Many multinational reporting entities conduct their currency hedging from a central treasury unit to reduce the cost of risk management and improve controls over derivative execution. After entering into derivative transactions with external counterparties, the central treasury unit will enter into an intercompany derivative to transfer the hedge to the operating entity with the risk to be hedged. To allow reporting entities that use a treasury center to comply with the

ASC 815-20-25-30(a) requirement that the operating entity with the foreign currency exposure be a party to the hedging instrument,

ASC 815 permits intercompany derivatives to be designated as the hedging instrument in a hedge of foreign currency risk in the consolidated financial statements of the reporting entity. Because this is an exception to the overall model, an intercompany derivative cannot be designated as the hedging instrument for hedges of risk other than foreign currency risk in the consolidated financial statements.

As discussed in

ASC 815-20-25-61, an intercompany derivative may be the hedging instrument in certain cash flow hedging relationships of foreign currency risk.

ASC 815-20-25-61

An internal derivative can be a hedging instrument in a foreign currency cash flow hedge of a forecasted borrowing, purchase, or sale or an unrecognized firm commitment in the consolidated financial statements only if both of the following conditions are satisfied:

- From the perspective of the member of the consolidated group using the derivative instrument as a hedging instrument (the hedging affiliate), the criteria for foreign currency cash flow hedge accounting otherwise specified in this Section are satisfied.

- The member of the consolidated group not using the derivative instrument as a hedging instrument (the issuing affiliate) either:

- Enters into a derivative instrument with an unrelated third party to offset the exposure that results from that internal derivative

- If the conditions in paragraphs 815-20-25-62 through 25-63 are met, enters into derivative instruments with unrelated third parties that would offset, on a net basis for each foreign currency, the foreign exchange risk arising from multiple internal derivative instruments. In complying with this guidance the issuing affiliate could enter into a third-party position with neither leg of the third-party position being the issuing affiliate’s functional currency to offset its exposure if the amount of the respective currencies of each leg are equivalent with respect to each other based on forward exchange rates.

Although the requirement that there be an intercompany derivative contract may seem a formality, it has important implications. For example, the gain or loss on the third-party hedging contract executed by the treasury center must be “pushed down” to the hedging unit (i.e., recorded in the foreign entity’s financial statements). The intercompany derivative does not eliminate in consolidation. At the treasury center, a gain from the external derivative gets offset by the loss from the intercompany derivative; at the hedging unit, the gain from the intercompany derivative is recorded and not eliminated in consolidation.

For purposes of separate, standalone company financial statements, an intercompany derivative between a subsidiary and a parent company (or another affiliated entity) would be sufficient to qualify for hedge accounting regardless of whether the parent company has entered into an offsetting contract with an outside party. An additional third-party contract is not needed in this circumstance, because a parent company is a party external to the reporting entity from the perspective of the subsidiary’s standalone financial statements.

Example DH 8-8 addresses treasury center hedging of foreign currency sales of members of a consolidated group.

EXAMPLE DH 8-8

Treasury center hedge of foreign-currency sales

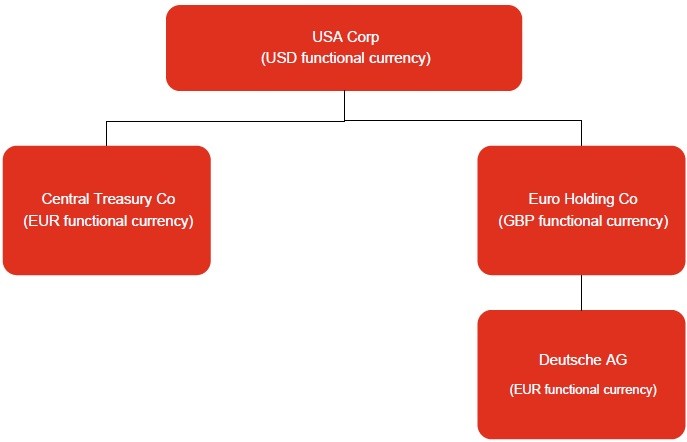

USA Corp is a US dollar (USD) functional currency reporting entity. USA Corp has a first-tier subsidiary (Euro Holding Co) in the United Kingdom that is a British pound sterling (GBP) functional currency entity. Euro Holding Co has a second-tier subsidiary (Deutsche AG) in Germany that is a euro (EUR) functional entity. USA Corp has another first-tier subsidiary (Central Treasury Co), which is a euro functional entity. The following diagram shows the organizational structure of USA Corp.

Central Treasury Co functions as a centralized treasury center for the consolidated group.

Deutsche AG forecasts USD sales and would like to enter into a foreign currency forward contract to deliver USD and receive EUR to hedge its exposure to USD.

Can Central Treasury Co execute a forward contract with an external party to deliver USD and receive EUR and designate it as a hedge of the foreign currency risk in Deutsche AG’s USD sales?

Analysis

Not without entering into an additional intercompany forward contract. Although Deutsche AG and Central Treasury Co are both euro-functional currency entities, Central Treasury Co cannot enter into a foreign currency hedging derivative on behalf of Deutsche AG because there is an intervening subsidiary that has a different functional currency (Euro Holding Co).

To qualify for hedge accounting, Central Treasury Co and Deutsche AG would have to enter into an intercompany forward contract under which Deutsche AG delivers USD and receives EUR and Central Treasury Co receives USD and delivers EUR. For Central Treasury Co, this intercompany forward will be offset by the forward contract that it enters into with the external party.

Deutsche AG would designate the intercompany derivative as the hedging instrument in a hedge of its USD sales. Central Treasury Co would carry both the intercompany derivative and the external forward contract at fair value through earnings (they should approximately offset each other). In the consolidated financial statements of USA Corp, the remaining hedging relationship would be Deutsche AG’s hedge of its foreign currency-denominated sales.