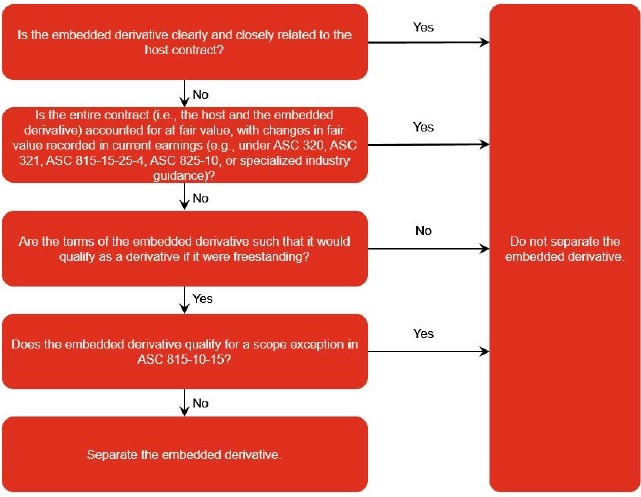

As described in

ASC 815-15-15-10, some foreign currency derivatives embedded in nonfinancial contracts do not have to be separated from their hosts.

ASC 815-15-15-10

An embedded foreign currency derivative shall not be separated from the host contract and considered a derivative instrument under 815-15-25-1 if all of the following criteria are met:

- The host contract is not a financial instrument.

- The host contract requires payment(s) denominated in any of the following currencies:

- The functional currency of any substantial party to that contract

- The currency in which the price of the related good or service that is acquired or delivered is routinely denominated in international commerce (for example, the U.S. dollar for crude oil transactions)

- The local currency of any substantial party to the contract

- The currency used by a substantial party to the contract as if it were the functional currency because the primary economic environment which the party operates is highly inflationary (as discussed in paragraph 830-10-45-11).

- Other aspects of the embedded foreign currency derivative are clearly and closely related to the host contract.

The evaluation of whether a contract qualifies for the exception in this paragraph should be performed only at inception of the contract.

ASC 815-15-15-11 clarifies that the determination of a counterparty’s functional currency should be made “based on available information and reasonable assumptions about the counterparty; representations from the counterparty are not required.” See

ASC 815-15-55-213 through

ASC 815-15-55-215 for a case study illustrating this determination.

ASC 830-10-55-5 provides guidance on economic factors that should be considered when determining the functional currency of a reporting entity. These include indicators relating to cash flows, sales prices, sales market, expenses, financing, and intra-entity transactions and arrangements. A reporting entity should not necessarily rely on a single indicator, such as the currency in which the counterparty’s sales prices are denominated; all relevant available information should be considered when determining the functional currency of a counterparty.

Question DH 4-6Is a guarantor considered a “substantial party to a contract” under

ASC 815-15-15-10?

PwC response

No. The implementation guidance in

ASC 815-15-55-84 through

ASC 815-15-55-86 clarifies that a guarantor is not a substantial party to a contract even if the guarantor is a related party (e.g., parent company). The evaluation of embedded derivatives should be conducted by the legal entity that is party to the contract.

Question DH 4-7

Does the fact that an index is quoted in a particular currency mean that it is routinely denominated in that currency? For example, if a coal index is quoted in US dollars, does that mean that coal is traded primarily in US dollars?

PwC response

No. This analysis will involve more than reviewing in what currency the product or service is typically quoted. Example 2 in

ASC 815-15-55-96 clarifies that the phrase “routinely denominated in international commerce” should be based on how similar transactions for certain products or services are structured around the world, not in just one local area. If similar transactions for a certain product or service are routinely denominated in international commerce in different currencies, the exception in

ASC 815-15-15-10 does not apply.

Question DH 4-8

A reporting entity concludes that changes in its operations will result in a change to its functional currency. Should the reporting entity reassess its existing contracts to determine if embedded derivative features should be separated?

PwC response

No.

ASC 815-15-15-10 states that the qualification for the scope exception should be performed only at the inception of the contract. Although the change in functional currency is significant, we do not believe it would require a reassessment of the contracts under

ASC 815-15-15-10.

Example DH 4-1, Example DH 4-2, and Example DH 4-3 illustrate the analysis for determining whether a contract contains an embedded foreign currency derivative.

EXAMPLE DH 4-1

Contract with payments linked to foreign-exchange rates

USA Corp is a US registrant that has a US dollar (USD) functional currency.

On August 1, 20X1, USA Corp enters into a contract for professional services denominated in USD. The terms of the contract require quarterly payments in USD. The contract also requires a fixed adjustment to the quarterly payment amount when the USD / Japanese yen (JPY) exchange rate reaches a specified level.

Is there an embedded foreign currency derivative that must be separated from the host contract?

Analysis

The contract payment adjustment is an embedded foreign currency derivative that should be separated from the professional services contract. Because the quarterly contract payments are not denominated in JPY (nor is it in substance JPY denominated), but are instead simply indexed to JPY, the embedded derivative does not qualify for the scope exception in

ASC 815-15-15-10.

EXAMPLE DH 4-2

Foreign currency denominated lease guaranteed by parent

USA Corp is a US registrant that has a USD functional currency. Deutsche AG is a consolidated subsidiary of USA Corp located in Germany, which has the euro as its functional currency.

Deutsche AG enters into a lease with Canadian Corp (which has a Canadian dollar functional currency), which requires annual lease payments in USD. USA Corp guarantees Deutsche AG’s payments on the lease.

Is there an embedded foreign currency derivative that must be separated from the host contract?

Analysis

The lease contains an embedded derivative that converts euro lease payments to USD that should be separated by Deutsche AG and in the consolidated financial statements of USA Corp. The substantial parties to the lease are Deutsche AG and Canadian Corp. Even though USA Corp guarantees the lease, it is not a substantial party to the contract. Since the lease payments are not denominated in one of the functional or local currencies of the substantial parties to the lease or a currency in which leases are routinely denominated in international commerce, the embedded derivative does not qualify for the scope exception in

ASC 815-15-15-10.

EXAMPLE DH 4-3

Commodity contract

USA Corp is a US registrant that has a USD functional currency.

USA Corp enters into a contract to purchase a commodity from Britannia PLC, which has a British pound sterling functional currency. The commodity purchase contract is denominated in euros.

The commodity underlying the contract is readily convertible to cash and USA Corp does not meet the requirements for applying the normal purchases and normal sales scope exception.

Is there an embedded foreign currency derivative that must be separated from the host contract?

Analysis

Since the commodity contract meets the definition of a derivative (because the underlying commodity is readily convertible to cash) and is not eligible for a scope exception, it should be accounted for as a derivative in its entirety. Therefore, there is no embedded foreign currency derivative to be separated; embedded derivatives are not separated from contracts that are accounted for as derivatives in their entirety.