GASB Preliminary Views: Revenue and Expense Recognition

Publication date: 20 Mar 2020

us GASB Exposure draft

Notice of Public Hearings and User Forums, and Request for Written Comments

PUBLIC HEARINGS AND USER FORUMS

Public hearings are tentatively scheduled as follows:

March 23, 2021, in Boise, ID (in conjunction with the annual conference of the National Association of State Comptrollers), beginning at 8:30 a.m. local time.

March 30–31, 2021, in Atlanta, GA, beginning at 8:30 a.m. local time.

April 8, 2021, in New York, NY, beginning at 8:30 a.m. local time.

April 13–14, 2021, in Chicago, IL, beginning at 8:30 a.m. local time.

April 20–21, 2021, in San Francisco, CA, beginning at 8:30 a.m. local time.

User forums are tentatively scheduled as follows:

April 9, 2021, in New York, NY, beginning at 8:30 a.m. local time.

April 15, 2021, in Chicago, IL, beginning at 8:30 a.m. local time.

Public hearings. The public hearings are being conducted on the same days as the public hearings on the Exposure Draft of the proposed Statement, Financial Reporting Model Improvements, and the Exposure Draft of the proposed Concepts Statement, Recognition of Elements of Financial Statements, to allow interested individuals or organizations to participate in both public hearings. Those individuals or organizations may participate in person, by videoconference (if available at the location), or by telephone. Details regarding participation will be provided after the Governmental Accounting Standards Board (GASB) receives a notice of intent to participate.

User forums. The user forums are being conducted primarily for interested individuals or organizations from the financial statement user community. Interested individuals or organizations may participate in a user forum in person, by videoconference (if available at the location), or by telephone. Participation in person is encouraged. Details regarding participation will be provided after the GASB receives a notice of intent to participate.

Deadline for written notice of intent to participate in the public hearings and user forums: February 26, 2021

Basis for public hearings and user forums. The GASB has scheduled the public hearings and user forums to obtain information from interested individuals and organizations about the issues discussed in this Preliminary Views and in the Exposure Drafts. The hearings and forums will be conducted by one or more members of the Board and its staff. Interested parties are encouraged to participate in a hearing or user forum, as appropriate, and through written response.

Public hearing oral presentation requirements. Individuals or organizations that want to make an oral presentation in person, by videoconference (if available at the location), or by telephone at a public hearing are required to provide, by the deadline for notice of intent to participate (February 26, 2021), a written notification of that intent, accompanied by their written submission in response to this Preliminary Views. A copy of additional comments that will be made at the public hearing addressing the issues discussed in this Preliminary Views should be provided two weeks before the public hearing. The notification, written submission, and additional comments should be addressed to the Director of Research and Technical Activities, Project No. 4-6P, and emailed to director@gasb.org.The notification should indicate the location of the hearing at which the respondent would like to participate and a preference for participating in person, by videoconference (if available at the location), or by telephone. A public hearing may be cancelled if sufficient interest is not expressed by the deadline.

The GASB intends to schedule all respondents who want to make oral presentations at a public hearing and will notify each individual or organization of the expected time of their presentation. The time allotted to each individual or organization will be limited to approximately 30 minutes—10 minutes to summarize or elaborate on the written submissions, or to comment on the written submissions or presentations of others, and 20 minutes to respond to questions from those conducting the hearing.

User forum participation requirements. Participation in a user forum is limited to external financial statement users, such as municipal bond analysts, taxpayer group members, and legislators. All participants are asked to engage in a discussion of the issues raised in this Preliminary Views, additional issues raised by the Board members and staff, and issues raised by other participants. Every participant will be provided with the opportunity to express his or her views.

Individuals who want to participate in a user forum should provide, by the deadline for notice of intent to participate (February 26, 2021), a written notification of that intent (addressed to the Director of Research and Technical Activities, Project No. 4-6P, and emailed to director@gasb.org). The notification should indicate the location of the user forum at which the respondent would like to participate and a preference for participating in person, by videoconference (if available at the location), or by telephone. Participation in person is encouraged.

Observers. Observers are welcome at the public hearings and user forums and are urged to submit written comments.

WRITTEN COMMENTS

Deadline for submitting written comments: February 26, 2021

Requirements for written comments: Any individual or organization that wants to provide written comments should provide those comments by February 26, 2021. Comments should be addressed to the Director of Research and Technical Activities, Project No. 4-6P, and emailed to director@gasb.org.

OTHER INFORMATION

Public files. Written comments and transcripts of the public hearings and user forums will become part of the Board’s public file. Written comments also are posted on the GASB’s website.

This Preliminary Views may be downloaded from the GASB’s website at www.gasb.org.

Final GASB publications may be ordered at www.gasb.org.

Notice to Recipients of This Preliminary Views

The GASB is responsible for (1) establishing and improving standards of state and local governmental accounting and financial reporting to provide useful information to users of financial reports and (2) educating stakeholders—including issuers, auditors, and users of those financial reports—on how to most effectively understand and implement those standards.

The due process procedures that we follow before issuing our standards and other communications are designed to encourage broad public participation in the standards-setting process. As part of that due process, the GASB is issuing this Preliminary Views to solicit comments on the Board’s proposal for revenue and expense recognition. This Preliminary Views identifies significant issues that are known to exist, presents the Board’s preliminary views on how it intends to address those issues, and invites respondents to comment on them and identify additional relevant issues.

A Preliminary Views is a Board document designed to set forth and seek comments on the GASB’s current views at a relatively early stage of a project. This Preliminary Views is a step toward an Exposure Draft of a Statement of Governmental Accounting Standards but is not an Exposure Draft. This document presents the GASB’s preliminary views on revenue and expense recognition and discusses the foundational principles, purposes, and objectives of the GASB’s proposal. A Preliminary Views generally is issued when the GASB anticipates that respondents are likely to be sharply divided on the issues or when the GASB itself is sharply divided on the issues. Because stakeholders were divided in their feedback to a previously issued Invitation to Comment, the GASB believes that a Preliminary Views is more appropriate at this time than an Exposure Draft. This Preliminary Views represents the GASB’s current views on the issues discussed in this document.

We invite your comments on all matters in this Preliminary Views. Respondents are requested to give their views only after reading the entire text of this Preliminary Views. Because guidance proposed in this Preliminary Views may be modified before it is issued as an Exposure Draft, it is important that you comment on any aspects with which you agree, as well as any with which you disagree. To facilitate our analysis of the responses to this Preliminary Views, it would be helpful if you explain the reasons for your views, including alternatives that you believe the GASB should consider.

All responses are distributed to all Board members and to staff members assigned to this project, and all comments are considered during the Board’s deliberations leading to an Exposure Draft. In deciding on changes in accounting and financial reporting standards, the GASB also takes into consideration the expected benefits to users of financial statements and the perceived costs of preparing and reporting the information. Only after the Board is satisfied that all alternatives have adequately been considered, and modifications have been made as considered appropriate, will a vote be taken to issue an Exposure Draft. The Board also will seek and consider comments on the Exposure Draft before proceeding to a final Statement.

This document presents the preliminary views of the Governmental Accounting Standards Board (GASB) on the development of a comprehensive revenue and expense recognition model. The proposed model is intended to improve the understandability, reliability, relevance, consistency, and comparability of information regarding revenues and expenses, thereby enhancing the usefulness of that information for making decisions or assessing a government’s accountability.

The Revenue and Expense Recognition Model

A revenue and expense recognition model, similar to other guidance, contains three components: (1) categorization, (2) recognition, and (3) measurement. Existing transaction-based guidance relies on scope definitions to describe the transactions that should be recognized and measured under said guidance. Given the wide range of revenue and expense transactions in the scope of this project, the Board believes that it is necessary to develop a new approach for categorization to organize those transactions prior to addressing recognition and measurement.

Categorization

The proposed categorization methodology would move away from the traditional determination of whether a transaction is exchange, exchange-like, or nonexchange based on an assessment of equal value. The proposed categorization methodology would apply to both revenue and expense transactions and would take the form of a sequential assessment of four characteristics to determine the type of transaction:

Whether there is a binding arrangement, such as a contract, a grant agreement, a memorandum of understanding, or legislation

Whether the parties to the transaction have approved the terms and conditions of the binding arrangement (there is mutual assent between parties of capacity)

Whether the parties to the transaction have substantive rights and obligations

Whether the substantive rights and obligations are interdependent.

If a transaction does not include a binding arrangement, the transaction would be excluded from the scope of this project. If a transaction has all four of the characteristics, it contains a performance obligation and would be identified as a Category A transaction. Otherwise, it would be identified as a Category B transaction.

Recognition of Category A Transactions

The recognition proposals are based on the type of transaction, as identified using the categorization methodology. For Category A transactions, revenues and expenses would be recognized based on the satisfaction of a performance obligation. A government would determine each performance obligation in the binding arrangement by identifying distinct goods or services. The recognition of revenues and expenses occurs upon the satisfaction of those performance obligations. A performance obligation is satisfied when (or as) one of the parties transfers control of a resource (the distinct good or service) to the other party. A performance obligation may be satisfied over time or at a point in time.

Recognition of Category B Transactions

The recognition approach for Category B transactions would be based on five subcategories of transactions: (1) derived revenue, (2) imposed revenue, (3) contractual binding arrangement, (4) general aid to governments, and (5) shared revenue. The first two subcategories are revenue-only transactions. The other three involve both revenue and expense transactions.

Recognition for derived revenue transactions would be based on when the underlying transaction occurs. For example, a sales tax receivable and sales tax revenue would be recognized when there is a sale subject to taxation.

Recognition for imposed revenue transactions would be based on the imposition date or the date of the omission or commission of an act. For example, a property tax receivable would be recognized when a governing body imposes the tax; property tax revenue would be recognized based on the period for which it is imposed.

Recognition for revenues and expenses in contractual binding arrangement transactions would be based on the terms and conditions specified in the agreement. For example, a receivable and revenue would be recognized when a pledge agreement that does not contain time requirements is executed.

Recognition for revenues and expenses in general aid to governments and shared revenue transactions would be based on the existence of a provider government’s appropriation, the commencement of the appropriation period, and the provider government’s intent to provide resources. For example, a general aid receivable and general aid revenue would be recognized by a school district when the state appropriates the general aid and has demonstrated its intent to provide the resources, and the payment is due.

Measurement

The measurement proposals in this Preliminary Views are limited to a foundational principle and two application topics. Consistent with existing guidance, the proposed principle is that assets and liabilities would be measured directly, and revenues and expenses would be measured by relying on their related asset or related liability.

The first application topic is that revenue would be recognized net of amounts probable of being refunded; that is, governments would recognize a liability for revenue transactions that include a right of refund when that refund is probable. The second application topic is that revenue would be recognized net of amounts probable of becoming uncollectible with a corresponding allowance for doubtful accounts.

Application Materials

Chapter 7 of this Preliminary Views includes a description of the application of the Board’s proposals in two other Exposure Drafts being issued, a proposed Statement, Financial Reporting Model Improvements, and a proposed Concepts Statement, Recognition of Elements of Financial Statements. Appendix C of this Preliminary Views includes illustrations of the application of the revenue and expense recognition model.

How the Changes Proposed in This Preliminary Views Would Improve Financial Reporting

The Board’s proposed requirements in this Preliminary Views, if ultimately issued as a Statement, would enhance the understandability, reliability, relevance, consistency, and comparability of state and local government financial reporting by providing a comprehensive model for the recognition of a broad range of revenue and expense transactions.

The application of the categorization methodology proposals in this Preliminary Views, which focus on the underlying characteristics of the transactions, would allow governments to more reliably and consistently categorize revenue and expense transactions. The recognition proposals in this Preliminary Views correspond to the transaction category; consequently, the recognition of elements of financial statements also would be more reliable and consistent. The resulting financial information would be more understandable, reliable, relevant, consistent, and comparable, which would allow users to better assess interperiod equity and accountability. Finally, the proposed categorization model would establish a foundational approach, which may be useful for future standards setting.

CHAPTER 1—OBJECTIVE AND SCOPE

Objective of the Revenue and Expense Recognition Project

1. The objective of this project is to develop a comprehensive, principles-based model that establishes categorization, recognition, and measurement guidance applicable to a wide range of revenue and expense transactions. Achieving that objective includes the (a) development of guidance applicable to topics for which existing guidance is limited, (b) improvement of existing guidance that has been identified as challenging to apply, (c) consideration of including a performance obligation approach in the GASB’s authoritative literature, and (d) assessment of existing and proposed guidance based on the conceptual framework. The expected outcome of this project is enhanced quality of information that users rely upon in making decisions and assessing accountability.

Components of a Revenue and Expense Recognition Model

2. The following three components comprise a revenue and expense recognition model:

Categorization is the process of classifying a transaction by identifying the relevant characteristics of that transaction in the context of a group of similar transactions. For example, based on existing standards, sales tax revenue is categorized as a nonexchange revenue transaction.

Recognition is the process of determining when an item should be reported as an element (such as an asset or an inflow of resources) in financial statements.

For example, existing guidance requires that an asset from a sales tax transaction be recognized when the exchange transaction from which the tax is derived occurs or when the resources are received, whichever occurs first. Sales tax revenue should be recognized in the same period that the asset is recognized, provided that the underlying exchange transaction has occurred.

Measurement is the process of determining the amount at which elements should be reported in financial statements. For example, existing standards require that revenues be reported net of estimated uncollectible amounts.

Scope and Applicability of This Project

Scope

The scope of this project includes the categorization, recognition, and measurement of revenues and expenses from a wide range of transactions. However, three groups of transactions are excluded:

Capital asset and inventory transactions: Capital asset transactions that are excluded from the scope of this project include purchases, sales, and abandonments of capital assets and nonmonetary transactions involving capital assets. The scope of this project also excludes depreciation expense, gains and losses from impairment, and remeasurement of capital assets. Furthermore, this project does not address the purchase, measurement, or remeasurement of inventory.

Financial instrument transactions: Financial instrument transactions that are excluded from the scope of this project include investments, financial guarantees, derivative instruments, financings such as leases, insurance, and short- and long-term debt.

The scope of this project also excludes interest expense as it relates to short- and long-term debt, interest income, and changes in the fair value of financial instruments.

Postemployment benefit and compensated absence transactions: Postemployment benefit transactions excluded from the scope of this project include pensions and other postemployment benefits (OPEB). The scope of this project also excludes compensated absences and termination benefits.

Additionally, the scope of this project includes donations of financial resources that are not specifically excluded above. Therefore, donations of capital assets, in-kind contributions, and contributed services are not in the scope of this project. A list of the pronouncements that are included and excluded from the scope of this project is provided in Appendix B.

Applicability

4. The provisions presented in this Preliminary Views, if adopted as final standards, would be applied to financial statements of all state and local governments.

Relationship to the Financial Reporting Model Improvements and Recognition of Elements of Financial Statements Projects

5. In addition to this Preliminary Views, the Board has approved two related Exposure Drafts—Financial Reporting Model Improvements (Financial Reporting Model Improvements Exposure Draft) and Recognition of Elements of Financial Statements (Recognition Concepts Exposure Draft). Chapter 7 of this Preliminary Views describes the application of the Board’s proposed concepts and accounting standards included in the aforementioned Exposure Drafts as they relate to transactions within the scope of this project. Appendix C includes cases that illustrate the application of provisions proposed in those documents to certain transactions in the scope of this project.

Project Overview

Project Background

6. The Board’s decision to add this project to its technical agenda in April 2016 was primarily informed by two considerations. First, a post-implementation review (PIR) was conducted for Statements No. 33, Accounting and Financial Reporting for Nonexchange Transactions, and No. 36, Recipient Reporting for Certain Shared Nonexchange Revenues. The results of the PIR indicated that the guidance contained in those two pronouncements was effective; however, specific financial reporting challenges were identified. Among those challenges was that stakeholders experience difficulties differentiating between exchange and nonexchange transactions. The second major consideration was that the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) issued guidance for revenue recognition from contracts with customers. The FASB and the IASB guidance for revenue recognition focused on the fulfillment of a performance obligation. Based on those considerations, the Board concluded that now is the appropriate time to develop a comprehensive model for revenue and expense recognition for governments.

7. In 2018, the Board issued an Invitation to Comment, Revenue and Expense Recognition, that included descriptions of three models. The first model relied on the exchange/nonexchange categorization methodology (primarily based on existing guidance), and the second model presented a performance obligation/no performance obligation categorization methodology. A third hybrid model, which combined the two methodologies, was included as an example. Stakeholder feedback on the Invitation to Comment models was mixed; that is, stakeholders expressed preferences for each of the three models presented.

Categorization

8. Based on stakeholder feedback on the Invitation to Comment, the Board decided to conduct additional analysis to assess the suitability of the categorization methodologies. The analysis demonstrated that both the exchange/nonexchange and the performance obligation/no performance obligation categorization methodologies, as described in the Invitation to Comment, offered limited suitability.

Exchange/Nonexchange Categorization

9. The Board considered the various characteristics of the existing definitions of exchange, exchange-like, and nonexchange transactions, each of which focuses on the key concept of equal value. After considering those characteristics, the overall conclusion reflected in the Board’s preliminary views is that relying on value as a categorization tool is unreliable because value reflects the subjective perceptions of the parties to the transaction. Value is not a characteristic of the item in the transaction nor of the transaction itself; therefore, it is not feasible to clarify the meaning of value. In an attempt to overcome that challenge, existing literature relies on additional characteristics, such as benefit and cost recovery. However, those characteristics have proven to be equally unreliable. Benefit also is subjective and, similar to value, reflects the resource recipient’s perception of utility. Cost recovery communicates a governing body’s decision about charges for services and therefore reflects public policy, not a clarification of value.

10. Furthermore, it has been observed in practice that some stakeholders determine whether a transaction is exchange, exchange-like, or nonexchange based on an arbitrary percentage of market prices. In other words, those stakeholders consider whether the amount of consideration transferred for a resource corresponds to a certain percentage of the market price for that resource. That approach results in inconsistencies because the same percentage is not used across various governments. Even if a single percentage were proposed, the Board does not believe that the relative proportion of consideration is indicative of the type of transaction.

11. A challenge that arises from inconsistency in the categorization of transactions as exchange, exchange-like, or nonexchange is that stakeholders may not consistently identify the appropriate recognition and measurement provisions relevant to a specific transaction. Therefore, it is possible for two governments to arrive at different categorization conclusions for similar transactions. Furthermore, certain transactions may simultaneously meet the definitions of exchange, exchange-like, and nonexchange transactions, which results in fragmentation in the application of the literature. In other words, stakeholders may not be certain which recognition provisions may be applicable and, consequently, may rely on incorrect recognition provisions that distort information. For example, if an exchange transaction is recognized following the provisions for nonexchange transactions, the amounts reported in financial statements or the timing of their reporting may not be appropriate. As a result, the information reported in financial statements may not be as understandable, reliable, relevant, consistent, and comparable as it should be.

12. The Board also considered the various characteristics of the performance obligation/no performance obligation categorization methodology and concluded that the definition of a performance obligation presented in the Invitation to Comment was overly complex. The complexity identified in the definition of a performance obligation also might result in inconsistent categorization of transactions. Therefore, the Board concluded that the methodology presented in the Invitation to Comment was not suitable for achieving the objective of this project. However, the Board did find many of the underlying attributes of a performance obligation model presented in the Invitation to Comment to be valuable in developing recognition principles, as noted below.

The Hybrid Model

13. As previously stated, the hybrid model combined the exchange/nonexchange categorization methodology with the performance obligation recognition approach. As previously noted, the Board concluded that the exchange/nonexchange categorization model was unsuitable. Furthermore, the hybrid model posed an additional challenge: because it combined the first two models presented in the Invitation to Comment, there was the potential to require a performance obligation recognition approach for certain transactions identified at present as exchange-like (which may not include performance obligations). Conversely, this model would have required recognition as nonexchange transaction grants that included performance obligations.

A New Categorization Methodology

14. Based on the analysis conducted subsequent to the Invitation to Comment, the Board decided to develop a new categorization methodology that retains the relevant characteristics from the two categorization methodologies proposed in the Invitation to Comment. For example, the characteristic of “something for something” in the exchange/nonexchange model and the characteristic of distinct goods or services in the performance obligation/no performance obligation model were useful in categorizing transactions.

Because the categorization methodology proposed in this Preliminary Views was developed from specific characteristics of the exchange/nonexchange and performance obligation/no performance obligation categorization methodologies in the Invitation to Comment, the Board decided to use the neutral categorization nomenclature of Category A and Category B in this document to make clear that it did not select any of the Invitation to Comment models. This new categorization methodology aims to include in Category A those revenue or expense transactions that include at least one performance obligation, and to identify Category B transactions as those that do not possess the characteristics of Category A transactions (and therefore do not include performance obligations). The application of the categorization methodology is described in Chapter 3.

Recognition and Measurement

15. One of the purposes of this project is to consider the performance obligation approach. The Board believes that the performance obligation approach constitutes a global shift away from the earnings recognition approach. Therefore, it provides an opportunity to address the recognition challenges identified in existing literature related to certain revenue and expense transactions. Specifically, the performance obligation recognition approach offers an opportunity to create consistency in the recognition of transactions that are identified in this document as Category A. (See Chapters 4 and 5.)

16. This Preliminary Views incorporates existing guidance provided in Statements 33 and 36 that the Board identified as effective and consistent with the conceptual framework. The Board proposes modifications to existing guidance for aspects identified as challenging, for example, the identification of when a receivable should be recognized for property taxes. The Board also proposes modifications to existing guidance for aspects that can be better aligned with the current conceptual framework, for example, the recognition of pledges that are subject to time requirements. (See Chapter 4.)

17. Measurement proposals included in this document are limited to a measurement principle and two application topics. A future due process document will include additional measurement proposals to further support the aforementioned recognition proposals. (See Chapter 6.)

How the Changes Proposed in This Preliminary Views Would Improve Financial Reporting

18. The Board expects that the outcomes of this project would result in specific benefits for auditors, preparers, and users of financial statements. Additionally, the guidance developed in the project is expected to serve as a foundation for the development of future standards.

19. The Board believes that the proposed categorization methodology is capable of producing understandable, reliable, relevant, consistent, and comparable results for stakeholders when identifying the type of transactions prevalent in governments, whether those transactions are recurring or unusual, because the foundation of the categorization methodology focuses on the characteristics of transactions. An effective and consistent categorization process would allow preparers and auditors of financial statements to identify the appropriate recognition and measurement provisions for each type of transaction, and, therefore, the information presented in financial statements would be representative of that transaction, which would enhance the quality of information provided to financial statement users.

20. The Board believes that achieving the goal of comprehensive guidance is not feasible by only filling the gaps in existing literature because the fragmentation in the literature (as previously described) is a structural issue, in part because of the reliance on the subjective concept of value. Therefore, a consistent categorization methodology is necessary to (a) expand guidance where little or no guidance currently exists and (b) avoid incongruent recognition conclusions. Furthermore, it is expected that applying this consistent approach would help preparers and auditors better understand the underpinnings of revenue and expense recognition, which would assist them in reducing the inconsistent application observed in current practice.

21. As noted above, the expected outcome of this project for users of financial statements is an improvement in the understandability, consistency, and comparability of information they receive from governmental resource flows statements. That improvement enhances the reliability and relevance of that information, which would be expected to assist users in their assessment of interperiod equity. Interperiod equity “. . . help[s] users assess whether current-year revenues are sufficient to pay for the services provided that year and whether future taxpayers will be required to assume burdens for services previously provided.”

That is, the recognition of both revenues and expenses in the appropriate reporting period is critical to the decision usefulness of information and the assessment of accountability.

22. The Board believes that this new categorization methodology represents a fundamental shift in perspective about how transactions are considered in the governmental environment. Traditionally, stakeholders considered whether a transaction was an exchange depending on the amount of consideration associated with the transaction, thereby making the amount of consideration an indicator of equal value. However, the public-purpose motivation of the governmental environment runs counter to relying on the consideration amount as an identifying feature of the type of transaction. The proposed categorization methodology effectively minimizes reliance on the amount of consideration for categorization purposes and focuses on the characteristics of transactions, which the Board considers to be more relevant. The Board believes that this fundamental shift in perspective would establish a foundational approach, and thus the principles presented in this document could be applied in the future to address issues outside the scope of this project.

Objective of This Preliminary Views

23. The objective of this Preliminary Views is to seek stakeholder feedback about the Board’s current views related to a revenue and expense recognition model. Specific topics to consider include:which the respondent would like

Categorization of transactions into two types identified as Category A and Category B, based on the four steps described in Chapter 3

Asset recognition for Category A and Category B revenue transactions

Liability recognition for Category A and Category B expense transactions

Clarification of guidance regarding deferred inflows of resources and deferred outflows of resources for transactions in the scope of this project

Expansion of guidance for revenue and expense recognition for Category A transactions

Measurement principles.

24. The Board intends to redeliberate those topics based on feedback received on this Preliminary Views before issuing an Exposure Draft of a proposed Statement for public comment. Additional topics that are expected to be addressed in that Exposure Draft that are not included in this Preliminary Views include:

a. Binding arrangement modifications, combinations, and transactions partially in the scope of other projects

b. Recognition of revenue and expense

(1) Recognition over time—estimation of progress

(2) Recognition of a series

c. Measurement of revenue and expense

(1) Determining the transaction amount

(2) Allocating the transaction amount.

Considerations Related to Benefits and Costs

25. One of the principles guiding the GASB’s setting of standards for accounting and financial reporting is the assessment of expected benefits and perceived costs. The GASB strives to determine that its standards address a significant user need and that the costs incurred through the application of its standards, compared with possible alternatives, are justified when compared with the expected overall public benefit. The potential benefits of the model are highlighted throughout this Preliminary Views. At this point, the GASB has not fully assessed the potential costs of implementing the model. One purpose of this Preliminary Views is to obtain additional input on the perceived challenges (which could equate to costs) and expected benefits associated with the improved information.

CHAPTER 2—FOUNDATIONAL PRINCIPLES FOR THE MODEL

1. As discussed in Chapter 1, the objective of this project is to develop a comprehensive, principles-based model that establishes categorization, recognition, and measurement guidance applicable to a wide range of revenue and expense transactions. In order to accomplish that objective, the Board concluded that establishing foundational principles for certain aspects of the model was needed so that preliminary views reached by the Board related to the three components of the model were consistent. This chapter describes the Board’s preliminary views associated with the foundational principles of the revenue and expense recognition model and explains the rationale for those views. Some of the principles discussed in this chapter also are expressed as preliminary views in other chapters.

Five Model Assumptions

2. The Board used the following five model assumptions as underpinnings for the development of the revenue and expense recognition model:

Model assumption 1: Revenues and expenses are of equal importance in resource flows statements.

Model assumption 2: Revenues and expenses should be categorized independently and not in relation to each other.

Model assumption 3: For accounting and financial reporting purposes, the government is an economic entity and not an agent of the citizenry.

Model assumption 4: Symmetry should be considered, to the extent possible, in the application of the three components of the model.

Model assumption 5: A consistent viewpoint, from the resource provider perspective, should be applied in the analysis of revenues and expenses.

Equal Importance of Revenues and Expenses

3. Model assumption 1 allows for the proposed recognition principles in this model to be applied independently for revenues and expenses, so that the recognition of a revenue or an expense is not influenced by a related revenue or expense. In arriving at that conclusion, the Board considered whether revenues should be dependent on the recognition of the related costs of service or whether expenses should be recognized by matching them to the revenues they generate. Historically, that matching principle may have been the basis for determinations about the period in which expenses were recognized in some private-sector accounting standards. That approach effectively subordinates expense recognition to revenue recognition. The Board acknowledges that matching is not a principle in the GASB conceptual framework; rather, that framework identifies interperiod equity as the key relationship between revenues and expenses because it “. . . help[s] users assess whether current-year revenues are sufficient to pay for the services provided that year. . . .”

For that reason, the Board concluded that revenues and expenses should be recognized independently by relying on their respective definitions:

------------------------------------

4Net assets are assets netted with liabilities.

4. The main recognition attribute of revenue and expense transactions is the inflow’s or outflow’s applicability to a reporting period. Therefore, the Board concluded that applicability to a reporting period also should be assessed independently for revenues and expenses. That approach would allow for information presented in resource flows statements to adequately represent the results of that reporting period’s activity, which allows for a better assessment of interperiod equity and, as a result, government accountability.

Independent Categorization of Revenues and Expenses

5. Model assumption 2 allows for the categorization of expense transactions independently from the source of revenue to which the expense relates. That is, revenue transactions are categorized independently from the programs they fund. In practice, the categorization of expense transactions is not always considered independently from revenues. Some stakeholders may categorize expense transactions based on the category of the source of funds. For example, if a city relies on property taxes to fund public safety, some stakeholders may conclude that public safety expense transactions would be categorized in the same manner as property tax transactions.

6. The Board believes that an independent categorization of revenue and expense transactions is appropriate because the categorization of expense transactions should be based on their characteristics and should not be affected by public policy, which may seek to associate specified revenues with the provision of certain goods or services (further discussed in paragraphs 11–16 in this chapter). If the revenue transaction categorization were to dictate the categorization of expense transactions, the categorization of expense transactions could be inconsistent among governments solely because of public policy effects. For example, it has been observed that solid waste collection services can be funded by at least three approaches:(a) a government may charge fees to recover the entire cost of the service, (b) a government may rely entirely on property taxes to provide the service, or (c) a government may charge fees to partially recover the cost of the service and subsidize the remainder with general resources of the government. If expense transactions were categorized based on the revenue policy used to fund the activity, the solid waste expenses would be categorized differently in each of those three scenarios.

Government as an Economic Entity

7. Considering the government as an economic entity (model assumption 3) prevents reporting revenues net of expenses, or expenses net of revenues for related transactions in the scope of this project. Some stakeholders believe that from a public policy perspective, a government acts as an agent of the citizenry. However, if that belief is further extended to accounting and financial reporting, one could argue that to represent its role as an agent, a government should recognize revenues and expenses net of each other for the activities and services provided to the citizenry. The Board believes that the financial information of a government would be obscured by netting revenues and expenses and, for that reason, concluded that for accounting and financial reporting purposes, a government is an economic entity.

8. Furthermore, the Board concluded that if a government believes it may be acting as an agent (custodian) in a specific activity, the government should first assess whether it is engaged in a fiduciary activity by applying the provisions of Statement No. 84, Fiduciary Activities.

Symmetrical Considerations

9. Model assumption 4 allows for categorization, recognition, and measurement proposals that are consistent between revenues and expenses and among categories of transactions. The symmetrical consideration is not intended to convey that symmetrical results are necessary between revenue and expense recognition. Rather, the intent of this model assumption is to convey that symmetrical principles should be developed for categorization, recognition, and measurement proposals applicable to revenues and expenses. It should be noted that in practice, recognition outcomes (in other words, when an item is recognized as an element of financial statements) may be different because of unavailability of information or reliance on estimates.

Consistent Viewpoint

10. Model assumption 5 allows for the use of a consistent point of view when analyzing distinct goods or services and the transfer of control of resources. In Chapters 4 and 5, the Board expresses a preliminary view regarding the proposed application of a performance obligation recognition approach. In support of that view, model assumption 5 establishes that the point of view of the party that is incurring the expense (the counterparty in revenue transactions and the government in expense transactions) should be relied upon in the analysis to identify distinct goods or services and transfer of control of a resource. As explained in Chapter 4, the assessment of distinct goods or services is informed by the characteristics of the identified goods or services within the context of the binding arrangement.

Model Underpinnings and Expense Transactions

11. As previously mentioned, the outcomes of model assumptions 1 and 2 allow the Board to propose independent categorization and recognition for expense transactions. The Board believes that it is necessary to establish this foundational principle because existing accounting literature is limited with regard to expense recognition. Some stakeholders believe that the appropriate recognition underpinning for expense transactions is to subordinate their recognition to revenues so that expenses can be matched

to the corresponding revenue. Model assumptions 1 and 2 prevent expense recognition based on matching. Matching also is not relevant in reporting for business-type activities because the GASB’s conceptual framework does not apply different concepts to governmental activities and business-type activities.

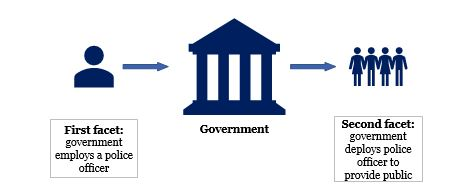

12. Some stakeholders believe that the appropriate conceptual underpinning for expense recognition is to rely on the revenue transaction category. That is, expense transactions could be categorized depending on the source of revenue that funds the activity. That approach focuses on identifying a relationship between the revenue and the benefit of the related expense transaction. In order to assess whether that approach was reliable for governments, the Board studied the effects of benefits in expense transactions. In the analysis, the Board identified two distinct facets in expense transactions. The first facet is the relationship between the government and the counterparty, and the second facet is the relationship between the government and the citizenry it serves (the benefit aspect).

13. Consider an expense transaction in which a government employs a police officer and deploys the police officer’s service capacity to provide public safety; the question is, who benefits from the service?

The first facet in the expense transaction is the relationship between the government and the police officer. The second facet in the expense transaction is the relationship between the government and the recipient of the police protection. When considering the categorization of the expense transaction, the Board concluded that reliance on the first facet produced consistent results, whereas reliance on the second facet produced inconsistent results.

14. As explained in Appendix A, the public nature of governmental goods or services usually produces positive externalities (benefits that reach a broader audience than the direct resource recipients). As a government incurs expenses in the provision of public services, the expense transactions may produce far-reaching benefits for the citizenry. Therefore, identifying the specific beneficiary of the transaction is inherently more challenging because governments would need to assess whether the benefit of governmental expenses is to provide services to the society as a whole, a specific segment of a society, or an individual. If the police officer in the example responds to an emergency call to assist a homeowner whose home is being burglarized and the police officer captures the alleged perpetrator, how would the assessment of benefit be made? The homeowner is the direct beneficiary; however, the neighborhood and potentially the city also would benefit from the police officer’s actions. Therefore, the identification of a beneficiary is not straightforward. Furthermore, the second facet of the transaction, the relationship between the government and the society, also conveys information about the government’s public policy decisions—which services should be provided. Given the challenges of identifying benefits and the influence of public policy decisions, it usually is not reliable to analyze expenses by focusing on the second facet of expense transactions.

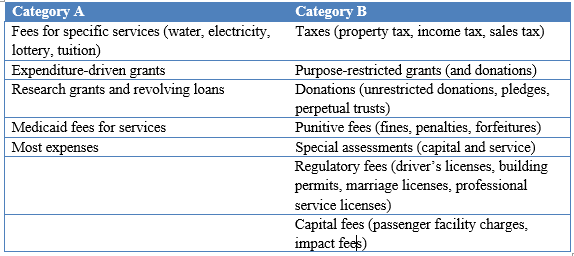

15. Conversely, the Board considered focusing expense categorization on the first facet of the expense transaction and concluded that it produces consistent results because it avoids the challenge of identifying beneficiaries. It should be noted that this approach results in a majority of expense transactions in the governmental environment being identified as Category A transactions. For example, employee salaries would be identified as Category A expenses regardless of whether the employee’s salary is funded by fees or property taxes, or whether the employee’s work provides an exclusive benefit to fee payers (such as utilities) or general benefits to society as a whole (such as public safety). Very few expense transactions would be identified as Category B. Examples of Category B expense transactions would include purpose-restricted grants, shared revenues, and general aid to governments.

16. At present, some stakeholders believe that expenses funded through taxes should be considered nonexchange transactions because the benefits of the expense transactions are provided for the collective benefit of the citizenry. The tentative decisions of the Board in this project apply a different approach. The Board acknowledges that this approach to categorization of expense transactions represents a major change from the way that some governmental expenses may have been viewed in the past. The Board believes that this approach would produce more consistent results when governments assess transactions as Category A or Category B and thereby would result in the application of the appropriate recognition guidance for expenses.

Categorization Methodology

17. The categorization methodology, as explained in Chapter 1, was developed by considering the effective characteristics identified in the exchange/nonexchange methodology and the performance obligation/no performance obligation methodology. The two major characteristics that provided the categorization underpinnings were (a) “something for something,” which was identified by stakeholders as a means to assess exchange transactions, and (b) the identification of performance obligations. Combining those two major characteristics resulted in the principles expressed in Chapter 3 for categorization. That is, Category A transactions represent an acquisition of resources coupled with a sacrifice of resources that are interdependent. Category B transactions are acquisitions without sacrifices, sacrifices without acquisitions, or acquisitions and sacrifices that are not interdependent.

Recognition Methodology

18. A recognition methodology was developed by combining the definitions of an inflow of resources and an outflow of resources with the hierarchy of recognition for elements of financial statements (hierarchy of recognition).

Because this methodology was derived from the conceptual framework, it is applied to all revenue and expense transactions regardless of their category. It is notable that the recognition methodology described in detail in paragraphs 20–31 in this chapter is an analytical tool that assisted in the development of principles-based guidance, which is presented in Chapters 4 and 5. Application guidance is more specific and is tailored to whether the transaction being analyzed is identified as Category A or Category B. For that reason, stakeholders would not be expected to apply the recognition methodology described in this chapter but could rely on this analytical tool to better understand the application proposals expressed as preliminary views of the Board in Chapters 4 and 5.

19. As a result of relying on the hierarchy of recognition, the recognition methodology described in this section focuses on the recognition of assets (increase in net assets) for revenue transactions and the recognition of liabilities (decrease in net assets) for expense transactions. Some stakeholders find this approach counterintuitive because they believe the focus should be on the recognition of revenues and expenses directly. The Board concluded that reliance on the hierarchy of recognition provides a methodical and disciplined approach for achieving the objective of providing principles-based guidance for a broad range of revenue and expense transactions.

Revenue Recognition

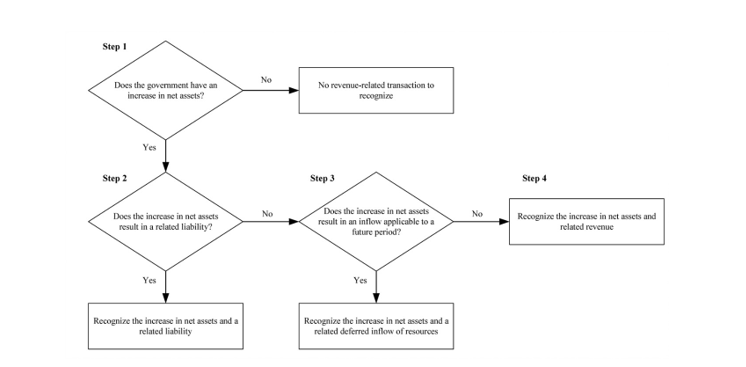

20. The proposed revenue recognition methodology consists of four steps as listed below and as depicted in the subsequent flowchart.

Step 1: Does the government have an increase in net assets?

Step 2: Does the increase in net assets result in a related liability?

Step 3: Does the increase in net assets result in an inflow of resources applicable to a future period?

Step 4: Recognize revenue.

21. Net assets are described as assets netted with liabilities.

The focus of the recognition methodology developed in this project is to consider each element of financial statements independently. The purpose of step 1 is to assist governments in determining whether an item should be recognized as an element of financial statements. Therefore, the determination of whether there is an increase in net assets in a revenue transaction in step 1 is based on consideration of the existence of a receivable, the receipt of cash, the extinguishment of a liability by a counterparty, or a combination of those circumstances that effectively increases net assets—but without considering whether that increase in net assets also represents a related liability (step 2), a deferred inflow of resources (step 3), or a revenue (step 4). Steps 2–4 of the recognition methodology assist in identifying the appropriate element of financial statements that should accompany the recognition of the increase in net assets (step 1).

Step 1: Does the Government Have an Increase in Net Assets?

22. The first step in the revenue recognition methodology is to determine the point in time at which a government has an increase in net assets (in isolation from any other element that arises from the transaction). An increase in net assets can be evidenced by (a) a legally enforceable claim that is a receivable, (b) the receipt of resources from a counterparty as an advance, (c) another party’s extinguishment of liabilities on behalf of the government, or (d) a combination of a–c pursuant to a revenue transaction. Determining that a government has an increase in net assets establishes that a revenue-related transaction has occurred that requires recognition of an element of financial statements—generally, the inception of the transaction.

Step 2: Does the Increase in Net Assets Result in a Related Liability?

23. The second step in the recognition methodology is to determine whether a government has a present obligation related to the increase in net assets. The Board concluded that a related liability arises if a government receives resources before a legally enforceable claim has been established (in which case, the resources are an advance). The Board concluded that a liability should be recognized regardless of whether the resources are refundable. For example, resources received prior to the government satisfying its performance obligation in a Category A transaction would represent a related liability (that is, a present obligation to perform). Similarly, if a government receives property tax payments before the government has imposed a levy, the government has an increase in net assets that results in a related liability (a present obligation) because the government has received resources in advance of having established a legally enforceable claim to those resources through the imposition of the property tax.

Step 3: Does the Increase in Net Assets Result in an Inflow of Resources Applicable to a Future Period?

24. The third step in the recognition methodology is to determine whether an increase in net assets that does not have a related liability should result in the recognition of a deferred inflow of resources. To make that assessment, the Board proposed recognition attributes that would assist stakeholders in determining the applicability to a reporting period of inflows of resources in the scope of this project. (See the discussion of applicability to a reporting period in paragraphs 32–35 in this chapter.) The rationale for this approach relates to the constraint imposed by the conceptual framework regarding the recognition of certain elements, as follows: “Recognition of deferred outflows of resources and deferred inflows of resources should be limited to those instances identified by the GASB in authoritative pronouncements, which are established after applicable due process procedures.”

Based on the attributes presented in paragraph 33 in this chapter, for example, a government that has imposed a property tax would recognize a receivable and a deferred inflow of resources if the property tax is imposed for a subsequent reporting period.

Step 4: Recognize Revenue

25. The fourth step in the recognition methodology provides for the recognition of revenue as a result of the prior steps; that is, an increase in net assets has been identified that does not have a related liability and is not applicable to a future period. Consequently, the government would recognize the increase in net assets as revenue. Proposals related to application guidance for revenue recognition are presented in Chapter 4.

Expense Recognition

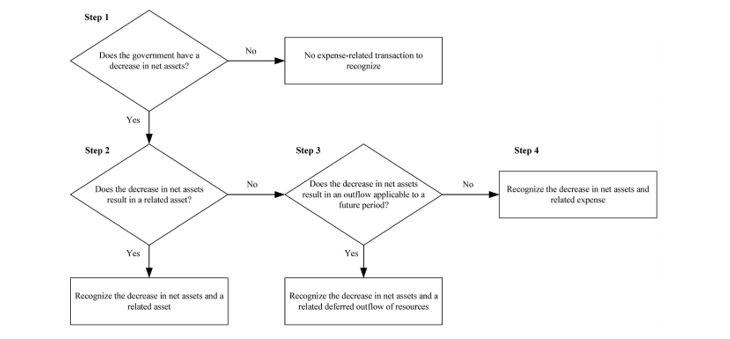

26. Similar to the revenue recognition methodology, the proposed expense recognition methodology consists of four steps as listed below and depicted in the subsequent flowchart.

Step 1: Does the government have a decrease in net assets?

Step 2: Does the decrease in net assets result in a related asset?

Step 3: Does the decrease in net assets result in an outflow of resources applicable to a future period?

Step 4: Recognize expense.

27. As previously noted, net assets are defined as assets netted with liabilities. The focus of the recognition methodology developed in this project is to consider each element of financial statements independently. The purpose of step 1 is to assist governments in determining whether an item should be recognized as an element of financial statements. Therefore, the determination of whether there is a decrease in net assets in an expense transaction in step 1 is based on a consideration of the existence of a payable, the provision of cash to a counterparty, or a combination of those circumstances that effectively decreases net assets—but without considering whether that decrease in net assets also represents a related asset (step 2), a deferred outflow of resources (step 3), or an expense (step 4). Steps 2–4 of the recognition methodology assist in identifying the appropriate element of financial statements that should accompany the recognition of the decrease in net assets (step 1).

Step 1: Does the Government Have a Decrease in Net Assets?

28. The first step in the expense recognition methodology is to determine the point in time at which a government has a decrease in net assets (in isolation from any other element that arises from the transaction). A decrease in net assets is evidenced by (a) a present obligation that is a liability, (b) the provision of resources to a counterparty before a liability arises, or (c) a combination of both pursuant to an expense transaction. Determining that a government has a decrease in net assets establishes that an expense-related transaction has occurred that requires recognition of an element of financial statements—generally, the inception of the transaction.

Step 2: Does the Decrease in Net Assets Result in a Related Asset?

29. The second step in the recognition methodology is to determine whether a government has an asset (for example, a prepaid item)

related to the decrease in net assets. The Board concluded that a related asset arises if a government provides resources to its counterparty before the government has incurred a liability (in which case the resources are a prepaid item). For example, if a government pays in advance for cleaning services the government expects to receive in subsequent months, the government has a decrease in net assets that results in a related asset—a prepaid item.

Step 3: Does the Decrease in Net Assets Result in an Outflow of Resources Applicable to a Future Period?

30. The third step in the recognition methodology is to determine whether a decrease in net assets that does not have a related asset should result in the recognition of a deferred outflow of resources. To make that assessment, the Board proposed recognition attributes that would assist stakeholders in determining the applicability to a reporting period of outflows of resources in the scope of this project. (See the discussion of applicability to a reporting period in paragraphs 32–35 in this chapter.) As mentioned in paragraph 24, the conceptual framework includes a constraint that prohibits the recognition of deferred outflows of resources unless authoritative pronouncements provide for recognition of that element.

Step 4: Recognize Expense

31. The fourth step in the recognition methodology provides for the recognition of expense as a result of the prior steps; that is, a decrease in net assets has been identified that does not have a related asset and is not applicable to a future period. Consequently, the government would recognize the decrease in net assets as an expense. Proposals related to application guidance for expense recognition are presented in Chapter 5.

Applicability to a Reporting Period and Recognition of Deferred Inflows of Resources and Deferred Outflows of Resources

32. The recognition methodology for both revenues and expenses described in the previous sections requires the consideration of an inflow’s or an outflow’s applicability to a reporting period to assess whether it should be recognized as a deferred inflow of resources or a deferred outflow of resources (step 3 in paragraphs 24 and 30, respectively). In order to develop principles-based guidance for step 3, the Board considered the appropriate level of prescriptiveness of the guidance to be able to develop the revenue and expense recognition model. In other words, the Board considered the level of guidance necessary to both retain the aforementioned conceptual constraint and provide effective guidance for transactions in the scope of this project without creating a finite list of transactions requiring deferral recognition. For transactions in the scope of this project, the Board believes it is possible to identify recognition attributes that would allow stakeholders to determine whether an increase or decrease in net assets is applicable to a future reporting period.

33. The Board’s preliminary view is that for Category A revenue and expense transactions, in applying the hierarchy of recognition, the attribute that establishes applicability to a reporting period is the satisfaction of a performance obligation in that period. The Board’s preliminary view is that for Category B revenue and expense transactions, in applying the hierarchy of recognition, the attribute that establishes applicability to a reporting period is compliance with time requirements in that period. The Board acknowledges that for transactions outside the scope of this project, those recognition attributes do not adequately describe the circumstances in which existing guidance requires the recognition of deferred inflows of resources and deferred outflows of resources. Therefore, the Board noted that those attributes are limited to transactions in the scope of this project. Moreover, this preliminary view should not be analogized to transactions outside the scope of this project.

34. A practical consequence of the preliminary view expressed in paragraph 33 is that Category A revenue and expense transactions in the scope of this project would not result in the recognition of deferred inflows of resources or deferred outflows of resources (even in governmental funds because, as explained in Chapter 7, the Board has proposed to no longer consider the period of availability in the Recognition Concepts Exposure Draft). Another practical consequence is that Category B transactions would include the recognition of both deferred inflows of resources and deferred outflows of resources for circumstances in which a transaction includes a time requirement that has not been met.

35. In reaching those conclusions, the Board considered relevant conceptual framework guidance, which establishes that “. . . financial reporting should help users assess whether current-year revenues are sufficient to pay for the services provided that year and whether future taxpayers will be required to assume burdens for services previously provided.”

The Board concluded that proposing two recognition attributes to describe a transaction’s applicability to a reporting period would assist stakeholders in presenting information in resource flows statements consistently from period to period. In turn, the transactions would be more representational of interperiod equity. It also is notable that this proposal is consistent with model assumption 1: revenues and expenses are of equal importance (paragraph 2a in this chapter). Thereby, their recognition is independent and related to their respective applicability to a reporting period. That approach avoids the subordination of one element to another for recognition purposes.

Category A Transaction Principles

36. As already discussed in the categorization and recognition principles sections, the Board agreed to propose a performance obligation recognition methodology for Category A revenue and expense transactions. Consequently, the Board concluded that it was important to establish a structural relationship between categorization, recognition, and measurement that would produce cohesive results. The Board concluded that the relationship between the three model components is established through the unit of account,

which has been identified as a performance obligation only for Category A transactions.

37. A recognition unit of account identifies the level of aggregation or disaggregation at which an asset or a liability should be recognized. The Board proposes that the identification of performance obligations (that is, the identification of the recognition units of account) consists of the identification of each distinct good or service in a binding arrangement. (Specific proposals to identify distinct goods or services are included in paragraphs 12–16 in both Chapters 4 and 5.) The relationship between a performance obligation, a distinct good or service, and a recognition unit of account is illustrated below.

38. The consistency between categorization, recognition, and measurement for Category A transactions is achieved through the identification of a consistent recognition unit of account— a performance obligation.

39. The categorization proposal presented in Chapter 3 results in the identification of transactions that contain at least one performance obligation as Category A. The Board concluded that the categorization methodology generally should be applied at a binding arrangement level, unless the government expects that the binding arrangement evidences both Category A and Category B transactions. Nevertheless, the categorization approach is used to identify transactions that include performance obligations, each of which is a recognition unit of account. (The relationship between binding arrangements and transactions is described in paragraph 9 in Chapter 7.)

40. Furthermore, the Board’s preliminary views expressed in Chapter 6 conclude that measurement would be applied to each performance obligation as an allocated amount.

Transfer of Control of a Resource

41. The Board further elaborated on the recognition attribute of the satisfaction of a performance obligation, which establishes the recognition of revenues and expenses. The Board believes that satisfaction of a performance obligation occurs when there is a transfer of control of resources (distinct goods or services). That is, in revenue transactions, a government satisfies its performance obligation when the counterparty receives control of a resource. Conversely, in expense transactions, a counterparty satisfies its performance obligation when a government receives control of a resource. As explained in Chapters 4 and 5, the Board believes that the transfer of control of resources happens either at a point in time or over time. For that reason, the Board proposes criteria to identify the circumstances in which recognition occurs over time. The Board further proposes that recognition at a point in time occurs when none of those criteria are met.

42. The Board focused on the transfer of control of a resource as the meaningful point in time at which a performance obligation is satisfied because it evidences the point at which a party to a transaction can utilize the present service capacity and determine the nature and manner of use of the present service capacity embodied in the goods or services provided by the counterparty.

Measurement Methodology

43. For this Preliminary Views, the Board considered basic measurement proposals to establish a measurement methodology. As discussed previously, the Board proposes a foundational measurement principle, applicable to both Category A and Category B transactions, that assets and liabilities be measured directly, and revenues and expenses be measured through their related asset or liability. Based on that measurement principle, the amount of consideration received, or receivable, would inform the amount of revenue to be recognized. Furthermore, the amount of consideration paid, or payable, would inform the amount of expense to be recognized. That approach is consistent with existing guidance and is identified in Chapter 6 as direct measurement of the most liquid item.

CHAPTER 3—CATEGORIZATION

1. This chapter describes the Board’s preliminary views regarding the categorization of revenue and expense transactions. As described in Chapter 1, categorization is the first component in the revenue and expense recognition model and is the process of classifying a transaction by identifying the relevant characteristics of that transaction in the context of a group of similar transactions. It is important to properly determine the type of transaction primarily because assets in revenue transactions and liabilities in expense transactions arise at different times depending upon the type of transaction. Correctly categorizing a transaction allows stakeholders to follow the appropriate recognition and measurement provisions for that type of transaction.

2. The categorization methodology described in this chapter represents a fundamental shift in perspective for revenue and expense transactions. Historically, revenue and expense transactions have been categorized as exchange, exchange-like, or nonexchange depending on an assessment of equal value. As highlighted in Chapter 1, reliance on equal value produces inconsistent categorization results. The Board believes that the four-step categorization methodology based on a transaction’s underlying characteristics presented in this chapter is a robust approach for determining the type of transaction. Furthermore, this categorization methodology minimizes reliance on the amount of consideration provided in a transaction, which historically has been used to indicate the transaction type. The model requires the exercise of professional judgment, as would any model. Nevertheless, the Board expects that the new methodology would produce consistent categorization results because it reduces reliance on subjective characteristics.

Categorization Methodology

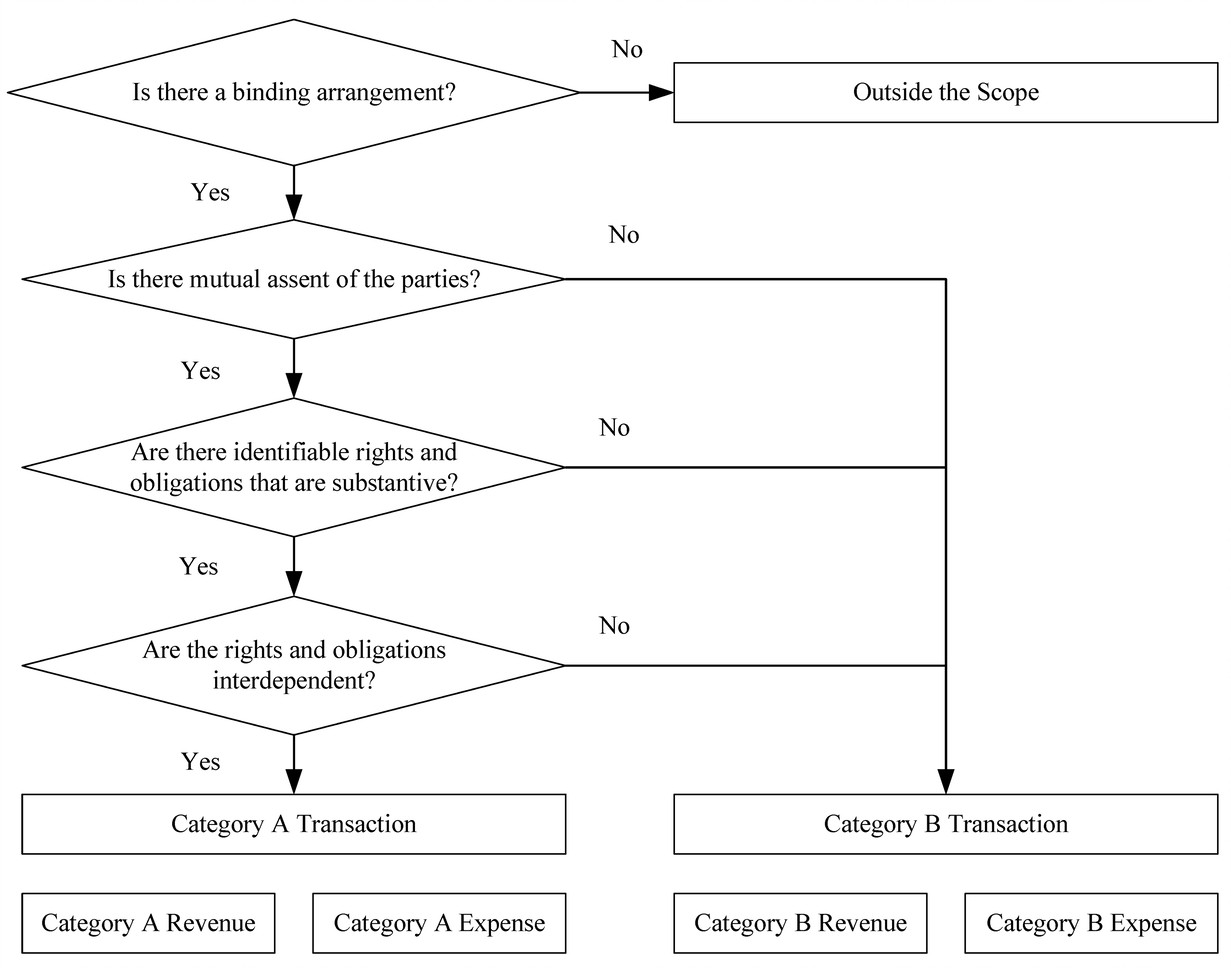

3. The Board’s preliminary view is that Category A revenue and expense transactions are composed of acquisitions coupled with sacrifices or sacrifices coupled with acquisitions that are interdependent. Category B revenue and expense transactions are acquisitions without sacrifices, sacrifices without acquisitions, or acquisitions and sacrifices that are not interdependent. To apply those principles, governments would follow a four-step categorization methodology outlined as follows:

Step 1: Is there a binding arrangement?

Step 2: Is there mutual assent of the parties?

Step 3: Are there identifiable rights and obligations that are substantive?

Step 4: Are the rights and obligations interdependent?

If a government cannot identify a binding arrangement, the transaction would be outside the scope of the model. If any of the required characteristics in steps 2, 3, or 4 are not present, the transaction would be classified as Category B. If a government identifies all four characteristics, the transaction would be classified as Category A.

4. The following flowchart illustrates the proposed categorization methodology.

5. The Board’s preliminary view is that transactions in the scope of this project should be evidenced by a binding arrangement. A binding arrangement is an understanding between two or more parties that creates rights, obligations, or both among the parties to a transaction. A binding arrangement would include a rebuttable presumption of enforceability and have economic substance. The term binding arrangement is intended to encompass a broad spectrum of arrangements, which can be written, oral, or implied by the government’s existing practices. Examples of written arrangements include contractual agreements, such as grant agreements, memorandums of understanding, and contracts. Additionally, legislation is an example of a binding arrangement that is not contractual in nature. Examples of more informal arrangements include the creation of a new customer account for water and sewer service from a public utility, the issuance of a legally enforceable purchase order, or the purchase of a ticket for a bus ride.

Rebuttable Presumption of Enforceability

6. Enforceability as described in this Preliminary Views is the ability of one or more parties in a transaction to compel other parties in the transaction to comply with the terms of a binding arrangement. In other words, the preliminary view expressed in paragraph 5 does not require that all the parties in the transaction have a means to compel compliance. For example, in property tax transactions, governments often rely on property liens to enforce tax collection; however, the taxpayer does not have the ability to enforce the binding arrangement.

7. Enforceability arises from the legal framework surrounding the binding arrangement, such as legislation, commercial code, or contract law. The preliminary view in paragraph 5 requires only the identification of a rebuttable presumption of enforceability to reflect specific challenges prevalent in the government environment. For example, states can defeat legally enforceable claims because they have sovereign powers. In other words, the preliminary view expressed in paragraph 5 does not require that governments have absolute certainty about the enforceability of a binding arrangement. Furthermore, a rebuttable presumption of enforceability conveys that even if a binding arrangement initially has been identified as enforceable, enforceability may be disproved at a later time. After an initial assessment, governments would not be required to reassess enforceability unless relevant facts and circumstances change.

8. Assessment of enforceability of a binding arrangement would not be limited to redress sought through a court of law. Although the most prevalent form of enforceability relies on court action, governments have additional mechanisms available to enforce the terms of a binding arrangement. Examples of those other enforceability mechanisms include reductions of future funding, debarment from a program, or coercive powers of sovereign governments. Another example of enforceability without the involvement of a court of law is when a public utility suspends service until a customer pays overdue bills.

9. The scope of this project also includes liabilities that arise from moral or constructive obligations. For example, state aid to school districts in cases in which the aid is not evidenced by a contractual type of binding arrangement generally cannot be enforced through the legal framework. In those cases, the transaction may include a moral or constructive obligation that the state has little or no discretion to avoid because of the potential social, moral, or economic consequences. In other words, the mechanism for enforcement for moral or constructive obligations that are liabilities is different from enforcement through legal actions, and although those transactions are not enforceable in a court of law, a government may successfully assert a rebuttable presumption of enforceability.

Economic Substance

10. A binding arrangement should have economic substance that results in economic consequences to the parties, such that there is an expected change in the risk, amount, or timing of the government’s cash flows or there is an expected change in the government’s service potential.

11. Economic substance should not be considered equivalent to significance (a materiality measure). Certain transactions in the government environment can be considered insignificant individually but would still have economic substance. For example, individual bus fares generally are insignificant amounts; however, for a transit authority, bus fares have economic substance and have an effect on the government’s service potential.

Failure to Identify a Binding Arrangement