Once a reporting entity determines its filing requirements (see

CO 1.2) and whether to apply the legal entity approach (see

CO 2.1.1) or the management approach (see

CO 2.1.2), it is necessary to determine the assets, liabilities, and operations that will be included in the carve-out financial statements.

The basis of presentation should be disclosed in the carve-out financial statements. The financial statements should be appropriately titled as either consolidated or combined in accordance with

ASC 810-10-05,

ASC 810-10-55-1B, and

Regulation S-X Rule 3A-01 through

Regulation S-X Rule 3A-04 (for filings with the SEC). When the financial statements constitute a legal entity that has a controlling financial interest in all other entities included in the financial statements, the statements are referred to as consolidated financial statements.

Conversely, in a situation when there are multiple legal entities included in the financial statements, but they are not under the control of a single legal entity that is part of the carve-out financial statements, the financial statements will be referred to as combined. Combined financial statements may also be presented when assets and operations that represent components of multiple legal entities are presented, such as when a set of carve-out financial statements is required for a collection of product lines that are not manufactured by the same division of an organization.

Example CO 3-1 illustrates how the structure of a transaction influences whether the financial statements are labeled as consolidated or combined.

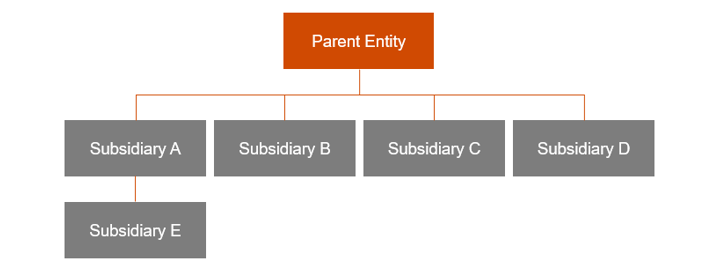

EXAMPLE CO 3-1

Divestiture scenario that results in preparation of combined financial statements

Parent Entity plans to sell Subsidiary A, Subsidiary B, and Subsidiary E to a buyer.

Should the carve-out financial statements be labeled as consolidated or combined?

Analysis

The financial statements should be labeled as combined. Consolidated financial statements are prepared on the basis of a controlling financial interest. Neither Subsidiary A nor Subsidiary B have a controlling financial interest in each other. Subsidiary A and Subsidiary B are sister entities. Financial statements are only labeled as consolidated when there is a parent-subsidiary relationship for all entities included in the financial statements. Although Subsidiary A and Subsidiary E have a parent-subsidiary relationship, because Subsidiary B is a sister entity, the financial statements should be labeled as combined. Financial statements cannot be labeled as both consolidated and combined.

If prior to the sale, Parent Entity created a newco and contributed Subsidiary A, Subsidiary B, and Subsidiary E to the newco, this would be a transaction of entities under common control. If newco’s financial statements include the period in which the newco was created, those financial statements would reflect the recapitalization retrospectively for all periods presented (i.e., as if the newco had always existed) and the financial statements would be labeled as consolidated.