Under

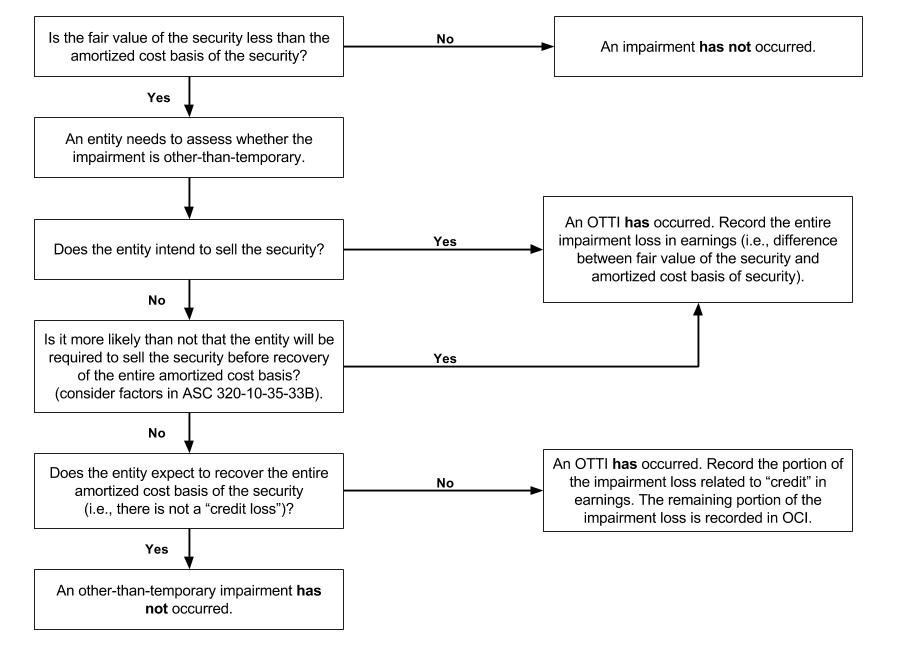

ASC 320-10-35-21, an available-for-sale or held-to-maturity debt security is considered to be impaired if its fair value is less than its amortized cost basis. An OTTI assessment is only required for securities that are considered impaired at the balance sheet date. It is possible that a credit loss may exist for a security whose fair value exceeds its amortized cost. However, in that case, the security would not be considered impaired, and no other authoritative guidance would require or permit recognition of the credit loss in earnings.

If a debt security is impaired, additional analysis is needed to determine whether the impairment is temporary or other-than-temporary. In making this determination, the various factors are assessed as follows:

- If an investor intends to sell an impaired debt security investment (that is, the investor has decided to sell the security), the impairment is considered to be other-than-temporary.

- If an investor does not intend to sell the impaired debt security, the investor must consider available evidence to assess whether it will more likely than not (MLTN) be required to sell the security before the recovery of its amortized cost basis (for example, whether its cash or working capital requirements, or contractual or regulatory obligations, indicate the security will be required to be sold before a forecasted recovery occurs). If the investor will MLTN be required to sell the security before recovery of its amortized cost basis, the impairment is considered to be other-than-temporary.

- If the investor does not intend to sell the impaired security and it is not MLTN that the investor will be required to sell the impaired security, the analysis moves on to determine whether a credit loss exists.

- If an investor does not expect to recover the entire amortized cost basis of the impaired security (that is, a credit loss exists), the investor would be unable to assert that it will recover its amortized cost basis even if it does not intend to sell the security or it is not MLTN required to sell the security. Therefore, in those situations, the impairment is considered to be other-than-temporary.

In assessing whether the amortized cost basis of an impaired security will be recovered, an investor must compare the present value of cash flows expected to be collected from the security with the amortized cost basis of the security. If the present value of the cash flows expected to be collected is less than the amortized cost basis of the security, the entire amortized cost basis of the security will not be recovered (that is, a credit loss exists), and an other-than-temporary impairment is considered to have occurred.

In determining whether a credit loss exists, the investor should use its best estimate of the present value of the cash flows expected to be collected from the debt security. One way of estimating the amount would be to consider the methodology in

ASC 310-10-35-22 through

ASC 310-10-35-27. When applying

ASC 310-10, the investor should discount the expected cash flows at the effective rate implicit in the debt security in the period before an other-than-temporary impairment is recognized. That effective interest rate will likely be the same rate as at the date of acquisition, unless the company estimates prepayments in accordance with

ASC 310-20-35-26.

For debt securities that are beneficial interests in securitized financial assets within the scope of

ASC 325-40, an investor must determine the present value of cash flows expected to be collected considering the guidance in

ASC 325-40-35-4 for determining whether there has been a decrease in cash flows expected to be collected from cash flows previously projected. The cash flows estimated at the current financial reporting date must be discounted at a rate equal to the current yield used to accrete the beneficial interest. See

ARM 5010.4518.

For debt securities accounted for under

ASC 310-30, an entity must consider that guidance in estimating the present value of cash flows expected to be collected from the debt security. See

ARM 5010.4516.

For trading securities, unrealized holding losses are included in earnings. It is generally not necessary to evaluate trading securities for impairment. However,

ASC 325-40-15-7 states: "For income recognition purposes, beneficial interests classified as trading are included in the scope of this Subtopic because it is practice for certain industries (such as banks and investment companies) to report interest income as a separate item in their income statements, even though the investments are accounted for at fair value." The method for recognizing and measuring interest income should not vary because the beneficial interest is classified as held-to-maturity, available-for-sale or trading, and the amount recognized each period should also be the same regardless of the classification of the security. For companies that separately report interest income, we believe that it would be necessary to evaluate

ASC 325-40 securities for impairment. This is because, as the investor updates and recalculates the amount of accretable yield for the beneficial interest each period, an assessment of the excess estimated cash flows over the security's reference amount is performed. As defined in

ASC 325-40-35-4: "The reference amount is equal to the initial investment minus cash received to date minus other-than-temporary impairments recognized in earnings to date plus the yield accreted to date." Without assessing and recognizing OTTI each period, the investor may inaccurately account for the reference amount of the security, thus impacting the accretable yield and interest income recognized each period. Thus, even if certain

ASC 325-40 securities are reported at fair value, investors that separately report interest income should continue to account for the reference amount, including OTTI, each period, in order to accurately determine the amount of interest income to be reported for the security.

There are numerous factors to be considered when evaluating whether a credit loss exists. See

ARM 5010.4512.

This model is illustrated in the following diagram

: