Appendix A

CREDIT CARD ILLUSTRATIONS

NOTE: The illustrations depicted in this appendix are simplified in nature and are meant to contrast the differences in estimating the life of a credit card receivable where the fundamental question is focused on whether future expected payments should be allocated to the measurement date balance or the measurement date balance and potential future funding. In practice, credit card receivables are evaluated for credit losses on a pooled basis, not on an individual loan basis. For credit card receivables, lenders do not project future payments, future uses of available credit, or credit losses at the individual loan level. However, to illustrate the impact of different payment allocation concepts on the life of a credit card receivable, it is helpful to consider examples which isolate an individual account balance. Understanding the life of the measurement date receivable is necessary to apply the current expected credit loss methodology.

The allowance for loan losses on a pool of receivables collectively evaluated for credit losses is not specifically allocated to individual loans within the pool. Rather, expected losses associated with an individual account would be provided for through the allowance on the pool as a whole. However, these examples illustrate what the current expected credit loss would be on an individual credit card receivable under the circumstances described if the receivable were actually evaluated on an individual basis. Therefore, readers should not assume the specific amounts allocated to each year are representative of what an entity would determine the actual amounts to be under either scenario as part of its credit loss assessment process. That is, the amounts illustrated are assumed to be more than the minimum payment, interest and fees are accrued and paid in each period to isolate changes in principal amounts owed, the individual account holder is assumed to continue to actively use the credit card, payments are held constant over time, and the loss calculated is illustrated on an individual account, none of which are meant to represent an actual fact pattern, or for that matter represent a realistic process, but are simply being used to isolate the issue raised.

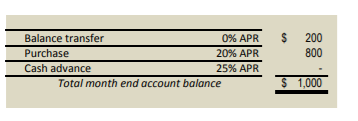

Measurement date receivable detail: components of balance

A credit card issuing bank has a pool of credit card receivables carried at amortized cost. At the end of Month 0, one receivable balance within the pool is made up of the following components:

For purposes of these illustrations, two simplifying assumptions have been incorporated: (1) monthly interest is computed using a composite interest rate of 16% applied to the prior month ending balance, and (2) each month, the entire cardholder payment is allocated first to the component bearing the highest rate of interest, and then to each successive component bearing the next highest rate of interest, until the payment is exhausted (this method is hereinafter described as "consistent with federal bank regulatory requirements"). It should be noted, however, that under federal bank regulations this payment allocation hierarchy need only be applied to the amount of the monthly cardholder payment that exceeds the minimum payment.

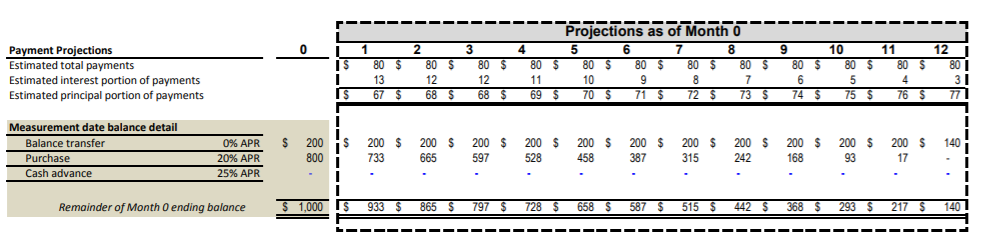

Illustration 1: Current GAAP (ASC 450-20) with 12-month loss emergence period |

- The entity has determined that the loss emergence period (the time from a loss-triggering event until charge-off) associated with its credit card receivables is 12 months.

At the end of Month 0, the entity estimates incurred losses associated with the Month 0 ending balance pursuant to ASC 450-20. The entity concludes it is not probable that a charge-off will occur on this account over the next 12 months and, therefore, that no loss has been incurred on the balance as of Month 0. Accordingly, pursuant to ASC 450-20, no allowance is accrued for this receivable as of the end of Month 0.

The table below illustrates the forecasted collections for the subsequent 12 months. Projected attrition of the Month 0 balance is based on the application of cardholder payments in a manner consistent with federal bank regulatory requirements.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE LIFE OF THE MEASUREMENT DATE RECEIVABLE

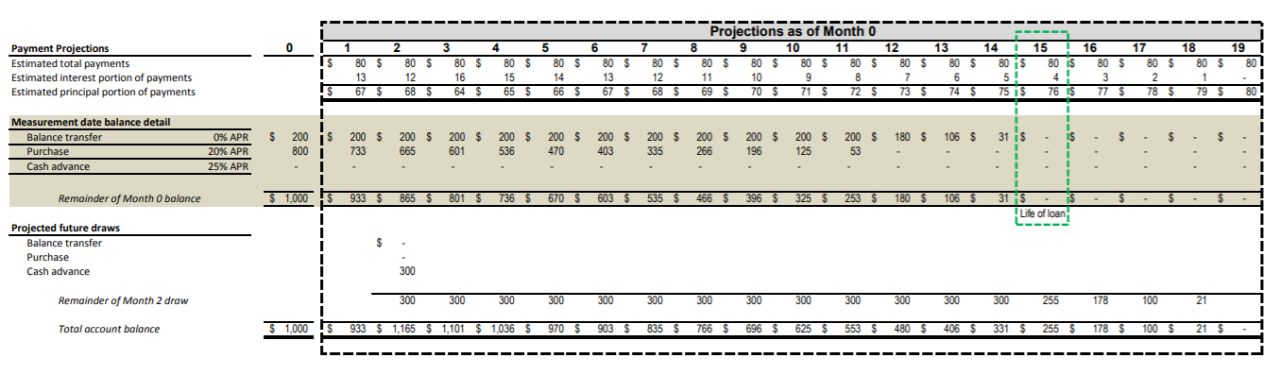

Illustration 2: CECL (ASC 326-20), VIEW A, looking forward from Month 0 |

- Assume the entity forecasts that (a) the borrower will draw $300 in the form of a cash advance at the end of Month 2 and (b) payments will be $80 per month At the end of Month 0, the entity applies View A in determining the life of the measurement date receivable balance.

The approach under View A is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying each future month's forecasted payment to the measurement date balance only, until that balance is fully repaid or until payments cease. As part of that analysis, View A applies payments to the measurement date balance in a manner consistent with federal bank regulatory requirements. Because the unused line of credit associated with the account is unconditionally cancellable, the entity does not consider projected future draws on it when evaluating the expected loss on the Month 0 balance.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View A. Based on the forecasted collections and applying the View A allocation approach, the life of the Month 0 balance is 15 months. Under this view, the balance remaining at the end of Month 15 and beyond relates to the draw made in Month 2.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE LIFE OF THE MEASUREMENT DATE RECEIVABLE

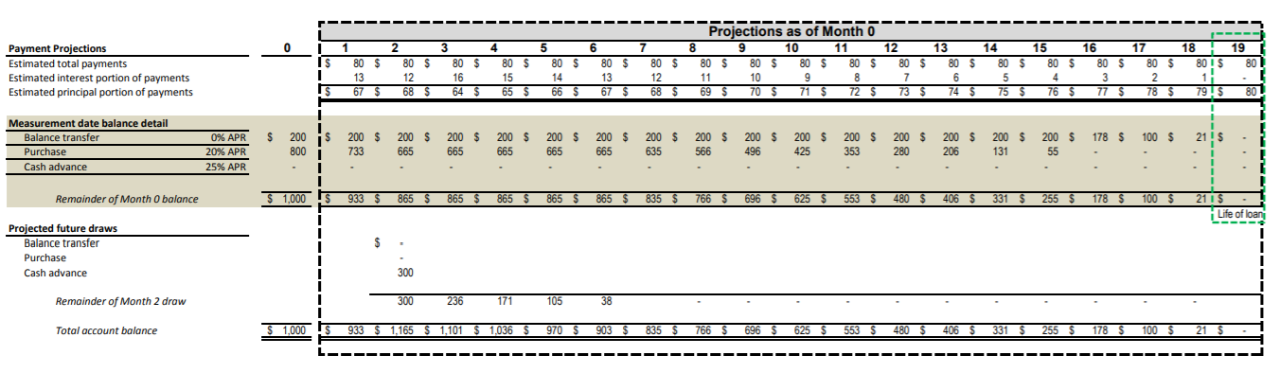

Illustration 3: CECL (ASC 326-20), VIEW B, looking forward from Month 0 |

- Assume the entity forecasts that (a) the borrower will draw $300 in the form of a cash advance at the end of Month 2 and (b) payments will be $80 per month At the end of Month 0, the entity applies View B in determining the life of the measurement date receivable balance.

The approach under View B is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying each future month's forecasted payment to the components of balance projected to exist at each future month end, incorporating future uses of the open line of credit. As part of that analysis, View B applies payments to each month's projected future balance in a manner consistent with federal bank regulatory requirements.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View B. Based on the forecasted collections and applying the View B allocation approach, the life of the Month 0 balance is 19 months.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

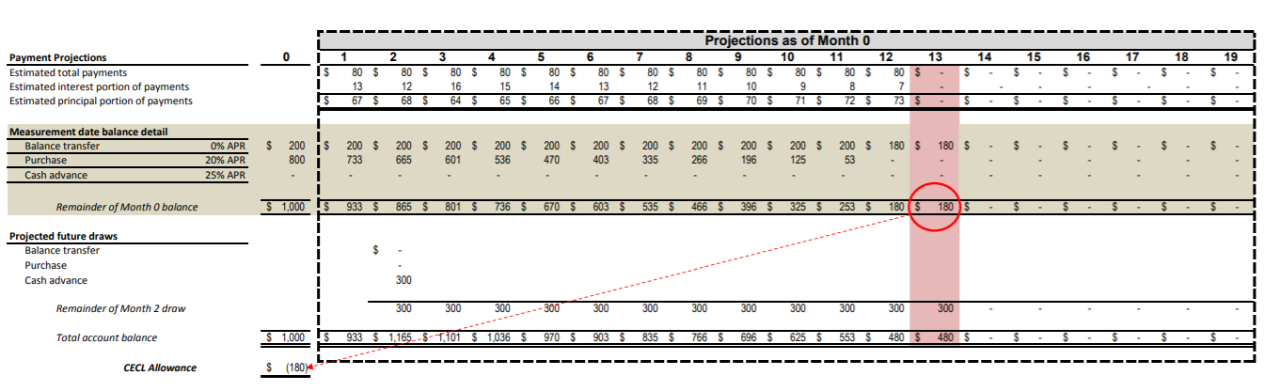

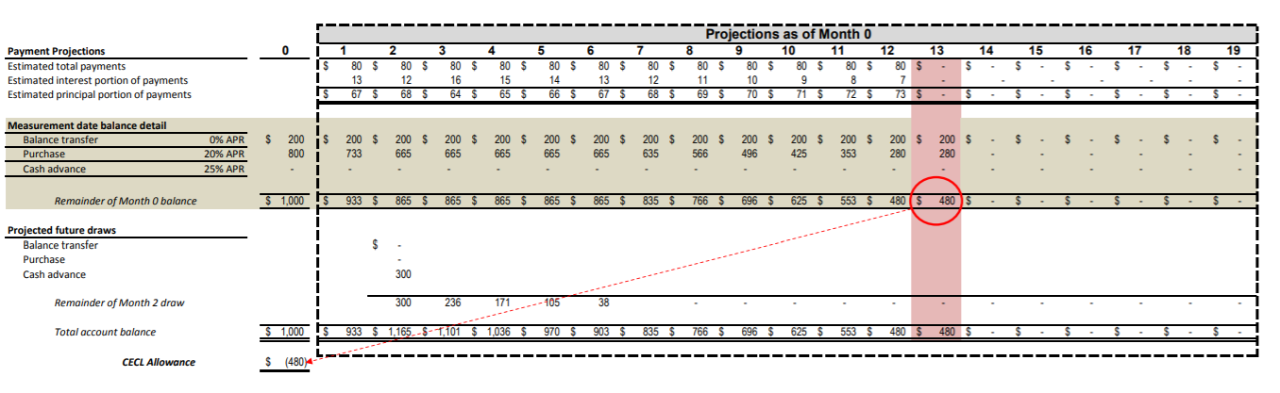

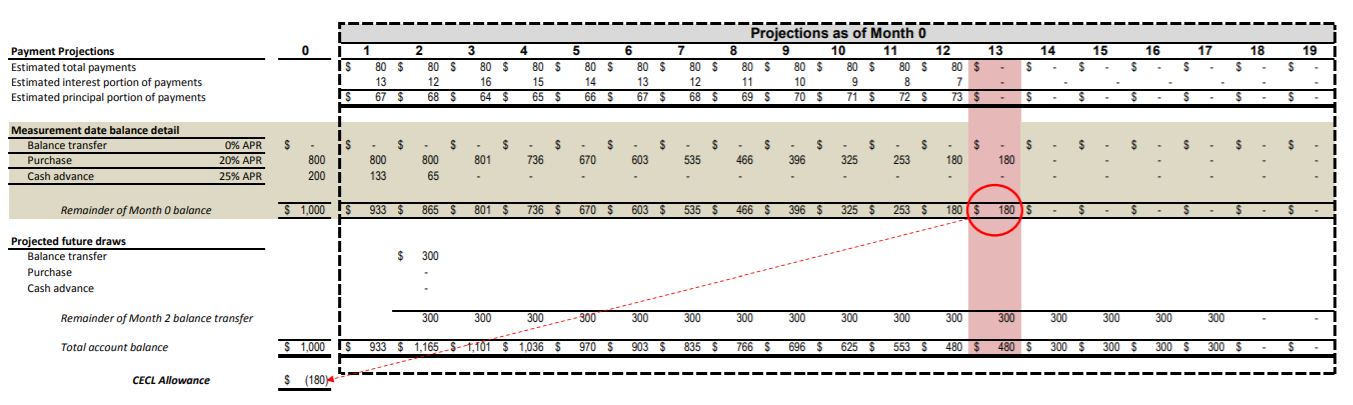

Illustration 4: CECL (ASC 326-20), VIEW A, looking forward from Month 0 |

- Assume same account usage and payments as in Illustration 2, and;

- Assume the entity expects that any unpaid balance remaining after month 12 will be uncollectible. The account balance at that time is projected to be $480.

At the end of Month 0, the entity estimates the current expected credit loss associated with the Month 0 ending balance pursuant to ASC 326-20 and applies View A in determining the life of the measurement date receivable balance.

The approach under View A is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying forecasted collections to the measurement date balance only, until that balance is fully repaid or until payments cease. As part of that analysis, View A applies payments to the measurement date balance in a manner consistent with federal bank regulatory requirements.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View A. Based on the forecasted collections and applying the View A allocation approach, $180 of the loss in Month 13 relates to the Month 0 balance and $300 relates to the draw made in Month 2. As a result, CECL allowance at Month 0 would be $180. In Month 2, assuming no other changes in assumptions, the CECL allowance would be increased to $480.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

Illustration 5: CECL (ASC 326-20), VIEW B, looking forward from Month 0 |

- Assume same account usage and payments as in Illustration 3, and;

- Assume the entity expects that any unpaid balance remaining after month 12 will be uncollectible. The account balance at that time is projected to be $480.

At the end of Month 0, the entity estimates the current expected credit loss associated with the Month 0 ending balance pursuant to ASC 326-20 and applies View B in determining the life of the measurement date receivable balance.

The approach under View B is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying each future month's forecasted payment to the components of balance projected to exist at each future month-end, incorporating future uses of the open line of credit. As part of that analysis, View B applies payments to each month's projected future balance in a manner consistent with federal bank regulatory requirements.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View B. Based on the forecasted collections and applying the View B allocation approach, the loss in Month 13 relates entirely to the balance at Month 0. As a result, the CECL allowance at Month 0 would be $480.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

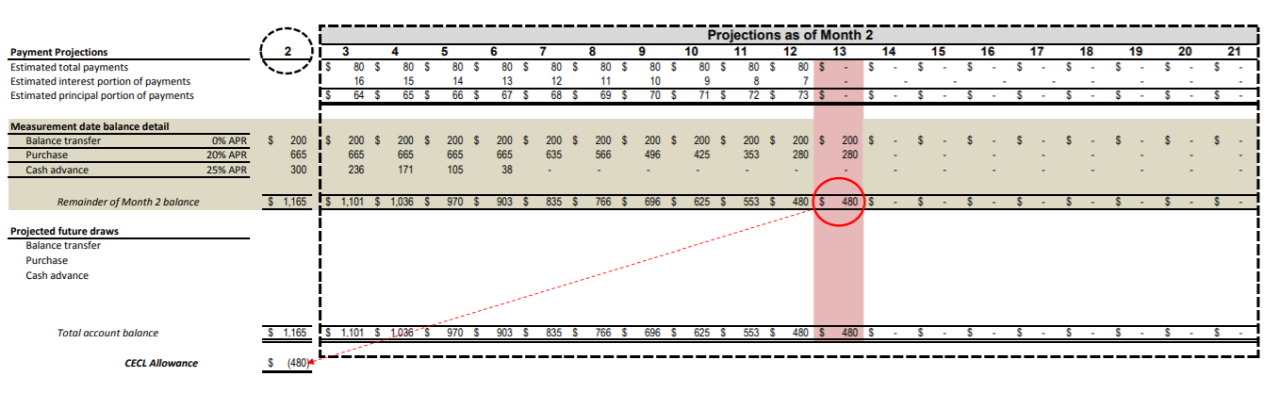

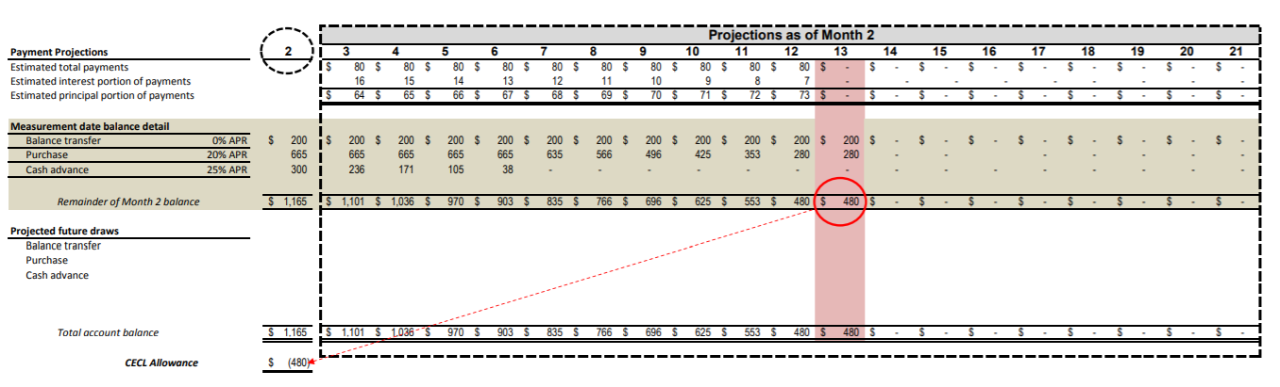

Illustration 6: CECL (ASC 326-20), VIEW A, looking forward from Month 2 |

- This example uses the same assumptions as Illustration 4, but presents the analysis that would take place in Month 2

- Assume the entity expects that any unpaid balance remaining after Month 12 will be uncollectible. The account balance at that time is projected to be $480.

- No additional draws are anticipated after Month 2

At the end of Month 2, the entity estimates the current expected credit loss associated with the Month 2 ending balance pursuant to ASC 326-20 and applies View A in determining the life of the measurement date receivable balance.

The approach under View A is to determine the net amount of the measurement date balance (in this case, the Month 2 balance) expected to be collected by applying forecasted collections to the measurement date balance only, until that balance is fully repaid or until payments cease. As part of that analysis, View A applies payments to the measurement date balance in a manner consistent with federal bank regulatory requirements.

Based on the forecasted collections and applying the View A allocation approach, the loss in Month 13 relates to the balance as of Month 2. As a result, the CECL allowance at Month 2 will equal $480.

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

Illustration 7: CECL (ASC 326-20), VIEW B, looking forward from Month 2 |

- This example uses the same assumptions as Illustration 5, but presents the analysis that would take place in Month 2

- Assume the entity expects that any unpaid balance remaining after Month 12 will be uncollectible. The account balance at that time is projected to be $480.

- No additional draws are anticipated after Month 2

At the end of Month 2, the entity estimates the current expected credit loss associated with the Month 2 ending balance pursuant to ASC 326-20 and applies View B in determining the life of the measurement date receivable balance.

The approach under View B is to determine the net amount of the measurement date balance (in this case, the Month 2 balance) expected to be collected by applying each future month's forecasted payment to the components of balance projected to exist at each future month-end, incorporating future uses of the open line of credit. As part of that analysis, View B applies payments to each month's projected future balance in a manner consistent with federal bank regulatory requirements.

Because no future use of the account is expected after Month 2, View A and View B produce the same remaining life for the measurement date balance and the same $480 CECL reserve at the end of Month 2.

View image

View image

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

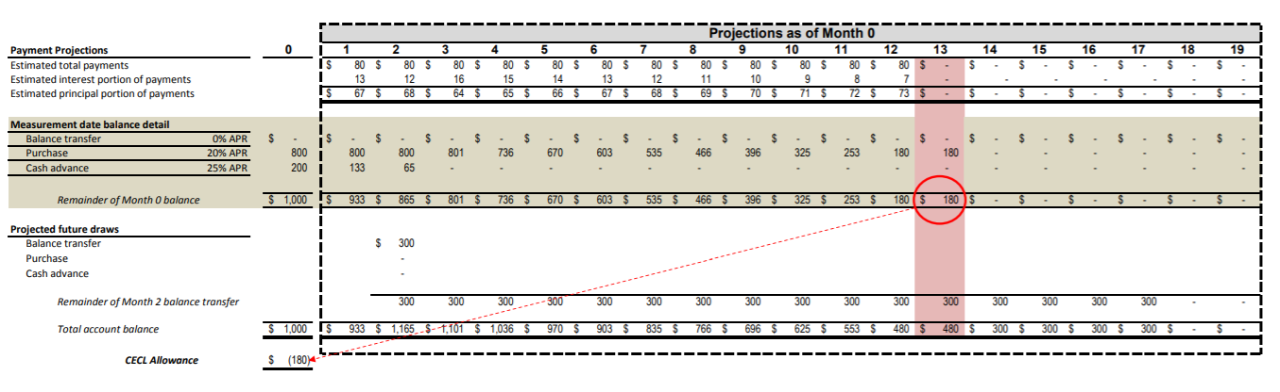

Illustration 8: CECL (ASC 326-20), VIEW A, looking forward from Month 0 |

- Assume the Month 0 balance is comprised of purchase and cash advance components instead of purchase and balance transfer components

- Assume the entity forecasts that (a) the borrower will draw $300 in the form of a balance transfer at the end of Month 2, (b) payments will be $80 per month, and (c) no other draws on the account will be made

- Assume the entity expects that any unpaid balance remaining after Month 12 will be uncollectible. The account balance at that time is projected to be $480.

At the end of Month 0, the entity estimates the current expected credit loss associated with the Month 0 ending balance pursuant to ASC 326-20 and applies View A in determining the life of the measurement date receivable balance.

The approach under View A is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying forecasted collections to the measurement date balance only, until that balance is fully repaid or until payments cease. As part of that analysis, View A applies payments to the measurement date balance in a manner consistent with federal bank regulatory requirements.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View A. Based on the forecasted collections and applying the View A allocation approach, $180 of the loss in Month 13 relates to the Month 0 balance and $300 relates to the draw made in Month 2. As a result, the CECL allowance at Month 0 will be $180.

View image

View image

CREDIT CARD ILLUSTRATIONS

DETERMINING THE AMOUNT OF THE MEASUREMENT DATE BALANCE EXPECTED TO BE COLLECTED

Illustration 9: CECL (ASC 326-20), VIEW B, looking forward from Month 0 |

- Assume the Month 0 balance is comprised of purchase and cash advance components instead of purchase and balance transfer components

- Assume the entity forecasts that (a) the borrower will draw $300 in the form of a balance transfer at the end of Month 2, (b) payments will be $80 per month, and (c) no other draws on the account will be made

- Assume the entity expects that any unpaid balance remaining after Month 12 will be uncollectible. The account balance at that time is projected to be $480.

At the end of Month 0, the entity estimates the current expected credit loss associated with the Month 0 ending balance pursuant to ASC 326-20 and applies View B in determining the life of the measurement date receivable balance.

The approach under View B is to determine the net amount of the measurement date balance (i.e., the Month 0 balance) expected to be collected by applying each future month's forecasted payment to the components of balance projected to exist at each future month-end, incorporating future uses of the open line of credit. As part of that analysis, View B applies payments to each month's projected future balance in a manner consistent with federal bank regulatory requirements.

The table below illustrates the forecasted collections and projected attrition of the Month 0 balance based on the application of View B. Based on the forecasted collections and applying the View B allocation approach, $180 of the loss in Month 13 relates to the Month 0 balance and $300 relates to the draw made in Month 2. As a result, the CECL allowance at Month 0 will be $180. This outcome is the same as under Illustration 8 because even with the application of View B, no payments were allocated to the Month 2 draw until the higher rate components, all of which were part of the Month 0 balance, were eliminated first.