|

Memo No.

Issue Date

Meeting Date(s)

|

7

June 1, 2018

TRG Meeting June 11, 2018

|

Contacts | Seth Drucker | Co-author, Practice Fellow | Ext. 317 |

| Jared Cline | Co-author, Postgraduate Technical Assistant | Ext. 388 |

| Damon Romano | Practice Fellow | Ext. 334 |

| Jay Shah | Project Manager | Ext. 340 |

| Trent LaFrano | Postgraduate Technical Assistant | Ext. 239 |

| Shayne Kuhaneck | Assistant Director | Ext. 386 |

Project | Transition Resource Group for Credit Losses |

Project Stage | Post-Issuance |

|

Disclaimer: This paper has been prepared for discussion at a public meeting of the Transition Resource Group for Credit Losses. It does not purport to represent the views of any individual members of the Board or staff. Comments on the application of generally accepted accounting principles (GAAP) do not purport to set out acceptable or unacceptable application of GAAP. Stakeholders are strongly encouraged to listen to feedback about this staff paper from TRG members and Board members during the TRG meeting and to read the meeting summary, which will be prepared by the staff after the meeting.

Memo Purpose

1. The purpose of this memo is to provide a summary of the following:

(a) The documents presented to the Transition Resource Group (TRG) members for the June 11, 2018 TRG for Credit Losses meeting

(b) Outreach that the staff performed in preparing the memos for the TRG meeting

(c) Other TRG submissions that are not being discussed at the TRG meeting

(d) Technical inquiries that the staff has recently answered regarding the amendments in Accounting Standards Update No. 2016-13, Financial Instruments-Credit Losses: Measurement of Credit Losses on Financial Instruments.

Documents for the Meeting

2. The following memos have been published and distributed to the TRG members in advance of the meeting:

(a) Memo No. 8, “Capitalized Interest”

(b) Memo No. 9, “Accrued Interest”

(c) Memo No. 10, “Transfer of Loans from Held for Sale to Held for Investment and Transfer of Credit Impaired Debt Securities from Available-for-Sale to Held-to-Maturity”

(d) Memo No. 11, “Recoveries”

(e) Memo No. 12, “Refinancing and Loan Prepayments”

3. The staff will introduce each of these topics for discussion at the meeting.

Staff Outreach Performed

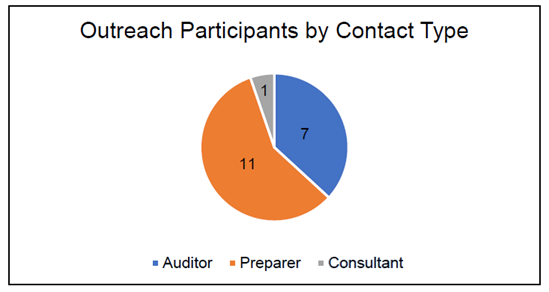

4. In preparing the memos for the TRG meeting, the staff reviewed the initial submissions from the AICPA’s Depository and Lending Institutions Expert Panel (DIEP) and performed separate outreach with individual preparers, auditors, and consultants to gain a better understanding of the issues and how they relate to each stakeholder group. The following graph summarizes the outreach performed:

Note: Preparers included large (>$1T in assets) and small (~$25B in assets) financial institutions, a government-sponsored entity, and nonfinancial institutions.

Other TRG Submissions

5. In addition to the five topics presented in the memos listed in paragraph 2, the staff received two other TRG submissions from the DIEP. The two other submissions discussed the following issues:

(a) Fair Value Option: A request for the FASB to allow a one-time election to apply the fair value option (FVO) to existing financial instruments upon adoption of Update 2016-13. This request would allow entities who choose to elect the FVO for instruments going forward to avoid having two different accounting models for their portfolios (that is, CECL and fair value). In addition to the TRG submission, the FASB has received multiple agenda requests for applying the FVO at transition.

(b) Nonpublic Business Entity Transition: A request for the FASB to consider clarifying the effective date and transition methodology language for nonpublic business entities to have an additional year from public SEC filers to adopt the amendments in Update 2016-13. Stakeholders have indicated that as written, nonpublic business entities with calendar year-ends would have to calculate their allowance for credit losses under the new amendments on January 1, 2021 to comply with the guidance. Therefore, if the FASB intended to provide additional time for nonpublic business entities to implement the amendments, stakeholders have indicated that the Board should clarify the guidance. In addition to the TRG submission, the FASB has received an agenda request for this issue.

6. For these issues, there does not appear to be disagreement among stakeholders about (a) what the guidance requires or (b) the potential solutions. Rather, these submissions are requests for additional transition relief and require the Board’s action. Consequently, the staff will bring these issues before the Board for discussion in the near term.

Recent Technical Inquiries

Loans and Receivables between Entities under Common Control

7. Paragraph 326-20-15-3(f) indicates that loans and receivables between entities under common control are not within the scope of the guidance in Subtopic 326-20, Financial Instruments—Credit Losses- Measured at Amortized Cost. A stakeholder asked the staff at which reporting level this scope exception should be applied (that is, parent or subsidiary).

8. To respond to the inquiry, the staff reviewed the meeting materials and archived webcast for the Board meeting at which this issue was discussed. In the materials, all common control arrangements (parent subsidiary, subsidiary-parent, or subsidiary-subsidiary) were considered. As part of those deliberations it was noted that in any of the arrangements described, the parent could require the forgiveness of a loan, and it is rare in practice for an entity under common control to pursue collection efforts for a related-party loan due from another entity under common control. Consequently, the Board agreed with the staff’s recommendation that these receivables should be exempt from the CECL model. Therefore, the staff informed the inquirer that it was the Board’s intent to provide this scope exception at all standalone reporting levels (that is, parent and subsidiary).

9. The staff plans no further work on this issue.

Gains and Losses on Subsequent Disposition of Leased Assets

10. Paragraph 326-20-15-2(b) specifically includes net investments in leases recognized by a lessor in accordance with Topic 842, Leases, within the scope of the guidance in Subtopic 326-20. Lessors with net investments in leases are in a unique situation relative to lenders with other financing receivables because the leased asset returns to the lessor upon early termination of the lease or the end of the lease term. At that point, the lessor may either sell or re-lease the leased assets to further derive cash flows from them. Several stakeholders asked the staff how expected gains and losses on the subsequent disposition of leased assets should be treated when measuring expected credit losses under Subtopic 326-20 on a portfolio of net investments in leases. Specifically, the stakeholders asked whether expected gains on the disposition should be considered in the calculation of the allowance.

11. After conducting outreach and reviewing Board materials, the staff believes that entities should estimate expected cash flows from the subsequent disposition of leased assets (whether those result in expected gains or losses on disposal) when calculating expected credit losses on a portfolio of net investments in leases under the guidance in Subtopic 326-20 if that estimate is reasonable and supportable consistent with the treatment of other inputs to the calculation of expected credit losses. The staff notes that the leasing guidance requires entities to include the cash flows (and therefore the resulting gain or loss) on the disposition of leased assets following the end of the lease term in the analysis of a single net investment in a lease which was clarified as part of the latest codification improvements project on leases. The staff does not view the pool-level assessment to preclude including cash flows from the subsequent disposition of leased assets expected to result in gains on disposal from the calculation of expected credit losses.

12. The staff plans no further work on this issue.

Billed Operating Lease Receivables

13. A stakeholder asked the staff to clarify whether billed operating lease receivables are within the scope of the guidance in Subtopic 326-20. The stakeholder noted that the guidance does not seem to be clear because:

(a) Topic 842 has specific guidance in paragraph 842-30-25-13 indicating that if the assessment of collectibility of an operating lease changes, any amount of lease income recognized that has not been collected should be reversed through a current-period adjustment to lease income

(b) However, the scope of Subtopic 326-20 includes financing receivables and billed operating lease receivables appear to meet that definition.

14. The staff believes that operating lease receivables are not within the scope of Topic 326. In addition to the guidance in Topic 842 noted above, paragraph 326-20-15-2 explicitly states that the guidance in that Topic only applies to the net investment in leases recognized by a lessor and does not refer to operating leases. In addition, the staff notes that the conforming amendments made in Topic 326 to Topic 842 were made only to sections that discusses sales-type and direct financing leases, and no changes were made to the operating leases sections. Therefore, the staff believes that it was never the Board’s intent to include operating leases within the scope of Subtopic 326-20. Therefore, the staff believes that Topic 842 would be followed for purposes of operating leases, and any change in assessment of collectibility for operating leases would be recognized through lease income.

15. The staff plans no further work on this issue.