusive; they cannot both be consummated. Thus, the

instrument security

will either be converted

into common stock

or be redeemed

for cash

. The holder cannot exercise the option to convert unless he forgoes the right to redemption, and vice versa.

470-20-05-5 A convertible Convertible

debt

instrument may offer advantages to both the issuer and the purchaser. From the point of view of the issuer, convertible debt has a lower interest rate than does nonconvertible debt. Furthermore, the issuer of convertible debt

instruments securities

, in planning its long-range financing, may view convertible debt as essentially a means of raising equity capital. Thus, if the

fair value of the underlying common stock increases sufficiently in the future, the issuer can force conversion of the convertible debt into common stock by calling the issue for redemption. Under these market conditions, the issuer can effectively terminate the conversion option and eliminate the debt. If the fair value of the stock does not increase sufficiently to result in conversion of the debt, the issuer will have received the benefit of the cash proceeds to the scheduled maturity dates at a relatively low cash interest cost.

470-20-05-6 On the other hand, the purchaser obtains an option to receive either the face or redemption amount of the

instrument security

or the number of common shares into which the

instrument security

is convertible. If the fair value of the underlying common stock increases above the conversion price, the purchaser (either through conversion or through holding the convertible debt containing the conversion option) benefits through appreciation. The purchaser may at that time require the issuance of the common stock at a price lower than the fair value. However, should the fair value of the underlying common stock not increase in the future, the purchaser has the protection of a debt security. Thus, in the absence of default by the issuer, the purchaser would receive the principal and interest if the conversion option is not exercised.

> Beneficial Conversion Features

470-20-05-7 Entities may issue convertible debt

instruments that securities and convertible preferred stock with a

beneficial conversion feature

. Those instruments

may be convertible into common stock at the lower of a conversion rate fixed at

time of issuance and the commitment date or

a fixed discount to the market price of the common stock at the date of conversion.

470-20-05-7A Entities also may issue convertible debt instruments that, by their stated terms, may be settled in cash (or other assets) upon conversion, including partial cash settlement.

470-20-05-8 Certain convertible debt instruments may have a contingently adjustable conversion ratio; that is, a conversion price that is variable based on future events such as any of the following:

- A liquidation or a change in control of an

the

entity - A subsequent round of financing at a price lower than the convertible security’s

convertible instrument’s

original conversion price - An initial public offering at a share price lower than an agreed-upon amount.

470-20-05-8A Certain convertible debt instruments may become convertible only upon the occurrence of a future event that is outside the control of the issuer or holder.

> Interest Forfeiture

470-20-05-9 When a convertible debt instrument is converted to equity securities, sometimes the terms of conversion provide that any accrued but unpaid interest at the date of conversion is forfeited by the former debt holder. This occurs either because the conversion date falls between interest payment dates or because there are no interest payment dates (a zero coupon convertible debt instrument).

> Convertible Instruments Issued to Nonemployees for Goods and Services

470-20-05-12 Paragraph superseded by Accounting Standards Update No. 2020-06.A convertible instrument that is issued to a nonemployee in exchange for goods or services or a combination of goods or services and cash and may contain a nondetachable conversion option that permits the holder to convert the instrument into the issuer’s stock. This Subtopic provides related guidance.

17. Amend paragraph 470-20-15-2 and add paragraphs 470-20-15-2A through 15-2D, with a link to transition paragraph 815-40-65-1, as follows:

Scope and Scope Exceptions

> Instruments

470-20-15-2 The guidance in this Subtopic applies to all debt instruments.

The guidance on

beneficial conversion features

and conversion features that reset applies also to convertible preferred stock. The guidance in the General Subsections does not apply to those instruments within the scope of the Cash Conversion Subsections.

The guidance on own-share lending arrangements applies to an equity-classified share-lending arrangement on an entity’s own shares when executed in contemplation of a convertible debt offering or other financing.

470-20-15-2A The guidance on convertible debt instruments in this Subtopic shall be considered after considering the guidance in the Fair Value Option Subsections of Subtopic 825-10 on financial instruments.

470-20-15-2B The guidance on convertible debt instruments in this Subtopic shall be considered after considering the guidance in Subtopic 815-15 on bifurcation of embedded derivatives for an embedded conversion option or other embedded feature (for example, an embedded prepayment option) as applicable (see paragraph 815-15-55-76A). The relevant guidance in this Subtopic does not affect an issuer’s determination under Subtopic 815-15 of whether an embedded conversion option or other embedded feature shall be separately accounted for as a derivative instrument.

470-20-15-2C The guidance in this Subtopic does not apply to a convertible debt instrument award issued to a grantee that is subject to the guidance in Topic 718 on stock compensation unless the instrument is modified as described in and no longer subject to the guidance in that Topic. The guidance in this Subtopic does not apply to stock-settled debt that is subject to the guidance in Subtopic 480-10 on distinguishing liabilities from equity or other Subtopics (see paragraph 470-20-25-14), unless the stock-settled debt also contains a substantive conversion feature (as discussed in paragraphs 470-20-40-7 through 40-10) for which all relevant guidance in this Subtopic shall be considered in addition to the relevant guidance in other Subtopics.

470-20-15-2D For purposes of determining whether an instrument is within the scope of

this Subtopic, the Cash Conversion Subsections, a

convertible preferred

stock share

shall be considered a convertible debt instrument if it has both of the following characteristics:

- It is a mandatorily redeemable financial instrument.

- It is classified as a liability under Subtopic 480-10.

For related implementation guidance, see paragraph

470-20-55-1A 470-20-55-70

.

[Content amended as shown and moved from paragraph 470-20-15-6] 18. Amend paragraph 470-20-25-1 and supersede paragraphs 470-20-25-4 through 25-9 and their related headings, with a link to transition paragraph 815-40-65-1, as follows:

Recognition

> Overall

470-20-25-1 The guidance in this Section shall be considered after consideration of the guidance in the Fair Value

Option Options

Subsections of Subtopic 825-10

on financial instruments and the guidance in Subtopic 815-15 on bifurcation of embedded derivatives, as applicable. The guidance in this Section is organized as follows:

- Debt instruments with detachable warrants

- Subparagraph superseded by Accounting Standards Update No. 2020-06.

Beneficial conversion features

- Subparagraph superseded by Accounting Standards Update No. 2020-06.

Conversion features that reset

- Convertible debt instruments

Conversion features that are not beneficial

- Subparagraph superseded by Accounting Standards Update No. 2020-06.

Convertible instruments issued to nonemployees for goods and services

- Own-share lending arrangements issued in contemplation of convertible debt issuance.

> Beneficial Conversion Features

470-20-25-4 Paragraph superseded by Accounting Standards Update No. 2020-06.The guidance in the following paragraph and paragraph 470-20-25-6 applies to all of the following instruments if the instrument is not within the scope of the Cash Conversion Subsections:

Convertible securities with beneficial conversion features that must be settled in stock

Convertible securities with beneficial conversion features that give the issuer a choice of settling the obligation in either stock or cash

Instruments with beneficial conversion features that are convertible into multiple instruments, for example, a convertible preferred stock that is convertible into common stock and detachable warrants

Instruments with conversion features that are not beneficial at the commitment date (see paragraphs 470-20-30-9 through 30-12) but that become beneficial upon the occurrence of a future event, such as an initial public offering.

470-20-25-5 Paragraph superseded by Accounting Standards Update No. 2020-06.An embedded beneficial conversion feature present in a convertible instrument shall be recognized separately at issuance by allocating a portion of the proceeds equal to the intrinsic value of that feature to additional paid-in capital. Paragraph 470-20-30-4 provides guidance on measuring intrinsic value that applies to both the determination of whether an embedded conversion feature is beneficial and the allocation of proceeds.

470-20-25-6 Paragraph superseded by Accounting Standards Update No. 2020-06.A contingent beneficial conversion feature shall be measured using the commitment date stock price (see paragraphs 470-20-30-9 through 30-12) but, as discussed in paragraph 470-20-35-3, shall not be recognized in earnings until the contingency is resolved.

470-20-25-7 Paragraph superseded by Accounting Standards Update No. 2020-06.For the application of Topic 740 to beneficial conversion features that result in basis differences, see paragraph 740-10-55-51.

> Conversion Features that Reset

470-20-25-8 Paragraph superseded by Accounting Standards Update No. 2020-06.If a convertible instrument has a conversion option that continuously resets as the underlying stock price increases or decreases so as to provide a fixed value of common stock to the holder at any conversion date, the convertible instrument shall be considered stock-settled debt and the contingent beneficial conversion option provisions of this Subtopic would not apply when those resets subsequently occur. However, the guidance in paragraph 470-20-25-5 applies to the initial recognition of such a convertible instrument, including any initial active beneficial conversion feature. Example 4 (see paragraph 470-20-55-18) illustrates application of the guidance in this paragraph

.

[Content amended and moved to paragraph 470-20-25-14] 470-20-25-9 Paragraph superseded by Accounting Standards Update No. 2020-06.For guidance on a contingent conversion feature that will reduce (reset) the conversion price if the fair value of the underlying stock declines after the commitment date to or below a specified price, see paragraph 470-20-35-4.

19. Supersede paragraphs 470-20-25-10 through 25-11 and 470-20-25-16 through 25-20 and the related headings, amend paragraph 470-20-25-12 through 25-13 and the related heading, and add paragraphs 470-20-25-14 through 25-15, with a link to transition paragraph 815-40-65-1, as follows:

> Convertible Debt Instruments Conversion Features That Are Not Beneficial

470-20-25-10 Paragraph superseded by Accounting Standards Update No. 2020-06.The guidance in paragraph 470-20-25-12 addresses debt instruments that have both of the following characteristics:

The debt instrument is convertible into common stock of the issuer or an affiliated entity at a specified price at the option of the holder.