Date: January 2019

BACKGROUND

Topic 326, Financial Instruments—Credit Losses, requires entities (and other organizations) to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts with the objective of presenting an entity’s estimate of the net amount expected to be collected on the financial assets. Under this guidance, entities will use reasonable and supportable forecasts to better inform their credit loss estimates. The standard does not require a specific credit loss method; however, it allows entities to use judgment in determining the relevant information and estimation methods that are appropriate in their circumstances.

Questions have been posed to the staff on acceptable, practical methods that may be relevant and appropriate for smaller, less complex pools of assets. Specifically, the FASB has received questions about whether the weighted-average remaining maturity (WARM) method is an acceptable method to estimate expected credit losses.

The WARM method uses an average annual charge-off rate (see calculation in Question #3 below). This average annual charge-off rate contains loss content over several vintages and is used as a foundation for estimating the credit loss content for the remaining balances of financial assets in a pool at the balance sheet date. The average annual charge-off rate is applied to the contractual term, further adjusted for estimated prepayments to determine the unadjusted historical charge-off rate for the remaining balance of the financial assets. The calculation of the unadjusted historical charge-off rate does not include a reasonable and supportable forecast period. Like other loss rate methods that can be used to estimate expected credit losses, consideration of reasonable and supportable forecasts when applying the WARM method can be accomplished in other ways, as illustrated later in this Q&A (See Question #5).

QUESTION 1

Is the WARM method an acceptable method to estimate allowances for credit losses under

Subtopic 326-20?

RESPONSE

The WARM method as described in the background section above may be an acceptable method to estimate expected credit losses under

Topic 326. Specifically, the WARM method considers an estimate of expected credit losses over the remaining life of the financial assets (that is, losses occurring through the end of the contractual term).

Paragraph 326-20-30-3 states that “…the allowance for credit losses may be determined using various methods.” The Board elaborated on its intent in paragraph BC50 of the basis for conclusions to Accounting Standards Update No. 2016-13,

Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments:

The Board has permitted entities to estimate expected credit losses using various methods because the Board believes entities manage credit risk differently and should have flexibility to best report their expectations…. The complexity of the portfolio, size of the entity, access to information, and management of the portfolio may result in approaches with varying degrees of sophistication. Because entities may have different levels of sophistication, the Board did not prescribe one type of methodology for measuring expected credit losses for financial assets measured at amortized cost.

The FASB staff believes that the WARM method is one of many methods that could be used to estimate an allowance for credit losses for less complex financial asset pools under

Subtopic 326-20.

QUESTION 2

What factors should an entity consider when determining whether to use the WARM method?

RESPONSE

There are a range of methods currently in use under the incurred loss method scaled to the size and the complexity of the entities that use them, ranging from simple spreadsheet calculations to complex econometric models. It is expected that entities will continue to employ an array of methods when Update 2016-13 is implemented. However, the complexity and sophistication of the methods used should consider the complexity and sophistication of the credit risk management processes being performed by the entity for specific pools of financial assets.

There is no expectation that a less complex entity should have to implement a sophisticated model to satisfy the requirements of Update 2016-13. If an entity is using a loss rate-based method today, that entity may be able to continue with a comparable method, including the WARM method. However, compared with the method it uses today to estimate incurred losses, the entity’s assumptions and inputs will need to change to arrive at an estimate for expected credit losses that contemplates the contractual term of the financial assets adjusted for prepayments as well as reasonable and supportable forecasts.

In selecting a specific method, an entity should consider whether the method is appropriate for estimating the reserve for a pool of financial assets. Consideration should be given to the complexity, size, and composition of the pool of financial assets, and the entity’s access to information (for example, is the pool homogenous with sufficient size and loss history with a predictive pattern) as well as the size of the entity and the risk-management strategy for the pool (for example, while the entity may be large and complex, the specific pool could be insignificant to the entity, lending itself to a less complex risk management strategy).

Certain common challenges can exist regardless of the loss rate method selected by an entity. These include, but are not limited to, situations involving minimal loss history, losses that are sporadic with no predictive patterns, low numbers of loans in each pool, data that is only available for a short historical period, a composition that varies significantly from historical pools of financial assets, or changes in the economic environment. In some instances, these challenges will be minor and can be effectively resolved using qualitative adjustments thereby making the WARM method acceptable. In other instances, these challenges will be more significant, and an entity may find that the WARM method is inappropriate for its situation.

QUESTION 3

How can an entity estimate the allowance for credit losses using a WARM method?

RESPONSE

The FASB staff has adapted the following example from a webinar the staff participated in with the bank regulatory agencies. For additional educational information, the archived webinar hosted by the bank regulatory agencies is available using this

link. The following example focuses on using annualized loss data as a foundation for estimating the allowance for credit losses for a pool of financial assets and is illustrative in nature. The facts and circumstances of an entity’s situation should be considered.

Fact Pattern

Estimate the allowance for credit losses as of 12/31/2020 Pool of financial assets of similar risk characteristics Management expects the following in 2021 and 2022: Management cannot reasonably forecast beyond 2022 Assume 0.25% qualitative adjustment to represent both current conditions and reasonable and supportable forecasts

|

The example illustrates estimating an allowance for credit losses on a pool of financial assets as of December 31, 2020. The pool has an outstanding balance of approximately $13.98 million as of December 31, 2020 and has financial assets with a contractual life of 5 years. The $13.98 million amortized cost is for a pool of financial assets with similar credit risk characteristics.

Management expects a rise in unemployment rates for 2021 and 2022 and cannot reasonably forecast beyond 2022. The example assumes a 0.25% qualitative adjustment for current conditions and reasonable and supportable forecasts discussed further below. It is important to note that this input will be a significant assumption when estimating expected credit losses under Update 2016-13 because it represents amounts for the current conditions and reasonable and supportable forecast. Moreover, because the example is for illustrative purposes, the staff has not assumed a specific type of financial asset pool given the breadth of products that exist in the market place and the specific facts and circumstances that may exist for a particular entity. Rather, the calculations are meant to depict the mechanics of the model in various ways. Therefore, as noted in the example calculations, an entity will need to determine if adjustments need to be made to historical loss data in accordance with paragraph 326-20-30-8 in addition to the reasonable and supportable forecasts.

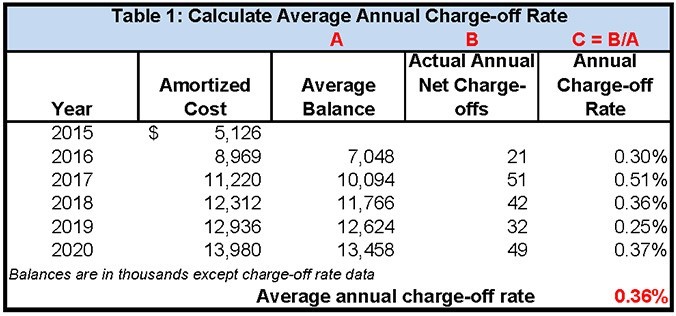

Step 1: Calculate Annual Charge-Off Rate

View image

View image

In Table 1 above:

Red bolded number of 0.36% is an average of 5 years of annual charge-off rates.

The historical time period used to determine the average annual charge-off rate is a significant judgment that will need to be properly supported and documented in accordance with paragraph 326-20-30-8. For this example, assume the entity compared historical information for similar financial assets with the current and forecasted direction of the economic environment, and believes that its most recent 5-year period is a reasonable period on which to base its expected credit-loss-rate calculation after considering the underwriting standards and contractual terms for loans that existed over the historical period in comparison with the current pool. Additionally, assume the entity considered whether any adjustments to historical loss information in accordance with paragraph 326-20-30-8 were needed before considering adjustments for current conditions and reasonable and supportable forecasts but determined that none were necessary. It should be noted that this is a simplified example using a generic pool. An entity that estimates the allowance for credit losses using the WARM method (or any method) should determine if its historical loss information needs to be adjusted for changes in underwriting standards, portfolio mix, or asset term within the pool at the reporting date.

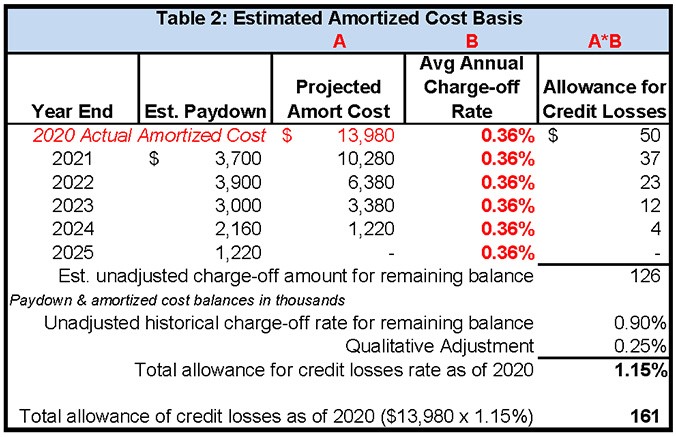

Step 2: Estimate the Allowance for Credit Losses

View image

View image

In Table 2 above:

First column titled “Year End” displays subsequent years, until 2025, which represents the time anticipated for the pool to be paid off.

Second column titled “Est. Paydown” represents expected payments in the future periods until the pool is expected to fully pay off. Management will need to estimate the future paydowns, which includes the scheduled payments + prepayments.

Note: Do not include the expected credit losses in this column. Paydowns should include scheduled payments and non-credit related prepayments.

Note: Estimated prepayments are also a significant judgment that will need to be properly supported and documented.

3. Third column titled “Projected Amort Cost”:

Begin with $13.98MM outstanding balance as of the balance sheet date of 12/31/2020.

- Subtract projected paydowns from the “Est. Paydown” column to estimate future projected amortized cost for each of the remaining years of the pool’s life (for example, $13,980M minus $3,700M equals $10,280M).

4. Fifth column titled “Allowance for Credit Losses”:

Take each of the future years’ projected amortized cost and multiply by the average annual charge-off rate, thereby estimating each of the remaining years’ losses and aggregating to estimate the cumulative losses (for example, in the first year, $13.98MM of amortized cost is multiplied by the average annual charge-off rate of 0.36% for a first year’s credit loss estimate of $50K dollars).

For the second year, which is 2022, the $10.28MM representing the ending balance as of 2021 and the beginning balance as of 2022 is multiplied by the average annual charge-off rate of 0.36% to estimate the second year’s credit losses of $37K dollars. This process is repeated for each remaining year.

Sum the last column to estimate the total expected credit losses of $126K dollars.

Note: This is not the full allowance for credit losses because the entity has not yet accounted for current conditions and reasonable and supportable forecasts.

Convert $126K of expected losses into a loss rate of 0.90% by dividing $126K by the amortized cost of $13.98MM.

5. Finally, add 0.25% of qualitative adjustments as an assumption established as part of the fact pattern of the example to estimate the allowance for credit losses rate of 1.15%. The 1.15% is multiplied by $13.98MM to estimate the total allowance for credit losses of $161K dollars.

Note: 0.25% is a significant assumption made by management that will need to be adequately documented and supported. For this example, in accordance with paragraph 326-20-55-4, the entity considered significant factors that could affect the expected collectability of the amortized cost basis of the pool and determined that the primary factor is the unemployment rate. As part of this analysis, assume that the entity observed that the unemployment rate has increased as of the current reporting period date. Based on current conditions and reasonable and supportable forecasts, the entity expects that unemployment rates are expected to increase further over the next one to two years. To adjust the historical loss rate to reflect the effects of those differences in current conditions and forecasted changes, the entity estimates a 25-basis-point increase in credit losses incremental to the 0.9 percent historical lifetime loss rate related to the expected deterioration in unemployment rates. Management estimates that the incremental 25-basis-point increase based on its knowledge of historical loss information during past years in which there were similar trends in unemployment rates. Management is unable to support its estimate of expectations for unemployment rates beyond the reasonable and supportable forecast period. Under this loss-rate method, the incremental credit losses for the current conditions and reasonable and supportable forecast (the 25 basis points) is added to the 0.9 percent rate that serves as the basis for the expected credit loss rate. No further reversion adjustments are needed because the entity has applied a 1.15% loss rate where it has immediately reverted into historical losses that reflect the contractual term in accordance with paragraphs 326-20-30-8 through 30-9. This approach reflects an immediate reversion technique for the loss-rate method. It is important to note that the 25-basis-point increase reflects the entity’s estimate of the incremental losses in years 2021 and 2022 from unemployment and assumes no incremental losses for the remaining years. Further, the reversion technique selected by the entity is a significant assumption that will need to be supported by management and is not a policy election or practical expedient.

QUESTION 4

The example in question #3 provides one way to estimate the allowance for credit losses using the WARM method. Are there other ways to perform the WARM estimation?

RESPONSE

Yes, there may be other acceptable ways for estimating the allowance for credit losses using a WARM method. An entity could choose to do the following:

Step 1: Calculate Annual Charge-Off Rate

Step 1 is the same. Therefore, entities should follow the steps above in Table 1 for determining the average annual charge-off rate.

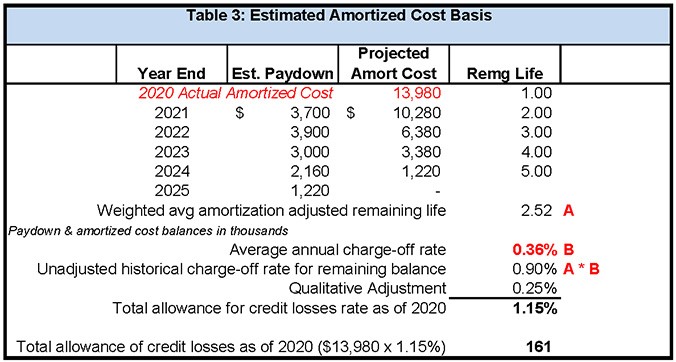

Step 2: Estimate the Allowance for Credit Losses

View image

View image

In Table 3 above:

1. The first three columns labeled “Year End,” “Est. Paydown,” and “Project Amort Cost” are identical to the estimation above in Question 3.

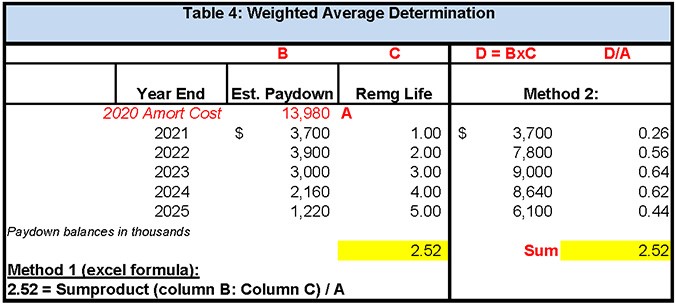

2. The last column titled “Remg Life” is used to determine 2.52 years of weighted-average amortization adjusted contractual life (see Table 4 for calculation). This column represents the time period that the “Projected Amortized Cost” will remain outstanding.

For example, assume that all paydowns are provided on the last day of the year. Therefore, the numbers shown in the “Estimated Paydown” column will occur on December 31st of every year. Consequently, every single dollar of 12/31/2020’s outstanding amount of $13.98MM will have a life of 1 year because some of that amount will be paid down at the end of the year. Therefore, the “remaining life” of $13.98MM is 1 year. Applying the same logic to the “Projected Amort Cost” balance in year 2021, every single dollar of 2021’s ending balance of $10.28MM will have a life of 2 years.

Note: The “Remg Life” column represents the number of years the entire “Projected Amort Cost” will be outstanding. For purposes of this example, the staff has made a simplifying assumption that all paydowns occur at the end of the year. Those numbers likely will be fractions of years (for example, 0.5, 1.5, 2.5, and so on) depending on when the paydowns are estimated to occur. Management will need to estimate and support the timing of those paydowns.

3. An entity should use the numbers in the table above to determine 2.52 years. This can be done in the following manner:

View image

View image

4. 2.52 years are multiplied by the average annual charge-off rate of 0.36% to arrive at 0.90% representing the unadjusted historical charge-off rate for the remaining balance.

5. In the example provided, the entity would add the same 0.25% of qualitative adjustment to arrive at the allowance for credit losses rate of 1.15%. The 1.15% is multiplied by $13.98MM to arrive at the total allowance for credit losses of $161K dollars.

The examples in questions #3 and #4 use simplifying assumptions to arrive at the answers calculated. Entities should be aware that all assumptions could have a significant effect on the ultimate allowance for credit losses estimated. Examples of those assumptions include, but are not limited to, the following: the estimated payoff profile considering contractual terms and any estimated prepayments (for example, straight line, amortizing or bullet loan), the historical time period an entity references as representative of the current pool’s remaining contractual life (for example, the most recent past 5 years or a different 5-year period representing the characteristics of the current pool), and the qualitative factors considered (for example, any qualitative factors that may be used to adjust historical information as discussed in Step 1 of Question #3 above or those qualitative factors used to adjust historical information for reasonable and supportable forecasts as discussed in Question #5 below). Entities should consider the guidance in paragraph 326-20-30-8, which states:

Historical credit loss experience of financial assets with similar risk characteristics generally provides a basis for an entity’s assessment of expected credit losses. Historical loss information can be internal or external historical loss information (or a combination of both). An entity shall consider adjustments to historical loss information for differences in current asset specific risk characteristics, such as differences in underwriting standards, portfolio mix, or asset term within a pool at the reporting date or when an entity’s historical loss information is not reflective of the contractual term of the financial asset or group of financial assets.

QUESTION 5

When an entity implements CECL using a loss rate method such as the WARM method, is it acceptable to adjust historical loss information for current conditions and the reasonable and supportable forecasts through a qualitative approach as was done in the example rather than a quantitative approach?

RESPONSE

Yes. If adjustments to historical loss information are appropriate, an entity could use a qualitative approach to adjust its historical data for current conditions and reasonable and supportable forecasts. As noted below, Update 2016-13 does not require a quantitative analysis. Nevertheless, an entity should maintain appropriate documentation, commensurate with its complexity and sophistication to support its qualitative adjustments and the effect of the relevant qualitative factors on the measurement of expected credit losses. Paragraph 326-20-30-9 states in part:

An entity shall not rely solely on past events to estimate expected credit losses. When an entity uses historical loss information, it shall consider the need to adjust historical information to reflect the extent to which management expects current conditions and reasonable and supportable forecasts to differ from the conditions that existed for the period over which historical information was evaluated. The adjustments to historical loss information may be qualitative in nature and should reflect changes related to relevant data (such as changes in unemployment rates, property values, commodity values, delinquency, or other factors that are associated with credit losses on the financial asset or in the group of financial assets). [Emphasis added.]

The example provided in this Q&A portrays a situation in which an entity has determined the loss rate of the pool of financial assets using historical information that is representative of the current pool. This historical information is then adjusted for how management expects the credit losses on the current pool to differ from the historical experience used as the starting point for estimating the expected credit losses on the pool. This approach is consistent with the guidance provided in paragraph 326-20-30-9 and is an acceptable method to determine adjustments for current conditions and reasonable and supportable forecasts. The Board provided an example in

Topic 326 that takes a similar approach and was specifically directed at assisting community banks and credit unions with implementation after receiving feedback from those entities. That example is as follows:

> > Example 1: Estimating Expected Credit Losses Using a Loss-Rate Approach (Collective Evaluation) 326-20-55-18 This Example illustrates one way an entity may estimate expected credit losses on a portfolio of loans with similar risk characteristics using a loss rate approach. 326-20-55-19 Community Bank A provides 10-year amortizing loans to customers. Community Bank A manages those loans on a collective basis based on similar risk characteristics. The loans within the portfolio were originated over the last 10 years, and the portfolio has an amortized cost basis of $3 million. 326-20-55-20 After comparing historical information for similar financial assets with the current and forecasted direction of the economic environment, Community Bank A believes that its most recent 10-year period is a reasonable period on which to base its expected credit-loss-rate calculation after considering the underwriting standards and contractual terms for loans that existed over the historical period in comparison with the current portfolio. Community Bank A’s historical lifetime credit loss rate (that is, a rate based on the sum of all credit losses for a similar pool) for the most recent 10-year period is 1.5 percent. The historical credit loss rate already factors in prepayment history, which it expects to remain unchanged. Community Bank A considered whether any adjustments to historical loss information in accordance with paragraph 326-20-30-8 were needed, before considering adjustments for current conditions and reasonable and supportable forecasts, but determined none were necessary. 326-20-55-21 In accordance with paragraph 326-20-55-4, Community Bank A considered significant factors that could affect the expected collectibility of the amortized cost basis of the portfolio and determined that the primary factors are real estate values and unemployment rates. As part of this analysis, Community Bank A observed that real estate values in the community have decreased and the unemployment rate in the community has increased as of the current reporting period date. Based on current conditions and reasonable and supportable forecasts, Community Bank A expects that there will be an additional decrease in real estate values over the next one to two years, and unemployment rates are expected to increase further over the next one to two years. To adjust the historical loss rate to reflect the effects of those differences in current conditions and forecasted changes, Community Bank A estimates a 10-basis-point increase in credit losses incremental to the 1.5 percent historical lifetime loss rate due to the expected decrease in real estate values and a 5-basis-point increase in credit losses incremental to the historical lifetime loss rate due to expected deterioration in unemployment rates. Management estimates the incremental 15-basis-point increase based on its knowledge of historical loss information during past years in which there were similar trends in real estate values and unemployment rates. Management is unable to support its estimate of expectations for real estate values and unemployment rates beyond the reasonable and supportable forecast period. Under this loss-rate method, the incremental credit losses for the current conditions and reasonable and supportable forecast (the 15 basis points) is added to the 1.5 percent rate that serves as the basis for the expected credit loss rate. No further reversion adjustments are needed because Community Bank A has applied a 1.65 percent loss rate where it has immediately reverted into historical losses reflective of the contractual term in accordance with paragraphs 326-20-30-8 through 30-9. This approach reflects an immediate reversion technique for the loss-rate method. 326-20-55-22 The expected loss rate to apply to the amortized cost basis of the loan portfolio would be 1.65 percent, the sum of the historical loss rate of 1.5 percent and the adjustment for the current conditions and reasonable and supportable forecast of 15 basis points. The allowance for expected credit losses at the reporting date would be $49,500.