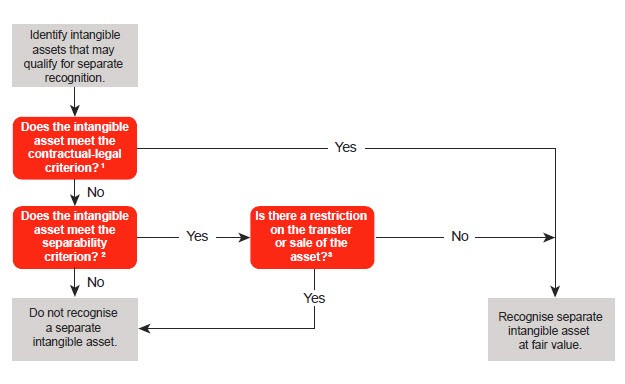

Example BCG 4-1, Example BCG 4-2, and Example BCG 4-3 demonstrate the application of the identifiable criteria when determining whether an intangible asset should be recognized in a business combination.

EXAMPLE BCG 4-1

Sales to customers through contracts

Company X acquires Company Y in a business combination on December 31, 20X1. Company Y conducts business with its customers solely through purchase orders. At the acquisition date, Company Y has customer purchase orders in place from 60% of its customers, all of whom are recurring customers. The other 40% of Company Y’s customers are also recurring customers. However, as of December 31, 20X1, Company Y does not have any open purchase orders with those customers.

Which portion of Company Y's customer relationships would be recognized and measured at the acquisition date?

Analysis

Company X needs to determine whether any of the acquired customer relationships are identifiable intangible assets that should be recognized. The purchase orders (whether cancellable or not) in place at the acquisition date from 60% of Company Y’s customers meet the contractual-legal criterion. Further, Company X needs to determine if a production backlog arises from the acquired purchase orders as this may meet the contractual-legal criterion for recognition. Consequently, the relationships with customers through these types of contracts also arise from contractual rights and, therefore, meet the contractual-legal criterion. The fair value of these customer relationships are recognized as an intangible asset apart from goodwill. Additionally, since Company Y has established relationships with the remaining 40% of its customers through its past practice of establishing contracts, those customer relationships would also meet the contractual-legal criterion and be recognized at fair value. Therefore, even though Company Y does not have contracts in place at the acquisition date with a portion of its customers, Company X would consider the value associated with all of its customers for purposes of recognizing and measuring Company Y’s customer relationships.

EXAMPLE BCG 4-2

Deposit liabilities and related depositor relationships

A financial institution that holds deposits on behalf of its customers is acquired. There are no restrictions on sales of deposit liabilities and the related depositor relationships.

Should deposit liabilities and related depositor relationships be accounted for at the acquisition date?

Analysis

Yes. Deposit liabilities and the related depositor relationship intangible assets may be exchanged in observable exchange transactions. As a result, the depositor relationship intangible asset would be considered identifiable and meet the separability criterion since the depositor relationship intangible asset can be sold in conjunction with the deposit liability.

EXAMPLE BCG 4-3

Unpatented process closely related to a trademark

An acquiree, a food and beverage manufacturer, sells hot sauce using a secret recipe. The acquiree owns a registered trademark, a secret recipe formula, and unpatented process used to prepare its famous hot sauce. If the trademark is sold, the seller would also transfer all knowledge associated with the trademark, which would include the secret recipe formula and the unpatented process used to prepare its hot sauce.

How should the trademark and complementary assets be accounted for at the acquisition date?

Analysis

The acquirer would recognize an intangible asset for the registered trademark based on the contractual-legal criterion. Separate intangible assets would also be recognized for the accompanying secret recipe formula and the unpatented process based on the separability criterion. The separability criterion is met because the secret recipe formula and unpatented process would be transferred with the trademark. As discussed in

BCG 4.4, the acquirer may group complementary intangible assets (registered trademark, related secret recipe formula, and unpatented process) as a single intangible asset if their useful lives are similar.