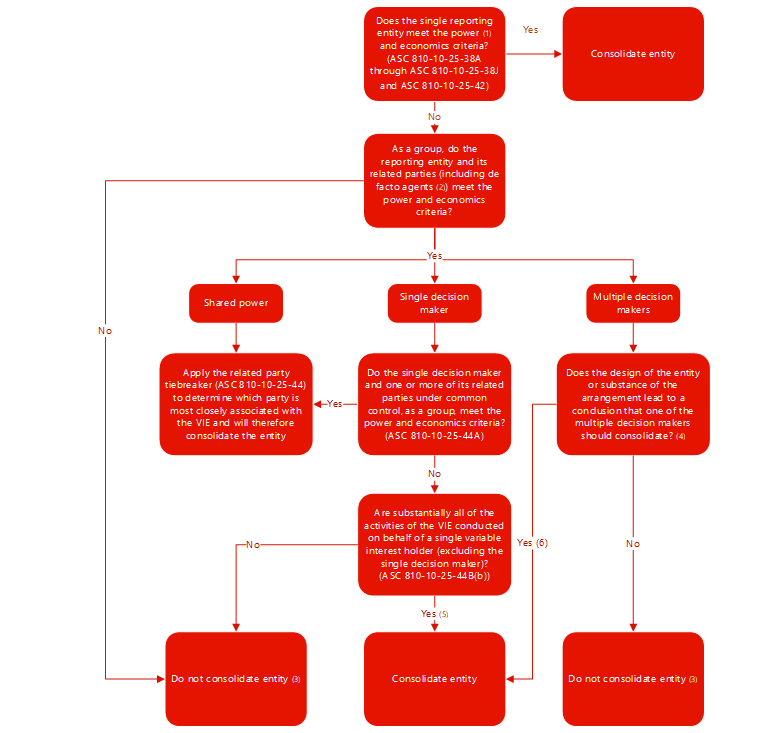

If the related party group has both characteristics of a primary beneficiary and is under common control, then the “related party tiebreaker” test should be performed to identify the variable interest holder within that related party group that is “most closely associated” with the VIE. The party that is most closely associated with the VIE should consolidate the VIE.

The term “common control” is not defined within U.S. GAAP.

ASU 2015-02’s basis for conclusions indicates that the FASB’s intent was for subsidiaries controlled (directly or indirectly) by a common parent, as well as a subsidiary and its parent, to be considered a common control group. When determining whether a related party group is under common control, we believe a parent entity should have a controlling financial interest over the related parties involved. A controlling financial interest is generally defined as ownership of a majority voting interest by one entity, directly or indirectly, or more than 50% of the outstanding voting shares of another entity, with certain exceptions. A controlling financial interest would also exist if the parent entity consolidates its subsidiaries based on the provisions in the VIE model. Refer to BCG 7 for further discussion related to common control transactions.

We do not believe the parent entity must be a legal entity for a common control group to exist. That is, a parent could be a natural person that holds a controlling financial interest in various entities.

Example CG 5-14 illustrates the determination of whether a commonly controlled related party group meets both characteristics of a primary beneficiary.

EXAMPLE CG 5-14

Determining whether a commonly controlled related party group meets both characteristics of a primary beneficiary

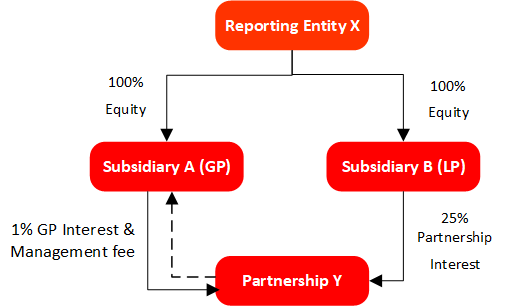

Subsidiary A and Subsidiary B are under common control of their parent, Reporting Entity X. Subsidiary A is the general partner and decision maker of Partnership Y, whereby it owns a 1% general partner interest and receives a management fee that is considered at market and commensurate. Subsidiary A does not hold any other interest in the partnership. Subsidiary B has 25% of the partnership’s limited partner interests. The other limited partner interests are held by unrelated parties. Neither Subsidiary A nor Subsidiary B has an interest in each other. As the limited partners do not have substantive kick-out or participating rights over the general partner, the Partnership is determined to be a VIE.

View image

View image

Does the commonly controlled related party group meet both characteristics of a primary beneficiary?

Analysis

Subsidiary analysis

No. Subsidiary A’s 1% general partner interest would not be considered more than insignificant and the management fee is at market and commensurate. Therefore, Subsidiary A does not have a variable interest in Partnership Y (unless it was determined that the partnership was structured to separate power and economics in an attempt to avoid consolidation). As a result, Subsidiary A is considered to be operating in an agency capacity and does not meet the power criterion. While Subsidiary B’s 25% limited partner interest is a potentially significant economic interest that would allow it to meet the losses/benefits criterion, neither subsidiary meets both criteria of a primary beneficiary on a stand-alone basis.

As Subsidiary A is acting in an agent capacity (i.e., it is not considered a decision maker), the related party group under common control would not meet the criteria in

ASC 810-10-25-44A in order to apply the related party tiebreaker test.

Further, unless “substantially all” of the partnership’s activities involve or are conducted on behalf of Subsidiary B, Subsidiary B would also not be required to consolidate the partnership under

ASC 810-10-25-44B.

While Subsidiary A’s decision-making fee is not considered a variable interest for the purposes of assessing whether Subsidiary A is the primary beneficiary, it still holds a variable interest in Partnership Y through its 1% general partner interest, and therefore both Subsidiary A and Subsidiary B should consider if they are required to make necessary VIE disclosures. See

FSP 18 for discussion on disclosures.

Parent analysis

Reporting Entity X, as a parent, meets both the power criterion (through Subsidiary A) and the losses/benefits criterion (through Subsidiary B), and therefore would be the primary beneficiary of Partnership Y and would consolidate Partnership Y in its consolidated financial statements.

View image

View image