STAFF PAPER | January 26, 2015 |

Project | FASB/IASB Joint Transition Resource Group for Revenue Recognition |

Paper topic | Application of IFRS 15 to permitted Islamic Finance Transactions |

|

|

This paper has been prepared by the staff of the IFRS Foundation and the FASB for discussion at a public meeting of the FASB | IASB Joint Transition Resource Group for Revenue Recognition. It does not purport to represent the views of any individual members of either board or staff. Comments on the application of U.S. GAAP or IFRS do not purport to set out acceptable or unacceptable application of U.S. GAAP or IFRS. |

Introduction

1. At its September 2014 meeting in Kuala Lumpur, the IASB Advisory Group on Shariah-Compliant Instruments and Transactions (the Advisory Group) discussed the implications of IFRS 15 for certain instruments common in the Islamic financial industry. The Advisory Group decided that it should seek views from the IASB/FASB Joint Transition Resource Group on Revenue Recognition.

Background

2. Islamic financial instruments do not include interest on loans (riba). Instead, a financier earns returns from permitted transactions that broadly include:

(a) | mark-up in purchase and sale contracts with deferred payment—Murabaha and other contracts; |

(b) | profit-share in venture and other partnership-like contracts—Musharaka, Mudaraba and other contracts; |

(c) | rent in lease contracts—Ijarah; |

(d) | fees from agency contracts—Wakalah, and |

(e) | profit, profit-share, rent or fees from undivided pro-rata ownership contracts—Sukuk. |

3. A distinguishing feature of instruments in Islamic finance is that they involve financing of assets in the real, as opposed to the financial, economy. An Islamic Financial Institution (IFI) must legally possess the underlying assets, even for very short time, with all risks and rewards incidental to ownership before it can resell or lease the underlying assets. Our attention in this paper is on the first transaction type identified in the preceding paragraph. An (IFI) may charge a premium or mark-up on the sale of a real asset, like a vehicle or a real estate property, to compensate for deferred payment. With limited exceptions, there is no anticipation of dealer profit from the sale itself. A similar mark-up on a cash loan would constitute riba or interest and would be forbidden.

4. Bank Aljazira (Saudi Arabia) includes the following definition in its 2013 annual report:

Murabaha is an agreement whereby the Bank sells to a customer a commodity or an asset, which the Bank has purchased and acquired based on a promise received from the customer to buy. The selling price comprises the cost plus an agreed profit margin.

5. Dubai Islamic Bank includes a similar definition in its 2013 annual report:

A contract whereby the Bank (the "Seller”) sells an asset to its customer (the "Purchaser”), on a deferred payment basis, after purchasing the asset and gaining possession thereof and title thereto, where the Seller has purchased and acquired that asset, based on a promised received from the Purchaser to buy the asset once purchased according to specific Murabaha terms and conditions. The Murabaha sale price comprises the cost of the asset and a pre-agreed profit amount. Murabaha profit is internally accounted for on a time-apportioned basis over the period of the contract based on the principal amount outstanding. The Murabaha sale price is paid by the Purchaser to the Seller on an instalment basis over the period of the Murabaha as stated in the contract.

6. Both of the banks are IFRS compliant and have adopted IFRS 9.

7. The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) provides a somewhat different definition:

Sale of goods with an agreed upon profit mark up on the cost. Murabaha sale is of two types. In the first type, the Islamic bank purchases the goods and makes it available for sale without any prior promise from a customer to purchase it. In the second type, the Islamic bank purchases the goods ordered by a customer from a third party and then sells the goods to the same customer. In the latter case, the Islamic Bank purchases the goods only after a customer has made a promise to purchase them from the bank. [Emphasis added]

8. Participants in the Kuala Lumpur meeting indicated that the “second type” identified in the AAOIFI definition is by far the most common in modern islamic finance. However, they identified two situations that might fall in the “first type:”

(a) An IFI maintains a car showroom that customers use to select vehicles for purchase. (In practice, however, most of these arrangements are of the "the second type”. The IFI does not have an inventory beyond the showroom vehicles. Instead, it orders vehicles from manufacturers or others based on choices made in the showroom.)

(b) An IFI trades in commodities. That is, it takes a position in a commodity and makes deferred-payment to customers from the stock in its position. If no customer is found, it closes out the position.

The issue

9. There is no question on three points:

(a) for the seller, the form of these transactions is that of cash purchase and, in almost all cases, immediate sale with deferred payment;

(b) for the purchaser, the form of these transactions is that of purchase on deferred payments, and

(c) the financial instruments created by the transactions fall within the scope of IFRS 9 and IAS 32, as would financing contracts provided to a business's customers.

10. The question at hand is not whether particular transactions are, in fact, Shariah compliant. That is beyond the scope and capability of either the Advisory Group or the Transition Resource Group.

11. The question, then, is whether deferred-payment transactions (with the possible exception of the "first type"in paragraph 7) described in this paper must first pass through IFRS 15 before being reported under IFRS 9 since the IFI must possess the underlying assets, even for a very short period of time, with all risks and rewards incidental to ownership before the subsequent sale. If so, the IFI's income statement would show sales and cost of goods sold in equal amounts and a gross profit of zero. The IFI would be required to make disclosures required by IFRS 15. Many participants at the Kuala Lumpur questioned the relevance of those disclosures for financial institutions.

12. Paragraph 5 of IFRS 15 describes the scope as "all contracts with customers"other than those that are excluded. The key language in the standard for purposes of this issue is the explanation in paragraph 6:

An entity shall apply this Standard to a contract (other than a contract listed in paragraph 5) only if the counterparty to the contract is a customer. A customer is a party that has contracted with an entity to obtain goods or services that are an output of the entity's ordinary activities in exchange for consideration. A counterparty to the contract would not be a customer if, for example, the counterparty has contracted with the entity to participate in an activity or process in which the parties to the contract share in the risks and benefits that result from the activity or process (such as developing an asset in a collaboration arrangement) rather than to obtain the output of the entity's ordinary activities. [Emphasis added]

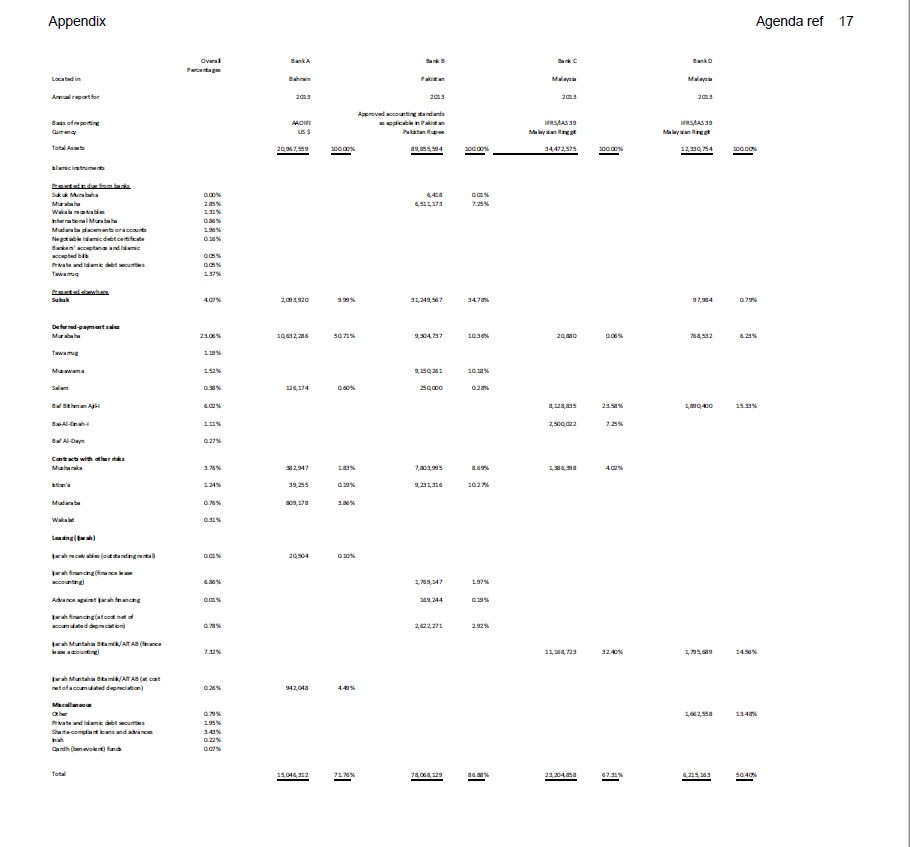

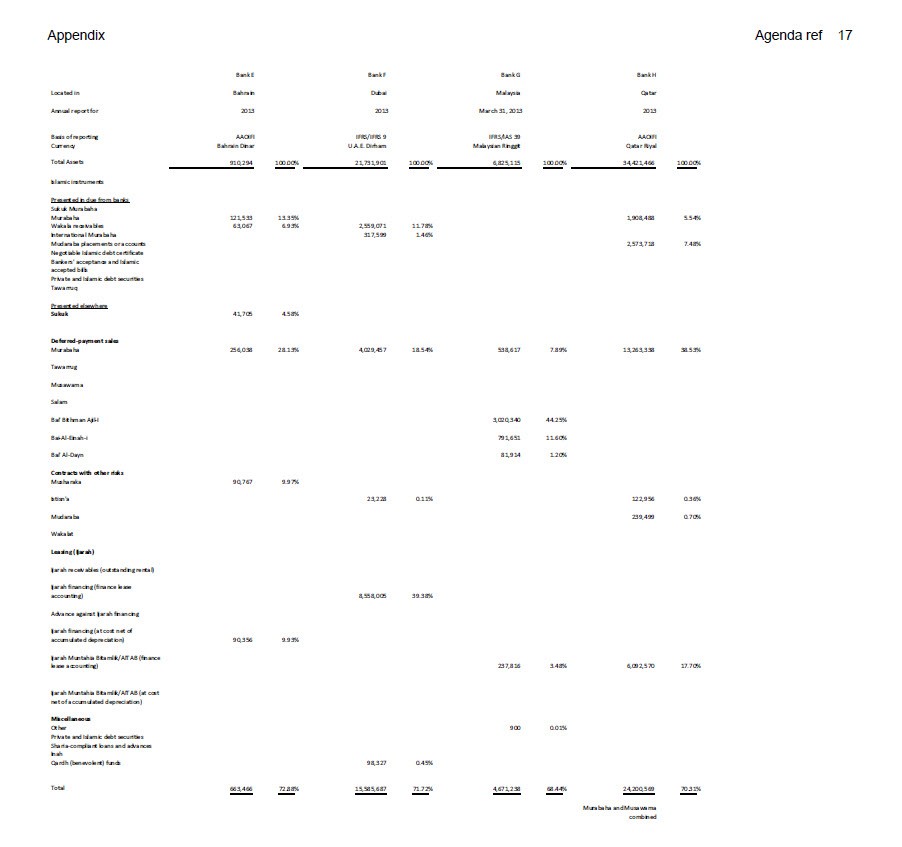

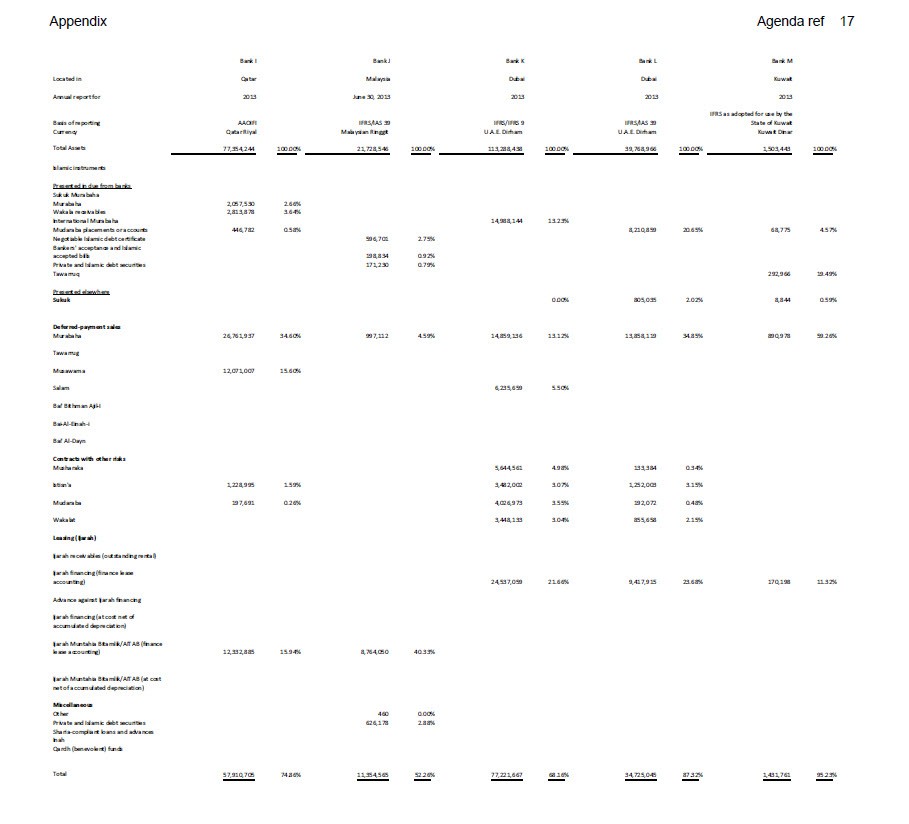

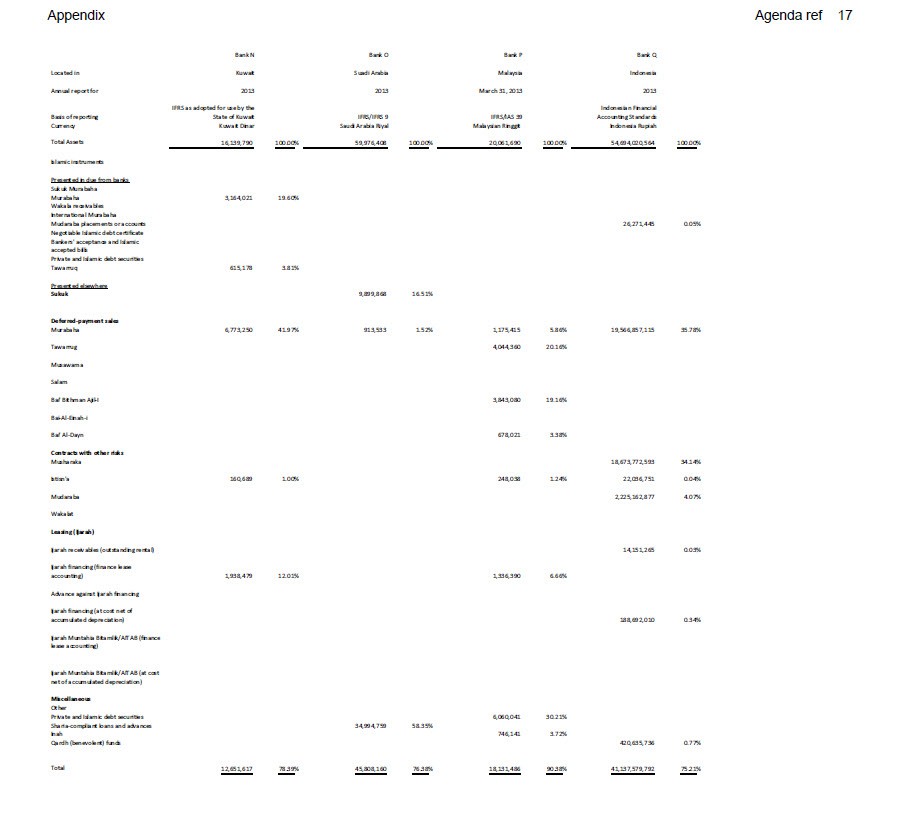

13. Those who maintain that IFRS 15 should not apply would likely look to the description of "the entity's ordinary activities"in paragraph 6. They would say that in most cases an IFI's ordinary activities are the provision of Shariah compliant financing and are not the sales of cars, real estate, or commodities. They would observe that the risk that IFIs incur is credit risk. Further, the return inherent in the mark-up for deferred payment is the principal source of profits for IFIs. The mark-up is consistent with a market perception of compensation for time value. They would likely also observe that none of the IFIs studied by the IASB staff (see Appendix) applied IFRS 15's predecessor, IAS 18.

14. Others observe that the issue is not limited to a judgement of the ordinary activities of the IFI. It is also about its status in the contract, i.e., whether it is a principal or an agent. Paragraph B35 poses a dilemma in this regard. Although the IFI is obliged to really possess the goods with all risks and rewards incidental to ownership, the IFI obtains legal title/possession of a product only momentarily before legal title is transferred to a customer.

15. Those who maintain that either IFRS15 or another specific treatment should apply would likely look at the special arrangements to effect such transactions. They cited the finance lease as example of a mode of finance, which requires specific accounting treatment, especially for the lessor whose ordinary course of business is finance lease. Although the IFI's ordinary activities are the provision of Sariah-compliant financing and are not the sales of cars, real estate, or commodities, it is nonetheless substantially different from conventional bank because of the following:

(a) it has an obligation to pay a third party for the goods purchased to be sold to a customer on the basis of Murabaha so it is not an agent in the contract;

(b) it must own the goods, not only the legal title, even for a short period of time, with all risks and rewards incidental to ownership, and

(c) it has an obligation to deliver the goods (not the cash) to the customer.

16. This group of participants maintain that the existence of a significant financing component in the contract is not relevant to whether the contract itself is within the scope of IFRS 15 or whether it warrants specific treatment. That is because the financing element is part of the arrangement of collection of the consideration where paragraphs 60 and 61 of IFRS15 apply.

Effect on practice

17. We cannot judge the diversity in practice that might emerge with the recent issuance of IFRS 15. Instead, we are concerned that IFIs might incur significant costs to analyse the possible application of the standard and that those costs might be avoided by timely communication to the marketplace.

The IASB is the independent standard-setting body of the IFRS Foundation, a not-for-profit corporation promoting the adoption of IFRSs. For more information visit www.ifrs.org

The Financial Accounting Standards Board (FASB) is an independent standard-setting body of the Financial Accounting Foundation, a not-for-profit corporation. The FASB is responsible for establishing Generally Accepted Accounting Principles (GAAP), standards of financial accounting that govern the preparation of financial reports by public and private companies and not-for-profit organizations in the United States and other jurisdictions. For more information visit www.fasb.org