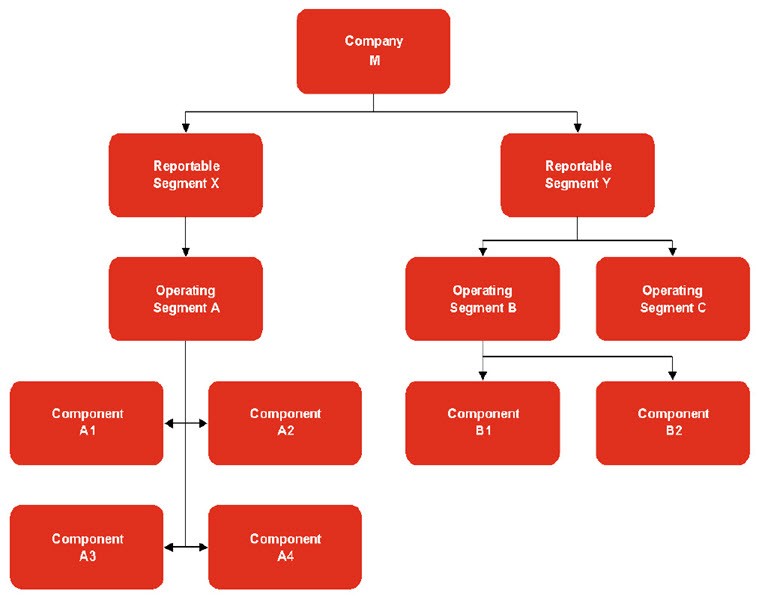

Figure BCG 9-2 provides a summary of the various reporting levels that may exist within an entity and how the reporting levels are used in determining an entity’s reporting units.

Figure BCG 9-2

Reportable segment versus operating segment versus component

Term and definition |

Use in determining reporting units |

|

- The reporting level that is disclosed for financial reporting purposes.

- Operating segments may be aggregated into one or more reportable segments if they meet specified criteria.

- An operating segment could be a reportable segment if an entity does not aggregate its operating segments for reporting purposes.

|

- Not applicable unless a reportable segment is an operating segment. Reporting units must be at the operating segment level or one level below the operating segment.

|

|

- Engages in business activities from which it may recognize revenues and incur expenses.

- Discrete financial information is available.

- Operating results are regularly reviewed by the CODM to allocate resources and assess performance.

|

An operating segment will be a reporting unit if:

- All of its components have similar economic characteristics.

- None of its components is a reporting unit.

- It comprises a single component.

Note: Unlike a component, as described below, an operating segment need not constitute a business to be deemed a reporting unit.

|

|

- One level below an operating segment.

|

A component may be a reporting unit if:

- The component constitutes a business for which discrete financial information is available.

- Segment management regularly reviews the component’s operating results.

However, components of an operating segment should be aggregated into a single reporting unit if they have similar economic characteristics, as defined by ASC 350-20-55. |

Example BCG 9-1 provides an example of the identification of reporting units.

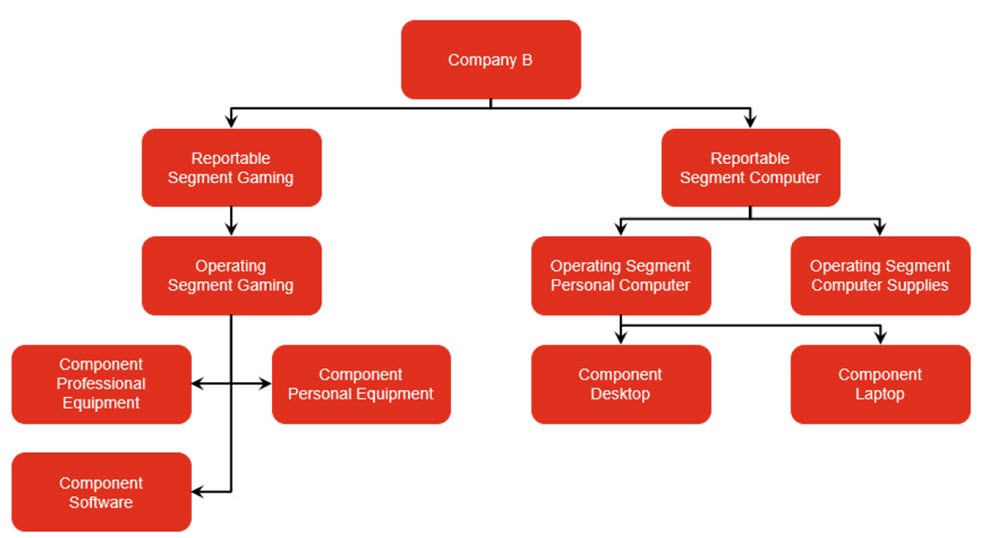

EXAMPLE BCG 9-1

Identification of reporting units

Company B manufactures, markets, and sells electronic equipment, including computers and gaming equipment for professional (e.g., casinos and gaming halls) and personal use. Company B’s CEO has been identified as the CODM and, on a monthly basis, receives, among other information, divisional income and cash flow statements for each operating segment, as well as sales on a product line basis. Based on the organizational structure of the company and information used to assess performance and allocate resources, management identified the following structure:

For segment reporting, Company B reports “Gaming” as a reportable segment and aggregates its two computer-related operating segments into a reportable segment “Computer.” Two of the three operating segments have various components that are businesses for which discrete financial information is available, and segment management regularly reviews the operating results of the businesses. The components “Personal Equipment,” “Software,” and “Desktop” have similar economic characteristics based on the nature of the products and the types of customers. Company B will have at least three reporting units (operating segments “Gaming,” “Personal Computer,” and “Computer Supplies”), and might have as many as six reporting units (five components and the operating segment “Computer Supplies”).

How many reporting units should Company B identify?

Analysis

Upon analyzing the economic characteristics of the identified components, Company B would likely conclude that:

- Component “Professional Equipment” is not economically similar to the components “Personal Equipment” and “Software,” so this component would be a separate reporting unit

- Components “Personal Equipment” and “Software” of the Gaming operating segment should be aggregated into a single reporting unit because they have similar economic characteristics

- The economic similarities between the “Desktop” and “Laptop” components of “Personal Computer” are not sufficient for them to be aggregated so these components would be separate reporting units

- The “Personal Equipment” and “Software” components share very similar economic characteristics with the “Desktop” component. Despite these similarities, the “Desktop” component must be treated separately because it resides in a different operating segment than components “Personal Equipment” and “Software”

- Operating segment “Computer Supplies” is a reporting unit because it does not have individual components

Company B would therefore identify five reporting units: “Professional Equipment,” “Personal Equipment and Software,” “Desktop,” “Laptop,” and “Computer Supplies.”